Chapter 10 – Bond Prices and Yields

1.

a. Catastrophe bond: Typically issued by an insurance company. They are

similar to an insurance policy in that the investor receives coupons and par

value, but takes a loss in part or all of the principal if a major insurance

claim is filed against the issuer. This is provided in exchange for higher

than normal coupons.

issuers are called Samurai bonds.

d. Junk bond: Those rated BBB or above (S&P, Fitch) or Baa and above

(Moody’s) are considered investment grade bonds, while lower-rated

bonds are classified as speculative grade or junk bonds.

e. Convertible bond: Convertible bonds may be exchanged, at the

repayment burden for the firm is spread over time just as it is with a

sinking fund. Serial bonds do not include call provisions

g. Equipment obligation bond: A bond that is issued with specific equipment

pledged as collateral against the bond.

h. Original issue discount bonds: Original issue discount bonds are less

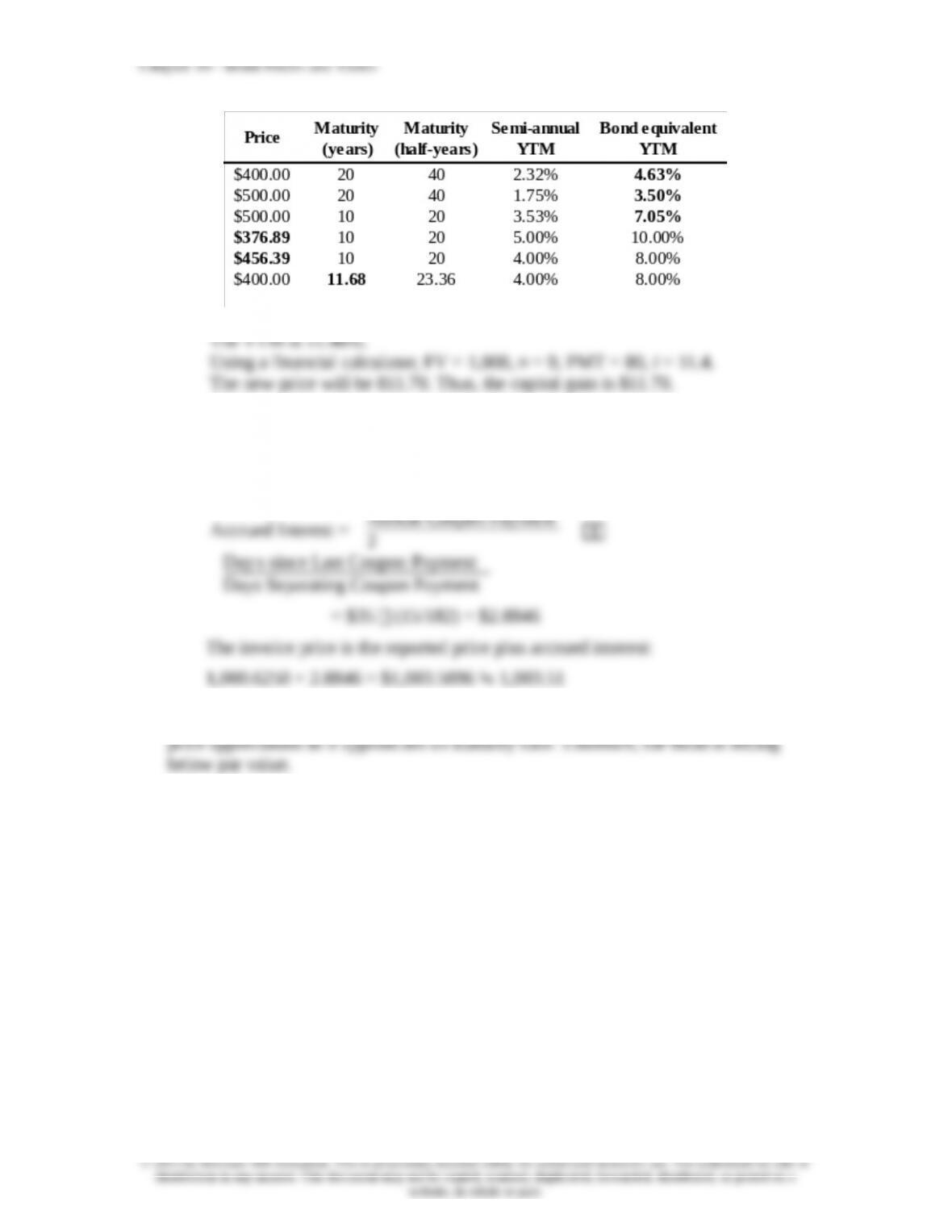

2. Callable bonds give the issuer the option to extend or retire the bond at the call

date, while the extendable or puttable bond gives this option to the bondholder.

