Chapter 16 – Interest Rates and Monetary Policy

PROBLEMS

1. Assume that the following data characterize the hypothetical economy of Trance: money

supply = $200 billion; quantity of money demanded for transactions = $150 billion; quantity of

money demanded as an asset = $10 billion at 12 percent interest, increasing by $10 billion for

each 2-percentage-point fall in the interest rate. LO1

a. What is the equilibrium interest rate in Trance?

b. At the equilibrium interest rate, what are the quantity of money supplied, the total quantity of

money demanded, the amount of money demanded for transactions, and the amount of money

demanded as an asset in Trance?

Answer: (a) 4%

Feedback:

Part a:

To answer this part of the question we use the table below. The first column is the interest

Interest Rate Asset Demand

for Money

Transactions

Demand

Combined

Demand for

Money

Money Supply

12% 10 150 160 200

We find the equilibrium interest rate by equating the quantity supplied with the quantity

Part b:

It also follows from the answer above that the equilibrium quantity of money supplied is

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

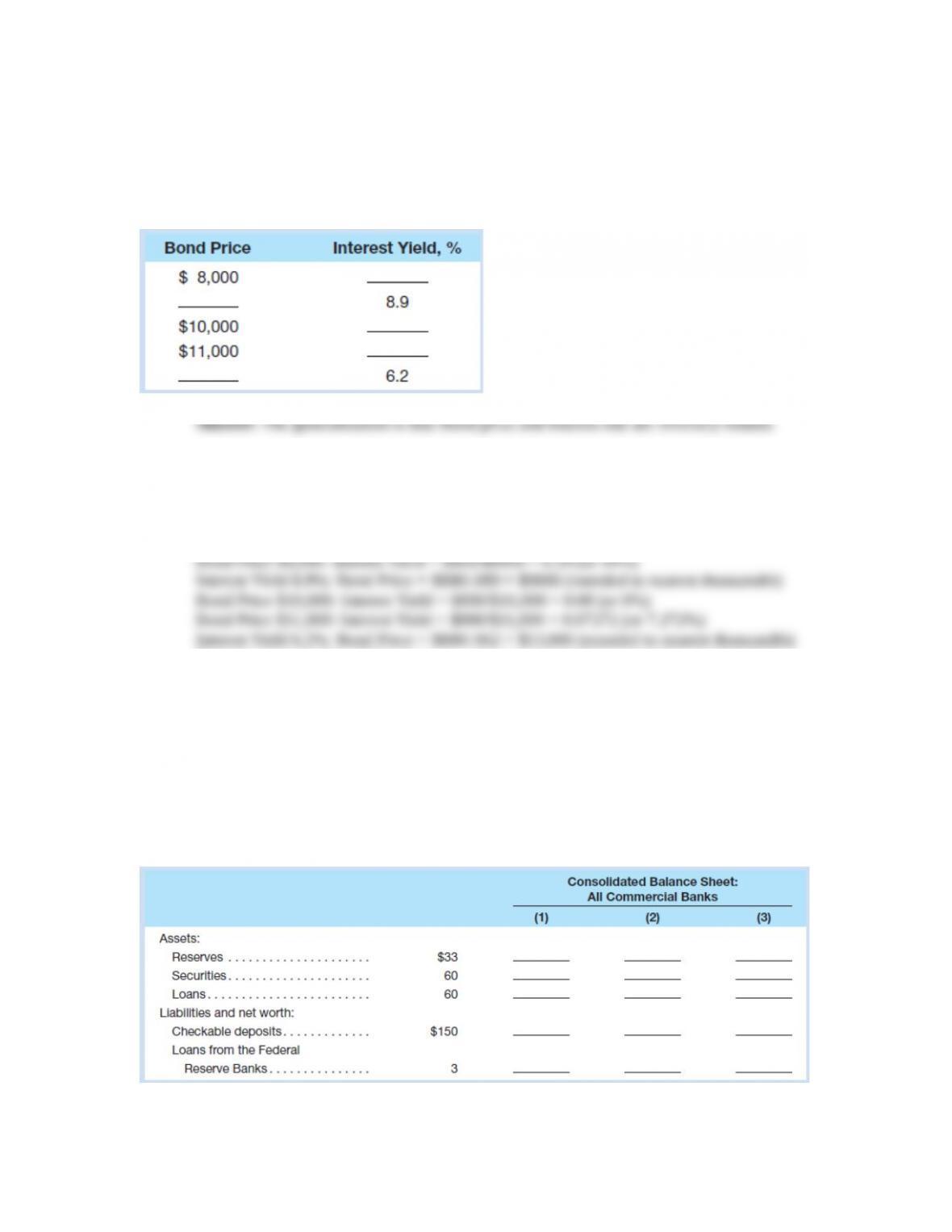

2. Suppose a bond with no expiration date has a face value of $10,000 and annually pays a fixed

amount of interest of $800. In the table provided, calculate and enter either the interest rate that

the bond would yield to a bond buyer at each of the bond prices listed or the bond price at each of

the interest yields shown. Round your answer to the nearest thousandth. What generalization can

be drawn from the completed table? LO1

Feedback:

To answer this question we use the formula for a perpetuity.

