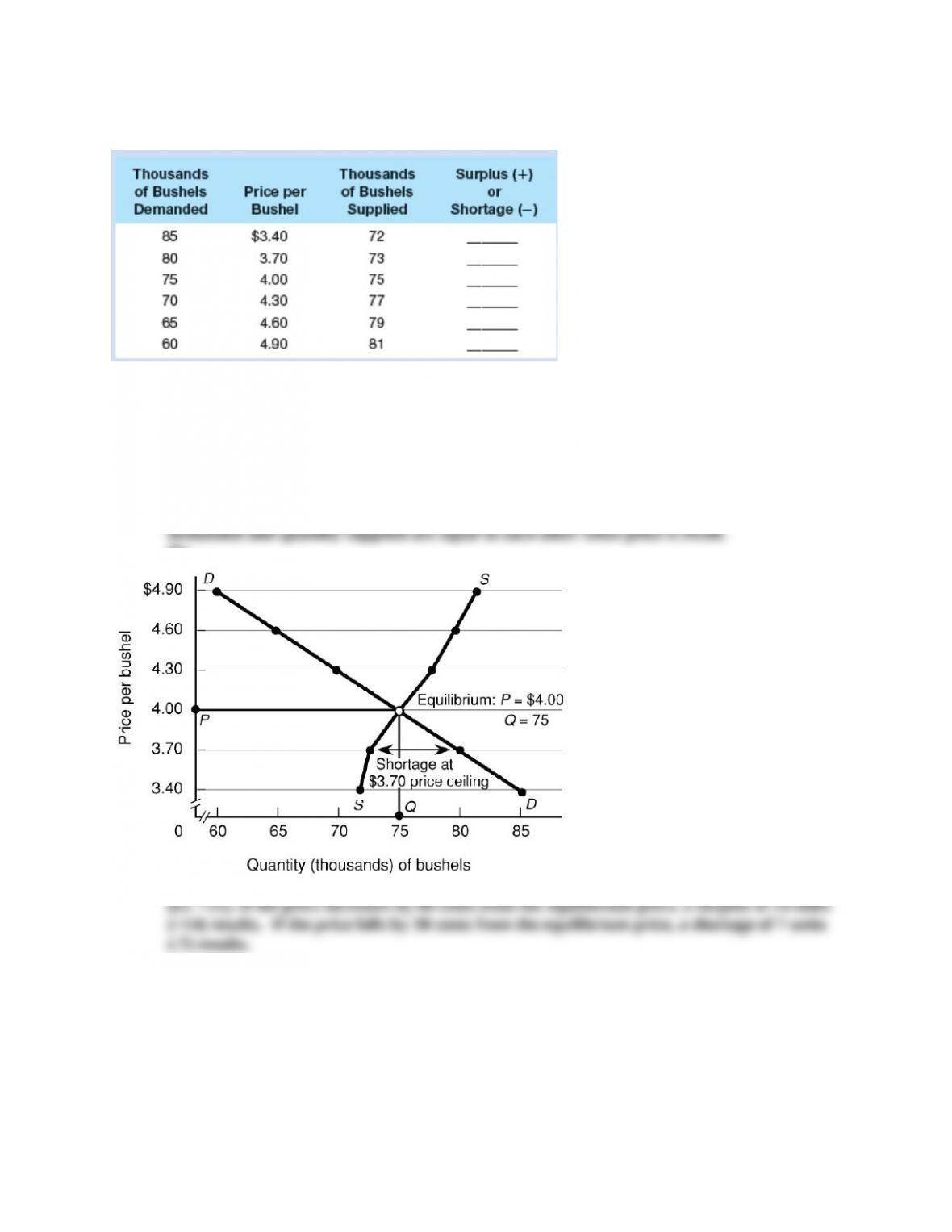

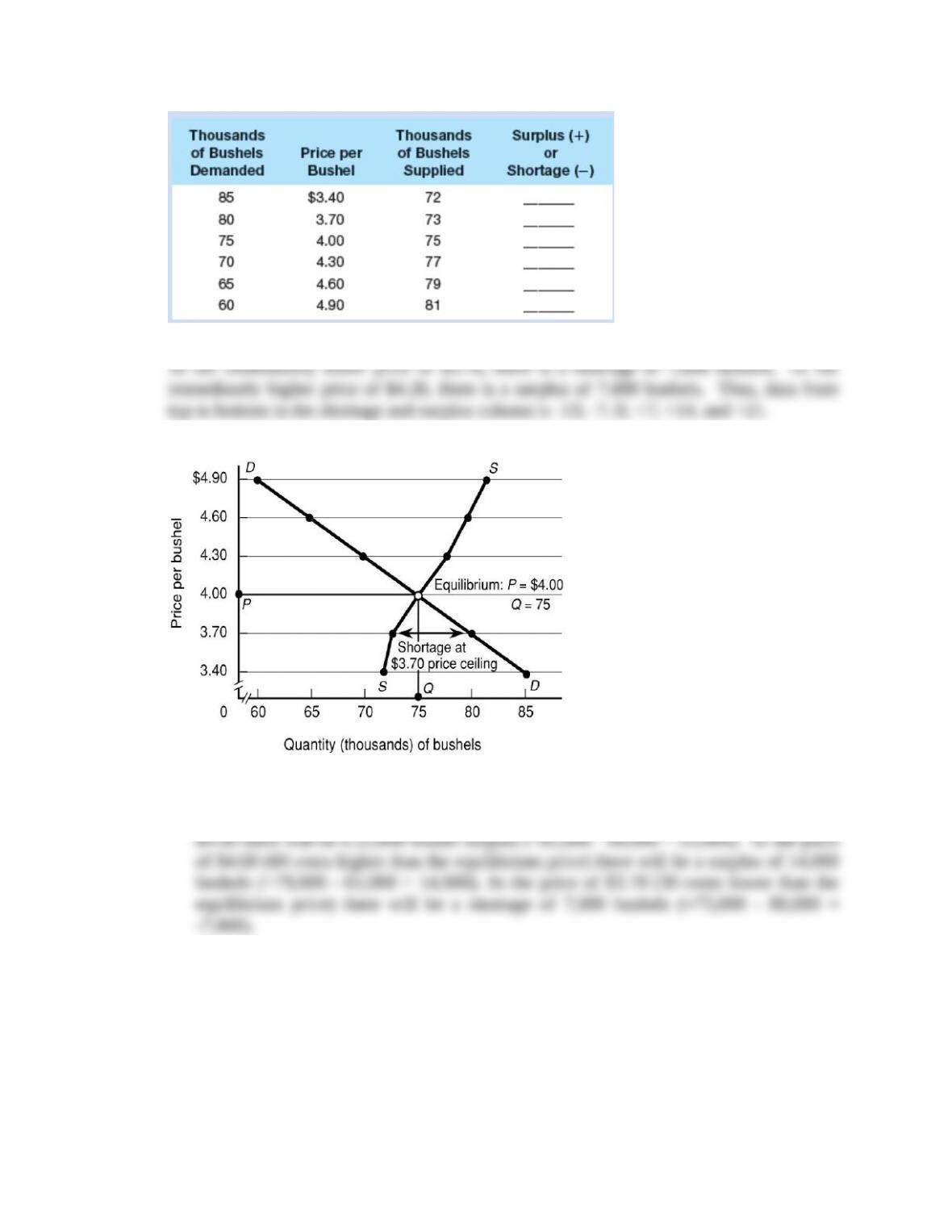

3. Refer to the expanded table below from review question 8. LO4

a. What is the equilibrium price? At what price is there neither a shortage nor a surplus? Fill in the

surplus-shortage column and use it to confirm your answers.

b. Graph the demand for wheat and the supply of wheat. Be sure to label the axes of your graph correctly.

Label equilibrium price P and equilibrium quantity Q.

c. How big is the surplus or shortage at $3.40? At $4.90? How big a surplus or shortage results if the

price is 60 cents higher than the equilibrium price? 30 cents lower than the equilibrium price?

Answers:

(a) Equilibrium price = $4.00. There is neither a shortage nor a surplus at $4.00. Quantity

(b)

(c) At $3.40, there is a shortage of 13 units (i.e., -13). At $4.90, there is a surplus of 21 units

Feedback: Consider the following data.

