64.

This stock has greater systematic risk than a stock with a beta of ___.

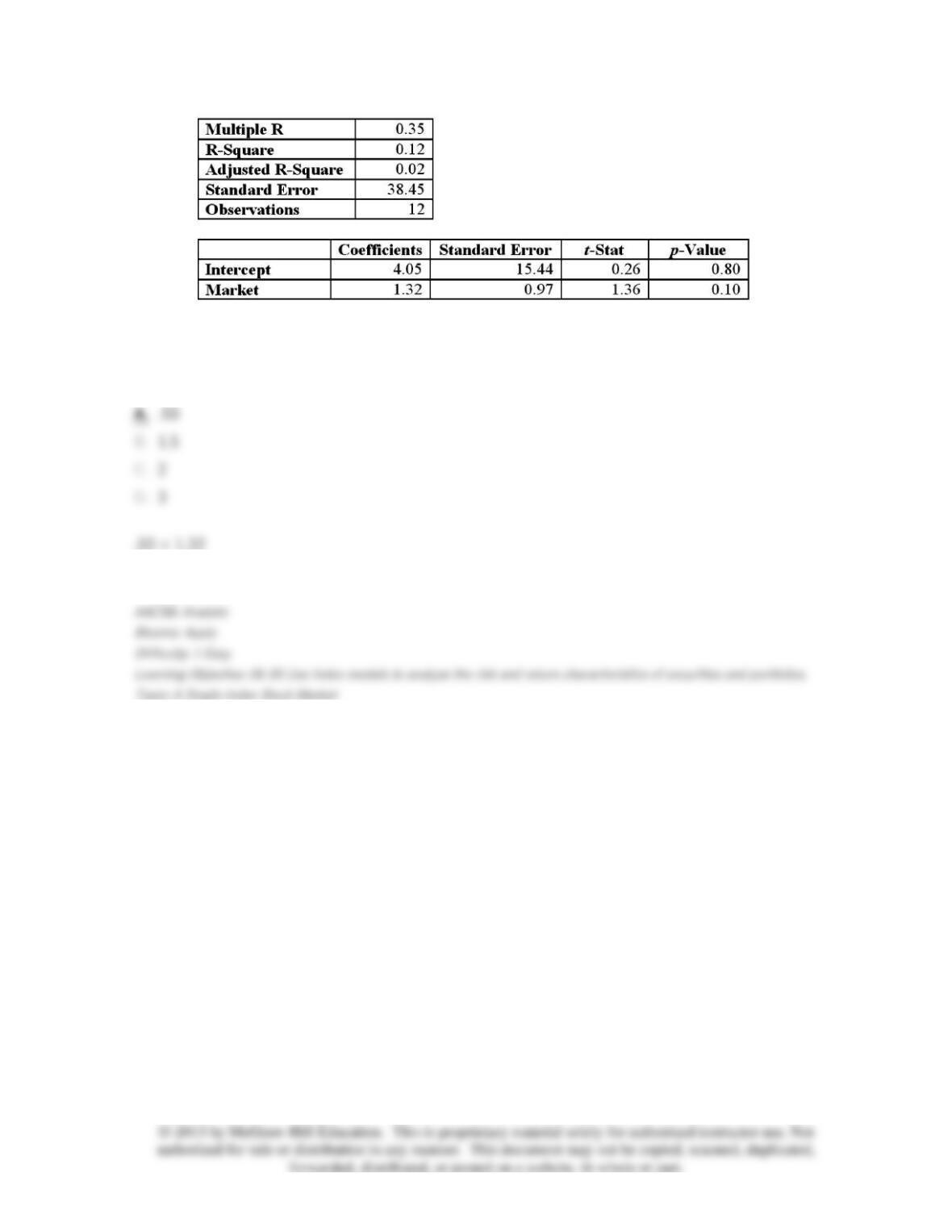

65.

The characteristic line for this stock is

R

stock = ___ + ___

R

market.

