Chapter 06 – Efficient Diversification

CHAPTER SIX

EFFICIENT DIVERSIFICATION

CHAPTER OVERVIEW

In this chapter, the concept of portfolio formation moves beyond the risky and risk-free asset

that is tangent to the so called efficient frontier of best diversified portfolios, will dominate all

risky portfolios regardless of the level of risk aversion.

As in Chapter 5, investors will optimally vary their asset-allocation decision according to their risk

tolerance by varying the amount they invest in the tangency portfolio and the amount invested in

the risk free asset. See Text figure 6.6. The single-factor-index model is introduced; which

find the minimum variance combinations of two securities. Upon completion of this chapter the

student should have a full understanding of systematic and firm-specific risk, and of how the

portfolio’s firm-specific risk can be reduced by combining securities with differing patterns of

returns. The student should be able to quantify this concept by being able to calculate and

interpret covariance and correlation coefficients.

and thus determine the firm‘s reaction to macroeconomic (market) events.

In addition, the students should be able to construct portfolios of different risk levels, given

information about risk-free rates and returns on risky assets or portfolios of risky assets. Students

should be able to calculate the expected return and standard deviation of these portfolios.

CHAPTER OUTLINE

1. Diversification and Portfolio Risk

2. Asset Allocation with Two Risky Assets

PPT 6-2 through PPT 6-17

When we put stocks in a portfolio, sp < S(Wisi). When Stock 1 has a return > E[r1], it is likely

that Stock 2 has a return < E[r2] so that return on the portfolio that contains stocks 1 and 2

remains close to its expected return. Covariance and correlation measure the tendency for r1 to

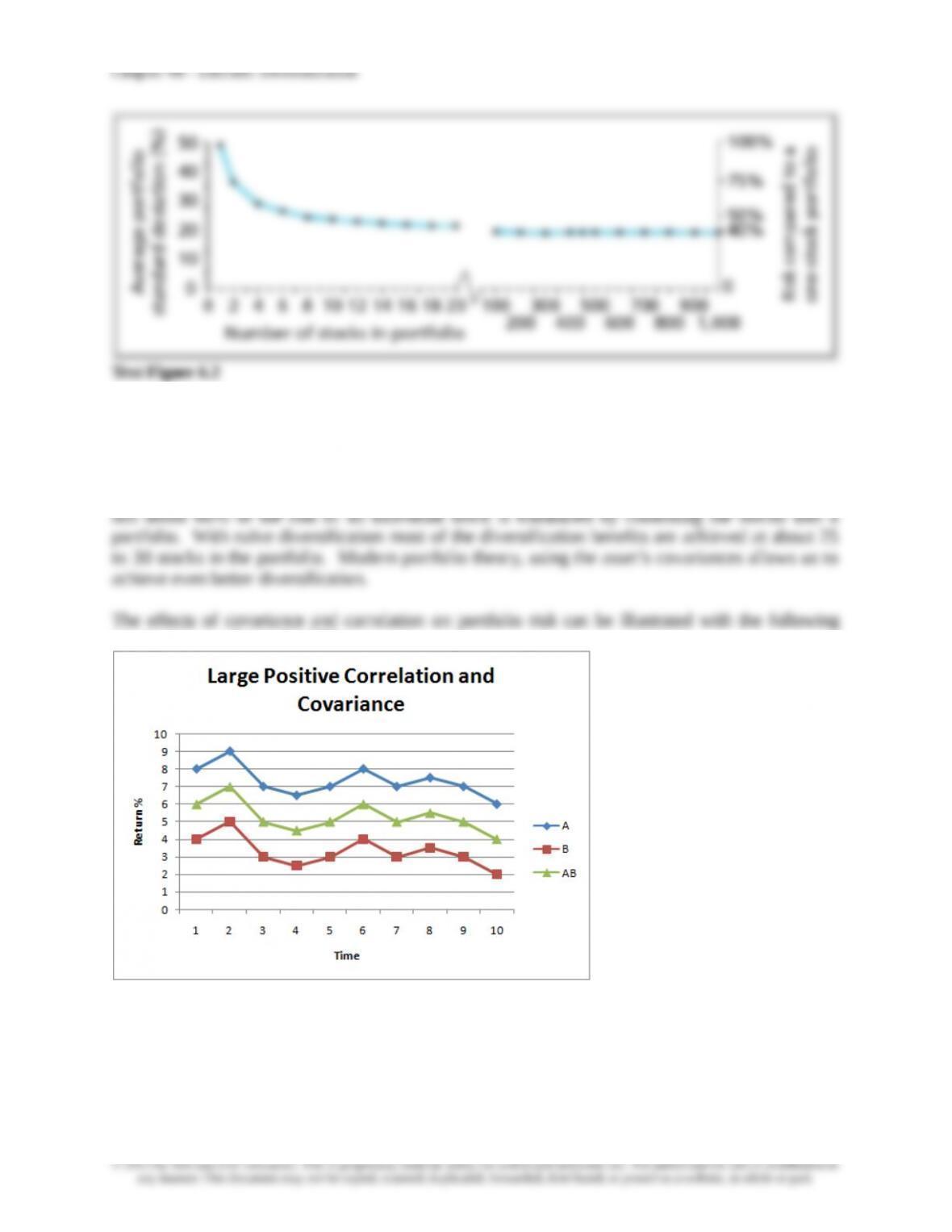

Text Figure 6.2 illustrates how adding securities to the portfolio reduces the portfolio risk as