(a) Pe = $4.00. Equilibrium occurs where there is neither a shortage nor surplus of wheat.

(b)

(c) Note: shortages will be negative and surpluses will be positive. At the price $3.40

there will be a 13,000 bushel shortage (= 72,000 – 85,000 = -13,000). At the price of

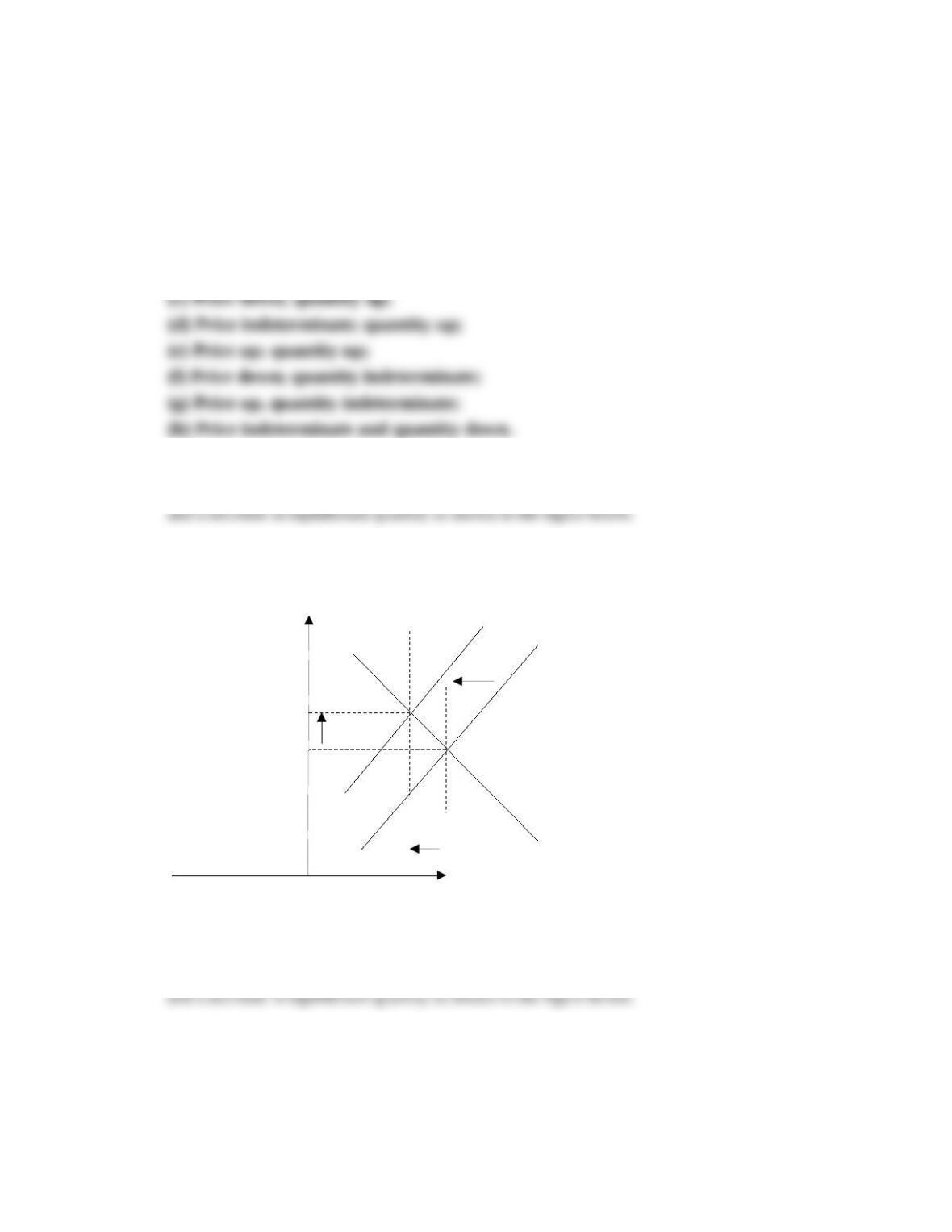

4. How will each of the following changes in demand and/or supply affect equilibrium price and

equilibrium quantity in a competitive market; that is, do price and quantity rise, fall, or remain

unchanged, or are the answers indeterminate because they depend on the magnitudes of the shifts? Use

supply and demand to verify your answers. LO5

a. Supply decreases and demand is constant.

b. Demand decreases and supply is constant.

c. Supply increases and demand is constant.