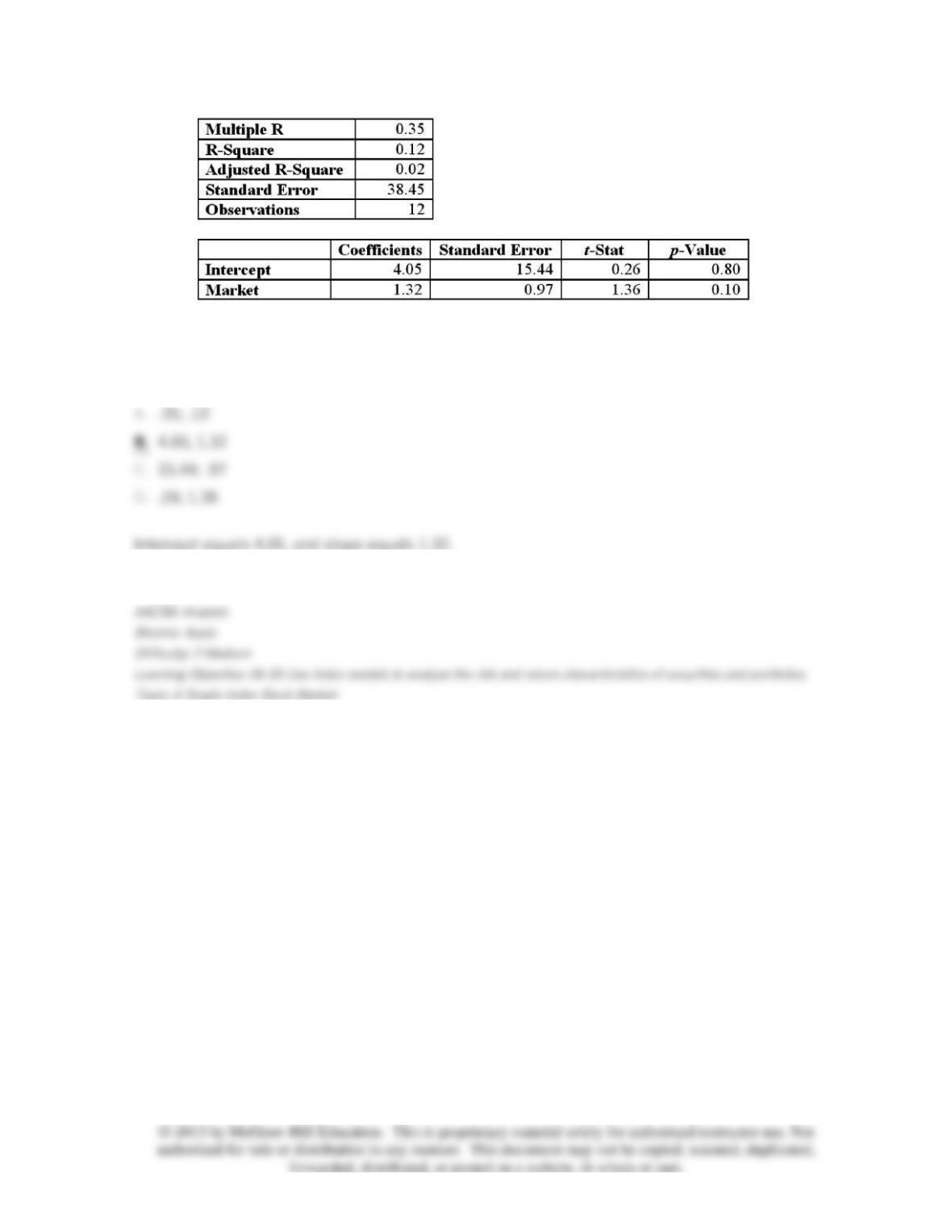

66.

