Chapter 05 – Risk and Return: Past and Prologue

CHAPTER FIVE

RISK AND RETURN: PAST AND PROLOGUE

CHAPTER OVERVIEW

should be able to construct portfolios of different risk levels, given information about risk free

rates and returns on risky assets. The student should be able to calculate the expected return and

standard deviation of these combinations.

Students will learn that theoretically one can easily construct portfolios of varying degrees of risk

1. Rates of Return

PPT 5-2 through PPT 5-6

The PPT begins by calculating holding period returns or HPRs and discusses why we calculate

returns and sometimes annualize them. Annualizing with and without compounding is illustrated.

performance over the time under evaluation. Once the return series is calculated, either a

geometric or an arithmetic average may be calculated. Dollar-weighted returns include the effects

of the investor’s choices of when they bought and sold securities. Thus dollar-weighted returns

give the investor a truer estimate of the rate of return they earned based on security return

performance and their own choices of when they bought and sold the security.

2. Risk and Risk Premiums

PPT 5-6 through PPT 5-14

This section begins by illustrating calculations of expected returns and standard deviation ex-ante

for individual securities via scenario analysis. Ex-post average return and standard-deviation

calculations are also provided. Basic characteristics of probability distributions are then covered

How many dollars can I expect to lose on my portfolio in a given time period at a given level of

probability?

The typical probability used is 5%.

In a given probability distribution we need to know what HPR corresponds to a 5% probability.

If returns are normally distributed then we can use a standard normal table or Excel to determine

VaR = E[r] + -1.64485s \

For Example:

A $500,000 stock portfolio has an annual expected return of 12% and a standard deviation of

35%. What is the portfolio VaR at a 5% probability level?

VaR = 0.12 + (-1.64485 * 0.35)

normal distributions. The text illustrates calculating VaR if you have a normal distribution. If

options or other complex instruments are included in the portfolio you will not have a normal

distribution. You then have to approximate the distribution or perhaps use a Monte Carlo

simulation to build a distribution of future returns.

5-2

distributions are not normally distributed. Note the actual 5% probability level will differ from

1.68445 standard deviations from the mean due to kurtosis and skewness if these are present. In

these cases the standard deviation is a not a sufficient statistic to measure risk.

Risk Premium and Risk Aversion

3. The Historical Record

PPT 5-15 through PPT 5-16

Annual Holding Period Returns Statistics 1926-2008 (From Table 5.3)

Geom.

Mean%

Arith.

Mean%

Excess

Return% Kurt. Skew.Series

The geometric mean is the best measure of the compound historical rate of return. Nevertheless

the arithmetic average is the best measure of the expected return. Notice the greater divergence

of the GAR and AAR for small stocks. This is because of the high variance and the higher

proportion of negative returns in the small stock portfolio. Although we don’t have statistical

significance it appears that some of the portfolios exhibit kurtosis. Kurtosis of the normal

normal distribution.

Portfolio

World Stock US Small Stock US Large Stock

Arithmetic Average .1100 .1726 .1143

Geometric Average .0920 .1143 .0934

5-3

Variance .0186 .0694 .0214

If returns are normally distributed then the following relationship among geometric and arithmetic

averages holds:

Arithmetic Average – Geometric Average = ½ s2

The comparisons above indicate that US Small Stocks may have deviations from normality and

US Lg. Stk -29.79 -22.92

Sm. Stk -46.25 -44.93

World Bnd -6.54 -8.69

LT Bnd -7.61 -7.25

These comparisons may indicate that the U.S. Large Stock portfolio, the US Small Stock

4. Inflation and Real Rates of Return

PPT 5-17 through PPT 5-19

The concept of real versus nominal rates and the Fisher Effect are presented. The reason for

needing the exact version of the Fisher Effect is given in a hidden slide with a hyperlink so that the

instructor may use it or not. Note that the approximation version and the exact version of the

Series

% Sharpe Ratio

World Stk 6.00 0.37

US Lg. Stk 6.13 0.37

Sm. Stk 8.17 0.36

World Bnd 2.46 0.24

Chapter 05 – Risk and Return: Past and Prologue

LT Bond portfolio: $1 x 1.02282 = $5.96; if you had invested $1 in the LT Bond portfolio for 82

years your $1 would have grown to the equivalent purchasing power of just under $6.

US Large Stock portfolio: $1 x 1.0682 = $118.87; if you invested $1 in the US Large Stock

portfolio for 82 years your $1 would have grown to the equivalent purchasing power of just under

should not hold bonds? No, adding bonds to a stock portfolio will eliminate proportionally more

risk than the return sacrificed and can lead to higher Sharpe ratios.

