Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-1

CHAPTER 20: MANAGEMENT COMPENSATION, BUSINESS

ANALYSIS, AND BUSINESS VALUATION

QUESTIONS

20-1 The key objective of the firm is to develop management compensation plans that

support the firm’s strategic objectives:

1. To motivate managers to exert a high level of effort to achieve the firm’s goal.

and for the effectiveness of their decision making.

20-2 Management compensation includes one or more of the following: salary, bonus,

and benefits or perquisites (“perks”).

Salary is a fixed payment, while a bonus is based upon the achievement

of performance goals for the period. Perks include special services and benefits

20-3 Risk aversion is the tendency to prefer decisions with assured outcomes over

those with uncertain outcomes. It is a relatively common decision-making

characteristic of managers. A risk-averse manager is biased against decisions

that have an uncertain outcome, even if the expected outcome is favorable. The

risk-averse manager prefers choices with certain outcomes to choices with more

favorable outcomes which are not certain. The effect is that certain decisions that

earnings per share).

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-2

20-4 Management compensation plans designed to motivate managers can have

undesired unethical effects. The presence of very strong motivation due to a

compensation plan, without compensating accounting controls designed to detect

20-5 From a financial reporting standpoint, the most desirable form of compensation is

deferred payment plans, which delay the expense on the income statement.

20-6 From the standpoint of taxes paid by the individual manager, the least desirable

forms of compensation are ones which have immediate tax consequences.

These include salary increases and cash bonuses. The most desirable form of

purposes.

20-7 The three bases for incentive bonus plans are stock price, a strategic

performance measurement systems (cost, revenue, profit, or investment center),

and the balanced scorecard. See Exhibit below:

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-3

Advantages and Disadvantages of Bonus Compensation Bases

Bonus Base

Motivation

Right Decision

Fairness

Stock Price

(+/-) depends on

whether stock and

stock options are

included in base pay

and/or bonus

(+) aligns

management

compensation with

short-term

shareholder interests

(+) consistent with

shareholder’s

interests

(-) lack of

controllability

Strategic

Performance

Measures (cost,

revenue, profit,

and investment

center)

(+) strongly motivating

if non-controllable

factors are excluded

(+) generally a good

measure of

economic

performance

(-) typically has only

a short term focus

(-) if bonus is very

high, can cause

inaccurate reporting

(+) intuitive, clear,

and easily

understood

(-) measurement

issues: differences

in accounting

conventions, cost

allocation methods,

financing methods,

etc.

Balanced

Scorecard:

Critical Success

Factors

(+) strongly

motivating if non-

controllable factors

are excluded

(+) aligns

management interest

with long-term

shareholder interests

(+) consistent with

management’s

strategy

(-) may be subject to

inaccurate reporting,

as for responsibility

accounting

measures

(+) if carefully

defined and

measured, CSFs

are likely to be

perceived as fair

(-) potential

measurement

issues, as for

responsibility

accounting

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-8 The six financial ratios used in the evaluation of liquidity are:

The first and second ratios are the accounts receivable and inventory

turnover ratios which measure the firm’s ability to manage two important

elements of current assets - accounts receivable and inventory. The lower the

balance in these accounts relative to sales, the less cash will be tied up in these

liabilities)

The sixth measure, free cash flow ratio (net free cash flow divided by

current liabilities) measures the effect of the firm’s free cash flow on liquidity.

20-9 The two types of bonus pools are unit-based and firm-wide. The unit-based is

determined from earnings in the unit only, while the firm-wide pool is determined

from the earnings of the aggregate firm. See below:

Advantages and Disadvantages of Different Bonus Pools

Motivation

Right Decision

Fairness

Unit-Based

(+) strong

motivation for an

effective

manager⎯ the

upside potential

(-) unmotivating for

manager of

economically

weaker units

(-) provides the

incentive for

individual managers

not to cooperate

with and support

other units, when

needed for the

good of the firm

(-) does not

separate the

performance of the

unit from the

manager’s

performance

Firm-Wide

(+) to attract

and retain good

managers

throughout the firm,

even in

economically

weaker units

(+) effort for the

good of the overall

firm is rewarded -

motivates teamwork

and sharing of

assets, etc, among

units

(+) separates the

performance of the

manager from that

of the unit

(+) can ap pear to

be more fair to

shareholders and

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

Key: (+) means the pool has a positive effect on the objective;

(-) means the pool has a negative effect on the objective.