Bond Price = Fixed Payment Amount / Interest Yield

or

Interest Yield = Fixed Payment Amount / Bond Price

Note here that the Face Value does not enter the equation because it has no expiration

date (you could actually drop this part of the question).

The generalization is that bond price and interest rate are inversely related.

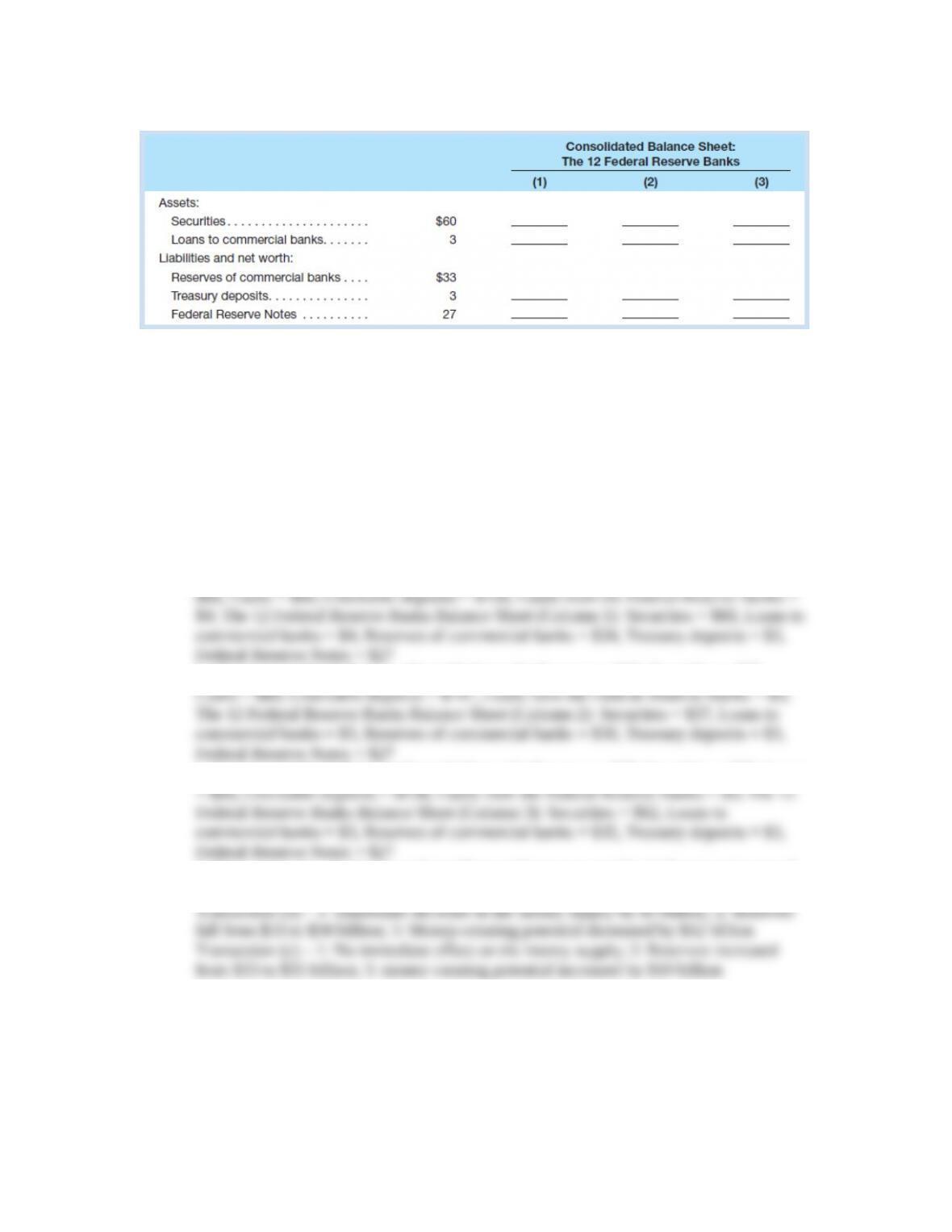

3. In the accompanying tables you will find consolidated balance sheets for the commercial

banking system and the 12 Federal Reserve Banks. Use columns 1 through 3 to indicate how the

balance sheets would read after each of transactions a to c is completed. Do not cumulate your

answers; that is, analyze each transaction separately, starting in each case from the numbers

provided. All accounts are in billions of dollars. LO3

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

a. A decline in the discount rate prompts commercial banks to borrow an additional $1 billion

from the Federal Reserve Banks. Show the new balance-sheet numbers in column 1 of each table.

