48. Which one of the following is the ticker symbol for the CBOE option contract on the S&P

100 Index?

49. The May 17, 2012, price quotation for a Boeing call option with a strike price of $50 due to

expire in November is $20.80, while the stock price of Boeing is $69.80. The premium on one

Boeing November 50 call contract is _________.

50. You purchase one IBM March 120 put contract for a put premium of $10. The maximum

profit that you could gain from this strategy is _________.

51. You buy one Hewlett Packard August 50 call contract and one Hewlett Packard August 50

put contract. The call premium is $1.25, and the put premium is $4.50. Your highest potential loss

from this position is _________.

52. You sell one Hewlett Packard August 50 call contract and sell one Hewlett Packard

August 50 put contract. The call premium is $1.25 and the put premium is $4.50. Your strategy will

pay off only if the stock price is __________ in August.

53. Suppose you purchase one Texas Instruments August 75 call contract quoted at $8.50 and

write one Texas Instruments August 80 call contract quoted at $6. If, at expiration, the price of a

share of Texas Instruments stock is $79, your profit would be _________.

54. __________ is the most risky transaction to undertake in the stock-index option markets if

the stock market is expected to fall substantially after the transaction is completed.

55. Which one of the following is a correct statement?

56. A put on Sanders stock with a strike price of $35 is priced at $2 per share, while a call

with a strike price of $35 is priced at $3.50. The maximum per-share loss to the writer of an

uncovered put is __________, and the maximum per-share gain to the writer of an uncovered call is