Price

Quantity

S2 S1

D1

P1

Q1

P2

Q2

d. Demand increases and supply increases.

e. Demand increases and supply is constant.

f. Supply increases and demand decreases.

g. Demand increases and supply decreases.

h. Demand decreases and supply decreases.

Answers:

(a) Price up; quantity down;

(b) Price down; quantity down;

Feedback:

Part a: The decrease in supply with a constant demand results in an increase in equilibrium price

Part b: The decrease in demand with a constant supply results in a decrease in equilibrium price

Price

Quantity

S1

D1

P1

Q1

P2

Q2

D2

Price

Quantity

S2

S1

D1

P1

Q1

P2

Q2

Part c: The increase in supply with a constant demand results in a decrease in equilibrium price

Part d: The increase in supply and the increase in demand unambiguously increases the

equilibrium quantity. This is because the increase in supply and the increase in demand both

Price

Quantity

S2

S1

D1

P1

Q1

P2

Q2

D2

Price

Quantity

S1

D1

P1

Q1

P2

Q2

D2

Part e: The increase in demand with a constant supply results in an increase in equilibrium price

Part f: The increase in supply and the decrease in demand unambiguously decreases the

Price

Quantity

S2

S1

D1

P1

Q1

P2

Q2

D2

Price

Quantity

S2

S1

D1

P1

Q1

P2

Q2

D2

Part g: The decrease in supply and the increase in demand unambiguously increases the

equilibrium price. This is because the decrease in supply and the increase in demand both put

Part h: The decrease in supply and the decrease in demand unambiguously decreases the

Price

Quantity

S2

S1

D1

P1

Q1

P2

Q2

D2

5. Use two market diagrams to explain how an increase in state subsidies to public colleges might affect

tuition and enrollments in both public and private colleges. LO5

Answer: The supply curve of the public colleges shifts to the right, reducing tuition and

Feedback: Consider the case of subsidies to public colleges. The state subsidies to public

colleges shift the supply curve of the public colleges to the right, thus reducing tuition

Now consider a tax on private colleges. This will reduce the supply of private colleges

(shift the private college supply schedule to the left). This will increase demand at public

6. ADVANCED ANALYSIS Assume that demand for a commodity is represented by the equation P = 10

– .2Qd and supply by the equation P = 2 + .2Qs, where Qd and Qs are quantity demanded and quantity

supplied, respectively, and P is price. Using the equilibrium condition Qs = Qd, solve the equations to

determine equilibrium price. Now determine equilibrium quantity. LO5

Feedback: Consider the following equations:

To solve this system of equations we use the fact that the equilibrium price in both equations must

be the same. Therefore we can equate the two (eliminate P from the system).

We now use the equilibrium condition for quantity: Qs = Qd= Q

We substitute Q for Qd and Qs

To find the equilibrium price we substitute the equilibrium quantity Q = 20 into either the demand

function or supply function.

Obviously the answers are the same; this is the equilibrium price, or P = 6.