measured by the standard deviation. Notice size of the standard deviation of a single stock

portfolio. At about 50%, holding a single stock is extremely risky. If the stock has an expected

return of 15% and a standard deviation of 50% then the investor can expect a very wide range of

possible returns of +65% and -35% two out of three years. These stocks were randomly selected

graphs that are also in the PPT:

Assets A and B have positive standard deviations and the correlation between A and B is +1.

Thus, the standard deviation of Portfolio AB is a simple weighted average of the standard

deviations of A and B and no risk is reduced by combining the two.

6-2

averaged or diversified away.

Return and Risk of a Two Asset Portfolio

The expected return of a portfolio is simply a weighted average of the returns of the portfolio

components. Because of the diversification effects however, the standard deviation of the

portfolio is not a simple weighted average of standard deviations of the components. The relevant

Cov(r1r2) = Covariance of returns for Security 1 and Security 2

6-3

Chapter 06 – Efficient Diversification

The PPT provides ample detail about the correlation coefficient and about why correlations are

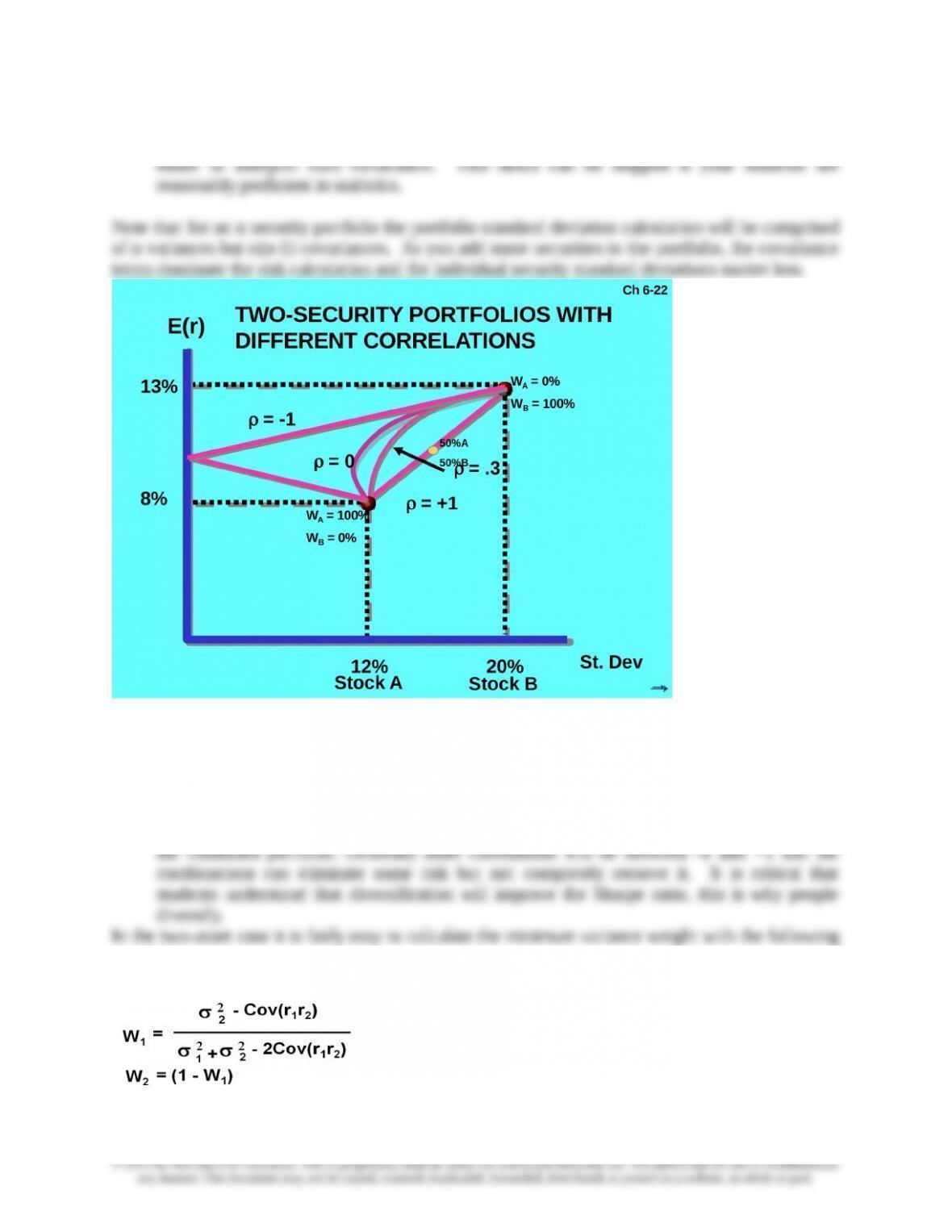

The graph depicts return/risk combinations of two securities, A and B for different hypothetical