_________.

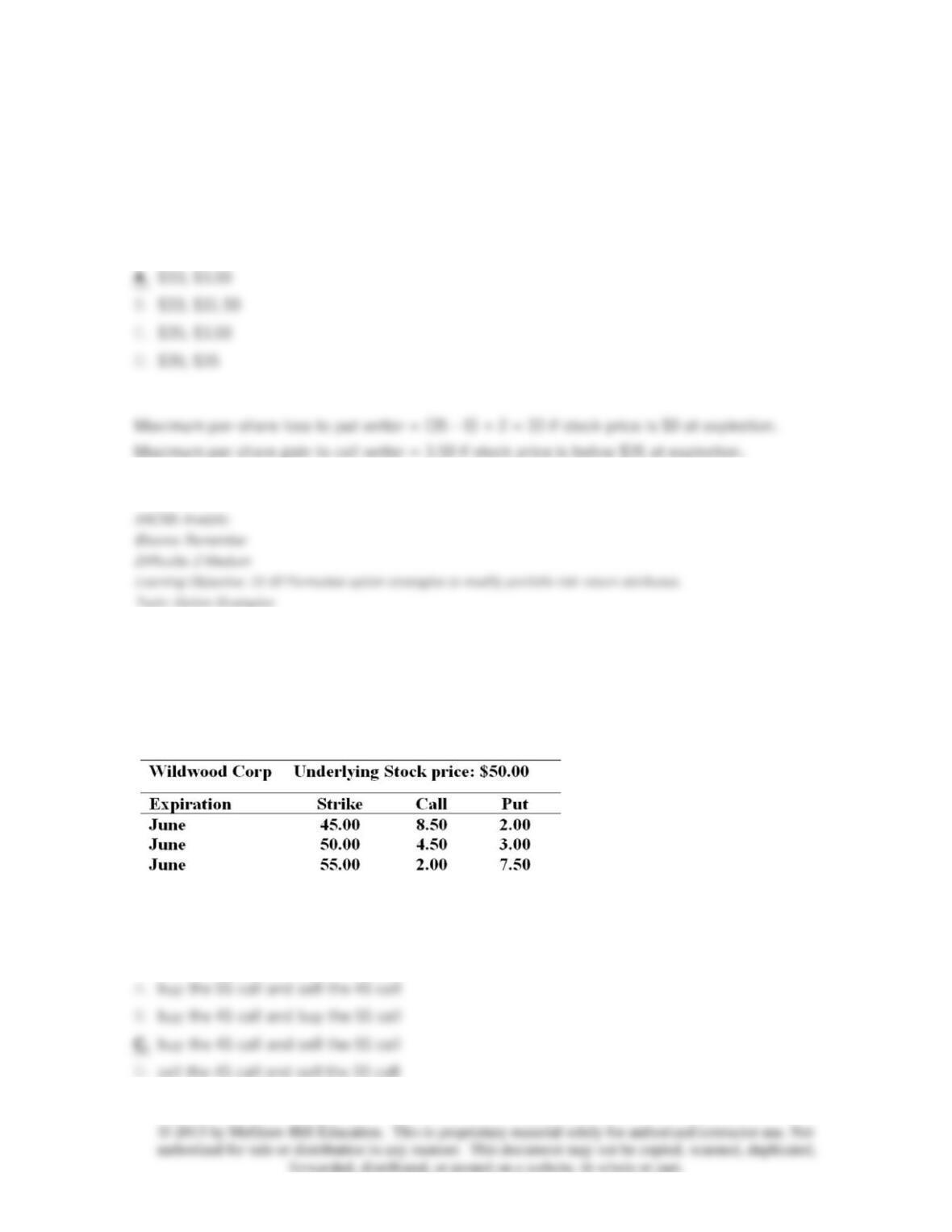

57. You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to establish a

bullish money spread to help limit the cost of your option position. You find the following option

quotes:

To establish a bull money spread with calls, you would _______________.

