39. An investor can design a risky portfolio based on two stocks, A and B. Stock A has an

expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return

of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns

of A and B is .4. The risk-free rate of return is 5%. The standard deviation of the returns on the

optimal risky portfolio is _________.

σ

rp

40. An investor can design a risky portfolio based on two stocks, A and B. The standard

deviation of return on stock A is 24%, while the standard deviation on stock B is 14%. The

correlation coefficient between the returns on A and B is .35. The expected return on stock A is

25%, while on stock B it is 11%. The proportion of the minimum-variance portfolio that would be

invested in stock B is approximately _________.

41. An investor can design a risky portfolio based on two stocks, A and B. The standard

deviation of return on stock A is 20%, while the standard deviation on stock B is 15%. The

correlation coefficient between the returns on A and B is 0%. The expected return on the

minimum-variance portfolio is approximately _________.

42. An investor can design a risky portfolio based on two stocks, A and B. The standard

deviation of return on stock A is 20%, while the standard deviation on stock B is 15%. The

correlation coefficient between the returns on A and B is 0%. The standard deviation of return on

the minimum-variance portfolio is _________.

43. A measure of the riskiness of an asset held in isolation is ____________.

44. Semitool Corp. has an expected excess return of 6% for next year. However, for every

unexpected 1% change in the market, Semitool’s return responds by a factor of 1.2. Suppose it

turns out that the economy and the stock market do better than expected by 1.5% and Semitool’s

products experience more rapid growth than anticipated, pushing up the stock price by another

1%. Based on this information, what was Semitool’s actual excess return?

45. The part of a stock’s return that is systematic is a function of which of the following

variables?

I. Volatility in excess returns of the stock market

II. The sensitivity of the stock’s returns to changes in the stock market

III. The variance in the stock’s returns that is unrelated to the overall stock market

46. Stock A has a beta of 1.2, and stock B has a beta of 1. The returns of stock A are ______

sensitive to changes in the market than are the returns of stock B.

47. Which risk can be partially or fully diversified away as additional securities are added to a

portfolio?

I. Total risk

II. Systematic risk

III. Firm-specific risk

48. According to Tobin’s separation property, portfolio choice can be separated into two

independent tasks consisting of __________ and __________.

49. You are constructing a scatter plot of excess returns for stock A versus the market index.

If the correlation coefficient between stock A and the index is -1, you will find that the points of

the scatter diagram ___________ and the line of best fit has a ______________.

50. The term

excess return

refers to ______________.

51. You are recalculating the risk of ACE stock in relation to the market index, and you find

that the ratio of the systematic variance to the total variance has risen. You must also find that

the ____________.

52. A stock has a correlation with the market of .45. The standard deviation of the market is

21%, and the standard deviation of the stock is 35%. What is the stock’s beta?

53. The values of beta coefficients of securities are __________.

54. A security’s beta coefficient will be negative if ____________.

55. The market value weighted-average beta of firms included in the market index will always

be _____________.

56. Diversification can reduce or eliminate __________ risk.

57. To construct a riskless portfolio using two risky stocks, one would need to find two stocks

with a correlation coefficient of ________.

58. Some diversification benefits can be achieved by combining securities in a portfolio as

long as the correlation between the securities is _____________.

59. If an investor does not diversify his portfolio and instead puts all of his money in one

stock, the appropriate measure of security risk for that investor is the ________.

60. Which of the following provides the best example of a systematic-risk event?

62. You find that the annual Sharpe ratio for stock A returns is equal to 1.8. For a 3-year

holding period, the Sharpe ratio would equal _______.

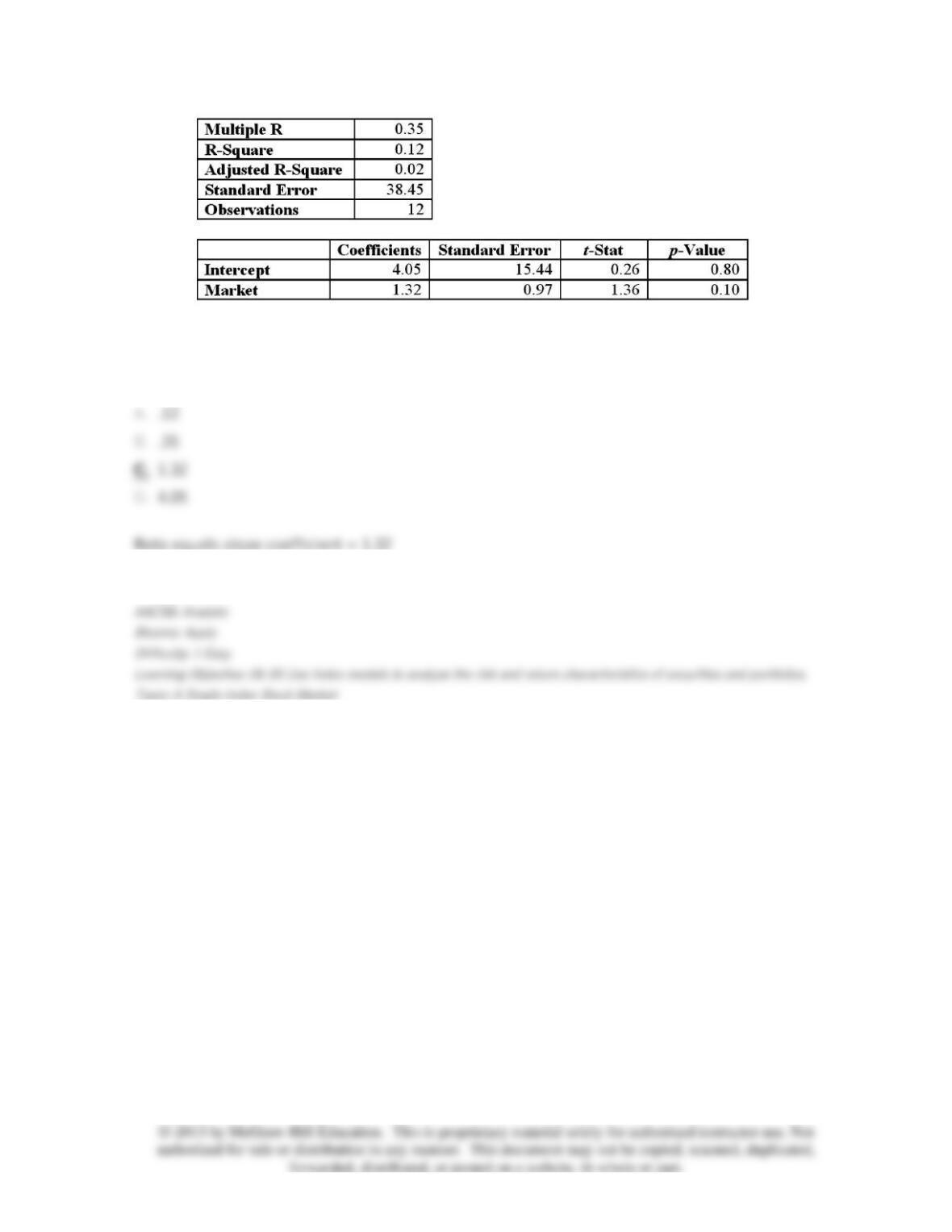

63.

The beta of this stock is ____.