Bonus D – Managing Personal Finances

D-41

PPT D-10

Easy-ish Budget Cuts

1. This slide shows the student how to trim the fat off

their monthly budget.

2. Cutting cable! Shock! Horror! Many shows are

available through free sites like Hulu.com; a lot of

people are going cable–less.

3. Encourage students to visit free budgeting sites

(like Mint.com) so they can track their spending.

This might surprise them.

PPT D-11

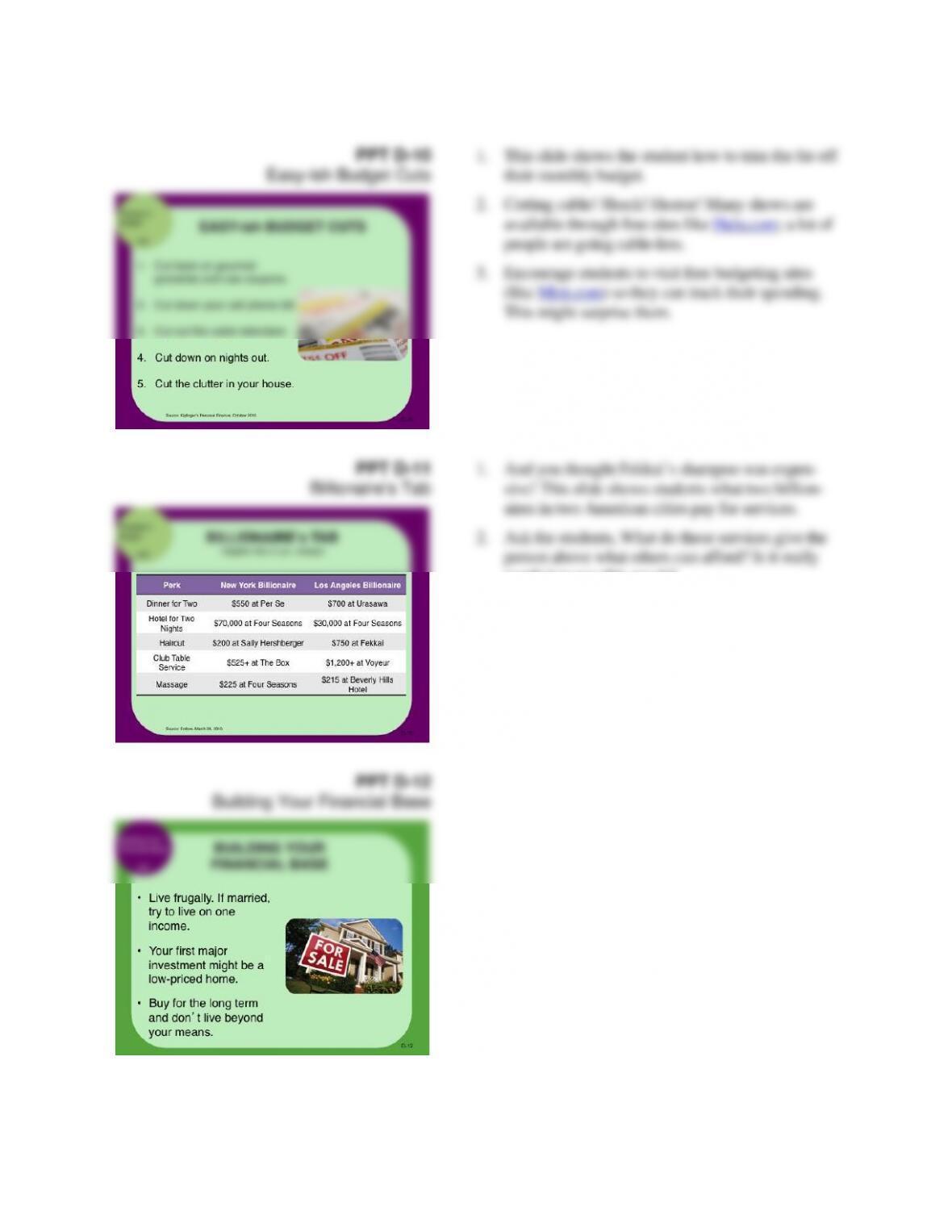

Billionaire’s Tab

1. And you thought Fekkai’s shampoo was expen-

sive! This slide shows students what two billion-

aires in two American cities pay for services.