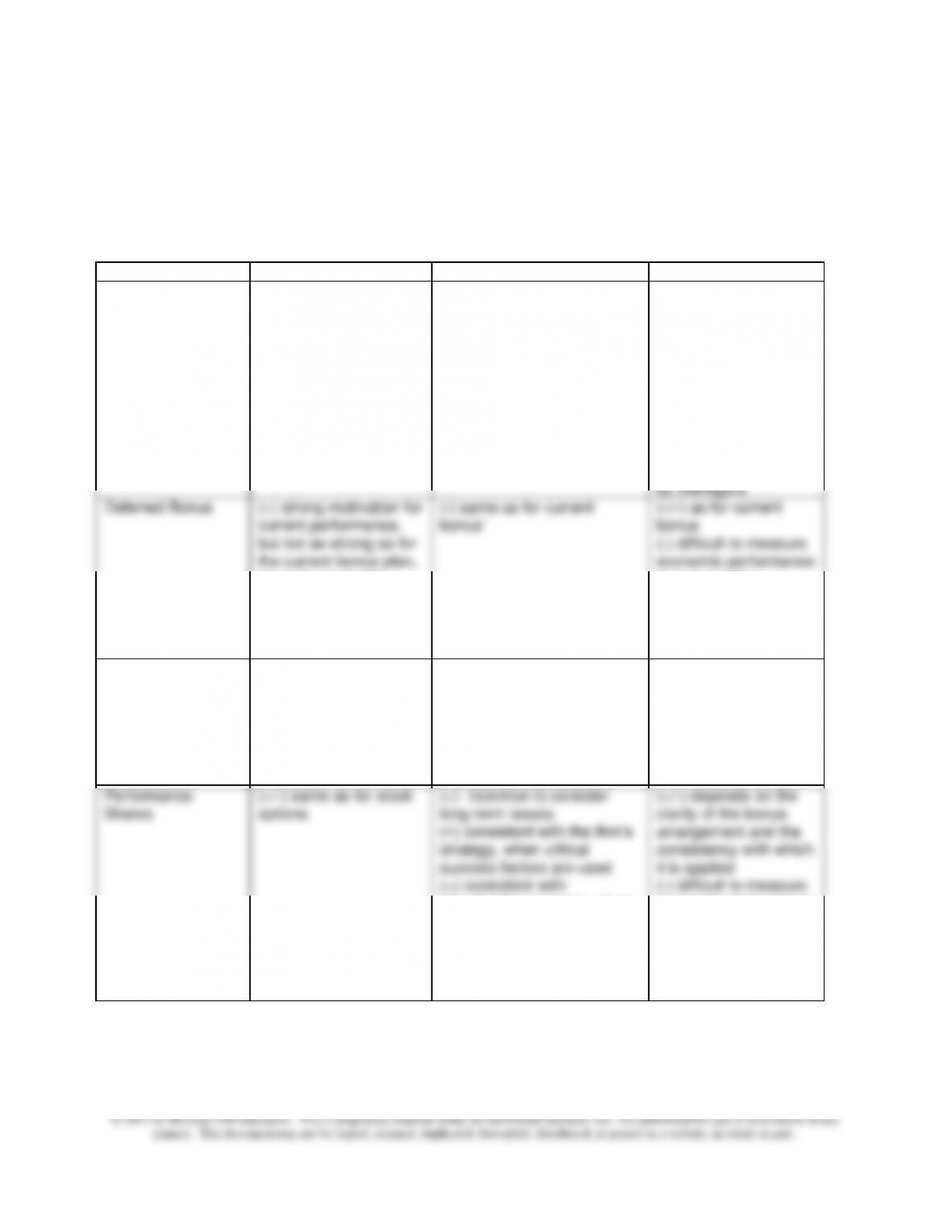

20-10 The four types of bonus payment options are current cash bonus, deferred

bonus, stock options, and performance shares. See Exhibit below:

Advantages and Disadvantages of Different Bonus Payment Options

Motivation

Right Decision

Fairness

Current Bonus

(+) strong motivation for

current performance;

stronger motivation

than for deferred plans

(-) short term focus

(-) risk averse manager

avoids risky but potentially

beneficial projects

(+/-)depends on the

clarity of the bonus

arrangement and the

consistency with which

it is applied

(-) difficult to measure

economic performance

in one or a few

financial measures

(-) simple measures

are easily manipulated

by managers

Deferred Bonus

(+) strong motivation for

current performance,

but not as strong as for

the current bonus plan,

since the reward is

delayed

(+) tax advantages of

deferred compensation

(-) same as for current

bonus`

(+/-) as for current

bonus

(-) difficult to measure

economic performance

in one or a few

financial measures

(-) simple measures

are easily manipulated

by managers

Stock Options

(+) unlimited upside

potential is highly

motivating

(-) delay in reward

reduces motivation

somewhat

(+) incentive to consider

longer term issues

(+) provides better risk

incentives than for current or

deferred bonus plans

(+) consistent with

shareholder interests

(+/-) as above, plus

(-) uncontrollable

factors affect stock

price

Performance

Shares

(+/-) same as for stock

options

(+) incentive to consider

long-term issues

(+) consistent with the firm’s

strategy, when critical

success factors are used

(+) consistent with

shareholder interests, when

earnings per share is used

(+/-) depends on the

clarity of the bonus

arrangement and the

consistency with which

it is applied

(-) difficult to measure

economic performance

in one or a few

financial measures

(-) simple measures

are easily manipulated

by managers

Key: (+) means the payment option has a positive effect on the objective;

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-6

20-11 This question is intended for class discussion. There are a number of possible

views on this question. The goal of the discussion should not be to determine

the equity of a certain level of executive pay, but rather to show the ethical issue

20-12 The five methods discussed in the chapter for directly measuring the value of a

firm: book value of equity, market value of equity (market capitalization), the

discounted cash flow method, multiples-based valuation, and enterprise value.

The book value method takes the amount of equity from the balance

sheet.

The market value method is the most simple and direct. The value of the

firm is determined from the number of outstanding shares multiplied by the

current market price of the shares.

The discounted cash flow (DCF) method develops the value of the firm as

the discounted present value of the firm’s net free cash flows. It has the

earnings ratios of the stocks of comparable publicly-held firms, and then adjusted

for discounting. The earnings multiplier has important limitations. It is based on

accounting earnings, and is therefore subject to the limitations of accounting

earnings. The advantage is that the earnings multiplier is easy to apply.

two or more of the valuation techniques and to evaluate the assumption in each

in order to arrive at an overall valuation assessment.

20-13 Bonuses are the fastest growing part of total compensation. The growth of

interest in bonus plans is likely the result of firms’ increasing competition for the

very best executive talent. Also, shareholders prefer bonus plans to other forms

20-7

20-14 The goal of strategic cost management is the success of the firm in maintaining

competitive advantage, so it is important to evaluate the overall performance of

20-15 The firm’s strategy changes as its product(s) move through the different phases

of the sales life cycle - product introduction, growth, maturity, and decline (the

sales life cycle is covered in Chapter 13). As a firm’s product moves from the

growth phase to the maturity phase, the firm’s strategy also moves from product

Compensation Plans Tailored for Different Strategic Conditions

Product Sales Life

Cycle Phase

Compensation Plan

Salary

Bonus

Benefits

First: Product

Introduction

High

Low

Low

Second: Growth

Low

High

Competitive

Third: Maturity

Competitive

Competitive

Competitive

Fourth: Decline

High

Low

Competitive

Key to Exhibit: “Competitive” lies between low and high.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-8

BRIEF EXERCISES

20-16

Inventory Turnover = _Cost of Good Sold_

Average Inventory

= ______$400,000______

= 111%

20-17

Market Value of Equity = Stock Price x # Shares Outstanding

20-18

Economic Value Added = EVA-based Net Income –

Cost of Capital x EVA-based Invested Capital

= $125,000

20-19

DCF Value = PV of cash flows + marketable securities – market value of debt

20-20

Multiples-Based Valuation = Earnings Multiplier x Earnings

20-21

Gross Profit Margin = _Gross Profit_

Net Sales

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-9

EXERCISES

20-22 Compensation, Strategy, and Market Value (20 min)

Jackson Supply is experiencing the anomaly of achieving its strategic

goals (customer service) while the stock price is falling relative to

competitors. Two questions arise:

1. Is the firm properly measuring customer service? Perhaps

more direct and effective measures are needed.

