1. A mutual fund with a beta of 1.1 has outperformed the S&P 500 over the last 20 years. We

know that this mutual fund manager _____.

2. The comparison universe is __________.

3. Which one of the following performance measures is the Sharpe ratio?

4. The

M

2 measure is a variant of ________________.

5. A managed portfolio has a standard deviation equal to 22% and a beta of .9 when the

market portfolio’s standard deviation is 26%. The adjusted portfolio

P

* needed to calculate the

M

2

measure will have ________ invested in the managed portfolio and the rest in T-bills.

P

M

6. Your return will generally be higher using the __________ if you time your transactions

poorly, and your return will generally be higher using the __________ if you time your transactions

well.

7. Consider the Sharpe and Treynor performance measures. When a pension fund is large

and well diversified in total and it has many managers, the __________ measure is better for

evaluating individual managers while the __________ measure is better for evaluating the manager

of a small fund with only one manager responsible for all investments, which may not be fully

diversified.

8. Consider the theory of active portfolio management. Stocks A and B have the same beta

and the same positive alpha. Stock A has higher nonsystematic risk than stock B. You should want

__________ in your active portfolio.

9. Suppose that over the same time period two portfolios have the same average return and

the same standard deviation of return, but portfolio

A

has a higher beta than portfolio

B.

According to the Sharpe ratio, the performance of portfolio

A

__________.

10. Which model is preferred by academics, and is gaining in popularity with practitioners,

when evaluating investment performance?

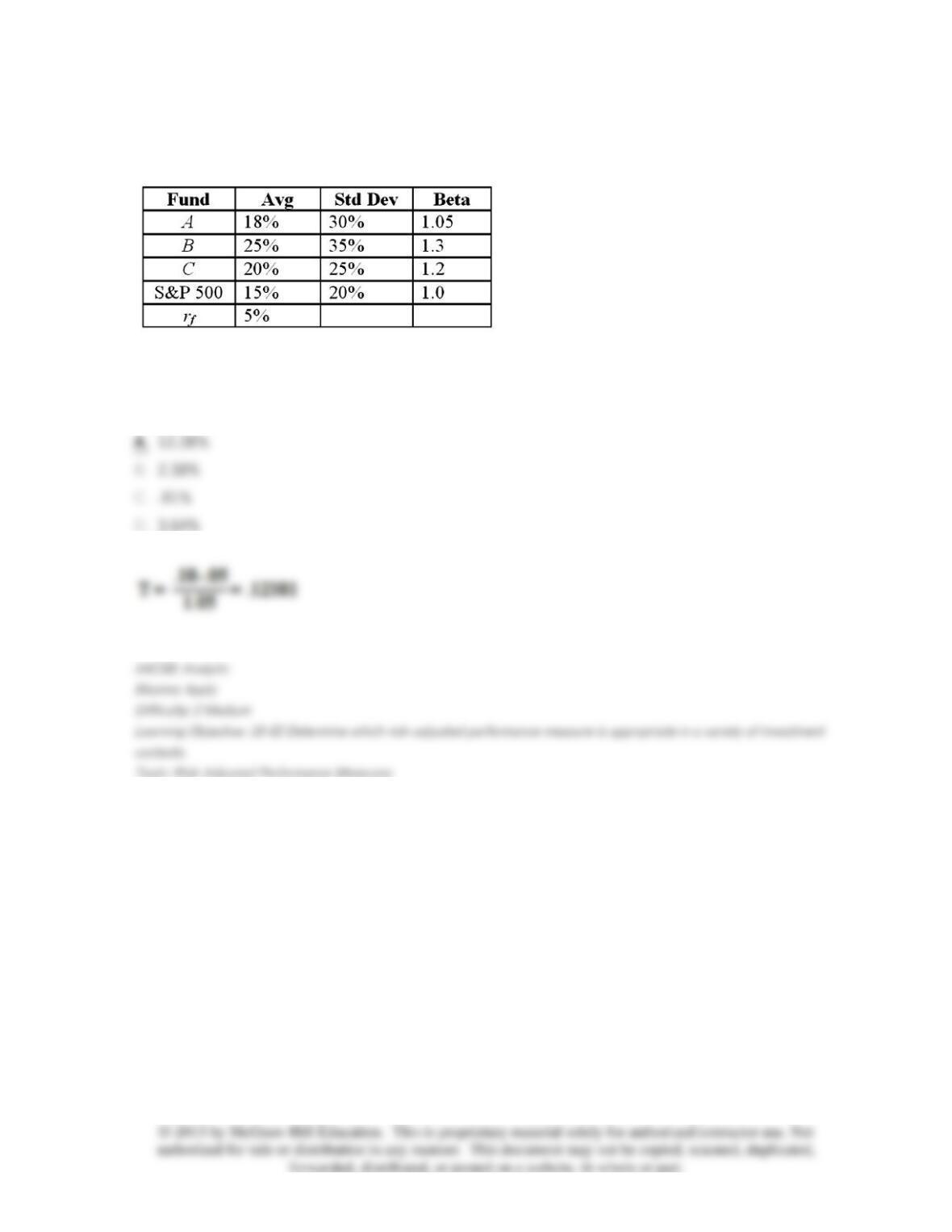

11. The risk-free rate, average returns, standard deviations, and betas for three funds and the

S&P 500 are given below.