2. Ask the students, What do these services give the

person above what others can afford? Is it really

worth it to pay this much?

PPT D-12

Building Your Financial Base

Bonus D – Managing Personal Finances

D-42

PPT D-13

Five Rules of Frugality

1. This slide shows five steps to saving money.

2. These are easy steps. Many think you have to give

up all fun if you want to live frugally. This slide

shows that you just need to spend time thinking

before you buy instead of being impulsive.

3. Ask the students, How many of you attend free

concerts instead of paying top–dollar for big acts?

PPT D-14

Financial Benefits of

Buying a Home

Although the housing crisis has dampened home pric-

es, historically real estate has been a sound investment.

PPT D-15

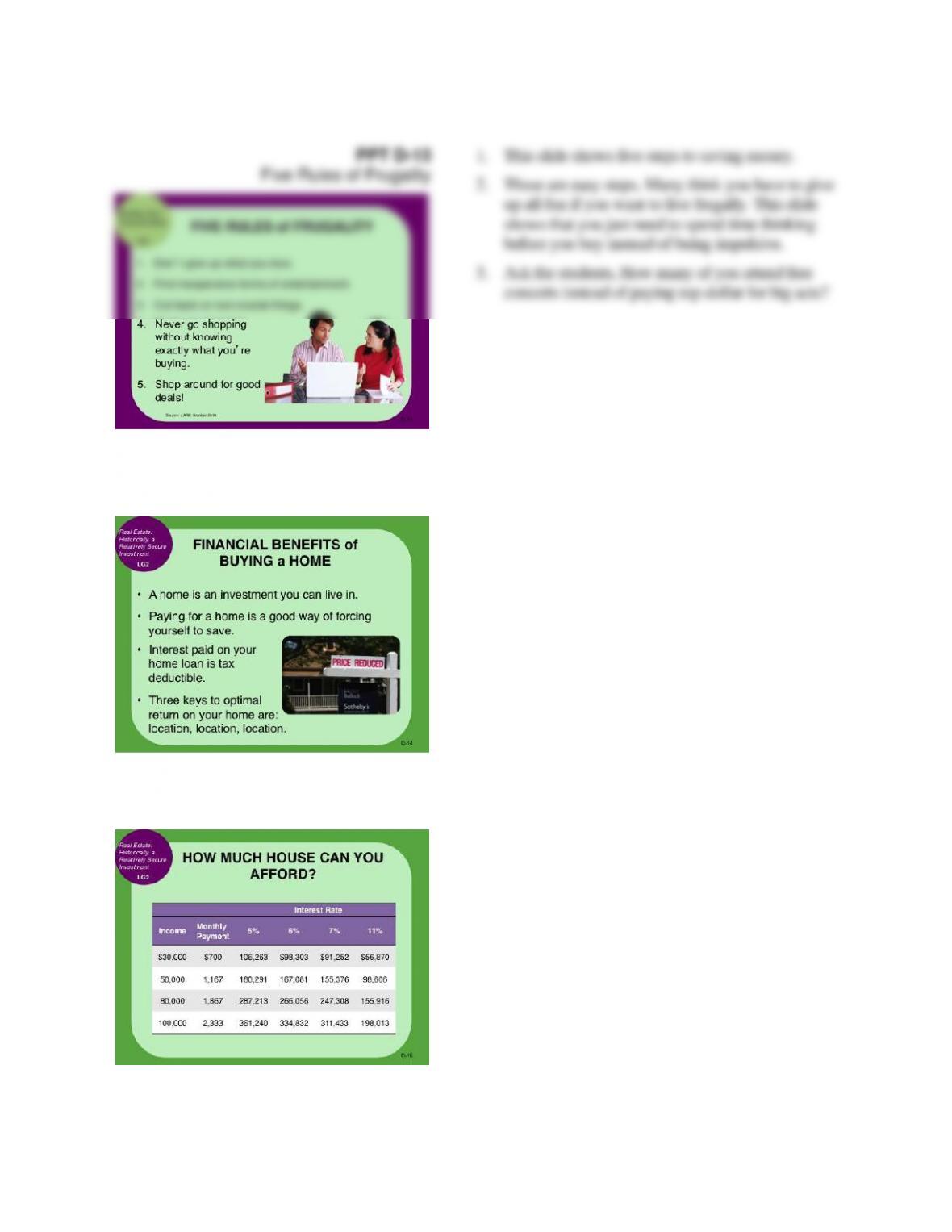

How Much House Can You Afford?

Bonus D – Managing Personal Finances

PPT D-16

Saving and Managing Credit

Warren Buffet is considered a contrarian investor.

PPT D-17

Credit Cards and Debt

PPT D-18

Credit Card Act of 2009

Bonus D – Managing Personal Finances

D-44

Bonus D – Managing Personal Finances

D-45

PPT D-22

Progress Assessment

1. The six steps you can take to control your fi-

nances are (1) take an inventory of your finan-

cial assets, (2) keep track of all your expenses,

(3) prepare a budget, (4) pay off your debts, (5)

start a savings plan, and (6) borrow only to buy

assets that increase in value or generate income.

2. The steps a person should follow to build capital

are find a job, create a budget, and live frugally.

Warren Buffet became one of the world’s richest

people but still lives in the house he purchased

in the 1950s! Invest the money you save to gen-

erate more capital.

3. Historically real estate has been a sound invest-

ment. It is the only investment you can live in.

Also, the payments are fixed with the exception

of taxes and utilities. As your income increases,

the house payments get easier to make, while

rent tends to increase overtime.

PPT D-23

Insuring Your Life

Nearly one-third of U.S. households are without life

insurance coverage. Due to the cost difference, many