2. It may be that investors do not value the firm’s customer

service goals. The investors may be looking for cost reduction, for

production diversification and innovation, supply-chain management

innovation, or other strategic initiatives. What are competitors doing?

The firm might benefit from consulting with industry experts or

financial analysts that specialize in medical supply. In the end,

Jackson Supply must realize that its ultimate strategy must be to

satisfy shareholders, and the specific goals that are chosen, such as

customer service, must be linked to that strategy. Success is judged

by investors and not by top management.

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-10

20-23 Evaluating an Incentive Pay Plan; Strategy (15 min)

Unless Fox is rewarded significantly by the boat manufacturers for

volume of sales, the current incentive plan is likely to reduce profits

by increasing sales at the expense of profit margins. Sales

representatives’ incentives are to sell as many boats as possible, and

since reducing the price will help them to achieve this goal, they are

likely to sell many boats at low prices. A better approach would be to

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-11

20-24 Alternative Compensation Plans (20 min)

1. On the negative side, stock option incentives tied to share

prices are influenced by the broad economic factors affecting the

stock market, many of which are uncontrollable by the managers.

On the plus, the use of stock options can effectively align the

managers’ incentives and efforts with those of the shareholders,

who value the increase in stock price. Whatever efforts the manger

can make to increase stock price will be rewarded.

EPS, ROI, and return on equity can be influenced by executives’

efforts and are therefore useful as motivational tools. The use of a

stock option plan often indicates that the firm’s strategy includes

plans for growth; executives expect that the firm’s growth will make

the options valuable in the coming years.

2. Plans based on EPS:

a. have a short-term focus, so that managers tend to

maximize short term earnings and not take actions which will in

the long-term benefit the company.

b. if the bonus incentive is very high, a focus on EPS can

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-12

20-25 Performance Evaluation and Risk Aversion (20 min)

1. A flat salary with a bonus based on number of processed

applications would be best. The flat salary reduces Lewis’ risk level

because it insulates her from the uncertainty of a fluctuating

2. Emphasis will be placed on volume with less attention given to the

quality of the processing. Jill should be giving attention to both the

3. Some possible measures include:

1. A measure based on the number of complaints or due to

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-13

20-26 Performance Evaluation and Risk Aversion (20 min)

1. Compensation for Amy should be the ROI-based bonus since she

is risk neutral. Amy would accept some risk to increase profit for

2. ROI is not a good evaluation standard for Amy because she has no

role in investing decisions. Return on sales would perhaps be a

better measure. This would emphasize sales margins as opposed to

3. a. Yes, this is a fair performance evaluation method. Since

Stiles Furniture is in a similar environment with the same capabilities

as NightTime, then Stiles will be affected by the same business and

capabilities. If Stiles is more successful with an alternative strategy,

then Amy should be held responsible for not altering her strategy as

well.

b. The advantage to residual income is that it will motivate Amy

to invest in all projects which earn over a threshold return. If Amy’s

division is earning a high ROI, and management is concerned that

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-14

20-27 Bonus Compensation Base and Pool (20 min)

This question is intended primarily for class discussion, and there are a

variety of possible responses. A suggested approach follows.

1. Alternative bonus compensation bases include the SBU responsibility

center measures (cost center, profit center, revenue center, and

investment center) as well as a potential wide variety of nonfinancial

measures.

2. The use of revenues will probably have an upward bias on bonuses,

at least at financial service companies in recent years. The reason is

that revenue has grown faster than profits for these firms in recent

years. The Wall Street Journal estimates that bonuses in 2013

be multi-dimensioned, including profits, sales growth, and other

measures of financial and operating performance.

3. The use of a firm-wide bonus pool likely makes sense in the financial

services industry, since the firms have highly integrated operations.

Firms in other industries, such as consumer products, might find a

Chapter 20 - Management Compensation, Business Analysis, and Business Valuation

20-15

20-27 (continued -1)

4. The revenue-based method is not fair if you are considering the

shareholder point of view. The reason is noted in part 2 above;

shareholders are likely to place a higher value on earnings and cash

flow as opposed to revenue growth only. Considering the fairness of

Source: Liz Rappaport, Aaron Lucchetti, and Stephen Grocer, “Wall Street

Pay: A Record $144 Billion,” The Wall Street Journal, October 12, 2010,

p. C1; Joe Nocera, “Corzine Crashes Like It’s 2008,” The New York Times,

November 1, 2011, p. A21.