correlation coefficients. If there is a perfect positive correlation between A and B,

combining the two securities yields no diversification benefits and combinations of A and B

fall on a straight line because in this case p = Wii. However if the assets are perfectly

negatively correlated, we can combine the two securities to completely eliminate variance in

equations:

6-4

Chapter 06 – Efficient Diversification

Once the weights are known, the minimum variance portfolio expected return and risk can be

the curve. Any minimum variance point on the bottom of the curve can be dominated by the

similar point on the upper portion of the curve. The curve from the global minimum–variance

portfolio, up and to the right, represents the efficient frontier, which are the best diversified

combinations or the least risky for each possible expected return level.

The text also illustrates the benefits of diversification, using historical data to examine the effects

risk tolerance due to the principle of separation which holds that that portfolio choice can be

separated into two independent tasks: (1) determination of the optimal risky portfolio and (2) the

personal choice of the best mix of the risky portfolio and the risk free asset. This is a crucial

point. It means that a widow (with high risk aversion) and a ‘yuppie’ (a young upwardly mobile

professional with low risk aversion) should both choose the same risky portfolio. Their asset

3. The Optimal Risky Portfolio with a Risk-Free Asset

6-5

4. Efficient Diversification with Many Risky Assets

PPT 6-18 through PPT 6-29

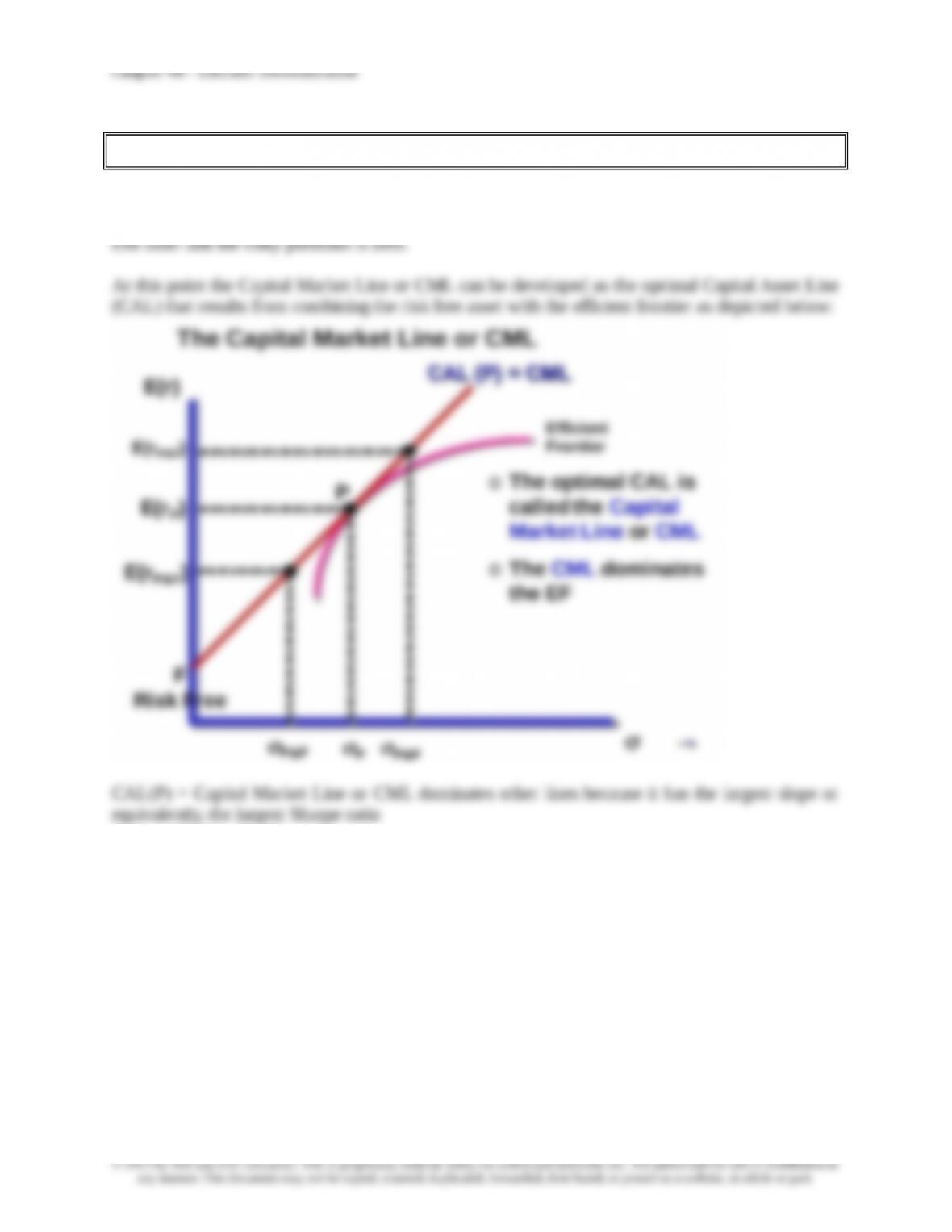

The inclusion of a risk-free asset in a portfolio results in a single combination of stock and bonds

that is optimal when that portfolio is combined with the risk-free asset. As explained in Chapter 5

the resulting capital allocation line is now linear. This is because the covariance between the risk

Slope = (E(rp) – rf) / p

That is, the CML maximizes the slope or the return per unit of risk or it equivalently maximizes

the Sharpe ratio. Regardless of risk preferences, some combinations of risky portfolio P & and

risk-free asset F will dominate all other combinations. All investors’ complete portfolio will fall on

the CML.

6-6

indicates a high level of additional return required by the individual investor to bear risk. The

slope of the indifference curve is the marginal rate of substitution (MRS). The slope of the CML

is the marginal rate of transformation (MRT). The optimal complete portfolio is found on the

CML where the MRS = MRT.

Practical Implications

portfolio P may have to be adjusted for individual clients for tax and liquidity concerns, if relevant,

and to adjust for the client’s unique circumstances.

5. A Single Index Asset Market

PPT 6-30 through PPT 6-38

We have learned that investors should diversify, thus individual securities will be held in a

portfolio.

6-7