What is the Treynor measure for portfolio

A?

12. The risk-free rate, average returns, standard deviations, and betas for three funds and the

S&P 500 are given below.

What is the

M

2 measure for portfolio

B?

13. The risk-free rate, average returns, standard deviations, and betas for three funds and the

S&P 500 are given below.

If these portfolios are subcomponents that make up part of a well-diversified portfolio, then

portfolio ______ is preferred.

14. The risk-free rate, average returns, standard deviations, and betas for three funds and the

S&P 500 are given below.

Based on the

M

2 measure, portfolio

C

has a superior return of _____ as compared to the S&P 500.

15. Which one of the following is largely based on forecasts of macroeconomic factors?

16. Based on the example used in the book, a perfect market timer would have made _______

by 2008 on a $1 investment made in 1926.

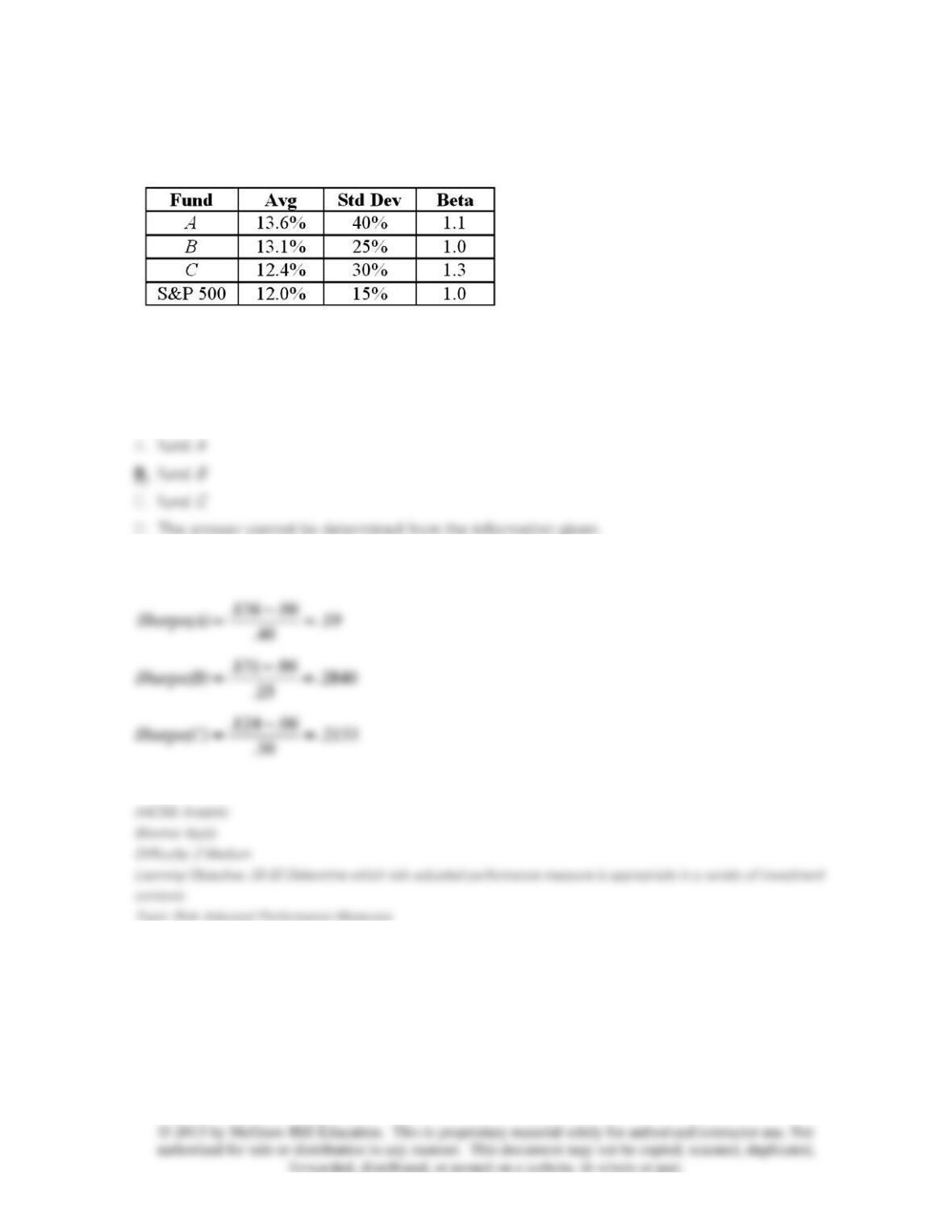

17. The average returns, standard deviations, and betas for three funds are given below along

with data for the S&P 500 Index. The risk-free return during the sample period is 6%.

You want to evaluate the three mutual funds using the Sharpe ratio for performance evaluation.

The fund with the highest Sharpe ratio of performance is __________.

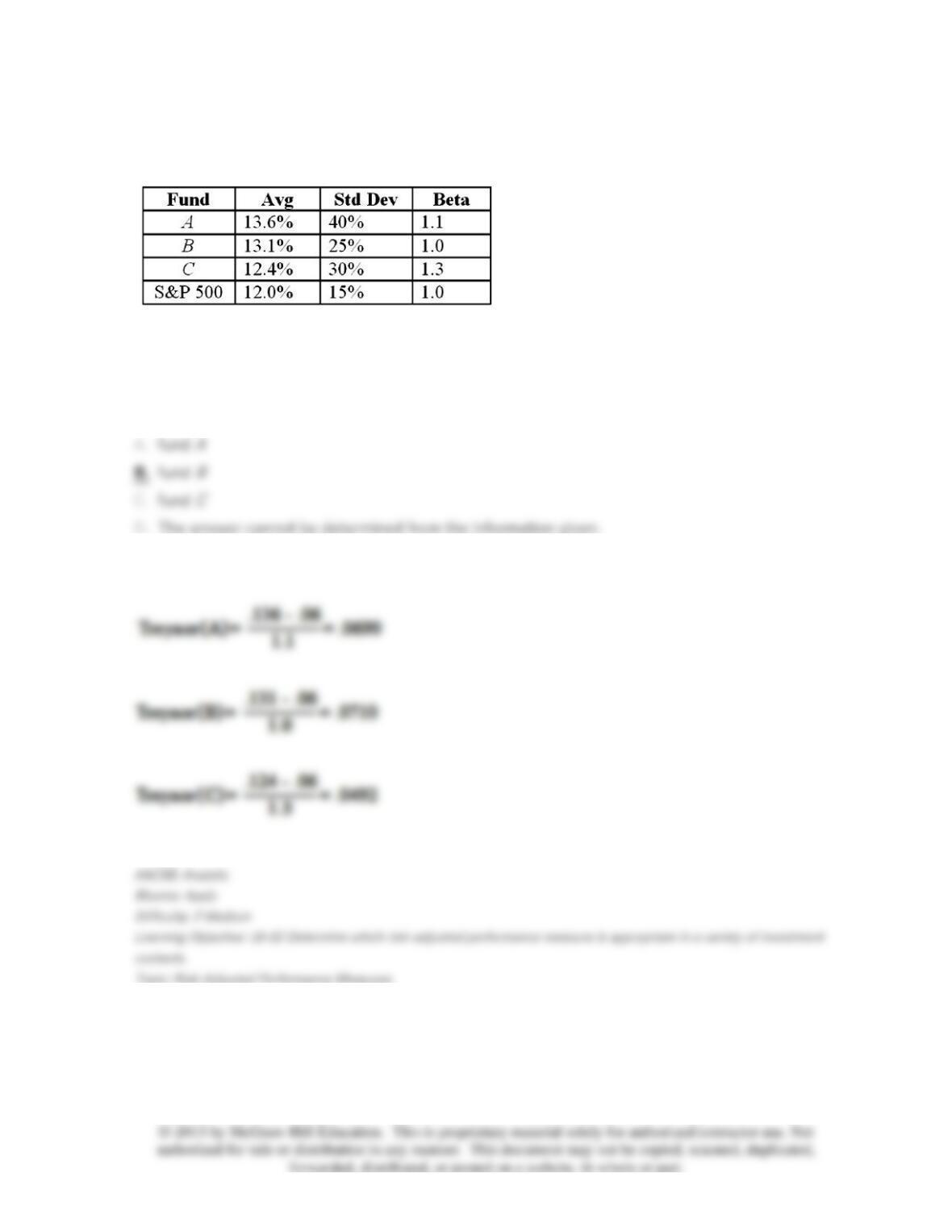

18. The average returns, standard deviations, and betas for three funds are given below along

with data for the S&P 500 Index. The risk-free return during the sample period is 6%.

You want to evaluate the three mutual funds using the Treynor measure for performance

evaluation. The fund with the highest Treynor measure of performance is __________.

19. The average returns, standard deviations, and betas for three funds are given below along

with data for the S&P 500 Index. The risk-free return during the sample period is 6%.

You want to evaluate the three mutual funds using the Jensen measure for performance

evaluation. The fund with the highest Jensen measure of performance is __________.

