Chapter 13 – Inventory Management

CHAPTER 13

INVENTORY MANAGEMENT

Teaching Notes

This is a fairly long and important chapter. Important points are:

1. Good inventory management is important for successful organizations.

2. The key inventory management issues are when to order and how much to order.

3. Because all items are not of equal importance, it is necessary to establish a classification system

for allocating resources for inventory control.

4. EOQ models answer the question of how much to order. Variations of the basic EOQ model

include the quantity discount model and the economic production quantity (EPQ) model.

5. EOQ models tend to be rather robust: even though one or more of the parameters may be only

roughly correct, the model can yield a total cost that is close to the actual minimum.

6. ROP models are used to answer the question of when to order. Different models are used,

depending on whether demand, lead time, or both are variable.

7. Other models described are the fixed interval model and the single-period model.

8. All of the models in this chapter pertain to independent demand.

The single-period model is used to handle ordering of perishables (e.g., fresh fruits and vegetables,

seafood, and cut flowers) as well as items that have a limited useful life (e.g., newspapers and magazines).

Analysis of single-period situations generally focuses on two costs: shortage and excess. Shortage costs

may include a charge for loss of customer goodwill as well as the opportunity cost of lost sales or

unrealized profit per unit. Excess cost pertains to items left over at the end of the period and is the

difference between purchase cost and salvage value. There may be costs associated with disposing of

excess items, which would make the salvage value negative and hence increase the excess cost per unit.

Answers to Discussion and Review Questions

1. Inventories are held: (1) to meet anticipated customer demand, (2) to smooth production

2. Effective inventory management requires: (1) a system to keep track of inventory on hand and on

3. The four costs associated with inventories include the following:

(1) Purchase cost – Amount paid to a vendor or supplier to buy the inventory.

(2) Carrying or holding costs – Cost of physically having items in storage. Costs include interest,

insurance, taxes, depreciation, picking, and warehousing costs (heat, light, rent, and security).

13-3

Education.

11. Service level can be defined in a number of ways. The text focuses mainly on “the probability

that demand will not exceed supply during lead time, i.e., that the amount of stock on hand will

12. The A-B-C approach refers to the classification of inventory items according to some measure of

importance, usually annual dollar value, and allocating control efforts on that basis. Although

13. In effect, this situation is a “quantity discount” case with a time dimension. Hence, buying larger

quantities will result in lower annual purchase costs, lower ordering costs (due to fewer orders),

14. A decrease in setup time will cause a decrease in the numerator of the formula for the economic

run quantity (Economic Production Quantity). This will lead to a decrease in the economic run

15. The single-period model is used to handle ordering of perishables (e.g., fresh fruits, vegetables,

seafood, & cut flowers) and items that have a limited useful life (e.g., newspapers, magazines, &

16. The optimal stocking level can be less than the expected demand when excess costs are high and

shortage costs are low.

17. A company can reduce the need for inventories by:

a. using standardized parts for multiple products

b. improving demand forecasting

Taking Stock

1. a. If we buy additional amounts of a particular good to take advantage of quantity discounts,

then we will save money on purchasing cost per unit and annual purchasing costs of the item.

Chapter 13 – Inventory Management

b. If we treat holding cost as a percentage of the unit price, then as the unit price increases, so

will the holding cost. As a result, if we are using the EOQ approach, we will place smaller

process inventory, more efficient operations, improved customer service, and greater

assurance of material availability.

2. When making inventory decisions involving holding costs, setting inventory levels, and deciding

on quantity discount purchases, the materials manager, the plant manager, the production

3. Technology has had a tremendous impact on inventory management. The utilization of bar coding

and RFID tags has reduced the cost of taking physical inventory and has enabled real time

Critical Thinking Exercises

1. The expansion of menu offerings provides fast food companies with a competitive edge in terms

of improving customer satisfaction and service. However, it has also complicated inventory

management at a company. There are more ingredients and inventory items to order and to

2. A supermarket manager could evaluate criticalness of an inventory shortage by answering the

following questions:

a. How important is the item? For example, does it relate to a holiday or other important events,

e.g., a graduation?

b. Are comparable substitutes readily available within the manager’s supermarket?

c. What alternatives are available at other supermarkets?

d. Is this an occasional occurrence, or indicative of a larger, perhaps ongoing, problem?