_______________ percent of the variance is explained by this regression.

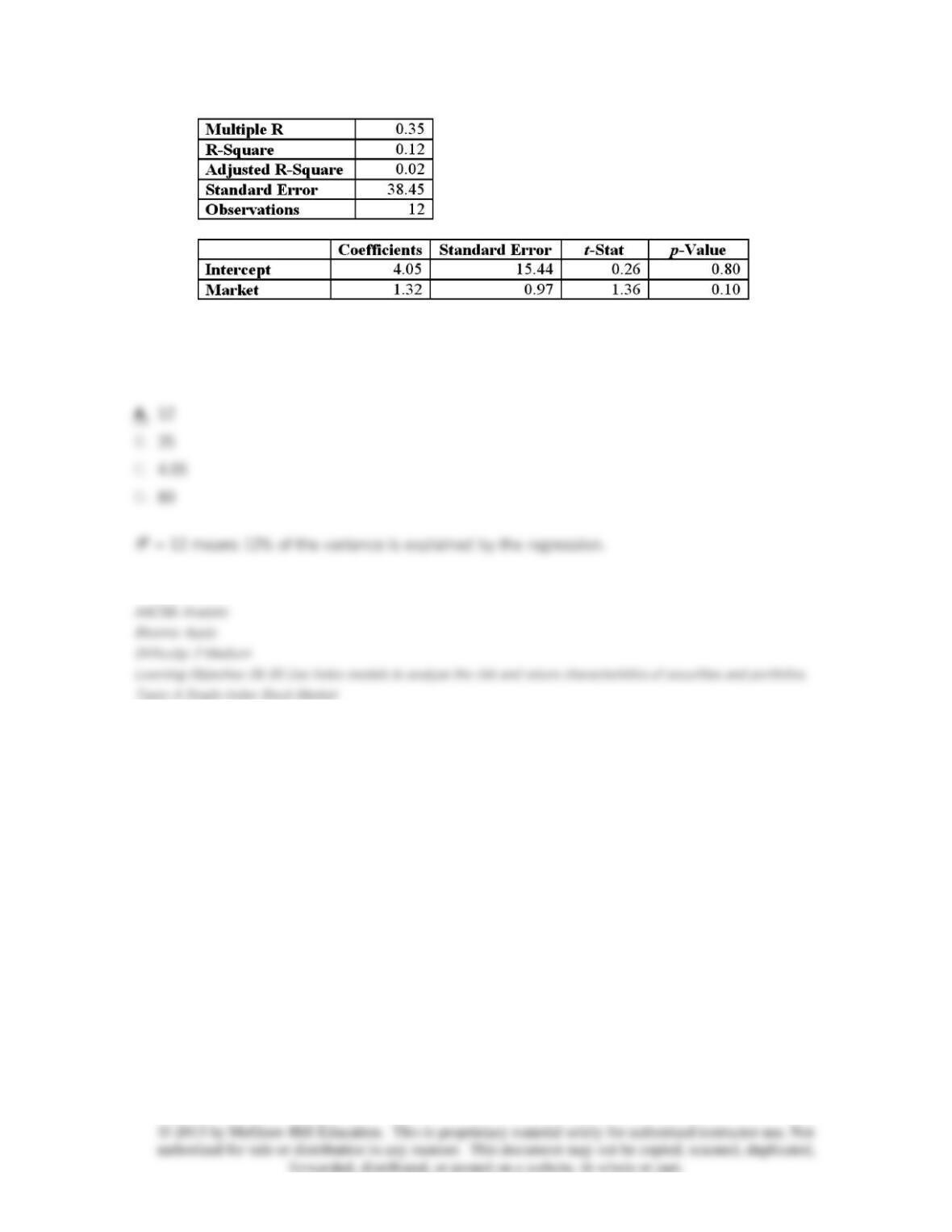

67.

The stock is ______ riskier than the typical stock.

68. Decreasing the number of stocks in a portfolio from 50 to 10 would likely

________________.

69. If you want to know the portfolio standard deviation for a three–stock portfolio, you will

have to ______.

70. Which of the following correlation coefficients will produce the least diversification

benefit?

71. Which of the following correlation coefficients will produce the most diversification

benefits?

72. What is the most likely correlation coefficient between a stock-index mutual fund and the

S&P 500?

73. Investing in two assets with a correlation coefficient of -.5 will reduce what kind of risk?

74. Investing in two assets with a correlation coefficient of 1 will reduce which kind of risk?

75. A portfolio of stocks fluctuates when the Treasury yields change. Since this risk cannot be

eliminated through diversification, it is called __________.

76. As you lengthen the time horizon of your investment period and decide to invest for

multiple years, you will find that:

I. The average risk per year may be smaller over longer investment horizons.

II. The overall risk of your investment will compound over time.

III. Your overall risk on the investment will fall.

77. You are considering adding a new security to your portfolio. To decide whether you should

add the security, you need to know the security’s:

I. Expected return

II. Standard deviation

III. Correlation with your portfolio

78. Which of the following is a correct expression concerning the formula for the standard

deviation of returns of a two-asset portfolio where the correlation coefficient is positive?

79. What is the standard deviation of a portfolio of two stocks given the following data: Stock

A has a standard deviation of 18%. Stock B has a standard deviation of 14%. The portfolio

contains 40% of stock A, and the correlation coefficient between the two stocks is -.23.

80. What is the standard deviation of a portfolio of two stocks given the following data: Stock

A has a standard deviation of 30%. Stock B has a standard deviation of 18%. The portfolio

contains 60% of stock A, and the correlation coefficient between the two stocks is –1.

81. The expected return of a portfolio is 8.9%, and the risk-free rate is 3.5%. If the portfolio

standard deviation is 12%, what is the reward-to-variability ratio of the portfolio?

82. A project has a 60% chance of doubling your investment in 1 year and a 40% chance of

losing half your money. What is the standard deviation of this investment?

rp

83. A project has a 50% chance of doubling your investment in 1 year and a 50% chance of

losing half your money. What is the expected return on this investment project?

84. The figures below show plots of monthly excess returns for two stocks plotted against

excess returns for a market index.

Which stock is likely to further reduce risk for an investor currently holding her portfolio in a well–

diversified portfolio of common stock?

85. The figures below show plots of monthly excess returns for two stocks plotted against

excess returns for a market index.

Which stock is riskier to a nondiversified investor who puts all his money in only one of these

stocks?