Chapter 17 – Futures Markets and Risk Management

CHAPTER SEVENTEEN

FUTURES MARKETS AND RISK MANAGEMENT

CHAPTER OVERVIEW

This chapter describes the futures markets, trading mechanics involved with futures trading,

strategies and risks associated with futures trading and pricing of futures contracts. The material

covers background material on stock index contracts, describes how such contracts can be used

for hedging and speculation and discusses the concept of index arbitrage. Swaps are also briefly

covered.

LEARNING OBJECTIVES

After studying the chapter students should be able to describe basic characteristics of futures

contracts, understand short and long positions and profits from such positions, and margin trading

arrangements for futures. Students should be able to develop prices for stock index contracts and

describe how such contracts can be used to speculate and hedge. Students should also have a

basic understanding of interest rate swaps.

CHAPTER OUTLINE

1. The Futures Contract

PPT 17-2 through PPT 17-5

Basic elements of futures and forwards are described. Futures contracts are more standardized

than forwards. Performance on futures contracts is warranted by the clearinghouse. Performance

is not warranted on forward contracts. Futures contracts are marked to market and can be traded

on secondary markets. With a forward contract there is no active secondary market.

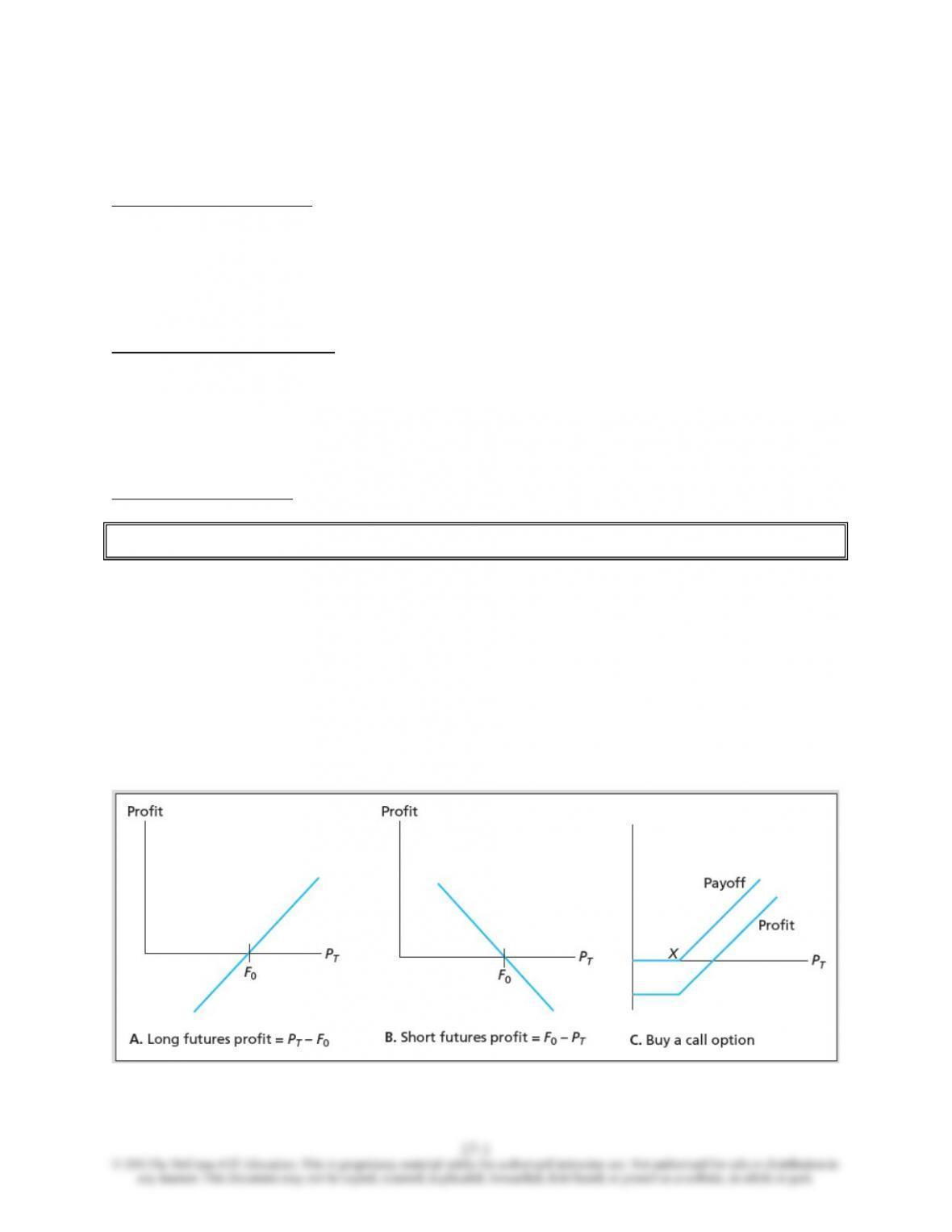

The futures price is the price that is agreed-upon for delivery at maturity. Long positions are

contracts in which the owner agrees to purchase the asset at maturity but the purchase price is

determined by the futures price at the time the contract is initiated. Short positions, or selling

futures, are a promise to deliver the underlying asset at contract maturity future delivery. A profit

graph of the gains and losses on futures and a call option are given below:

Chapter 17 – Futures Markets and Risk Management

The payoff function for the option is different because an option holder has the right to buy the

underlying asset but need not, whereas the long futures position is a commitment to buy the

