62. You are considering investing $1,000 in a complete portfolio. The complete portfolio is

composed of Treasury bills that pay 5% and a risky portfolio,

P

, constructed with two risky

securities, X and Y. The optimal weights of X and Y in

P

are 60% and 40%, respectively. X has an

expected rate of return of 14%, and Y has an expected rate of return of 10%. To form a complete

portfolio with an expected rate of return of 11%, you should invest __________ of your complete

portfolio in Treasury bills.

63. You are considering investing $1,000 in a complete portfolio. The complete portfolio is

composed of Treasury bills that pay 5% and a risky portfolio,

P

, constructed with two risky

securities, X and Y. The optimal weights of X and Y in

P

are 60% and 40% respectively. X has an

expected rate of return of 14%, and Y has an expected rate of return of 10%. To form a complete

portfolio with an expected rate of return of 8%, you should invest approximately __________ in the

risky portfolio. This will mean you will also invest approximately __________ and __________ of your

complete portfolio in security X and Y, respectively.

64. You are considering investing $1,000 in a complete portfolio. The complete portfolio is

composed of Treasury bills that pay 5% and a risky portfolio,

P

, constructed with two risky

securities, X and Y. The optimal weights of X and Y in

P

are 60% and 40%, respectively. X has an

expected rate of return of 14%, and Y has an expected rate of return of 10%. If you decide to hold

25% of your complete portfolio in the risky portfolio and 75% in the Treasury bills, then the dollar

values of your positions in X and Y, respectively, would be __________ and _________.

65. You are considering investing $1,000 in a complete portfolio. The complete portfolio is

composed of Treasury bills that pay 5% and a risky portfolio,

P

, constructed with two risky

securities, X and Y. The optimal weights of X and Y in

P

are 60% and 40%, respectively. X has an

expected rate of return of 14%, and Y has an expected rate of return of 10%. The dollar values of

your positions in X, Y, and Treasury bills would be _________, __________, and __________,

respectively, if you decide to hold a complete portfolio that has an expected return of 8%.

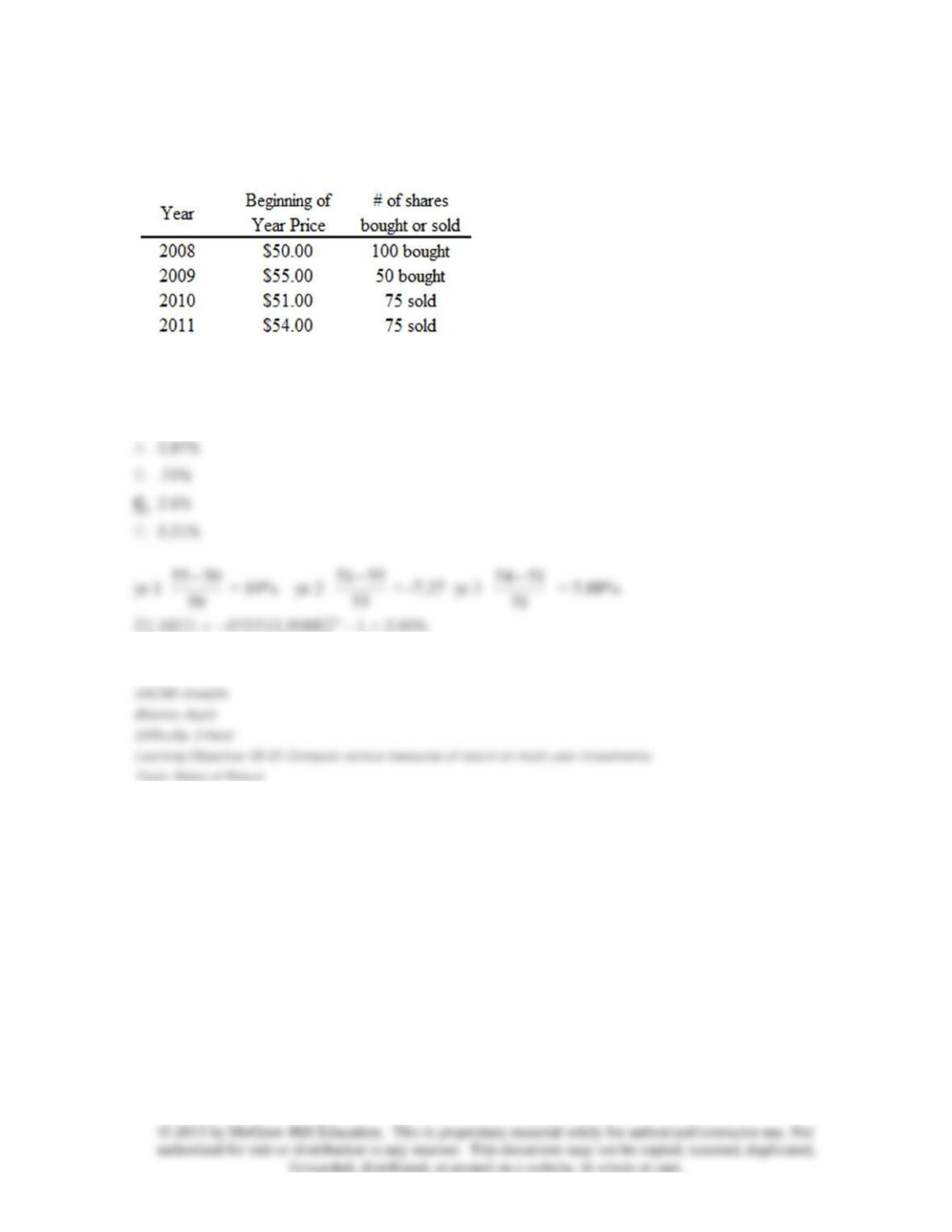

66. You have the following rates of return for a risky portfolio for several recent years:

If you invested $1,000 at the beginning of 2008, your investment at the end of 2011 would be

worth ___________.

67. You have the following rates of return for a risky portfolio for several recent years:

The annualized (geometric) average return on this investment is _____.

68. A security with normally distributed returns has an annual expected return of 18% and

standard deviation of 23%. The probability of getting a return between -28% and 64% in any one

year is _____.

69. The Manhawkin Fund has an expected return of 16% and a standard deviation of 20%. The

risk-free rate is 4%. What is the reward–to-volatility ratio for the Manhawkin Fund?

70. From 1926 to 2010 the world stock portfolio offered _____ return and _____ volatility than

the portfolio of large U.S. stocks.

71. The price of a stock is $55 at the beginning of the year and $50 at the end of the year. If

the stock paid a $3 dividend and inflation was 3%, what is the real holding-period return for the

year?

72. The price of a stock is $38 at the beginning of the year and $41 at the end of the year. If

the stock paid a $2.50 dividend, what is the holding-period return for the year?

73. You invest all of your money in 1-year T-bills. Which of the following statements is (are)

correct?

I. Your nominal return on the T-bills is riskless.

II. Your real return on the T-bills is riskless.

III. Your nominal Sharpe ratio is zero.

74. Which one of the following would be considered a risk-free asset in real terms as opposed

to nominal?

75. What is the geometric average return of the following quarterly returns: 3%, 5%, 4%, and

7%?

76. What is the geometric average return over 1 year if the quarterly returns are 8%, 9%, 5%,

and 12%?

77. If the nominal rate of return on investment is 6% and inflation is 2% over a holding period,

what is the real rate of return on this investment?

78. According to historical data, over the long run which of the following assets has the best

chance to provide the best after-inflation, after-tax rate of return?

79. The buyer of a new home is quoted a mortgage rate of .5% per month. What is the APR on

the loan?

80. A loan for a new car costs the borrower .8% per month. What is the EAR?

81. The CAL provided by combinations of 1-month T-bills and a broad index of common

stocks is called the ______.

82. Which of the following arguments supporting passive investment strategies is (are)

correct?

I. Active trading strategies may not guarantee higher returns but guarantee higher costs.

II. Passive investors can free-ride on the activity of knowledge investors whose trades force prices

to reflect currently available information.

III. Passive investors are guaranteed to earn higher rates of return than active investors over

sufficiently long time horizons.

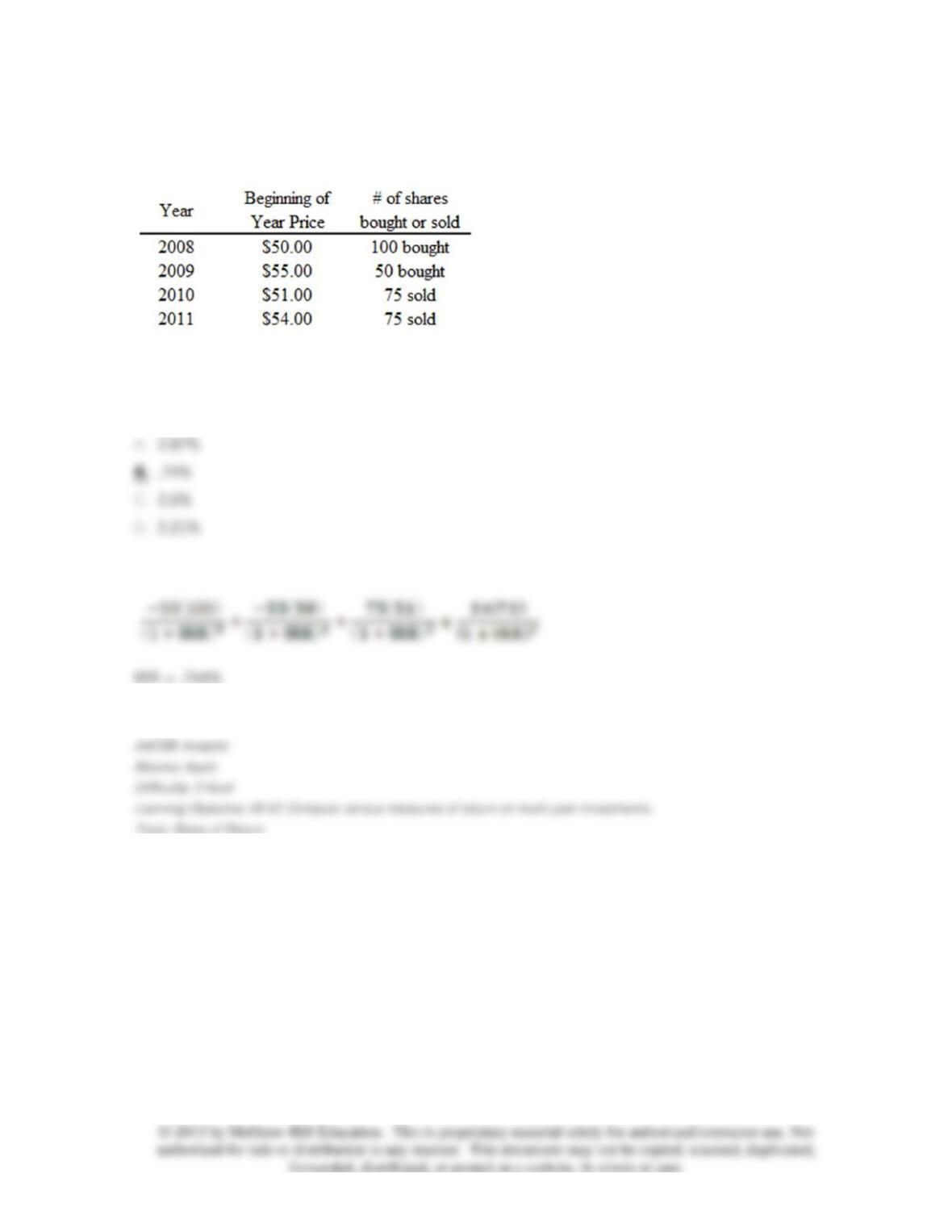

83. You have the following rates of return for a risky portfolio for several recent years. Assume

that the stock pays no dividends.

What is the geometric average return for the period?

84. You have the following rates of return for a risky portfolio for several recent years. Assume

that the stock pays no dividends.

What is the dollar-weighted return over the entire time period?