3.

a. YTM will drop since the company has more money to pay the interest on

its bonds.

4. Semi-annual coupon = $1,000 6% 0.5 = $30.

10-1

5. Using a financial calculator, PV = –746.22, FV = 1,000, n = 5, PMT = 0.

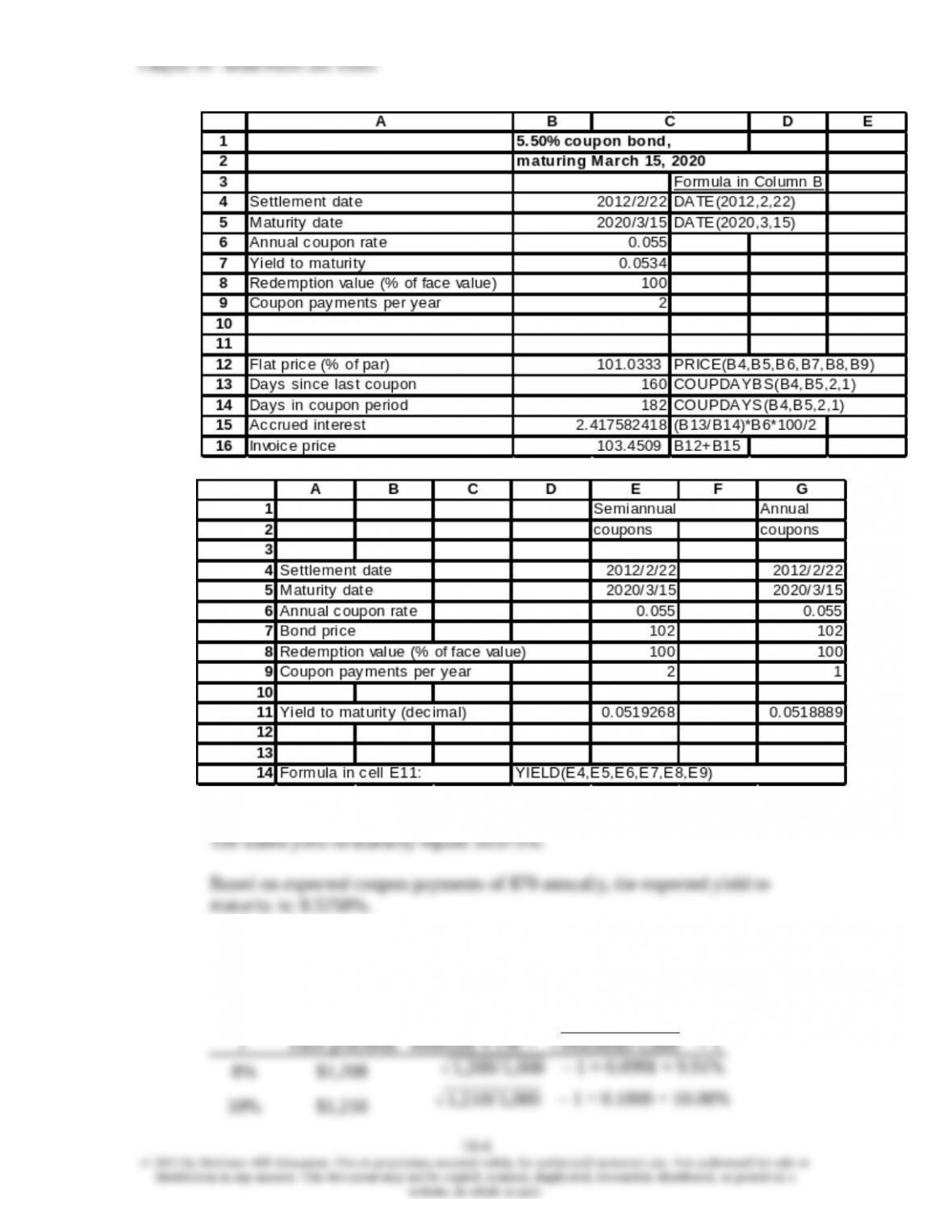

6. A bond’s coupon interest payments and principal repayment are not affected by

changes in market rates. Consequently, if market rates increase, bond investors in

7. The bond callable at 105 should sell at a lower price because the call provision is

more valuable to the firm. Therefore, its yield to maturity should be higher.