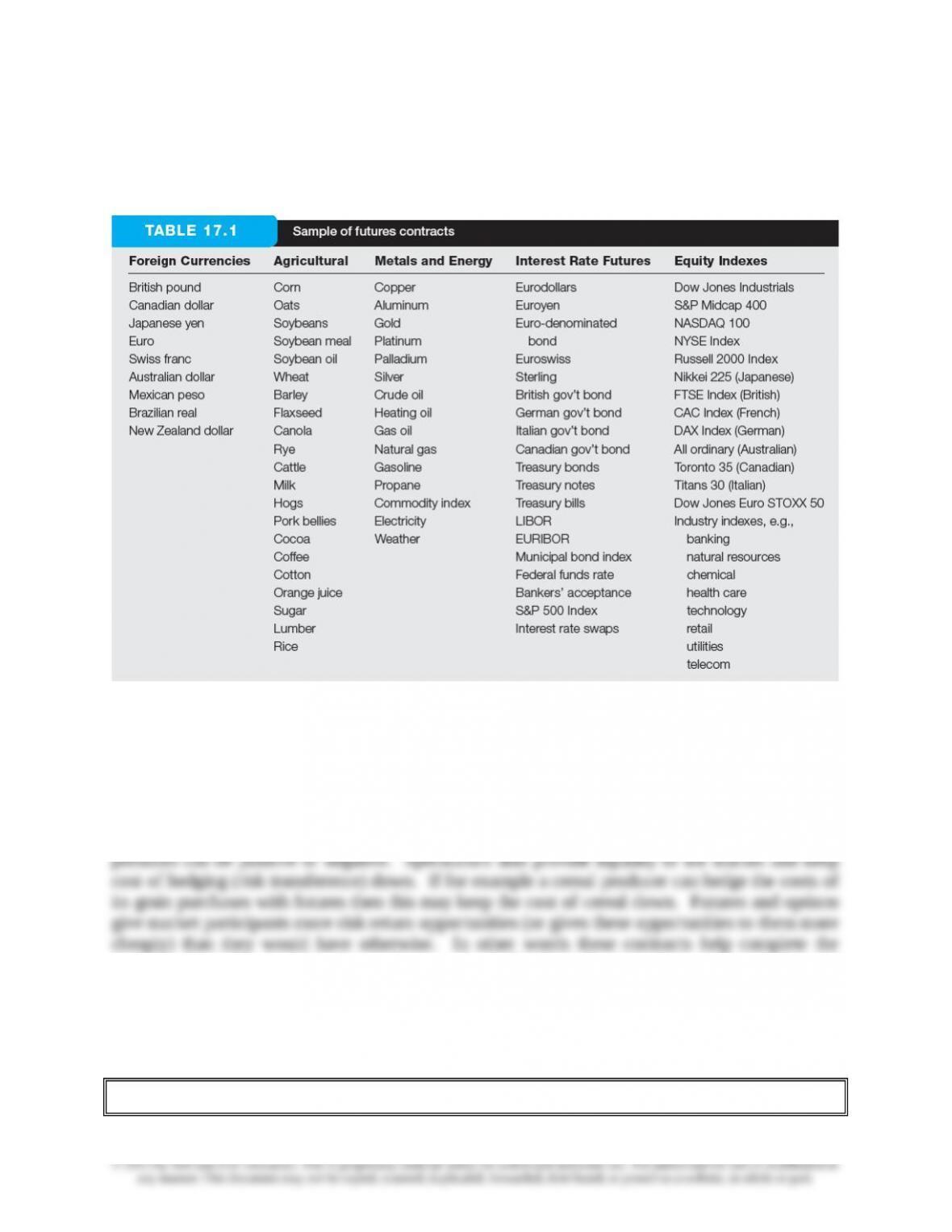

underlying at the price F0 when the contract matures. A list of future contracts is provided below

broken up into the major categories.

There are several oil contracts available. Students may ask questions about oil speculation since

that has been in the news at times when oil prices rose over $100 a barrel. Speculators bore much

of the blame for this. This brings up the argument about whether speculation should be allowed in

futures and in spot markets. Hedging oil prices allows oil users to better predict their cost and

helps keep final costs of their products down. Futures markets allow price discovery and give

investors better information about expected future spot prices. The futures price is a biased

estimate of the expected future spot price. The reason for the bias is a risk premium and the risk

markets. Some fear that there is transference of volatility from the derivatives markets to the spot

markets. Evidence generally indicates that this is not true in normal markets but it probably does

happen in abnormal markets such as a panic; hence circuit breakers are employed in the stock

markets that break the link between the two markets.

2. Trading Mechanics

PPT 17-6 through PPT 17-10

17–2

Chapter 17 – Futures Markets and Risk Management

markets. Entering a futures contract is a commitment to buy or sell the underlying asset.

However, because the contract is liquid, over 90% of futures contracts do not result in delivery.

They are instead closed out with a reversing trade. The clearinghouse nets the investor’s position

to zero and no more changes are made to the investor’s margin account. An investor might worry

that they will forget and accidentally be forced to take or make delivery. It is common to have