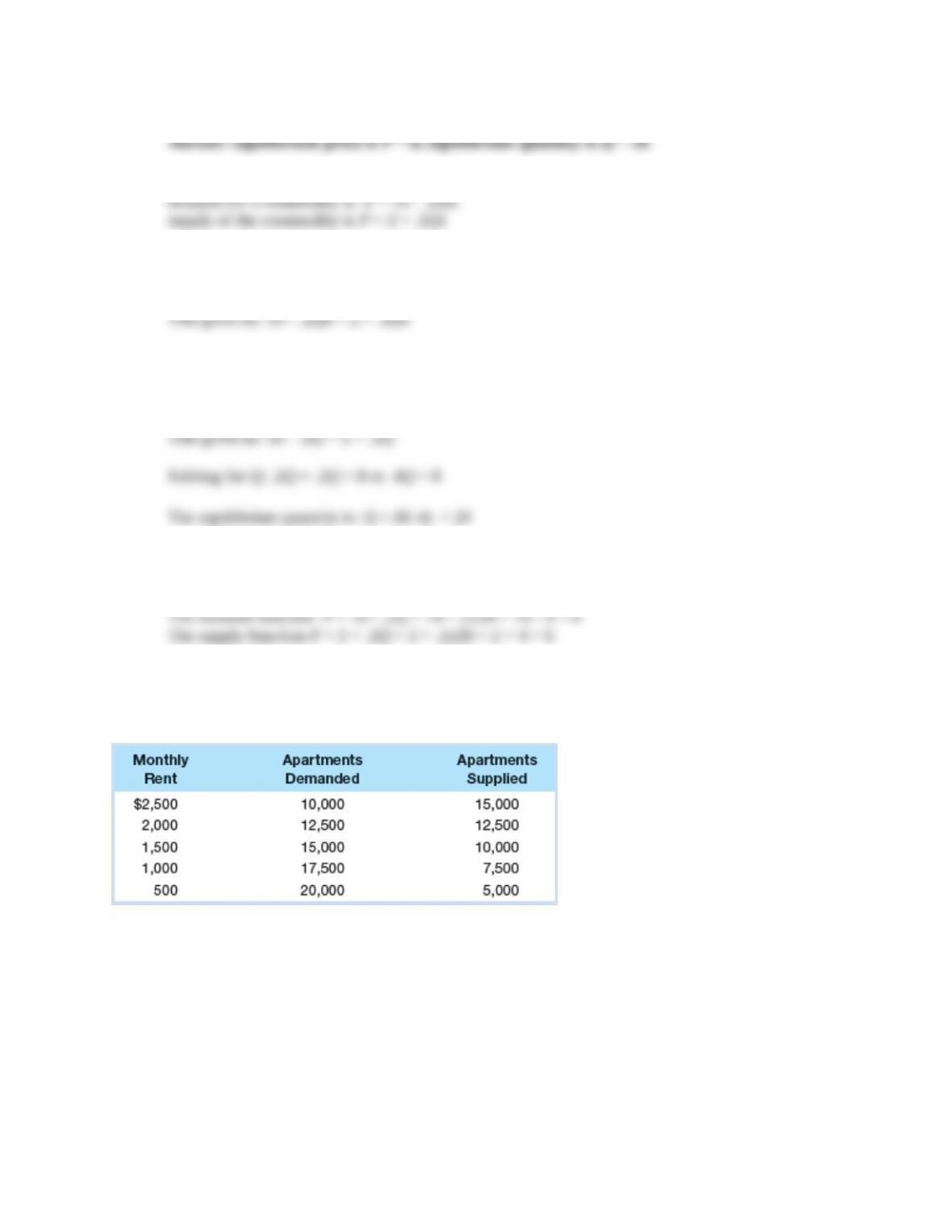

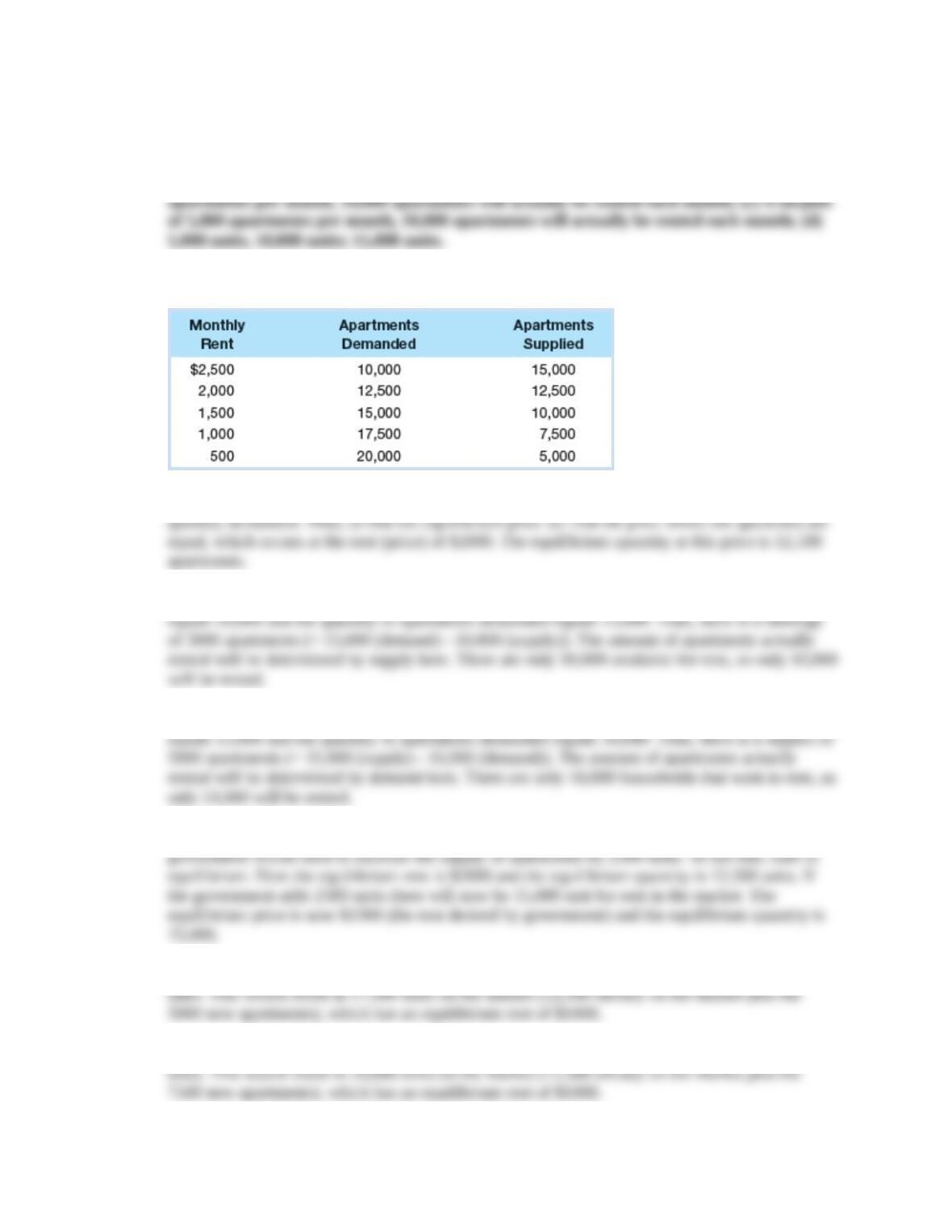

7. Suppose that the demand and supply schedules for rental apartments in the city of Gotham are as given

in the table below. LO6

a. What is the market equilibrium rental price per month and the market equilibrium number of

apartments demanded and supplied?

b. If the local government can enforce a rent-control law that sets the maximum monthly rent at $1,500,

will there be a surplus or a shortage? Of how many units? And how many units will actually be rented

each month?

c. Suppose that a new government is elected that wants to keep out the poor. It declares that the minimum

rent that can be charged is $2,500 per month. If the government can enforce that price floor, will there be

a surplus or a shortage? Of how many units? And how many units will actually be rented each month?

d. Suppose that the government wishes to decrease the market equilibrium monthly rent by increasing the

supply of housing. Assuming that demand remains unchanged, by how many units of housing would the

government have to increase the supply of housing in order to get the market equilibrium rental price to

fall to $1,500 per month? To $1,000 per month? To $500 per month?

Answers: (a) 12,500 apartments at a rent of $2000 per month; (b) A shortage of 5,000

Feedback: Consider the following demand and supply schedules:

Part a: The market equilibrium price is determined by the relationship quantity supplied equals

Part b: If the government imposes a maximum rent of $1500 the quantity of apartments supplied

Part c: If the government imposes a minimum rent of $2500 the quantity of apartments supplied

Part d: If the government wants to reduce the market equilibrium rent to $1500 per month the

If the government wanted to reduce the equilibrium rent to $1000 they would need to add 5000

If the government wanted to reduce the equilibrium rent to $500 they would need to add 7500