recommend the purchase of term insurance rather than

whole life.

Bonus D – Managing Personal Finances

D-46

Bonus D – Managing Personal Finances

D-47

PPT D-27

Where Health Care Money Goes

1. This slide illustrates the percentage of money

that goes to different aspects of health care.

2. Before showing the slide you could give the stu-

dents these categories in a random order and ask

them to rank which ones they think are the high-

est percentage based on money spent for health

care.

3. Note to students that hospital care is the highest

percentage, which makes sense because people

are usually hospitalized only for serious medical

issues.

PPT D-28

What to Know about Health

Savings Accounts

1. Health savings accounts (HSAs) are not for eve-

ryone. Some people choose to save money by

choosing a high-deductible plan.

2. Those plans might work for young, healthy peo-

ple. Consulting a financial planner should be the

first step.

3. If you have cash to pay medical bills, keep your

money in the HSA. At 65, you can withdraw the

money penalty-free and use it for anything.

Bonus D – Managing Personal Finances

D-48

PPT D-29

Social Security

It is important that students understand they cannot re-

ly on Social Security alone as their sole retirement op-

tion.

PPT D-30

Individual Retirement Accounts

Bonus D – Managing Personal Finances

D-49

Bonus D – Managing Personal Finances

PPT D-34

Planning for Those Who Will Inherit

PPT D-35

Progress Assessment

1. Three advantages of using a credit card are (1)

you may have to have a credit card to buy cer-

tain goods or rent a car, (2) credit cards allow

you to easily track your expenses, and (3) they

are more convenient than carrying cash or writ-

ing checks.

2. Term insurance is often recommended for most

people, since it is cheaper than whole life.

3. The primary advantage of an IRA and Keogh is

that the money invested is not taxed until it is

withdrawn. A Keogh plan is like an IRA for the

self-employed. While the current IRA contribu-

tion limit is $5,000, it increases each year in

line with inflation. An additional $1,000 can be

added if you are over the age of 50.

