Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

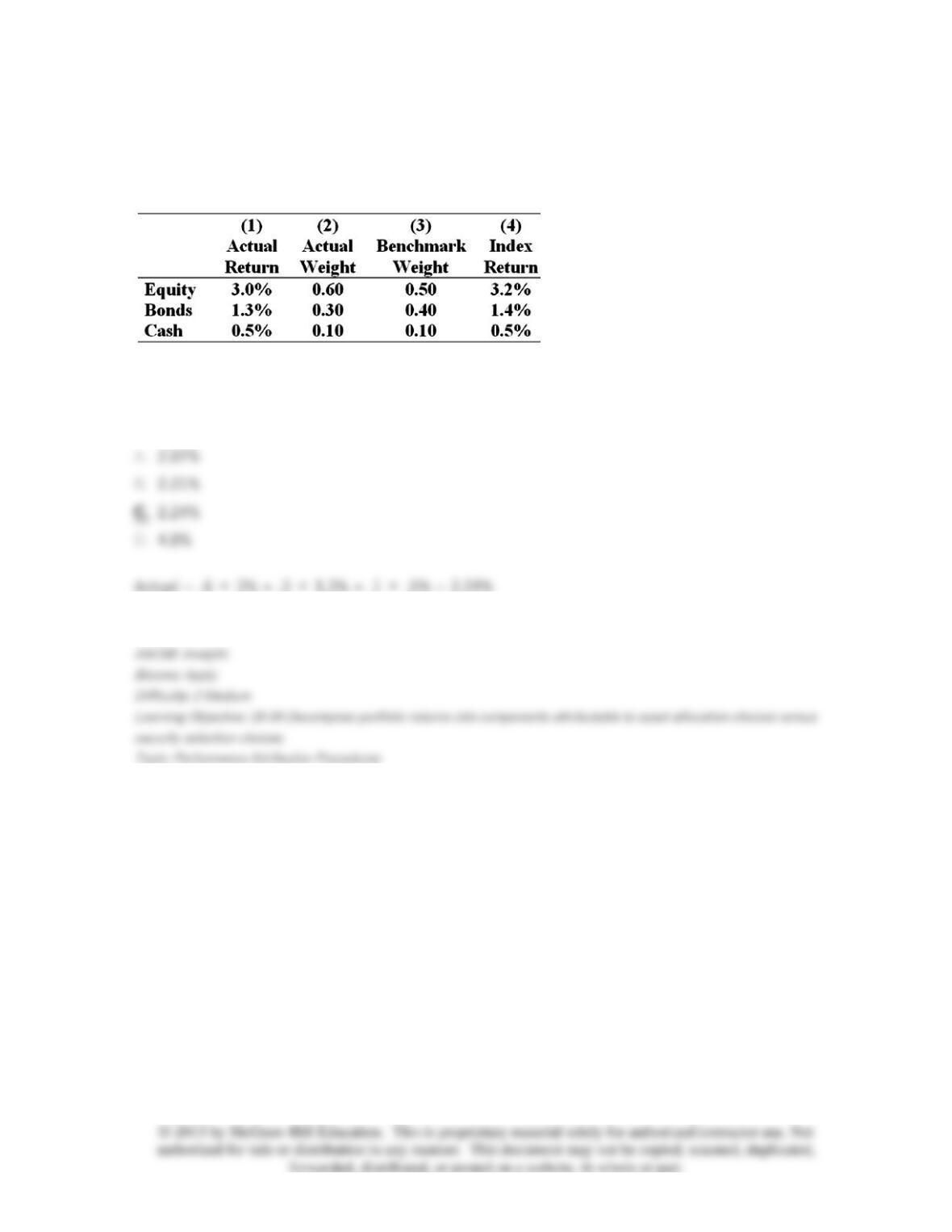

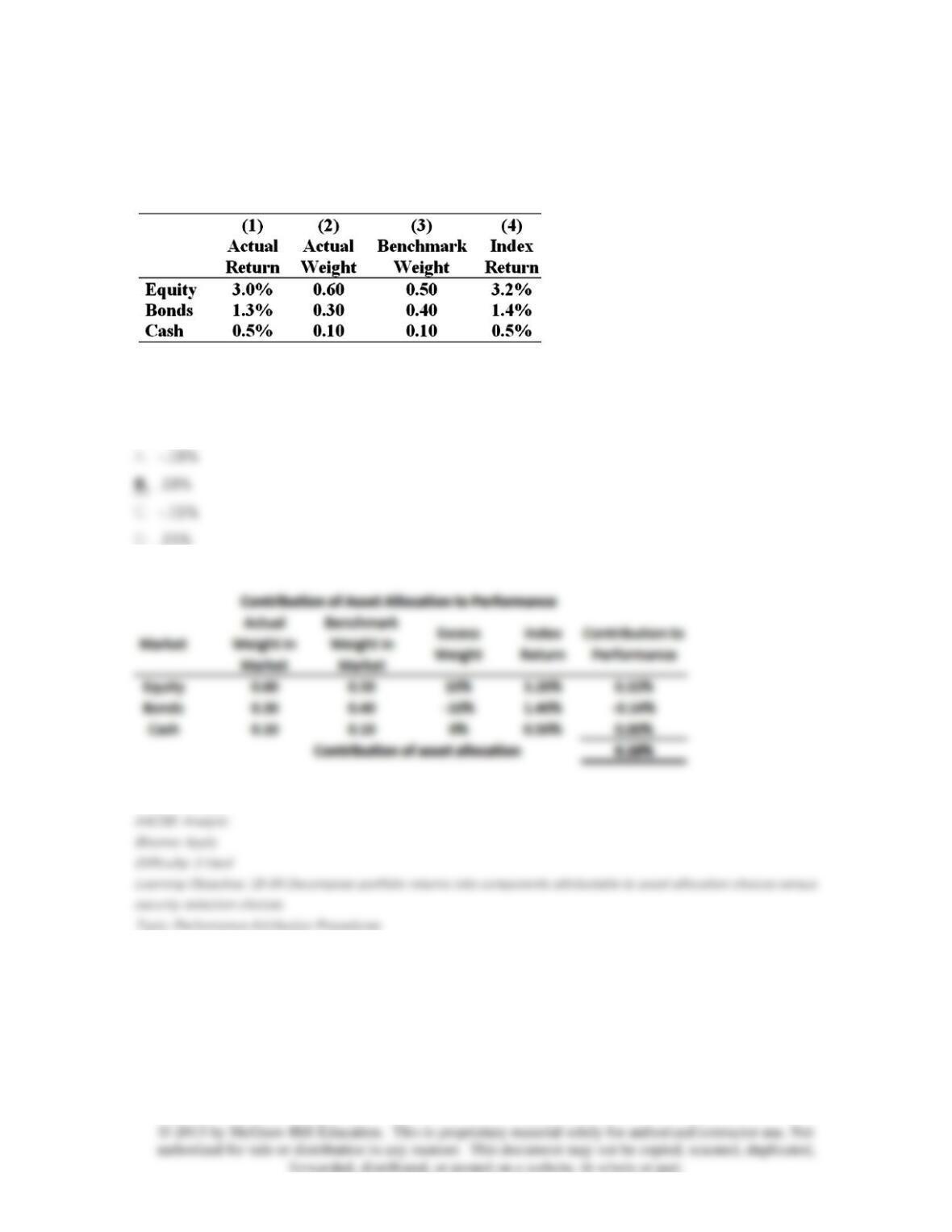

62. The table presents the actual return of each sector of the manager's portfolio in column

(1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral

sector allocations in column (3), and the returns of sector indexes in column 4.

What was the manager's return in the month?

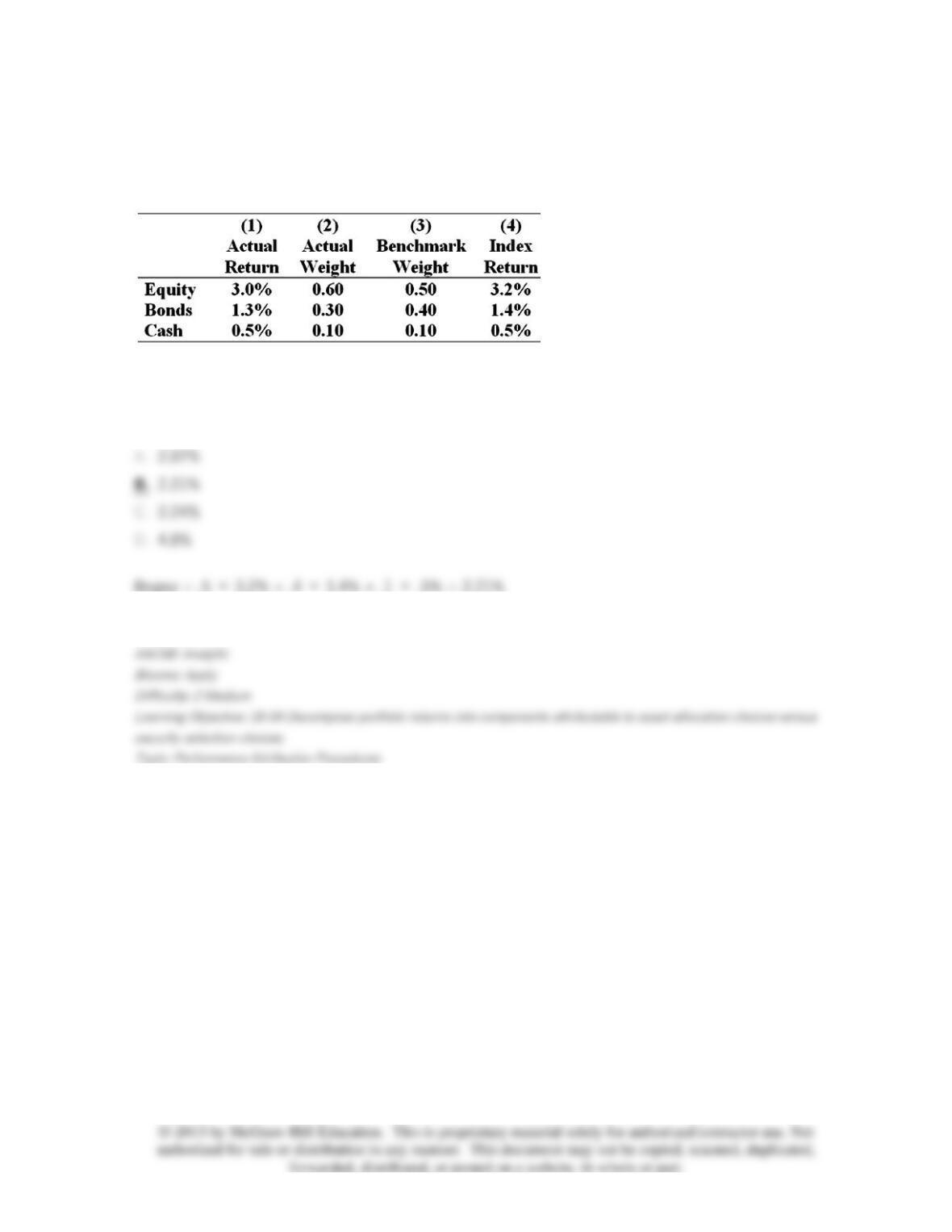

63. The table presents the actual return of each sector of the manager's portfolio in column

(1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral

sector allocations in column (3), and the returns of sector indexes in column 4.

What was the bogey's return in the month?

