Chapter 16 – Interest Rates and Monetary Policy

Chapter 16 – Interest Rates and Monetary Policy

McConnell Brue Flynn 20e

DISCUSSION QUESTIONS

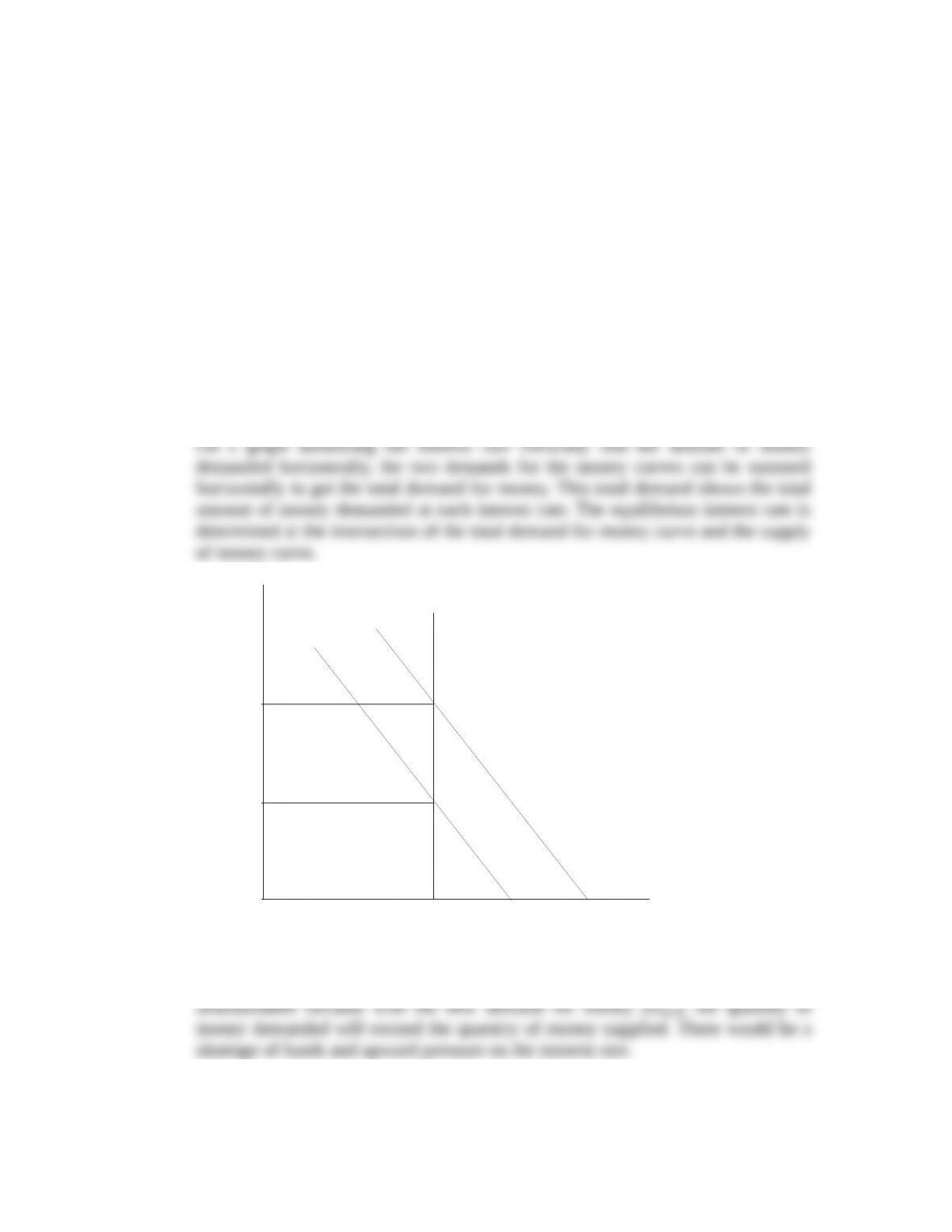

1. What is the basic determinant of (a) the transactions demand and (b) the asset demand for

money? Explain how these two demands can be combined graphically to determine total money

demand. How is the equilibrium interest rate in the money market determined? Use a graph to

show the impact of an increase in the total demand for money on the equilibrium interest rate (no

change in money supply). Use your general knowledge of equilibrium prices to explain why the

previous interest rate is no longer sustainable. LO1

Answer: (a) The level of nominal GDP. The higher this level, the greater the

amount of money demanded for transactions. (b) The interest rate. The higher the

interest rate, the smaller the amount of money demanded as an asset.