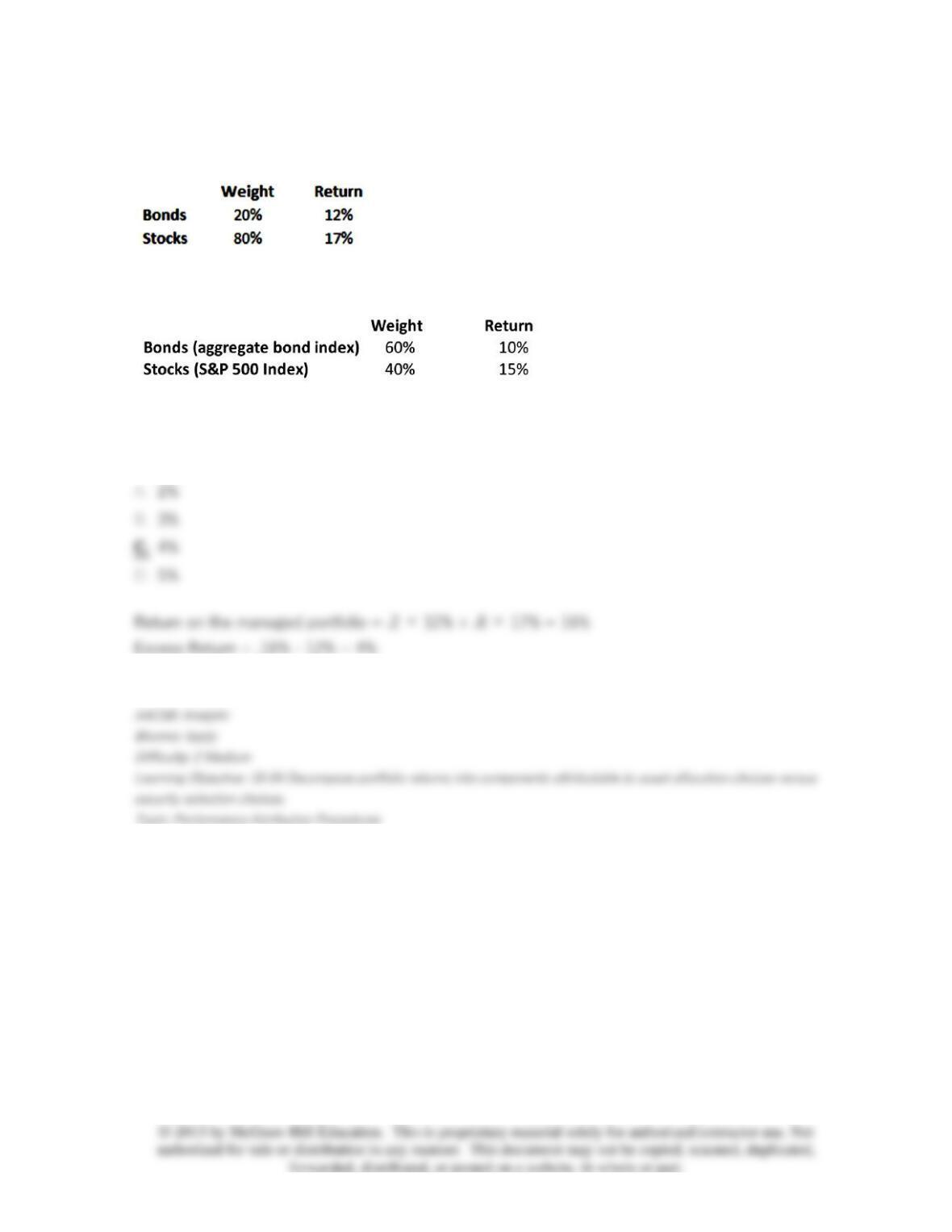

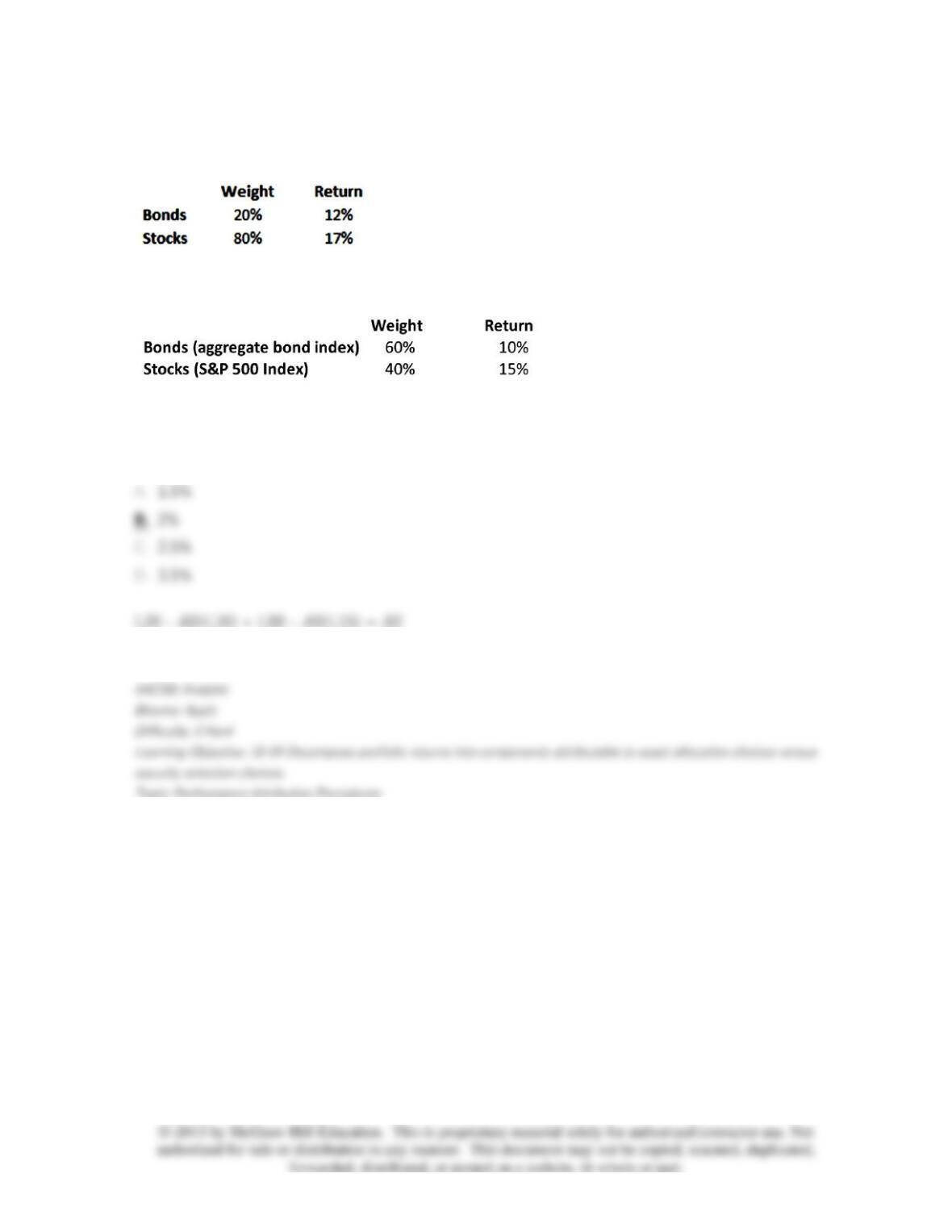

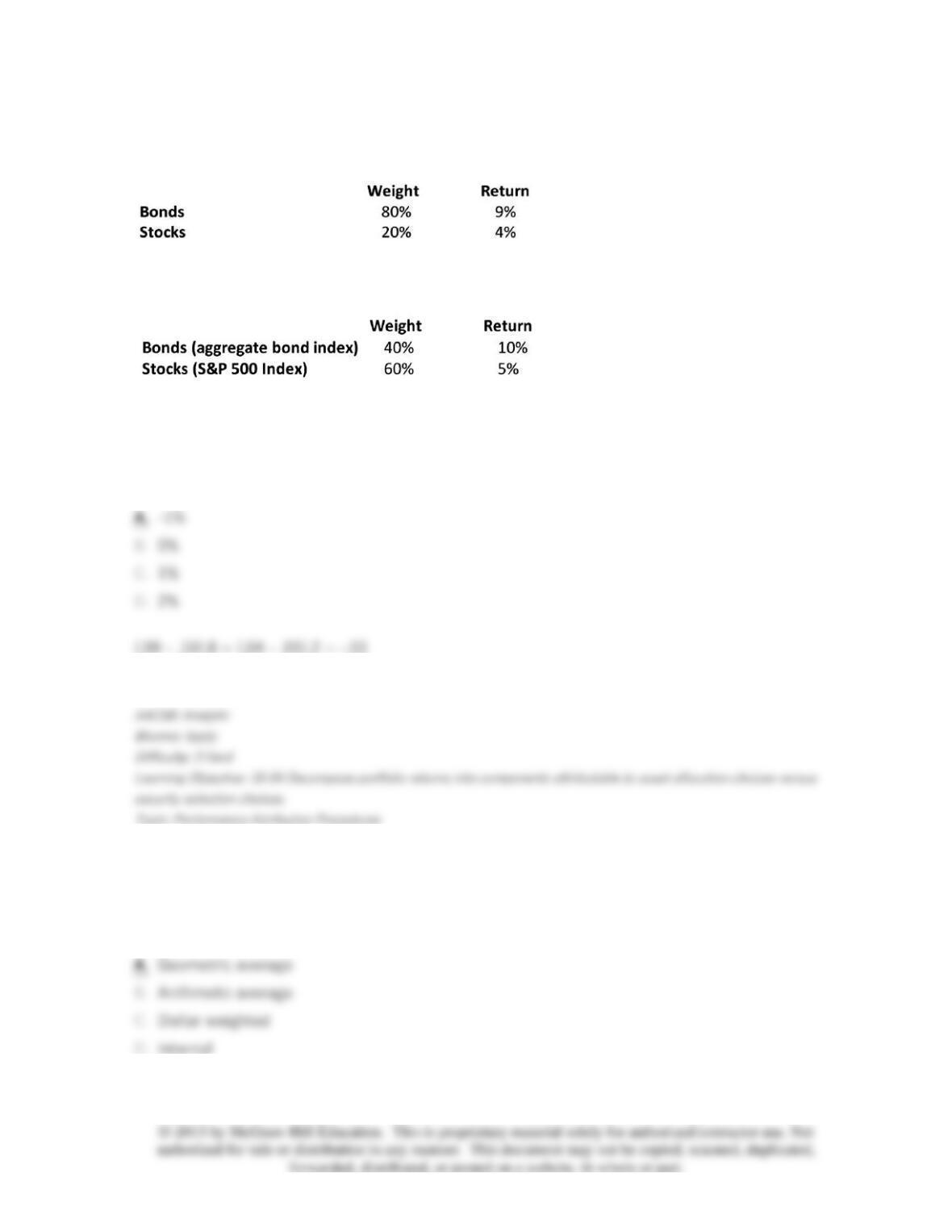

20. In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the

following investments in asset classes:

The return on a bogey portfolio was 12%, based on the following:

The total excess return on the managed portfolio was __________.