4. The main steps in estate planning are (1) choose

a guardian for your children, (2) prepare a will,

and (3) assign an executor for your estate. It is

also important to sign a durable power of attor-

ney to enable someone else to handle your fi-

nances in the event you are not able to do so.

Bonus D – Managing Personal Finances

lecture

links

lecture link D-1

MILLIONAIRE WOMEN NEXT DOOR

Thomas J. Stanley and William D. Danko’s 1996 book The Millionaire Next Door examined to-

day’s millionaires, who turned out to be small-business owners that drove old cars, shopped in ware-

houses, and pinched pennies. But years later Stanley realized that he was getting a lot of mail from

wealthy women who complained that this portrait of the millionaire didn’t fit them at all. Stanley noted

that 92% of the people in the original study were men, who would have different experiences and out-

looks than women do. Stanley then started a new project—a three-year study of wealthy women, Million-

aire Women Next Door, published in 2003.

D-52

4. DON’T LOOK BACK. Four out of five millionaire women say they never look back.

Instead, they use experience to look forward. They believe it is up to them to turn their

situations around.

lecture link D-2

THE RENT-VERSUS-BUY DECISION

As powerful and persuasive an argument as that was in the 1970s and 1980s, it bears reexamining

in the current era of mortgage points, escalating maintenance costs, and the fairly rapid rate with which

the average American seems to change homes every seven years. And you don’t need a calculator to

know that those who bought homes at the peak of the housing market in 1989 have seen their property

values depreciate 10, 20, and even 30%.

Nevertheless, if you crunch the numbers, buying remains a better deal than renting. But it is nei-

ther “obviously” nor “of course” the right decision. It takes a little more thought.

Bonus D – Managing Personal Finances

D-53

The issue isn’t whether it’s better to rent or buy; the issue is really an individual one based on

lifestyle.

lecture link D-3

KNOW YOUR CREDIT SCORE

Lenders have long used credit scores and reports to determine whether or not to lend you money

and how much interest to charge. But other stakeholders are also interested in your credit report—auto

insurers, employers, landlords, even utility companies.