Qm

i1

i0

Dm 0 Dm1

Sm

Amount of money demanded and supplied

Rate of interest, i

(percent)

With an increase in total money demand, the previous interest rate (i0) is

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

2. What is the basic objective of monetary policy? What are the major strengths of monetary

policy? Why is monetary policy easier to conduct than fiscal policy? LO3

Answer: The basic objective of monetary policy is to assist the economy in

achieving a full-employment, non-inflationary level of total output.

The major strengths of monetary policy are its speed and flexibility compared to

3. Distinguish between the federal funds rate and the prime interest rate. Why is one higher than

the other? Why do changes in the two rates closely track one another? LO4

Answer: The Federal funds interest rate is the interest rate banks charge one

The Federal funds rate is lower than the prime interest rate for a number of

reasons. Federal funds are loaned overnight, so lenders don’t have to wait long for

4. Why is a decrease in the supply of Federal funds shown as an upshift of the supply curve in

Figure 16.3, whereas an increase in Federal funds is shown as a downshift of the supply curve?

LO4

Answer: The decrease in the supply of Federal funds is shown as an upshift in the supply

curve because the FED will ensure that the quantity of funds supplied equals the quantity

of funds demanded at the targeted rate of 4.5%. In effect, the FED creates a perfectly

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

5. Suppose that you are a member of the Board of Governors of the Federal Reserve System. The

economy is experiencing a sharp rise in the inflation rate. What change in the Federal funds rate

would you recommend? How would your recommended change get accomplished? What impact

would the actions have on the lending ability of the banking system, the real interest rate,

investment spending, aggregate demand, and inflation? LO5

Answer: To reduce inflation, the Federal funds rate should be raised. This would

be accomplished typically through open-market operations (selling bonds), but

6. Explain the links between changes in the nation’s money supply, the interest rate, investment

spending, aggregate demand, real GDP, and the price level. LO5

Answer: A change in the nation’s money supply (achieved by changing reserves

in the banking system) will cause an opposite change in the interest rate. A

reduction in the money supply will make funds increasingly scarce and drive up

7. What do economists mean when they say that monetary policy can exhibit cyclical asymmetry?

How does the idea of a liquidity trap relate to cyclical asymmetry? Why is this possibility of a

liquidity trap significant to policymakers? LO6

Answer: Cyclical asymmetry refers to the condition that a restrictive monetary

policy is relatively potent at contracting economic activity, while an expansionary

monetary policy is relatively weak at stimulating an economy. The weakness in

Cyclical asymmetry, and the potential for a liquidity trap, is important to

policymakers because it suggests that while monetary policy can effectively fight

16-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

8. LAST WORD Did Operation Twist target long-term or short-term interest rates? How does

ZIRP cause problems for savers and pension funds? How might low interest rates lead to

problematic fiscal policy decisions?

Answer: Operation Twist targeted longer-term interest rates. ZIRP caused interest rates to

go to extremely low levels. This causes problems for savers and pension funds because

the yields on investments are extremely low. For example, low yields could force a retiree

Extremely low interest rates could also distort fiscal policy decisions because the interest

payments needed to finance deficit spending are low. This could cause policymakers to

REVIEW QUESTIONS

1. When bond prices go up, interest rates go_______ . LO1

a. Up.

b. Down.

c. Nowhere.

Feedback: When bond prices go up, interest rates go down. This happens because bond

prices and interest rates are inversely related. To see why they are inversely related, recall

that bonds are promises to repay particular amounts of money at particular points in the

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

2. A commercial bank sells a Treasury bond to the Federal Reserve for $100,000. The money

supply: LO3

a. Increases by $100,000.

b. Decreases by $100,000.

c. Is unaffected by the transaction.

Feedback: The money supply will increase by $100,000. This is true because when the