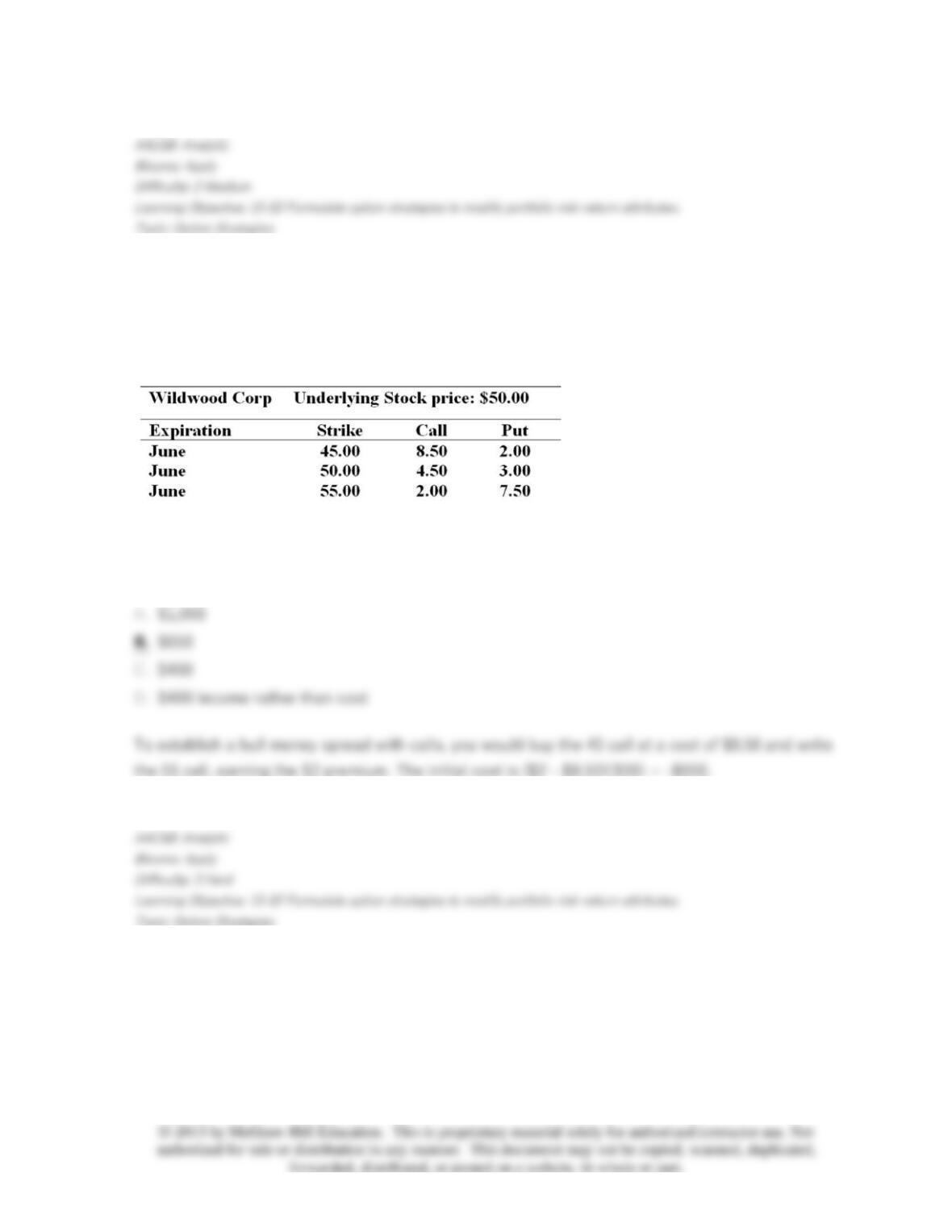

58. You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to establish a

bullish money spread to help limit the cost of your option position. You find the following option

quotes:

Ignoring commissions, the cost to establish the bull money spread with calls would be _______.