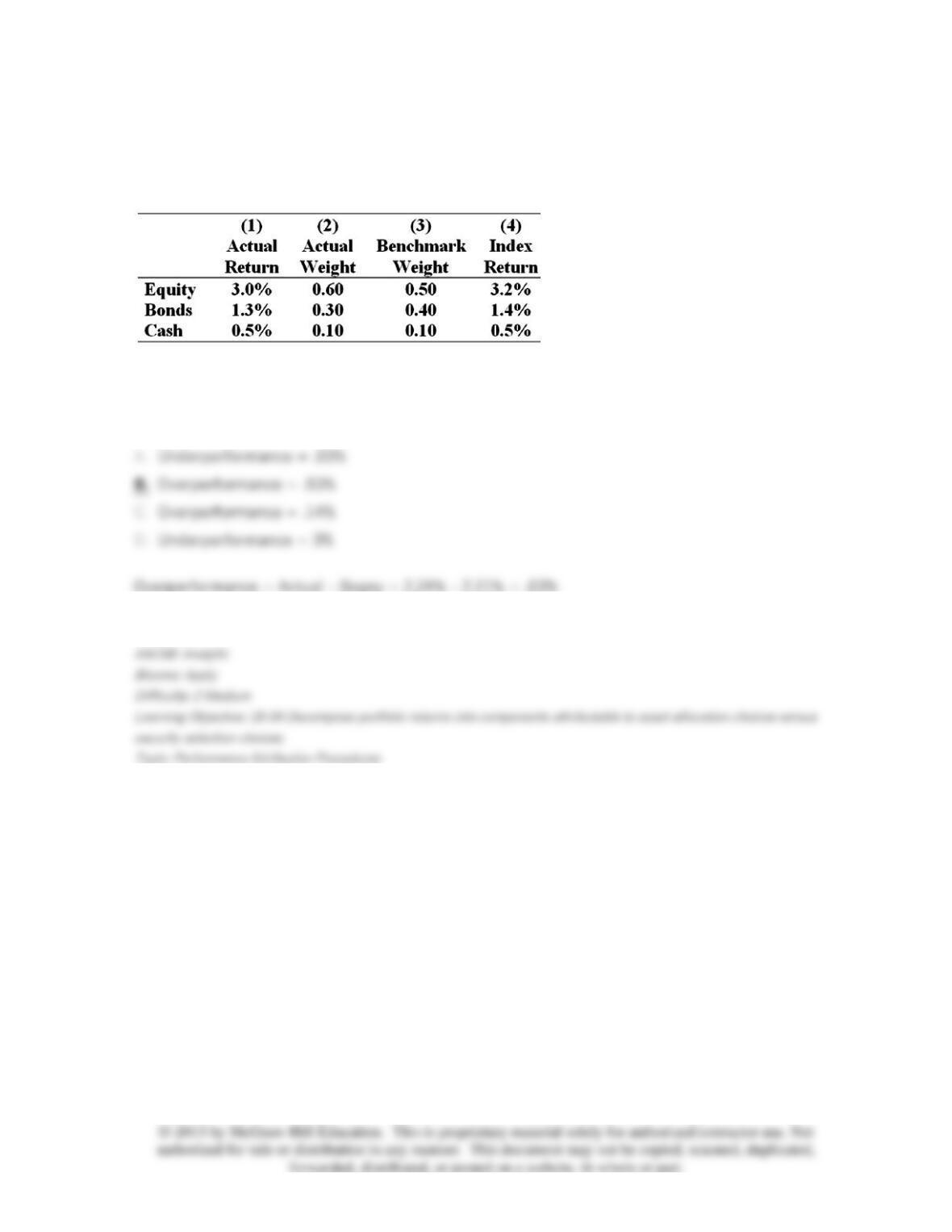

64. The table presents the actual return of each sector of the manager's portfolio in column

(1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral

sector allocations in column (3), and the returns of sector indexes in column 4.

What was the manager's over- or underperformance for the month?

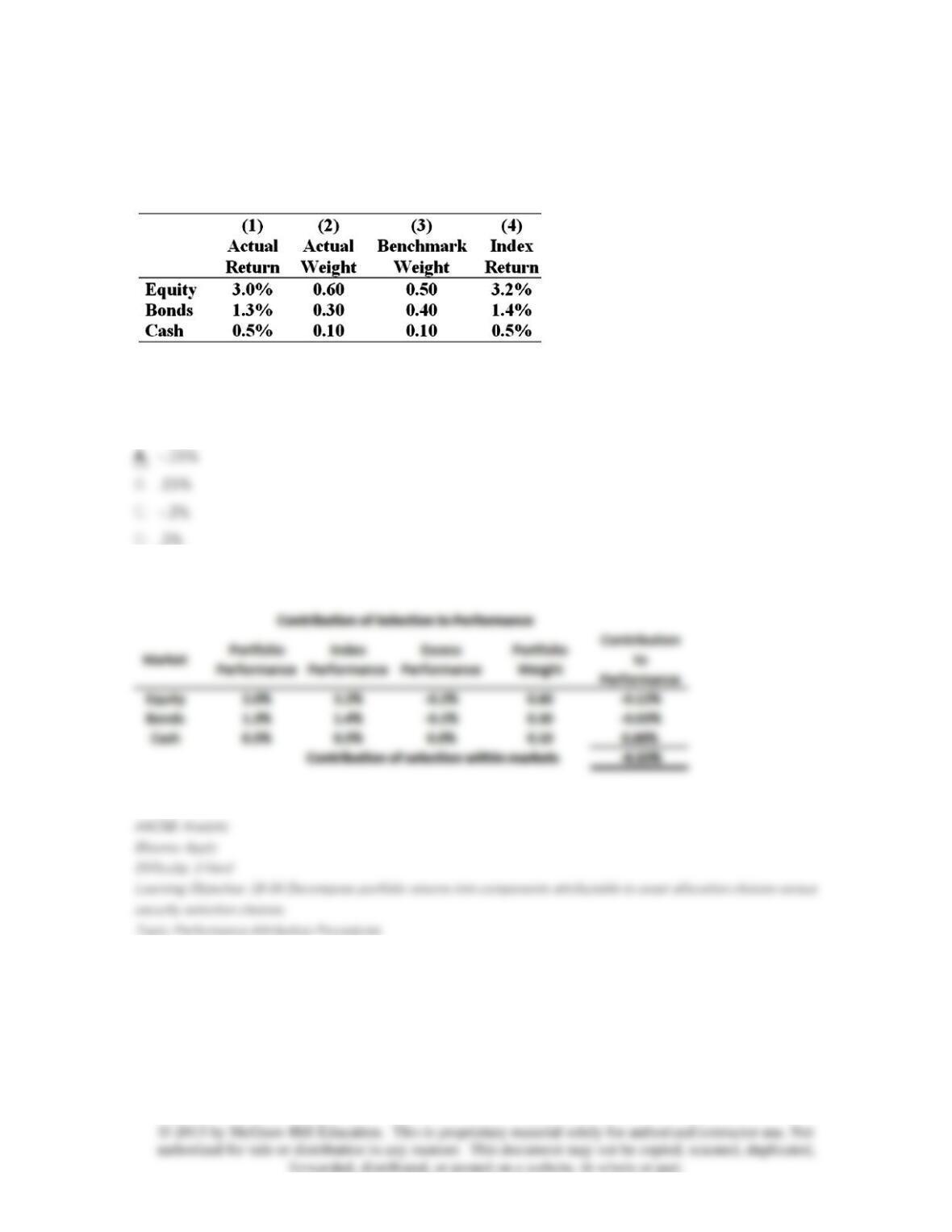

65. The table presents the actual return of each sector of the manager's portfolio in column

(1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral

sector allocations in column (3), and the returns of sector indexes in column 4.

What is the contribution of security selection to relative performance?

66. The table presents the actual return of each sector of the manager's portfolio in column

(1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral

sector allocations in column (3), and the returns of sector indexes in column 4.

What is the contribution of asset allocation to relative performance?

67. Morningstar's RAR produce results that are similar but not identical to ________.

68. The Treynor-Black model assumes that security markets are _________.

69. The information ratio is equal to the stock's ____ divided by its ______.

70. Empirical tests to date show ______________.

71. A portfolio generates an annual return of 13%, a beta of .7, and a standard deviation of

17%. The market index return is 14% and has a standard deviation of 21%. What is the

M

2

measure of the portfolio if the risk-free rate is 5%?

72. A portfolio generates an annual return of 17%, a beta of 1.2, and a standard deviation of

19%. The market index return is 12% and has a standard deviation of 16%. What is the

M

2

measure of the portfolio if the risk-free rate is 4%?

73. A portfolio generates an annual return of 13%, a beta of .7, and a standard deviation of

17%. The market index return is 14% and has a standard deviation of 21%. What is the Treynor

measure of the portfolio if the risk-free rate is 5%?

74. A portfolio generates an annual return of 16%, a beta of 1.2, and a standard deviation of

19%. The market index return is 12% and has a standard deviation of 16%. What is the Treynor

measure of the portfolio if the risk-free rate is 6%?

75. A portfolio generates an annual return of 13%, a beta of .7, and a standard deviation of

17%. The market index return is 14% and has a standard deviation of 21%. What is the Sharpe

measure of the portfolio if the risk-free rate is 5%?

76. A portfolio generates an annual return of 16%, a beta of 1.2, and a standard deviation of

19%. The market index return is 12% and has a standard deviation of 16%. What is the Sharpe

ratio of the portfolio if the risk-free rate is 6%?

77. A portfolio generates an annual return of 13%, a beta of .7, and a standard deviation of

17%. The market index return is 14% and has a standard deviation of 21%. What is Jensen's alpha

of the portfolio if the risk-free rate is 5%?

78. A portfolio generates an annual return of 16%, a beta of 1.2, and a standard deviation of

19%. The market index return is 12% and has a standard deviation of 16%. What is Jensen's alpha

of the portfolio if the risk-free rate is 6%?

79. The portfolio that contains the benchmark asset allocation against which a manager will

be measured is often called _____________.

80. An attribution analysis will

not

likely contain which of the following components?

81. Which of the following investment strategies would have produced the highest returns in

the time period since 1926?

82. What phrase might be used as a substitute for the Treynor-Black model developed in

1973?

83. What is the term for the process used to assess portfolio manager performance?

84. A fund has excess performance of 1.5%. In looking at the fund's investment breakdown,

you see that the fund overweighted equities relative to the benchmark and that the average return

on the fund's equity portfolio was slightly lower than the equity benchmark return. The excess

performance for this fund is probably due to _______________.

85. For a market timer, the _____________ will be higher when

RM

is higher.

86. The Treynor-Black model combines an actively managed portfolio with an efficiently

diversified portfolio in order to:

I. Improve the diversification of the overall portfolio

II. Improve the overall portfolio's Sharpe ratio

III. Reach a higher CAL than would otherwise be possible