29. The

M

2 measure of portfolio performance was developed by ______________.

30. Probably the biggest problem with evaluating the portfolio performance of actively

managed funds is the assumption that __________________________.

31. Perfect-timing ability is equivalent to having __________ on the market portfolio.

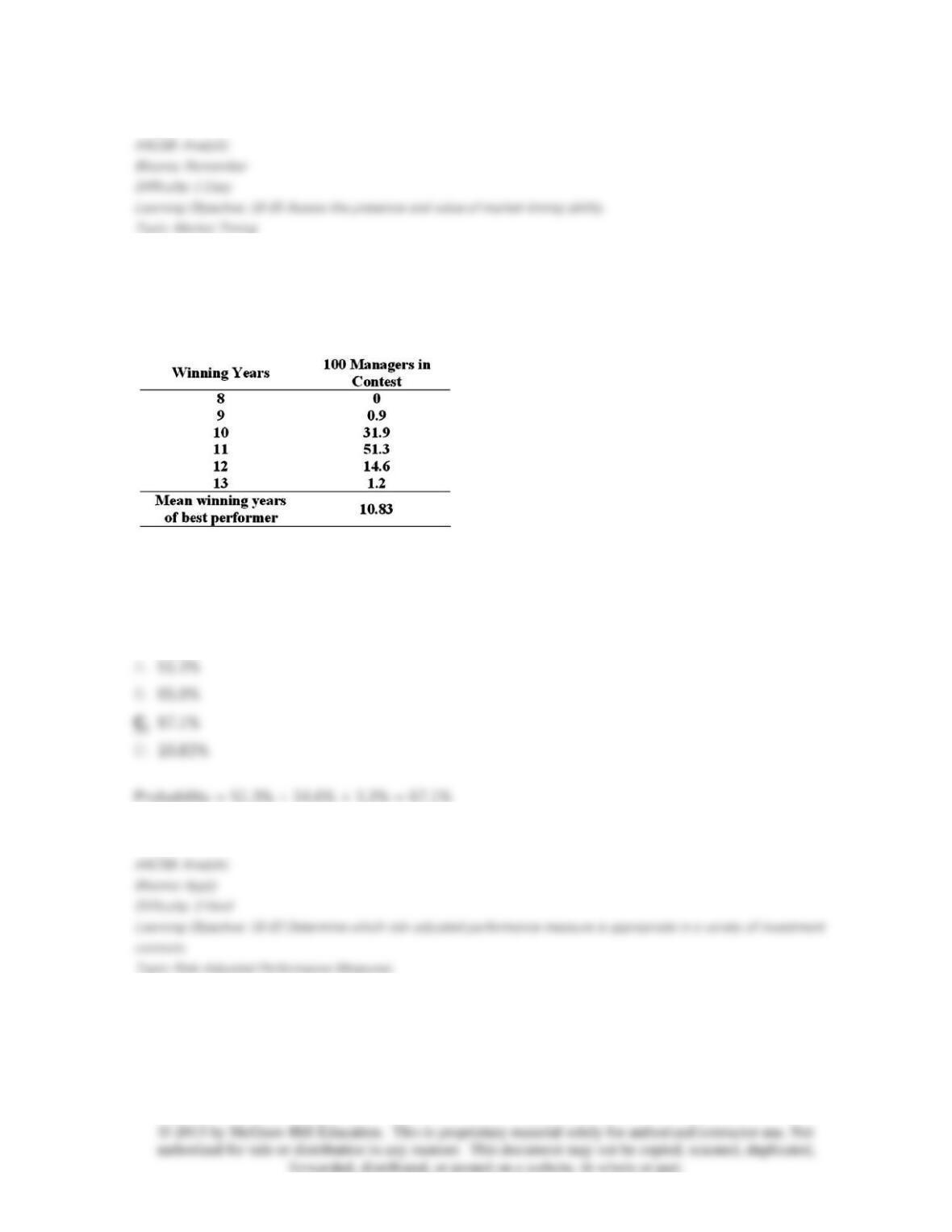

32. One hundred fund managers enter a contest to see how many times in 13 years they can

earn a higher return than their competitors. The probability distribution of the number of

successful years out of 13 for the best-performing money managers is

Out of this sample, chance alone would indicate that there is a ______ probability that someone

would beat the market at least 11 times out of 13 years.

33. The Treynor-Black model is a model that shows how an investment manager can use

security analysis and statistics to construct __________.

34. If an investor is a successful market timer, his distribution of monthly portfolio returns will

__________.

35. Recent analysis indicates that the style of investing is a critical component of fund

performance. In fact, on average about _____ of fund performance is attributable to the asset

allocation decision.

36. In the Treynor-Black model, the active portfolio will contain stocks with __________.

37. Portfolio performance is often decomposed into various subcomponents, such as the

return due to:

I. Broad asset allocation across security classes

II. Sector weightings within equity markets

III. Security selection with a given sector

The one decision that contributes most to the fund performance is _____.

38. The theory of efficient frontiers has __________.

39. In the Treynor-Black model, security analysts __________.

40. In the Treynor-Black model, security analysts __________.

41. Active portfolio management consists of:

I. Market timing

II. Security selection

III. Sector selection within given markets

IV. Indexing

42. A market-timing strategy is one in which asset allocation in the stock market __________

when one forecasts that the stock market will outperform Treasury bills.

43. In the Treynor-Black model, the contribution of individual security to the active portfolio

should be based primarily on the stock’s _________.

44. If all ______ are ______ in the Treynor-Black model, there would be no reason to depart

from the passive portfolio.

45. In the Treynor-Black model, the weight of each analyzed security in the portfolio should be

proportional to its __________.

46. The critical variable in the determination of the success of the active portfolio is the

stock’s __________.

47. Consider the theory of active portfolio management. Stocks A and B have the same

positive alpha and the same nonsystematic risk. Stock A has a higher beta than stock B. You

should want __________ in your active portfolio.

48. Consider the theory of active portfolio management. Stocks A and B have the same beta

and nonsystematic risk. Stock A has a higher positive alpha than stock B. You should want

__________ in your active portfolio.

49. The market-timing form of active portfolio management relies on __________ forecasting,

and the security selection form of active portfolio management relies on __________ forecasting.

50. Active portfolio managers try to construct a risky portfolio with _______.

51. In performance measurement, the bogey portfolio is designed to _________.

52. __________ portfolio managers experience streaks of abnormal returns that are hard to

label as lucky outcomes, and _________ anomalies in realized returns have been sufficiently

persistent that portfolio managers could use them to beat a passive strategy over prolonged

periods.

53. A passive benchmark portfolio is:

I. A portfolio in which the asset allocation across broad asset classes is neutral and not

determined by forecasts of performance of the different asset classes

II. One in which an indexed portfolio is held within each asset class

III. Often called the bogey

54. The correct measure of timing ability is ____________ for a portfolio manager who correctly

forecasts 55% of bull markets and 55% of bear markets.

55. It is very hard to statistically verify abnormal fund performance because of all of the

following

except

which one?

56. The term

alpha transport

refers to _____.

57. Portfolio managers Martin and Krueger each manage $1 million funds. Martin has perfect

foresight, and the call option value of his perfect foresight is $150,000. Krueger is an imperfect

forecaster and correctly predicts 50% of all bull markets and 70% of all bear markets. The correct

measure of timing ability for Krueger is __________.

58. Portfolio managers Martin and Krueger each manage $1 million funds. Martin has perfect

foresight, and the call option value of his perfect foresight is $150,000. Krueger is an imperfect

forecaster and correctly predicts 50% of all bull markets and 70% of all bear markets. The value of

Krueger’s imperfect forecasting ability is __________.

59. Douglass, an imperfect forecaster, correctly predicts 57% of all bull markets and 68% of all

bear markets. Simmonds is a perfect forecaster. If Douglass is able to charge a fee of $125,000,

the fee that Roy Simmonds should charge is __________. Assume that both forecasters manage

similar-size funds.

60. A mutual fund invests in large-capitalization stocks. Its performance should be measured

against which one of the following?

61. Assume you purchased a rental property for $100,000 and sold it 1 year later for $115,000

(there was no mortgage on the property). At the time of the sale, you paid $3,000 in commissions

and $1,000 in taxes. If you received $10,000 in rental income (all received at the end of the year),

what annual rate of return did you earn?