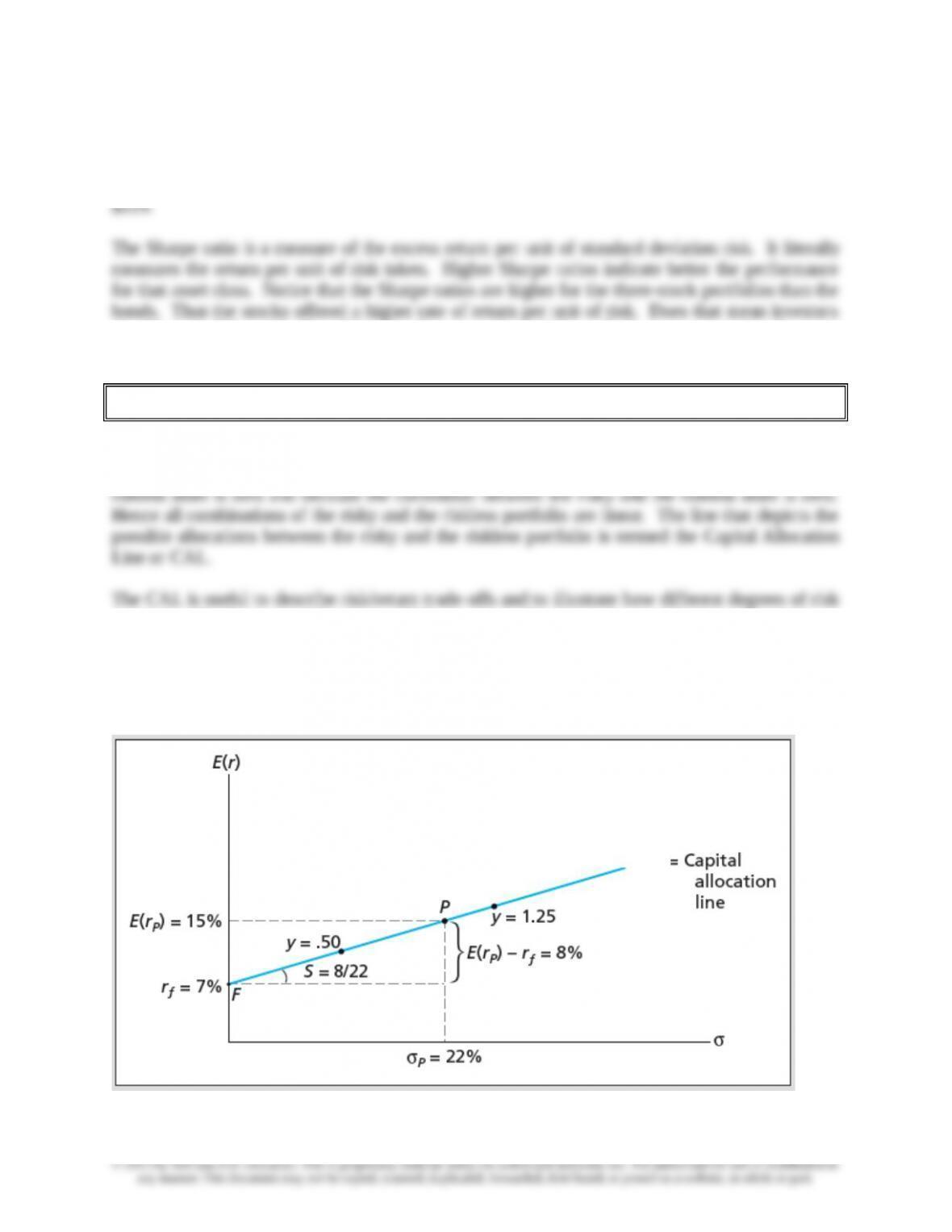

5. Asset Allocation across Risky and Risk-Free Portfolios

PPT 5-20 through PPT 5-24

Investors can choose to hold risky and riskless assets. We may consider investments in a money

market mutual fund as a proxy for the riskless investments that an investor might actually engage

in. These combinations fall on a straight line (see below) because the standard deviation of the

aversion will affect asset allocation. Risk aversion will impact the combinations chosen by an

investor. An investor with a low tolerance for risk will likely prefer to invest some funds in the

risk-less asset. An investor with a high tolerance for risk may choose to use leverage.

Understanding the CAL now will help students understand the modeling in the next chapter when

we consider multiple risky asset combinations.

5-5

CAL

a zero standard deviation. With 100% of your money in the risky asset you will have a 15%

expected return and a 22% standard deviation. Combinations (y) less than one represent varying

percentages invested in the risky asset P and (1-y) the percentage invested in the risk free F.

Combinations above P are possible by borrowing money at F. This is conceptually equivalent to

buying stock on margin. More risk-averse investors would choose a lower y and less risk-averse

2

p

fp A5.0rrE

E(rp) = Expected return on portfolio p

rf = the risk free rate

0.5 = Scale factor

A x sp2 = Proportional risk premium

A larger A indicates that the investor requires more return to bear risk. In the asset allocation

decision the optimal weight in the risky portfolio P (WP) is:

2

P

fP

pA

r)r(E

w

The coefficient of risk aversion A is generally thought to be between 2 and 4.

With an assumed utility function of the form:

U = E[r] – 1/2Asp2

The A term can used to create indifference curves. Indifference curves describe different

combinations of return and risk that provide equal utility (U) or satisfaction. Indifference curves

are curvilinear because they exhibit diminishing marginal utility of wealth. The greater the A the

steeper the indifference curve and all else equal, such investors will invest less in risky assets. The

smaller the A the flatter the indifference curve and all else equal, such investors will invest more in

risky assets.

6. Passive Strategies and the Capital Market Line

PPT 5-25 through PPT 5-27

In a passive strategy the investor makes no attempt to either find undervalued strategies or

actively switch their asset allocations. Investing in a broad stock index and a risk-free investment

is an example of a passive strategy. The CAL that employs the market (or an index that mimics

Excess Returns and Sharpe Ratios Implied by the CML

Excess Return or Risk

Premium

Time Period Average Sharpe

5-6

1956-1984 5.01 17.58 0.28

1985-2008 5.95 18.23 0.33

The average risk premium implied by the CML for large common stocks over the entire time

period is 7.86%. But the subperiod variation and the large standard deviation indicate that

investors cannot be very confident about using the historical data to estimate what the risk