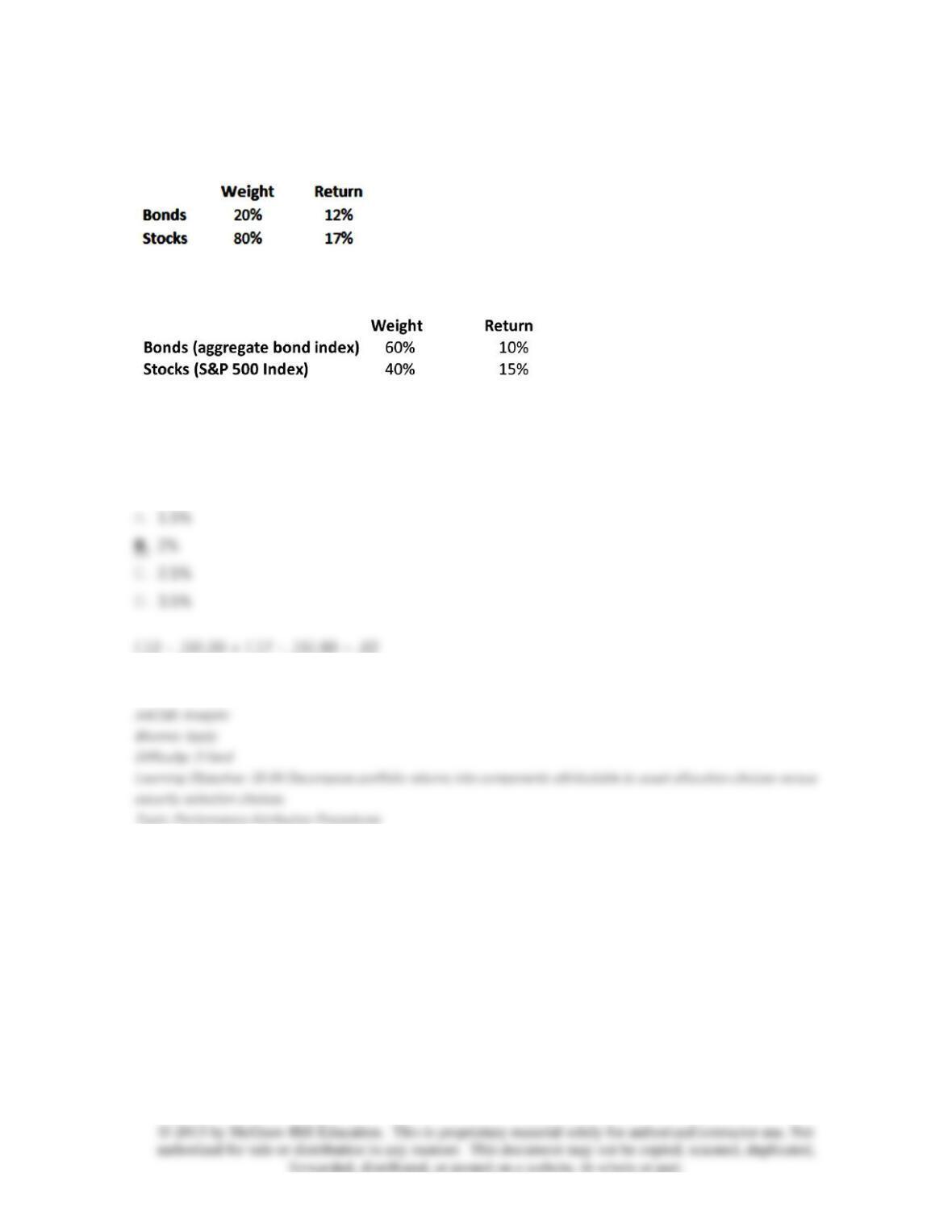

21. In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the

following investments in asset classes:

The return on a bogey portfolio was 12%, based on the following:

The contribution of asset allocation across markets to the total excess return was __________.

22. In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the

following investments in asset classes:

The return on a bogey portfolio was 12%, based on the following:

The contribution of security selection within asset classes to the total excess return was

__________.

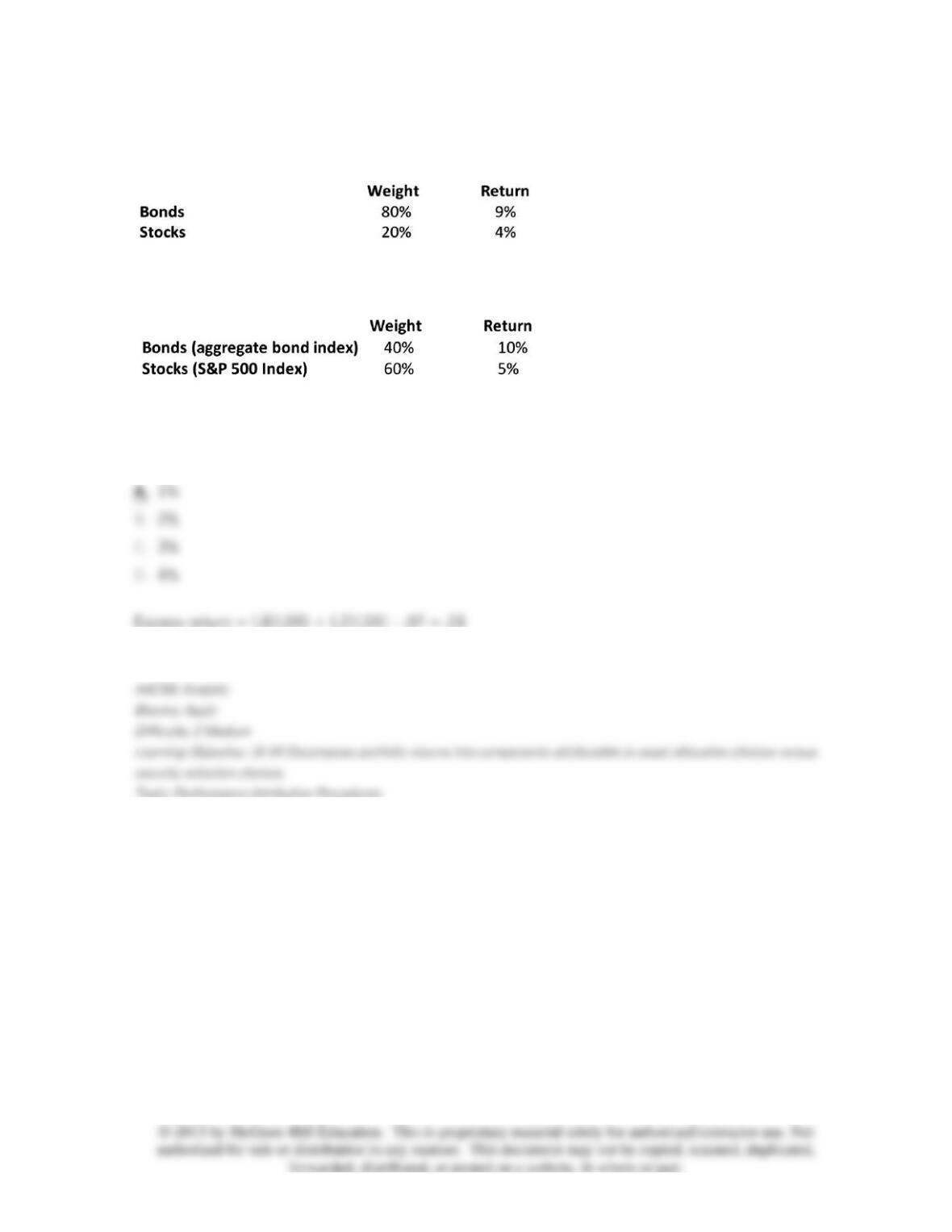

23. In a particular year, Lost Hope Mutual Fund made the following investments in asset

classes:

The return on a bogey portfolio was 12%, based on the following:

The total extra return on the managed portfolio was __________.