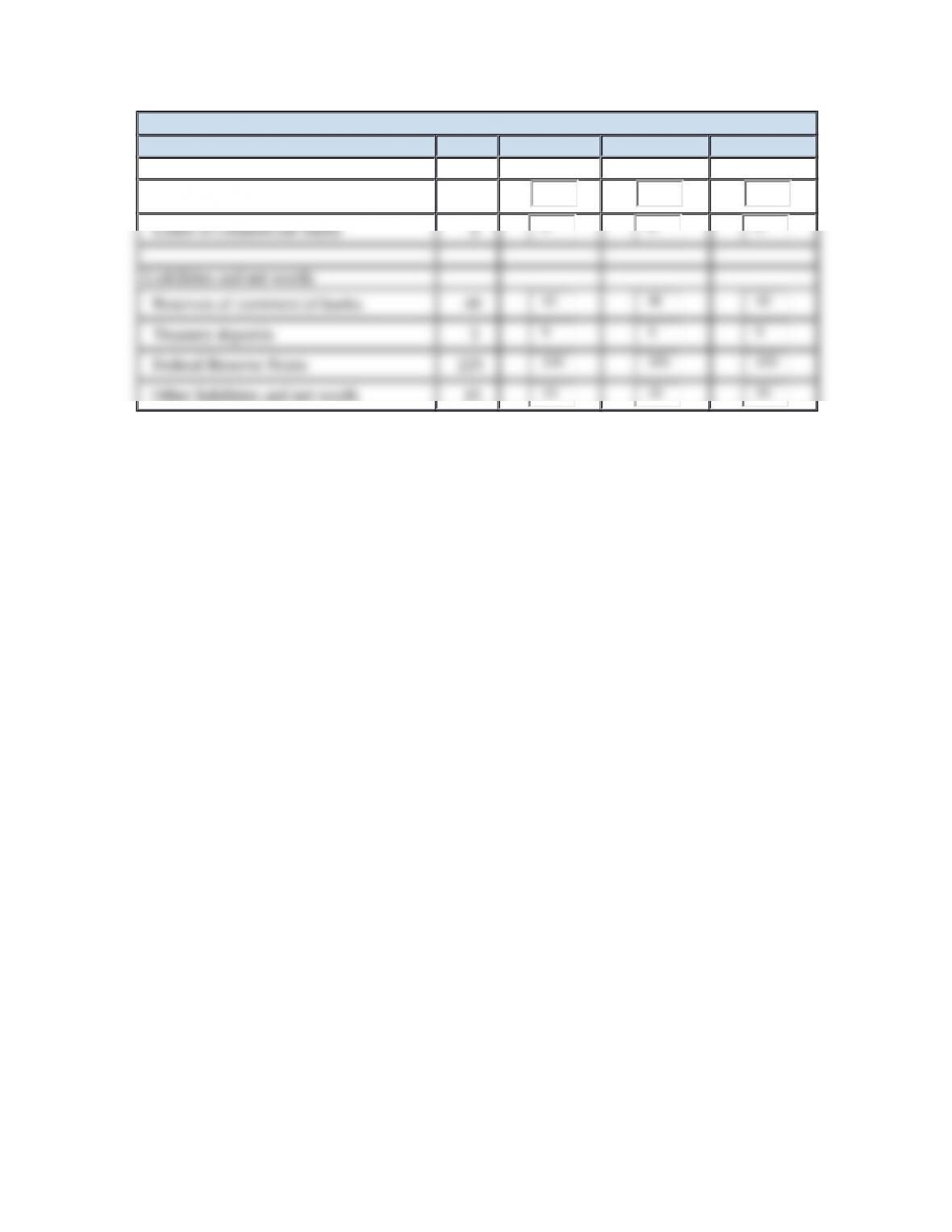

3. Use commercial bank and Federal Reserve Bank balance sheets to demonstrate the effect of

each of the following transactions on commercial bank reserves: LO3

a. Federal Reserve Banks purchase securities from banks.

b. Commercial banks borrow from Federal Reserve Banks at the discount rate.

c. The Fed reduces the reserve ratio.

d. Commercial banks increase their reserves after the Fed increases the interest rate that it pays on

reserves.

Consolidated Balance Sheet: All Commercial Banks

A B C

Assets:

Reserves $ 40 $ $ $

16-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

42 41 40

Chapter 16 – Interest Rates and Monetary Policy

Consolidated Balance Sheet: 12 Federal Reserve Banks

A B C

Assets:

Securities $283 $ $ $

Feedback: In the tables above, columns A through C show the changes caused by the

answers to the questions. It is assumed the initial reserve ratio is 20 percent. Thus, as the

first column shows, the commercial banks are initially completely loaned up. The

answers are not cumulated: We return to the first column each time to show the resulting

change in columns A, B, or C.

a. It is assumed the Fed buys $2 billion worth of securities. This should increase

commercial bank reserves by $2 billion and reduce securities by $2 billion. This is the

immediate effect to the consolidated balance sheet. With demand deposits of $200 billion,

required reserves are $40 billion (= 20 percent of $200 billion). Therefore, excess

reserves are $2 billion (= $42 billion – $40 billion) and the banking system can increase

the money supply (by making loans) by $10 billion more (= $2 billion × 5) in the longer

term.