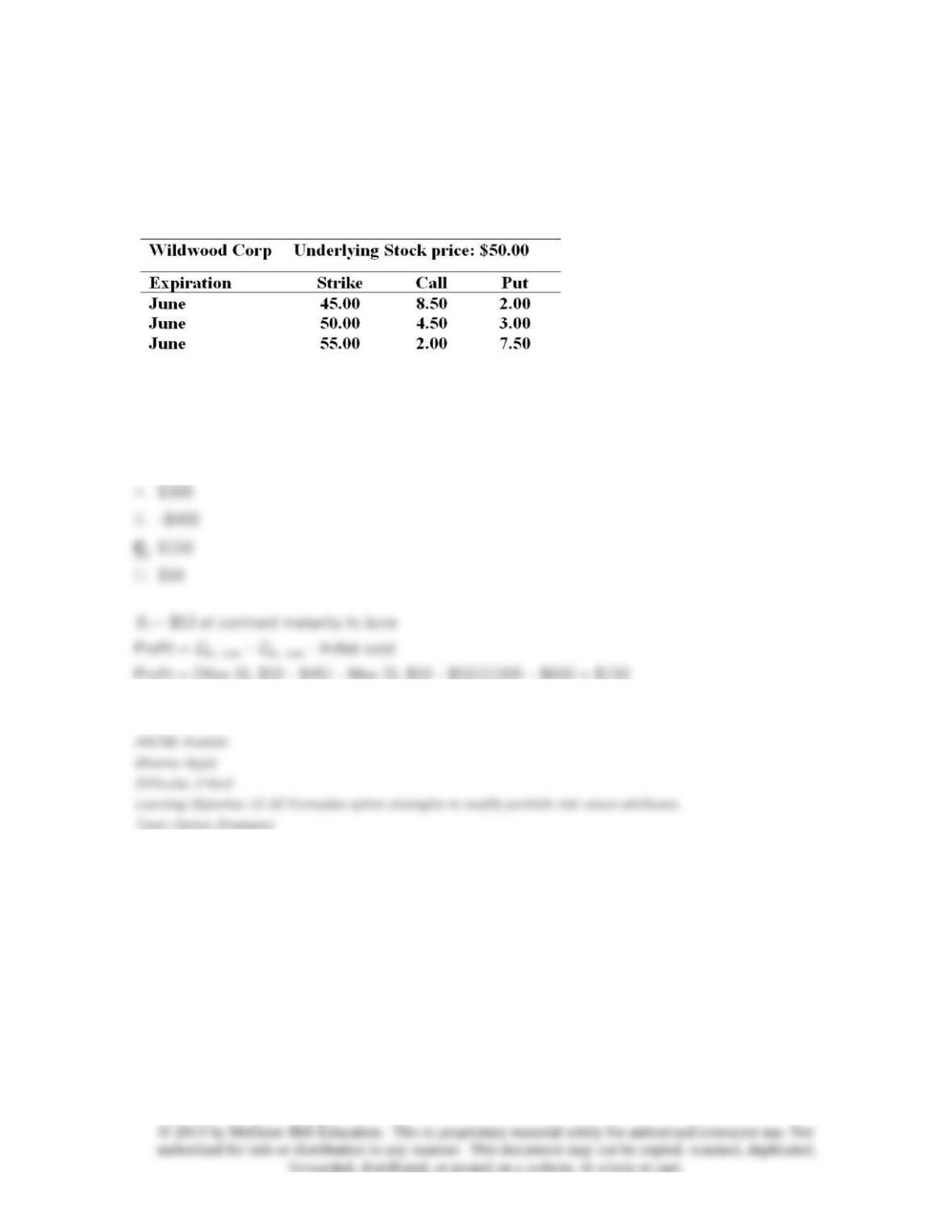

59. You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to establish a

bullish money spread to help limit the cost of your option position. You find the following option

quotes:

If in June the stock price is $53, your net profit on the bull money spread (buy the 45 call and sell

the 55 call) would be ________.

60. You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to establish a

bullish money spread to help limit the cost of your option position. You find the following option

quotes:

To establish a bull money spread with puts, you would _______________.

61. You are cautiously bullish on the common stock of the Wildwood Corporation over the

next several months. The current price of the stock is $50 per share. You want to establish a

bullish money spread to help limit the cost of your option position. You find the following option

quotes:

Suppose you establish a bullish money spread with the puts. In June the stock’s price turns out to

be $52. Ignoring commissions, the net profit on your position is _______________.

62. The common stock of the Avalon Corporation has been trading in a narrow range around

$40 per share for months, and you believe it is going to stay in that range for the next 3 months.

The price of a 3-month put option with an exercise price of $40 is $3, and a call with the same

expiration date and exercise price sells for $4.

What would be a simple options strategy using a put and a call to exploit your conviction about

the stock price’s future movement?

63. The common stock of the Avalon Corporation has been trading in a narrow range around

$40 per share for months, and you believe it is going to stay in that range for the next 3 months.

The price of a 3-month put option with an exercise price of $40 is $3, and a call with the same

expiration date and exercise price sells for $4.

Selling a straddle would generate total premium income of _____.

64. The common stock of the Avalon Corporation has been trading in a narrow range around

$40 per share for months, and you believe it is going to stay in that range for the next 3 months.

The price of a 3-month put option with an exercise price of $40 is $3, and a call with the same

expiration date and exercise price sells for $4.

Suppose you write a strap and the stock price winds up to be $42 at contract expiration. What was

your net profit on the strap?

65. The common stock of the Avalon Corporation has been trading in a narrow range around

$40 per share for months, and you believe it is going to stay in that range for the next 3 months.

The price of a 3-month put option with an exercise price of $40 is $3, and a call with the same

expiration date and exercise price sells for $4.

How can you create a position involving a put, a call, and riskless lending that would have the

same payoff structure as the stock at expiration?

66. A stock is trading at $50. You believe there is a 60% chance the price of the stock will

increase by 10% over the next 3 months. You believe there is a 30% chance the stock will drop by

5%, and you think there is only a 10% chance of a major drop in price of 20%. At–the-money 3-

month puts are available at a cost of $650 per contract. What is the expected dollar profit for a

writer of a naked put at the end of 3 months?

67. A covered call strategy benefits from what environment?