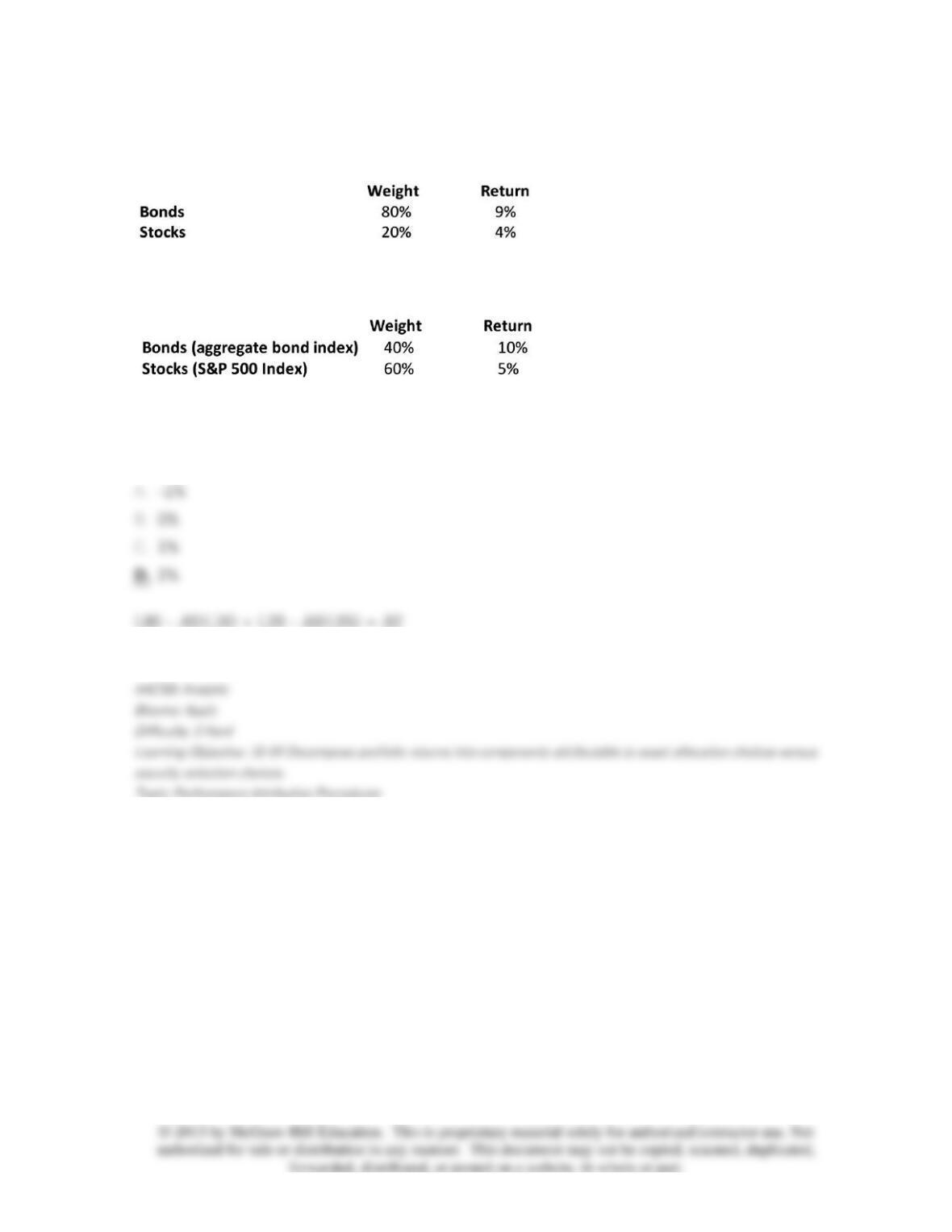

24. In a particular year, Lost Hope Mutual Fund made the following investments in asset

classes:

The return on a bogey portfolio was 12%, based on the following:

The contribution of asset allocation across markets to the total extra return was __________.

25. In a particular year, Lost Hope Mutual Fund made the following investments in asset

classes:

The return on a bogey portfolio was 12%, based on the following:

The contribution of security selection within asset classes to the total extra return was

__________.

26. Which one of the following averaging methods is the preferred method of constructing

returns series for use in evaluating portfolio performance?

27. The __________ calculates the reward to risk trade-off by dividing the average portfolio

excess return by the portfolio beta.

28. 28. In creating the

P

* portfolio, one mixes the original portfolio

P

and T-bills to match the

_________ of the market.