b. It is assumed the commercial banks borrow $1 billion from the Fed. The immediate

effect to the commercial banks’ consolidated balance sheet is to increase reserves by $1

billion on the asset side and increase loans from the Federal Reserve banks by $1 billion

on the liabilities side. In the longer term, the commercial banks may now increase the

money supply (through making loans) by $5 billion (= $1 billion × 5).

c. Changing the reserve ratio in itself does not change the balance sheets. However, in the

longer term, if we assume the reserve ratio has been decreased from 20 percent to 19

percent, required reserves are now $38 billion (= 19 percent of $200 billion) and the

commercial banks can now increase the money supply (through making loans) by $10.53

billion (= $2 billion × (1/0.19)). Proof: 19 percent of $210.53 billion is $40 billion.

d. Both columns A and B show an increase in commercial bank reserves. However,

column A is the better answer because it shows that the increase in reserves came from

selling securities, whereas the increase in reserves in column B came from loans from the

Federal Reserve Banks. It is unlikely that the Federal Reserve Banks would lend money

to commercial banks at an interest rate lower than the rate the Federal Reserve Banks pay

commercial banks on their reserves. The more likely scenario (which is not shown in the

balance sheets above) is that the commercial banks would increase their reserves by

decreasing loans to their customers.

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

285 283 283

Chapter 16 – Interest Rates and Monetary Policy

4. A bank currently has $100,000 in checkable deposits and $15,000 in actual reserves. If the

reserve ratio is 20 percent, the bank has ___________ in money-creating potential. If the reserve

ratio is 14 percent, the bank has ___________ in money-creating potential. LO3

a. $20,000; $14,000.

b. $3,000; $2,100.

c. -$5,000; $1,000.

d. $5,000; $1,000.

Feedback: If the reserve ratio is 20 percent, the bank has – $5,000 in money-creating

potential. If the reserve ratio is 14 percent, the bank has $1,000 in money-creating

potential. To see why this is true, first consider the case where the bank has a reserve ratio

of 20 percent. Given that it has $100,000 in checkable deposits, the reserve ratio of 20

percent implies that the bank must keep $20,000 (= 0.20 × $100,000) worth of reserves.

5. A bank borrows $100,000 from the Fed, leaving a $100,000 Treasury bond on deposit with the

Fed to serve as collateral for the loan. The discount rate that applies to the loan is 4 percent and

the Fed is currently mandating a reserve ratio of 10 percent. How much of the $100,000 borrowed

by the bank must it keep as required reserves? LO3

a. $0.

b. $4,000.

c. $10,000.

d. $100,000.

Feedback: The bank must keep $0 as required reserves. This is true because the reserve

ratio does not apply to money that commercial banks borrow from the Fed. Thus, in this

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

6. Which of the following Fed actions will increase bank lending? LO3

Select one or more answers from the choices shown.

a. The Fed raises the discount rate from 5 percent to 6 percent.

b. The Fed raises the reserve ratio from 10 percent to 11 percent.

c. The Fed buys $400 million worth of Treasury bonds from commercial banks.

d. The Fed lowers the discount rate from 4 percent to 2 percent.

Answer: The two correct answers are: c. The Fed buys $400 million worth of Treasury

Feedback: These are correct because bank lending will rise when the Fed buys $400

million worth of Treasury bonds from commercial banks and when the Fed lowers the

discount rate from 4 percent to 2 percent. If the Fed buys $400 million worth of Treasury

bonds from commercial banks, the Fed will create $400 million worth of new money to

7. If the Federal Reserve wants to increase the federal funds rate using open-market operations, it

should _____________bonds. LO4

a. Buy.

b. Sell.

Feedback: If the Fed wants to increase the federal funds rate using open-market

operations, it should sell bonds. This is true because those who purchase bonds from the

Fed will have to pay for them with money. Thus, when the Fed sells bonds, money flows

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Chapter 16 – Interest Rates and Monetary Policy

8. True or False: A liquidity trap occurs when expansionary monetary policy fails to work because

an increase in bank reserves by the Fed does not lead to an increase in bank lending. LO6

Feedback: This statement is true because situations in which monetary policy fails

because increases in reserves do not lead to increases in lending are indeed referred to as

liquidity traps. Liquidity traps are very difficult for the Fed to deal with because they

9. True or False: In the United States, monetary policy has two key advantages over fiscal policy:

(1) isolation from political pressure and (2) speed and flexibility. LO6

Feedback: This statement is true because U.S. monetary policy is indeed isolated from

political pressure and does have notable advantages over U.S. fiscal policy in terms of

speed and flexibility. Monetary policy’s political isolation is provided by the Federal

Reserve being a quasi-independent part of the government and by making sure that

16-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.