futures is a deposit that is made to assure that the contracting party will fulfill the contract. The

profits and losses on the contract are realized on an immediate basis at the end of the day when

the futures prices is settled. The margin is basically prepaying the possible losses for the day.

When the margin falls to a predetermined level, the maintenance margin level, more margin is

required to keep the position open. If the investor can’t or won’t post the required margin, the

clearinghouse’s risk. The clearinghouse basically requires the participants to prepay potential

daily losses and then all the house does is transfer funds from the long to the short and vice versa.

Note that brokers may require higher margin accounts than the exchange mandated minimums

stated here. They typically will require higher minimums for retail accounts.

DAY SETTLE $ VALUE PRICE

MARGIN

TOTAL

SPOT

Wed. 100-00 $100,000.00 $2000.00 $543.75 -79.9% -2.2%

+$2156.25

$2700.00

17–3

in column (3). The price change, column (4) is the new price minus the old price. Column (5)

contains the effects on the margin account. Note that as the investor went short, a drop in price is

a gain and adds to the margin account whereas price increases are losses. The total %HPR is

found from as the cumulative (cum) percent change in the margin account column. For instance,

16.2% = (3137.50 – 2700)/2700, (the price fell so this is a gain to the short, who can ostensibly

5.8% = (2543.75 – 2700)/2700,

-79.9% = (543.75 – 2700)/2700

The spot HPR (cum) is the percent change in the $ value column, keeping the Monday open as

0.45% = (97,406.25 – 97,843.75)/97,843.75

-0.16% = (98,00.00 – 97,843,75)/97,843.75

-2.2% = (100,000.00 – 97,843.75)/97,843.75

The leverage multiplier can be found by taking the ratio of the futures return / Spot HPR return,

for example 16.2% / 0.45% ≈ 36.