3. The relevant considerations related to the purchase of stamps include:

a. How many stamps does he have now? Does he know how many he has? If so, how many?

b. What is his usage rate or current need for stamps?

c. What else does he need the cash for today?

13-5

Education.

4. Student answers will vary. Some possible answers are provided below:

a. Intentionally over-estimating or under-estimating any inventory costs would violate the

Virtue Principle.

b. If a buyer purchased two years’ worth of an item to decrease purchasing costs, this action

would violate the Utilitarian Principle due to the increase in carrying costs.

Chapter 13 – Inventory Management

13-6

Education.

Solutions

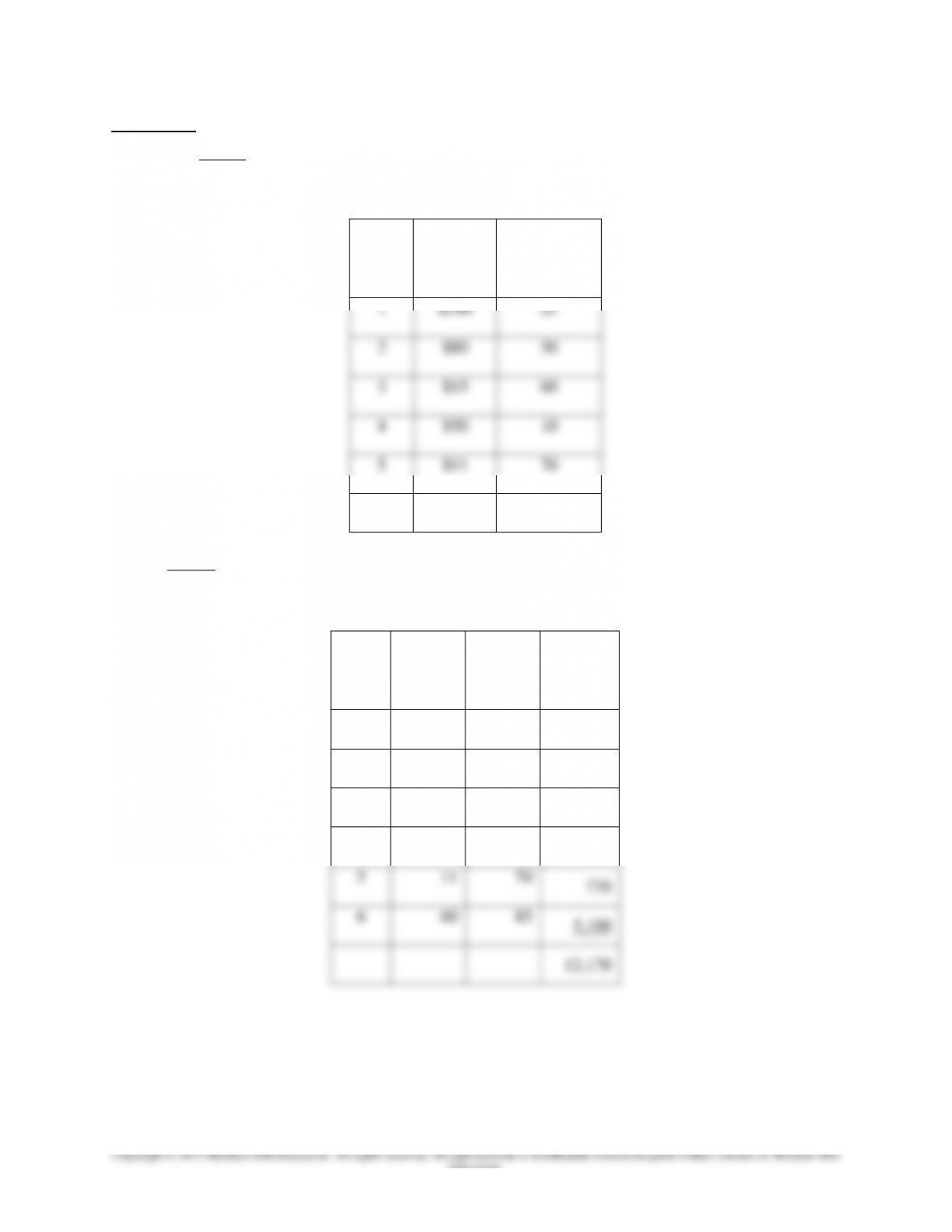

1. a. Given:

Determine an A-B-C classification for the following items:

Item

Unit

Cost

Annual

Volume

(00)

1

$100

25

2

$80

30

3

$15

60

4

$50

10

5

$11

70

6

$60

85

Step 1:

Determine the Annual Dollar Value (Unit Cost * Annual Volume) for each item and the sum of

the individual Annual Dollar Values.

Item

Unit

Cost

Annual

Volume

(00)

Annual

Dollar

Value

1

$100

25

$2,500

2

80

30

2,400

3

15

60

900

4

50

10

500

5

11

70

770

6

60

85

5,100

12,170

Chapter 13 – Inventory Management

13-7

Education.

Step 2:

Arrange the items in descending order based on Annual Dollar Values. Determine the A, B, and

C items. Then, determine the percentage of items and the percentage of Annual Dollar Value for

each category (round to two decimals).

Item

Annual

Dollar

Value

Category

Percentage of

Items

Percentage of Annual

Dollar Value

6

$5,100

A

16.67%

[(1/6)*100]

41.91%

[($5,100/$12,170)*100]

1

2,500

B

33.33%

[(2/6)*100]

40.26%

[($4,900/$12,170)*100]

2

2,400

3

900

C

50.00%

[(3/6)*100]

17.83%

[($2,170/$12,170)*100]

5

770

4

500

12,170

100.00%

100.00%

b. Given:

D = 4,500, S = $36, and H = $10.

10

0 H

c. Given:

D = 18,000/year, S = $100, H = $40 per unit per year, p = 120 units per day, and u = 90

units/day.

Find the economic production quantity (EPQ) (round to an integer value):

Chapter 13 – Inventory Management

13-8

Education.