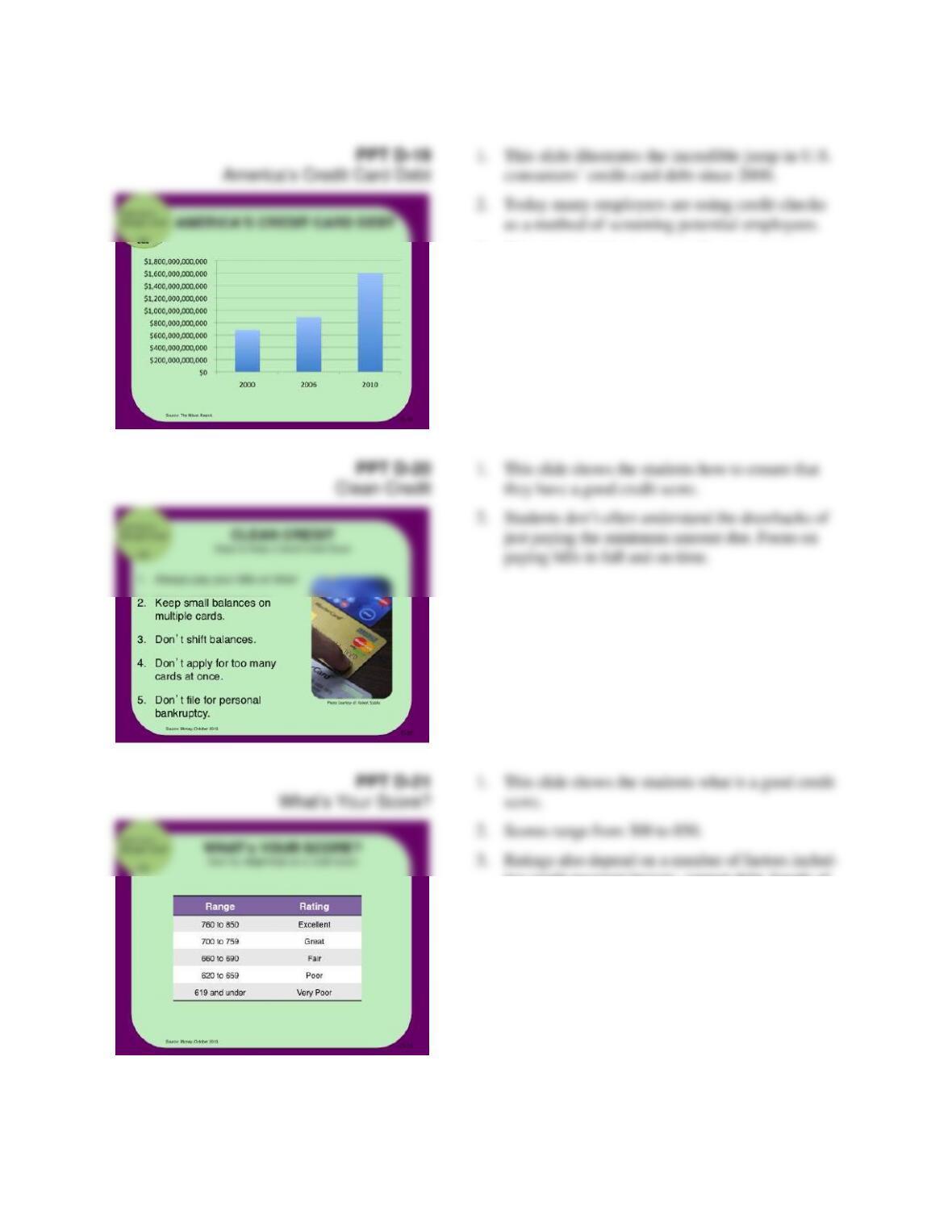

750 to 788 score range.

You’re being judged on five major areas:

1. PAST PAYMENT HISTORY. Your payment punctuality weighs heavily (about 35%)

on your credit score. The more recent your tardiness, the more points you sacrifice.

5. TYPES OF CREDIT. These include credit cards, retail accounts, and installment loans

(like car loans and mortgages). Your use, or overuse, of these has a 10% impact on your

overall score. If you have had no credit, lenders will consider you a higher risk than

someone who has managed credit cards responsibility.

Bonus D – Managing Personal Finances

3. LIMIT CREDIT CARD APPLICATIONS. Each time you apply for credit, a lender’s

inquiry to view your report is noted, which can reduce your score.

4. THINK TWICE BEFORE CANCELLING CARDS. The more companies you owe

money to, the worse your credit score will be. But closing accounts may not improve

your score. This is because you gain points if you only use a small percentage of the total

credit available on your cards. Eliminating accounts can reduce that ratio.

lecture link D-4

AMERICA’S GROWING CREDIT CARD AVERSION

On February 22, 2010, the provisions of Congress’s Credit CARD Act of 2009 came into effect.

The law’s central reform prohibits card companies from suddenly increasing rates on fixed rate

cards. Also, companies are no longer allowed to institute over-the-limit fees without first consulting the

cardholders. If the customers don’t agree to pay the fines, they are simply barred from spending anymore

on their card, thus halting a vicious cycle that drove many people deep into debt.

According to financial experts, consumers are experiencing an “emotional realignment” with their

cards. What was once a convenient purchasing tool has transformed for some into an uncontrollable debt

accumulator. For cardholders already burdened with debt, their natural inclination is to avoid the same

behaviors that led to their problems. Others avoid the danger of credit cards by switching to debit instead.

At the end of 2008, for instance, Visa announced that the purchase volume of debit cards outweighed that

of credit cards for the first time. Still, economists fear Americans may become too afraid of using credit.

Jumping from such an excessive credit boom to almost no card activity at all could cause a slower eco-

nomic recovery in the long run.ii