b. The Federal Reserve Banks sell $3 billion in securities to members of the public, who pay for

the bonds with checks. Show the new balance-sheet numbers in column 2 of each table.

c. The Federal Reserve Banks buy $2 billion of securities from commercial banks. Show the new

balance-sheet numbers in column 3 of each table.

d. Now review each of the above three transactions, asking yourself these three questions: (1)

What change, if any, took place in the money supply as a direct and immediate result of each

transaction? (2) What increase or decrease in the commercial banks’ reserves took place in each

transaction? (3) Assuming a reserve ratio of 20 percent, what change in the money-creating

potential of the commercial banking system occurred as a result of each transaction?

Answer: a. Commercial Bank Balance Sheet (Column 1): Reserves = $34, Securities =

b. Commercial Bank Balance Sheet (Column 2): Reserves = $30, Securities = $60,

c. Commercial Bank Balance Sheet (Column 3): Reserves = $35, Securities = $58, Loans

d. Transaction (a) – 1: No immediate effect on the money supply; 2: Reserves increased

from $33 to $34 billion; 3: Money-creating potential increased by $5 billion

16-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

Feedback: Part a:

Since the decline in the discount rate prompts commercial banks to borrow an additional

$1 billion from the Federal Reserve Banks, the commercial banks’ reserves increase by

Part b:

Since the Reserve Banks sell $3 billion in securities to members of the public, who pay

For the Twelve Federal Reserve Banks we see a decrease in securities by $3 billion, from

Part c:

Since the Federal Reserve Banks buy $2 billion of securities from commercial banks the

CONSOLIDATED BALANCE SHEET: ALL COMMERCIAL BANKS

(1) (2) (3)

Assets:

Reserves

$ 33

$34

$30

$35

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

CONSOLIDATED BALANCE SHEET:

TWELVE FEDERAL RESERVE BANKS

(1) (2) (3)

Assets:

Liabilities and net worth:

Reserves of commercial banks

Treasury deposits

Federal Reserve Notes

$33

3

27

$34

3

27

$30

3

27

$35

3

27

Part d:

Transaction (a):

Transaction (b):

There is an immediate effect on the money supply here because the banks checkable

deposits have fallen to $147 billion immediately after the transaction. Thus, there is an

immediate decrease in the money supply by $3 billion.

Transaction (c):

There is no immediate effect on the money supply because the banks checkable deposits

16-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

4. Refer to Table 16.2 and assume that the Fed’s reserve ratio is 10 percent and the economy is in

a severe recession. Also suppose that the commercial banks are hoarding all excess reserves (not

lending them out) because of their fear of loan defaults. Finally, suppose that the Fed is highly

concerned that the banks will suddenly lend out these excess reserves and possibly contribute to

inflation once the economy begins to recover and confidence is restored. By how many

percentage points would the Fed need to increase the reserve ratio to eliminate one-third of the

excess reserves? What would be the size of the monetary multiplier before and after the change in

the reserve ratio? By how much would the lending potential of the banks decline as a result of the

increase in the reserve ratio? LO3

Feedback: At the 10% reserve ratio the amount of excess reserves is $3,000. If the Fed

The monetary multiplier before the change is 10 (= 1/0.1).

5. Suppose that the demand for Federal funds curve is such that the quantity of funds demanded

changes by $120 billion for each 1 percent change in the Federal funds interest rate. Also, assume

that the current Federal funds rate is at the 3 percent rate that is targeted by the Fed. Now suppose

that the Fed retargets the rate to 3.5 percent. Assuming no change in demand, will the Fed need to

increase or decrease the supply of Federal funds? By how much will the quantity of Federal funds

have to change for the equilibrium to occur at the new target rate? LO4

Feedback: Since the current Federal funds rate is at the 3 percent rate and Fed retargets

6. Suppose that inflation is 2 percent, the Federal funds rate is 4 percent, and real GDP falls 2

percent below potential GDP. According to the Taylor rule, in what direction and by how much

should the Fed change the real Federal funds rate? LO4

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

Feedback:

The Taylor rule assumes that the Fed has a 2 percent “target rate of inflation” that it is

willing to tolerate and that the FOMC follows three rules when setting its target for the

Federal funds rate:

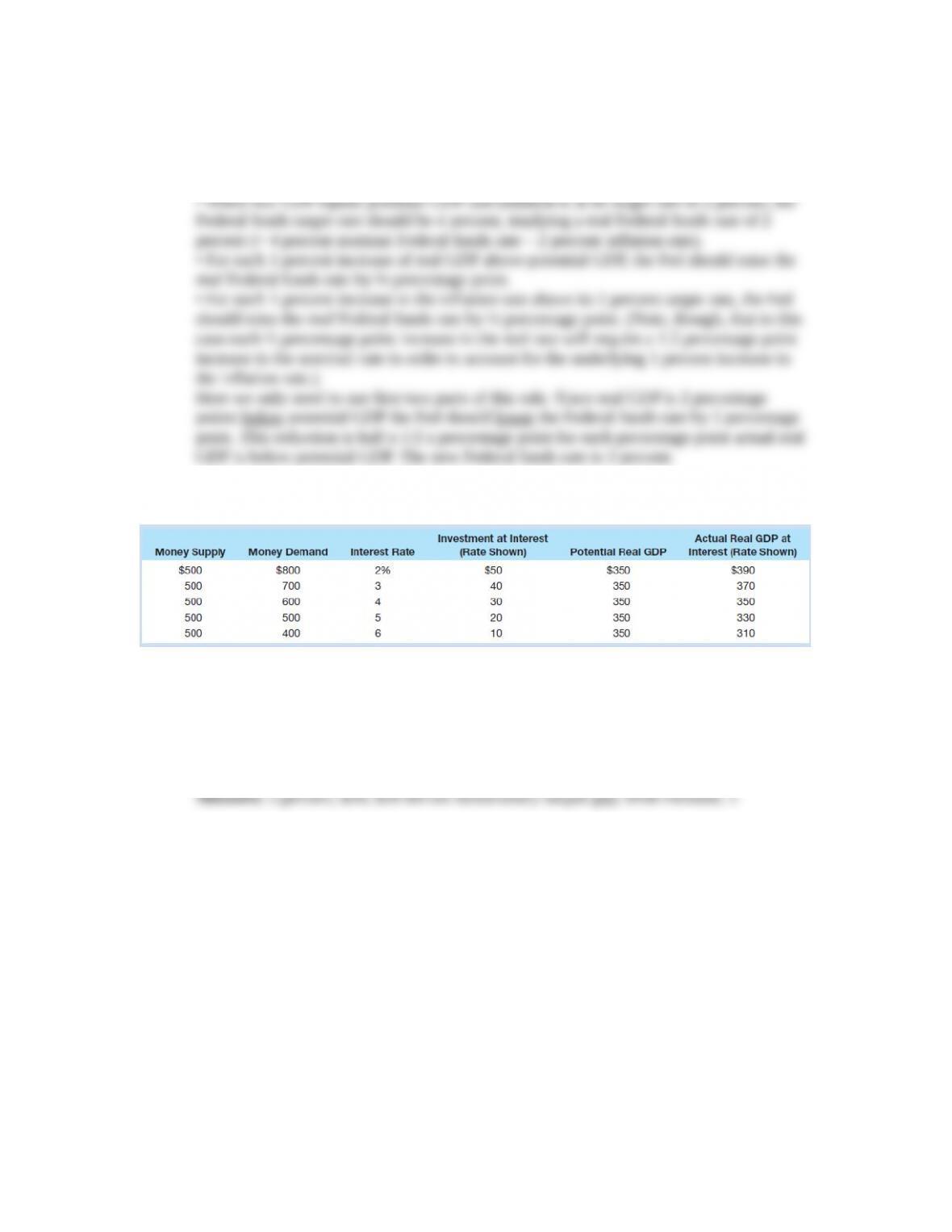

7. Refer to the accompanying table for Moola to answer the following questions. LO5

What is the equilibrium interest rate in Moola? What is the level of investment at the equilibrium

interest rate? Is there either a recessionary output gap (negative GDP gap) or an inflationary

output gap (positive GDP gap) at the equilibrium interest rate, and, if either, what is the amount?

Given money demand, by how much would the Moola central bank need to change the money

supply to close the output gap? What is the expenditure multiplier in Moola?

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

Feedback:

The equilibrium interest rate occurs at the interest rate where the quantity of money

Investment at this interest rate is $20.

At the interest rate of 5% potential GDP is $350 and actual GDP is $330. Since actual

To find the expenditure multiplier we can divide the change in actual GDP by the change

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.