in interest rates or GDP; or a financial crisis such as that which occurred in 2007 and 2008. If a

well diversified portfolio has no unsystematic risk then any risk that remains must be systematic;

the variation in returns of a well–diversified portfolio must be due to changes in systematic factors.

We have already learned that covariance is the predominant statistic in determining the risk of a

portfolio. Similarly, the systematic risk of an individual stock is a function of the covariance of

axis. This is referred to as alpha. Beta is the slope of the regression line. A higher beta means

higher systematic risk. Betas above 1 are riskier than the market since a regression of the market

excess returns versus market excess returns would, by definition, yield a beta of 1.

6-8

of each security is compared or related to the common index, data requirements are much smaller

than they would be if each pair-wise correlation was measured. Betas also provide an easy

reference point since the market beta is 1.

The Treynor-Black Model (advanced topic)

If a manager has the ability to find undervalued stocks, what strategy should a portfolio manager

managers, the process involves some passive investment in stocks in addition to acquiring the

undervalued stocks.

6-9

Chapter 06 – Efficient Diversification

portfolio is its ratio of alpha to nonsystematic risk.

By combining the active and passive portfolios, the manager can achieve a superior reward-to–risk

combination. Understanding the results of the Treynor-Black Model is best accomplished through

a graphical presentation. A graph is provided in the PPT. The standard Capital Market Line

(CML) is shown in the graph. The portfolio of actively managed stocks is shown as point A.

alpha in relation to the stock’s unsystematic risk. Suppose an investor holds a passive portfolio M

but believes that an individual security has a positive alpha. A positive alpha implies the security is

undervalued. Suppose Google has the positive alpha. Adding Google moves the overall portfolio

away from the diversified optimum, thus bearing residual risk that could be eliminated; however, it

might be worth it to earn the positive alpha. We need to determine the optimal portfolio including

• The improvement in the Sharpe ratio (S) over the Sharpe of the passive portfolio M can be

found as:

• This ratio is called the “information ratio.”

• For multiple stocks in the active portfolio:

6-10

PassiveM Google, G W1 W;

)β(1W1

W*

G

*

M

G

O

G

G

*

G

2

G

G

2

M

2

O)σ(e

α

SS

;

)σ(e

G

ii

2

i

i

2

i

*

i

)e(

)e(

W

)e(

…

)e()e()e( n

2

n

2

2

2

1

2

1

n

ii

2

i

6. Risk of Long-Term Investments

PPT 6-39 through PPT 6-40

The last section of this chapter provides a comparison of the variance and standard deviation of

short-term and long-term investments. PPT 6-41 and PPT 6-42 present a calculation for variance

iA

n

i

iAAiA

n

i

iAA W ; αWα

2

iA

n

i

2

iAA

2W)e(