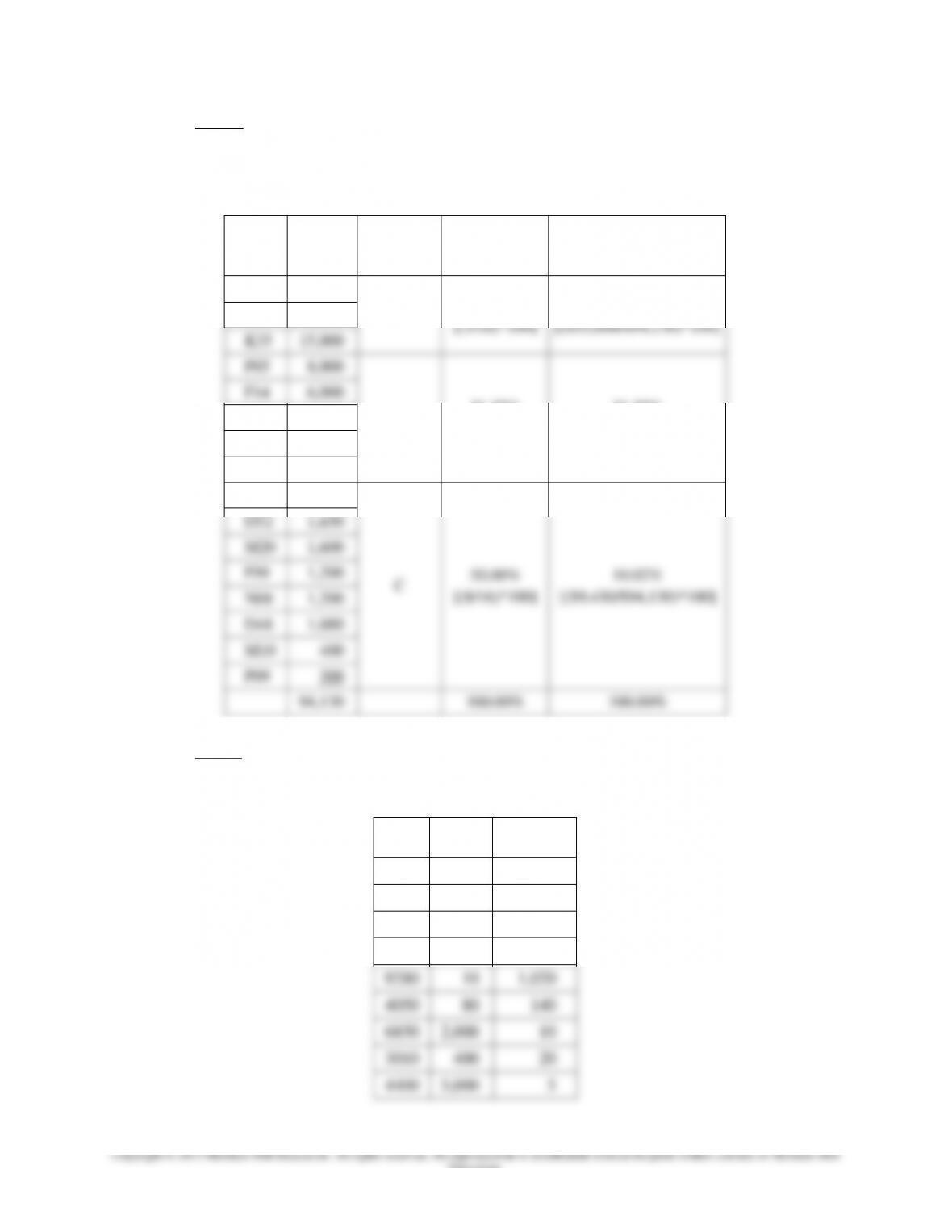

2. a. Given:

The following table contains figures on the monthly volume and unit costs for a random

sample of 16 items. Develop an A-B-C classification for these items:

Item

Unit Cost

Usage

K34

$10

200

K35

25

600

K36

36

150

M10

16

25

M20

20

80

Z45

80

200

F14

20

300

F95

30

800

F99

20

60

D45

10

550

D48

12

90

D52

15

110

D57

40

120

N08

30

40

P05

16

500

P09

10

30

Chapter 13 – Inventory Management

Step 1:

Determine the Annual Dollar Value (Unit Cost * Usage) for each item and the sum of the

individual Annual Dollar Values.

Item

Unit Cost

Usage

Annual

Dollar

Value

K34

$10

200

$2,000

K35

25

600

15,000

K36

36

150

5,400

M10

16

25

400

M20

20

80

1,600

Z45

80

200

16,000

F14

20

300

6,000

F95

30

800

24,000

F99

20

60

1,200

D45

10

550

5,500

D48

12

90

1,080

D52

15

110

1,650

D57

40

120

4,800

N08

30

40

1,200

P05

16

500

8,000

P09

10

30

300

94,130

Chapter 13 – Inventory Management

Education.

Step 2:

Arrange the items in descending order based on Annual Dollar Values. Determine the A, B,

and C items. Then, determine the percentage of items and the percentage of Annual Dollar

Value for each category (round to two decimals).

Item

Annual

Dollar

Value

Category

Percentage of

Items

Percentage of Annual

Dollar Value

F95

$24,000

A

18.75%

[(3/16)*100]

54.83%

[($55,000/$94,130)*100]

Z45

16,000

K35

15,000

P05

8,000

B

31.25%

[(5/16)*100]

31.55%

[($29,700/$94,130)*100]

F14

6,000

D45

5,500

K36

5,400

D57

4,800

K34

2,000

C

50.00%

[(8/16)*100]

10.02%

[($9,430/$94,130)*100]

D52

1,650

M20

1,600

F99

1,200

N08

1,200

D48

1,080

M10

400

P09

300

94,130

100.00%

100.00%

b. Given:

Determine an A-B-C classification for the following items:

Item

Usage

Unit Cost

4021

90

$1,400

9402

300

12

4066

30

700

6500

150

20

9280

10

1,020

4050

80

140

6850

2,000

10

3010

400

20

4400

5,000

5