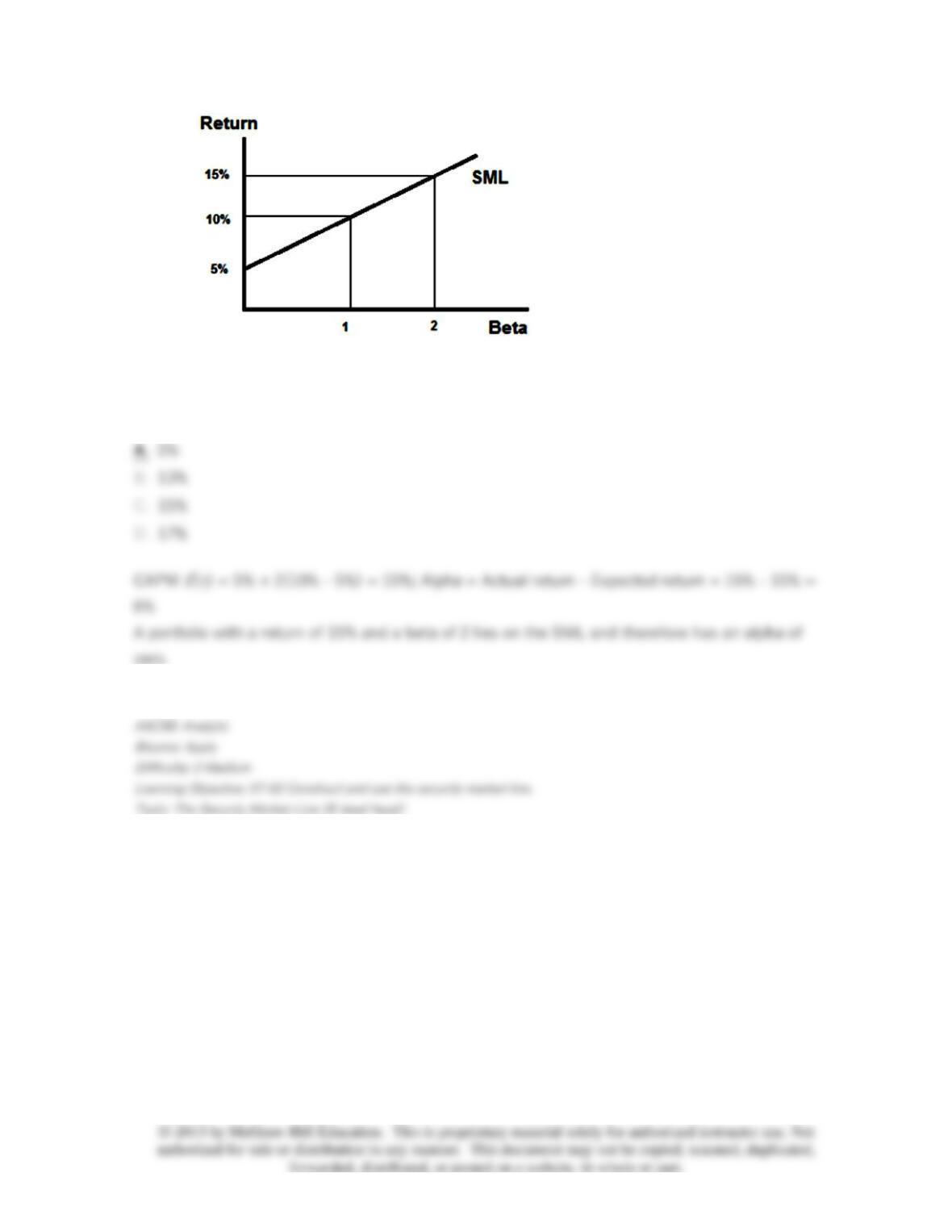

68.

What is the alpha of a portfolio with a beta of 2 and actual return of 15%?

69. If the simple CAPM is valid and all portfolios are priced correctly, which of the situations

below is possible? Consider each situation independently, and assume the risk-free rate is 5%.

70. Two investment advisers are comparing performance. Adviser A averaged a 20% return

with a portfolio beta of 1.5, and adviser B averaged a 15% return with a portfolio beta of 1.2. If the

T-bill rate was 5% and the market return during the period was 13%, which adviser was the better

stock picker?

B

71. The expected return on the market is the risk-free rate plus the _____________.

72. You consider buying a share of stock at a price of $25. The stock is expected to pay a

dividend of $1.50 next year, and your advisory service tells you that you can expect to sell the

stock in 1 year for $28. The stock’s beta is 1.1,

rf

is 6%, and

E

[

rm

] = 16%. What is the stock’s

abnormal return?

73. If the beta of the market index is 1 and the standard deviation of the market index

increases from 12% to 18%, what is the new beta of the market index?

74. According to the CAPM, what is the market risk premium given an expected return on a

security of 13.6%, a stock beta of 1.2, and a risk-free interest rate of 4%?

75. According to the CAPM, what is the expected market return given an expected return on a

security of 15.8%, a stock beta of 1.2, and a risk-free interest rate of 5%?

76. What is the expected return on a stock with a beta of .8, given a risk-free rate of 3.5% and

an expected market return of 15.5%?

77. Research has identified two systematic factors that affect U.S. stock returns. The factors

are growth in industrial production and changes in long-term interest rates. Industrial production

growth is expected to be 3%, and long-term interest rates are expected to increase by 1%. You are

analyzing a stock that has a beta of 1.2 on the industrial production factor and .5 on the interest

rate factor. It currently has an expected return of 12%. However, if industrial production actually

grows 5% and interest rates drop 2%, what is your best guess of the stock’s return?

78. A stock has a beta of 1.3. The systematic risk of this stock is ____________ the stock

market as a whole.

79. There are two independent economic factors,

M

1 and

M

2. The risk-free rate is 5%, and all

stocks have independent firm-specific components with a standard deviation of 25%. Portfolios A

and B are well diversified. Given the data below, which equation provides the correct pricing

model?

80. Using the index model, the alpha of a stock is 3%, the beta is 1.1, and the market return is

10%. What is the residual given an actual return of 15%?

81. The risk premium for exposure to aluminum commodity prices is 4%, and the firm has a

beta relative to aluminum commodity prices of .6. The risk premium for exposure to GDP changes

is 6%, and the firm has a beta relative to GDP of 1.2. If the risk-free rate is 4%, what is the

expected return on this stock?

82. The two-factor model on a stock provides a risk premium for exposure to market risk of

9%, a risk premium for exposure to interest rate risk of (-1.3%), and a risk-free rate of 3.5%. The

beta for exposure to market risk is 1, and the beta for exposure to interest rate risk is also 1. What

is the expected return on the stock?

83. The risk premium for exposure to exchange rates is 5%, and the firm has a beta relative to

exchange rates of .4. The risk premium for exposure to the consumer price index is -6%, and the

firm has a beta relative to the CPI of .8. If the risk-free rate is 3%, what is the expected return on

this stock?

84. The two-factor model on a stock provides a risk premium for exposure to market risk of

12%, a risk premium for exposure to silver commodity prices of 3.5%, and a risk-free rate of 4%.

The beta for exposure to market risk is 1, and the beta for exposure to commodity prices is also 1.

What is the expected return on the stock?

85. The measure of risk used in the capital asset pricing model is ___________.