8. The bond price will be lower. As time passes, the bond price, which is now above

9. Current yield =

Annual Coupon

Bond Price

=

$ 1,000 4.8%

$970

= 4.95%

10. a. The purchase of a credit default swap. The investor believes the bond may

11. c. When credit risk increases, the swap premium increases because of higher

12. The current yield and the annual coupon rate of 6% imply that the bond price was

at par a year ago.

13. Zero coupon bonds provide no coupons to be reinvested. Therefore, the final value of

14.

a. Effective annual rate on a three-month T-bill:

10-2

15. The effective annual yield on the semiannual coupon bonds is (1.04)2 = 8.16%. If

16.

a. The bond pays $50 every six months.

Current price:

[$50 Annuity factor(4%, 6)] + [$1000 PV factor(4%, 6)] = $1,052.42

17.

a. Use the following inputs: n = 40, FV = 1,000, PV = –950, PMT = 40. We

will find that the yield to maturity on a semi-annual basis is 4.26%. This

implies a bond equivalent yield to maturity of: 4.26% 2 = 8.52%

18. Since the bond payments are now made annually instead of semi-annually, the

bond equivalent yield to maturity is the same as the effective annual yield to

maturity. The inputs are: n = 20, FV = 1000, PV = –price, PMT = 80. The

resulting yields for the three bonds are:

10-3

19.

Nominal Return =

Interest + Price Appr e ciation

Initial Price

1 + Nominal Return

1 + In flation Rate

$ 42.02 + $ 30 .6 0

$ 1,020.00

1 + 0.03

1.0 3

1 + 0.0 50400

1 + 0.071196

1.071196

1 + 0.01

1.0 1

The real rate of return in each year is precisely the 4% real yield on the bond.

20. Remember that the convention is to use semi-annual periods:

Price of a Zero-Coupon Bond =

Face Value

(1+ Semiannual YTM) T

21. Using a financial calculator, input PV = –800, FV = 1,000, n = 10, PMT = 80.

22. The reported bond price is: 100 2/32 percent of par = $1,000.6250

15 days have passed since the last semiannual coupon was paid, so there is an

accrued interest, which can be calculated as:

Annual Coupon Payment

23. If the yield to maturity is greater than current yield, then the bond offers the prospect of

24. The coupon rate is below 9%. If coupon divided by price equals 9% and price is less

than par, then coupon divided by par is less than 9%.

25. The solution is obtained using Excel:

10-5

26. The solution is obtained using Excel:

27. Using financial calculator, n = 10; PV = –900; FV = 1,000; PMT = 140

28. The bond is selling at par value. Its yield to maturity equals the coupon rate, 10%. If the

first-year coupon is reinvested at an interest rate of r percent, then total proceeds at the

end of the second year will be: [100 (1 + r) + 1100]. Therefore, realized compound

yield to maturity will be a function of r as given in the following table:

12% $1,212

29. April 15 is midway through the semi-annual coupon period. Therefore, the invoice price

30. Factors that might make the ABC debt more attractive to investors, therefore

justifying a lower coupon rate and yield to maturity, are:

The ABC debt is a larger issue and therefore may sell with greater

liquidity.

31.

a. The floating-rate note pays a coupon that adjusts to market levels.

Therefore, it will not experience dramatic price changes as market yields

fluctuate. The fixed rate note therefore will have a greater price range.

b. Floating rate notes may not sell at par for any of these reasons:

The yield spread between one-year Treasury bills and other money market

Chapter 10 – Bond Prices and Yields

The coupon increases are implemented with a lag, i.e., once every year.

d. The fixed-rate note currently sells at only 93% of the call price, so that

yield to maturity is above the coupon rate. Call risk is currently low, since

yields would have to fall substantially for the firm to use its option to call

the bond.

e. The 9% coupon notes currently have a remaining maturity of fifteen years

known. The effective maturity for comparing interest rate risk of floating

rate debt securities with other debt securities is better thought of as the

next coupon reset date rather than the final maturity date. Therefore,

“yield-to-recoupon date” is a more meaningful measure of return.

32.

a. The bond sells for $1,124.7237 based on the 3.5% yield to maturity:

[n = 60; i = 3.5; FV = 1,000; PMT = 40]

Therefore, yield to call is 3.3679% semiannually, 6.7358% annually: