42. WEBS are _____________.

43. You are a U.S. investor who purchased British securities for 3,500 pounds 1 year ago when

the British pound cost $1.35. No dividends were paid on the British securities in the past year.

Your total return based on U.S. dollars was __________ if the value of the securities is now 4,200

pounds and the pound is worth $1.15.

44. Real U.S. interest rates move above Japanese interest rates. If you believe that Japanese

interest rates won’t move and that interest rate parity will hold, then ____________.

45. Suppose a U.S. investor wants to invest in a British firm currently selling for ₤50 per share.

The investor has $7,000 to invest, and the current exchange rate is $1.40/₤.

How many shares can the investor purchase?

46. Suppose a U.S. investor wants to invest in a British firm currently selling for ₤50 per share.

The investor has $7,000 to invest, and the current exchange rate is $1.40/₤.

After 1 year, the exchange rate is unchanged and the share price is ₤55. What is the dollar–

denominated return?

47. Suppose a U.S. investor wants to invest in a British firm currently selling for ₤50 per share.

The investor has $7,000 to invest, and the current exchange rate is $1.40/₤.

After 1 year, the exchange rate is unchanged and the share price is ₤55. What is the pound–

denominated return?

48. Suppose a U.S. investor wants to invest in a British firm currently selling for ₤50 per share.

The investor has $7,000 to invest, and the current exchange rate is $1.40/₤.

After 1 year, the exchange rate is $1.60/₤ and the share price is ₤55. What is the dollar-

denominated return?

49. Suppose a U.S. investor wants to invest in a British firm currently selling for ₤50 per share.

The investor has $7,000 to invest, and the current exchange rate is $1.40/₤.

After 1 year, the exchange rate is $1.50/₤ and the share price is ₤45. How much of your dollar-

denominated return is due to the currency change?

50. You find that the exchange rate quote for the yen is 121 yen per dollar. This is an example

of ________ quote. You also find that the euro is worth $1.33. This second quote is an example of

_______ quote.

51. Among emerging countries the largest equity market in 2011 was located in

_____________.

52. In the PRS country composite risk ratings, a score of ______ represents the least risky and

a score of _____ represents the most risky.

53. Which emerging country had the highest percentage growth in market capitalization

during the 2000-2011 period?

54. The dollar-per-euro spot rate is 1.2 when an importer of French wines places an order. Six

months later, when she takes delivery, the spot rate is 1.3 dollars per euro. If her original invoice

was for 30,000 euro, what is her gain or loss due to exchange rate risk?

55. An importer of televisions from Japan has a contract to purchase a shipment of televisions

for 2 million yen. The spot rate increases from 105 yen per dollar to 108 yen per dollar. What is the

importer’s gain or loss?

56. A country has a PRS political risk rating of 75, a financial score of 40, and an economic

score of 35. The country’s composite rating is _________.

57. The risk-free rate in the United States is 2.5%, and the risk-free rate in Europe is 3.2%. If

the spot rate of dollars per euro is 1.32, what is the likely forward rate in terms of dollars per

euro?

58. The risk-free rate in the United States is 4%, and the risk-free rate in Japan is 1.2%. If the

spot rate of yen to dollars is 105, what is the likely yen-per-dollar forward rate?

59. The yen-per-dollar spot rate is 104. The yen-per-dollar forward rate is 107. If the U.S. risk–

free rate is 2.4%, what is the likely yen risk-free rate?

60. In the PRS financial risk ratings, the United States rates poorly because of the U.S.

________.

I. Large budget deficit

II. Large trade deficit

III. Large amount of total debt

61. The major participants who directly purchase securities in the capital markets of other

countries are predominantly ____________.

62. Of the following, which is the most commonly used international index?

63. WEBS differ from mutual funds in that:

I. WEBS can be shorted.

II. WEBS trade continuously on the AMEX.

III. WEBS are passively managed.

64. The variation in the betas of emerging markets suggests that ____________.

65. One year U.S. interest rates are 5%, and European interest rates are 7%. The spot euro

direct exchange rate quote is 1.32, and the 1-year forward rate direct quote is 1.35. If you can

borrow either $1 million or €1 million to start with, what would be your dollar profits from interest

arbitrage based on these data?

66. One year U.S. interest rates are 7%, and European interest rates are 5%. The spot euro

direct exchange rate quote is 1.30 and the 1-year forward rate direct quote is 1.25. If you can

borrow either $1 million or €1 million to start with, what would be your dollar profits from interest

arbitrage based on these data?

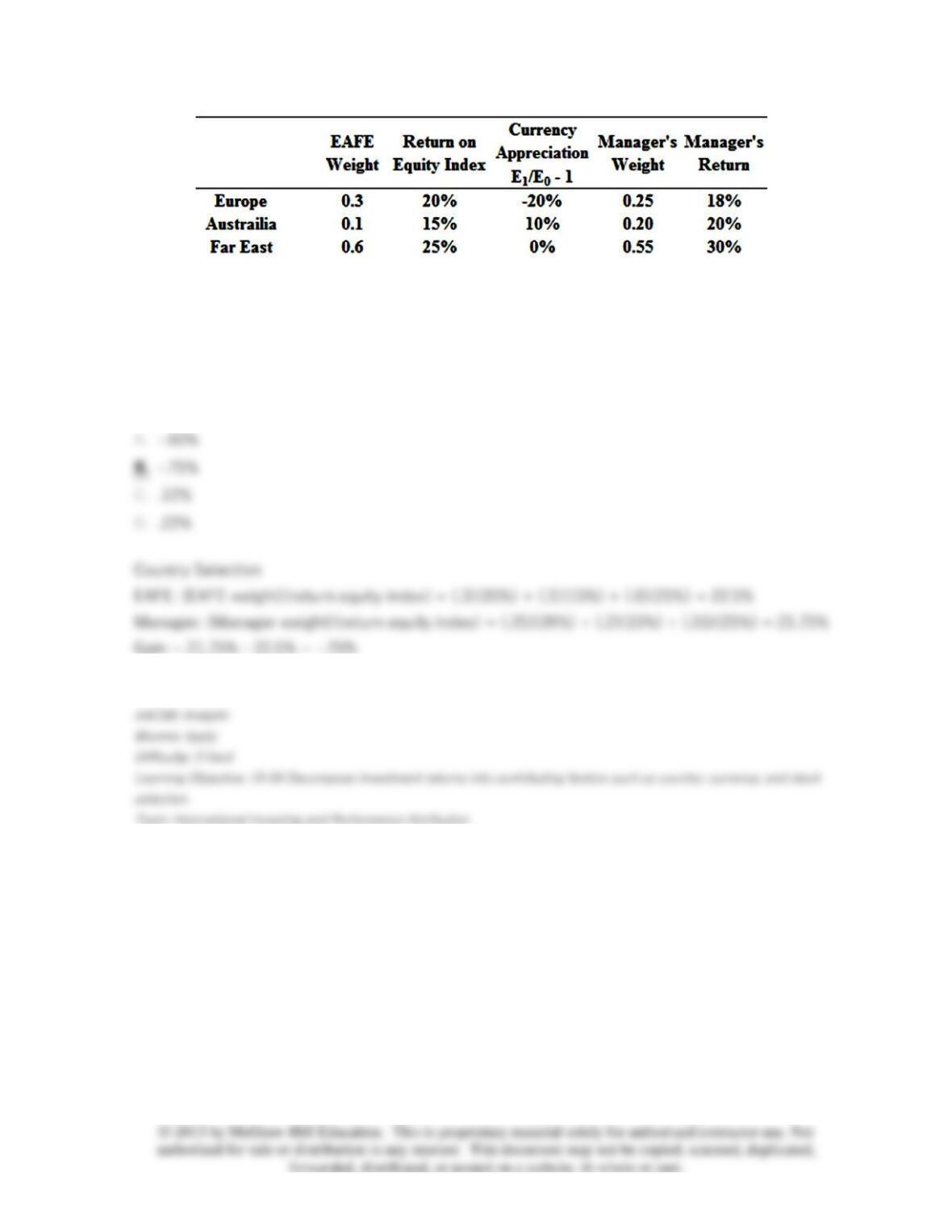

67.

All exchange rates are expressed as units of foreign currency that can be purchased with one U.S.

dollar. Answer the following about decomposing the manager’s performance.

What is the difference in return of the manager’s portfolio due to currency selection?

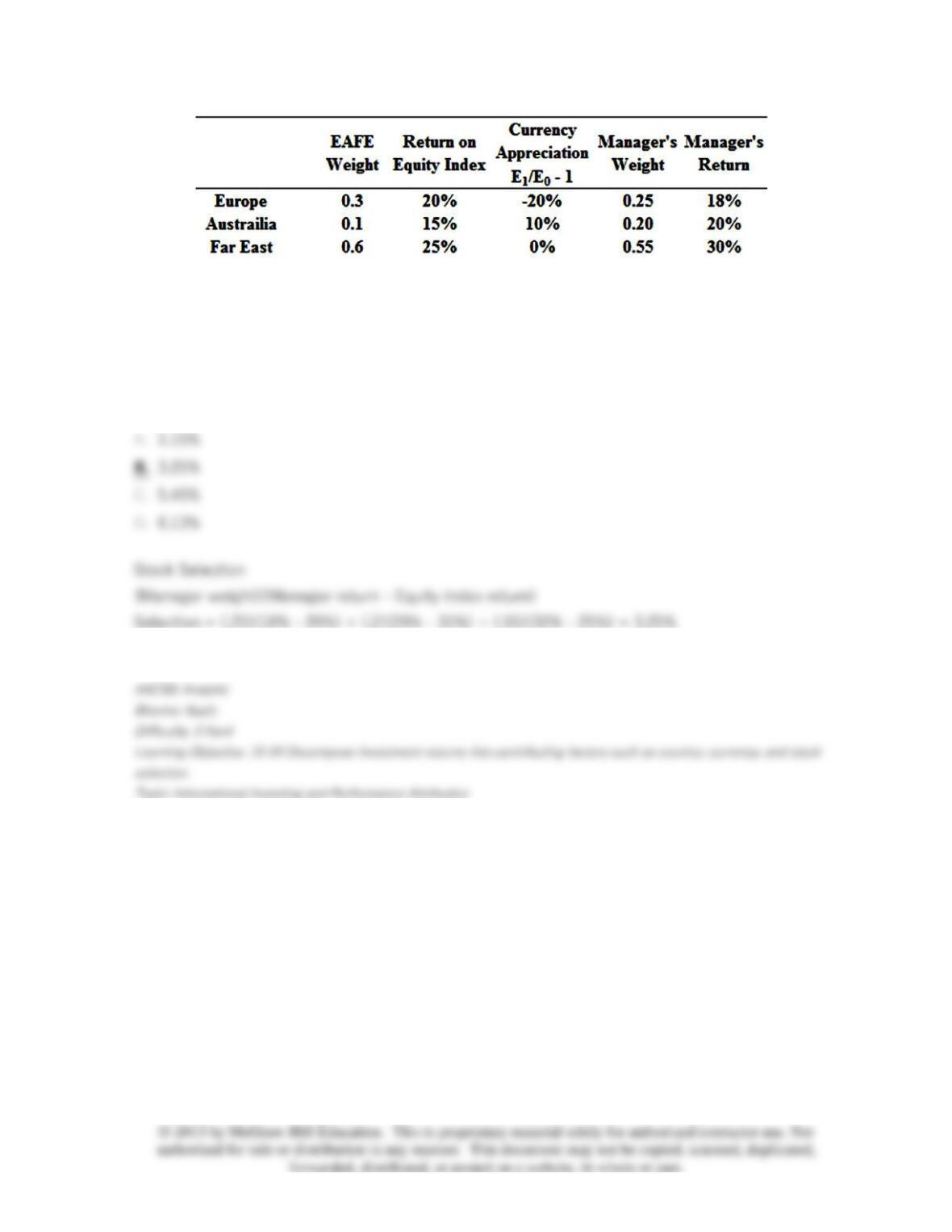

68.

All exchange rates are expressed as units of foreign currency that can be purchased with one U.S.

dollar. Answer the following about decomposing the manager’s performance.

What is the difference in return of the manager’s portfolio due to country selection?

69.

All exchange rates are expressed as units of foreign currency that can be purchased with one U.S.

dollar. Answer the following about decomposing the manager’s performance.

What is the difference in return of the manager’s portfolio due to stock selection?