Why Delivery on Futures is Not an Issue:

3. Futures Market Strategies

PPT 17-11 through PPT 17-13

Futures contracts can be used to speculate on price movements or to hedge against price

movements. A speculator is hoping to profit from a price change. If a speculator expects the

4. The Determination of Futures Prices

PPT 17-14 through PPT 17-18

Pricing on futures contracts is described using the spot–futures parity theorem. The theorem is

1. Borrow S0 S0-S0(1+rf)T

2. Buy spot for S0 -S0ST

3. Sell futures

short

0 F0 – ST

Total 0 F0 – S0(1+rf)T

In the text example, a few assumptions should be made explicit. First, the only cost of carry in

5. Financial Futures

PPT 17-19 through PPT 17-27

Stock index contracts have improved many trading and hedging strategies. Stock contracts are

available on a variety of domestic and international stock indexes. They offer considerable

advantages over direct stock purchases. The advantages of futures indexes apply to investment

via index arbitrage. This is a form of program trading. Sample contracts are presented in Text

Figure 17.2 which is replicated here (see below). Index contracts reduce the cost of a classic

market timing strategy involving switching between Treasury bills and stocks based on market

conditions. It is cheaper to buy Treasury bills and then shift stock market exposure by buying and

selling stock index futures. In this strategy the investor is changing the relative weights on the

Chapter 17 – Futures Markets and Risk Management

Foreign currency and interest rates are also available in the financial futures markets. The majority

of currency activity occurs off exchange with major banks acting as dealers in spot and forward

trading. Quotes from the dealer spot and forward markets are displayed. Futures contracts are

issuing the forward contract the bank may cancel the contract at the customer’s request.

Major contracts include contracts on Eurodollars, Treasury Bills, Treasury notes and Treasury

bonds. Contracts on some foreign interest rates are also available. A short position in these

contracts will benefit if interest rates increase and may be used to hedge a bond portfolio. A long

position benefits if interest rates fall. A bank that has short term loans funded by longer term debt

6. Swaps

PPT 17-28 through PPT 17-30

One of the markets that have experienced phenomenal growth is the swap market. From 2004 to

2007 the notional principal of interest rate swaps grew at 25% per year. Swaps are basically

groups of forwards that are packaged together. They allow participants in the market to hedge

Swaps are among the most flexible tools available and can serve a variety of purposes. In the

example below two institutions use swaps to limit their interest rate risk. If an institution has

variable rate or short term interest bearing assets funded by longer term fixed rate liabilities it is at

risk from falling interest rates. If an institution has fixed rate or long term interest bearing assets

funded by shorter term variable rate liabilities it is at risk from rising interest rates. Since an

Company A wants variable rate

financing to match their

variable rate investments.

They will pay LIBOR + 5 basis

points.

Company B wants fixed-

rate financing. They will

pay 7.05%.

Chapter 17 – Futures Markets and Risk Management

Recall that LIBOR is the London Interbank Offer Rate, the rate that banks charge each other in

the international banking market. Note that the swap dealer is not exposed to interest rate risk,

but they do face counterparty credit risk. The two deals may not be done synchronously, and

probably won’t be. The dealer (typically a bank) manages the ‘swap book.’ The variable side is

trillion notional principal in interest rate swaps outstanding. These numbers are from the BIS

(Bank of International Settlements) which collects data on all OTC derivatives and publishes a

triennial survey of market size. The $342 trillion (yes that is not a typo, its trillion) vastly

overstates the market size because interest rate swaps don’t involve principal exchanges. The

numbers for interest rate swaps include only single currency swaps, and the euro is now the