Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

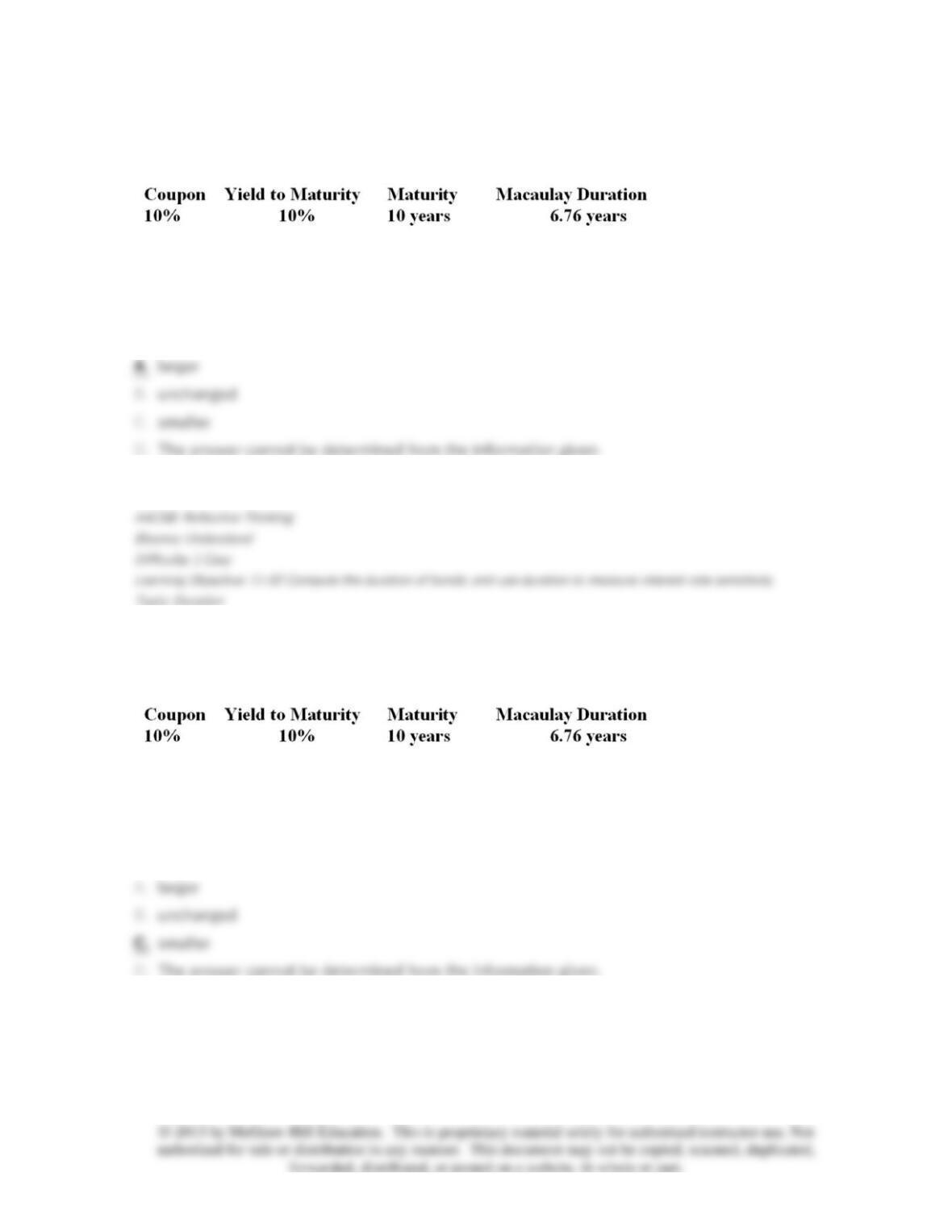

64. Steel Pier Company has issued bonds that pay semiannually with the following

characteristics:

If the bond's coupon was smaller than 10%, the modified duration would be _____ compared to the

original modified duration.

65. Steel Pier Company has issued bonds that pay semiannually with the following

characteristics:

If the maturity of the bond was less than 10 years, the modified duration would be _____

compared to the original modified duration.

66. Steel Pier Company has issued bonds that pay semiannually with the following

characteristics:

If the yield to maturity decreases to 8.045%, the expected percentage change in the price of the

bond using modified duration would be ____.

%Δ

67. A 20-year maturity corporate bond has a 6.5% coupon rate (the coupons are paid

annually). The bond currently sells for $925.50. A bond market analyst forecasts that in 5 years

yields on such bonds will be at 7%. You believe that you will be able to reinvest the coupons

earned over the next 5 years at a 6% rate of return. What is your expected annual compound rate

of return if you plan on selling the bond in 5 years?

68. When bonds sell above par, what is the relationship of price sensitivity to rising interest

rates?

69. A zero-coupon bond is selling at a deep discount price of $430. It matures in 13 years. If

the yield to maturity of the bond is 6.7%, what is the duration of the bond?

70. You have an investment that in today's dollars returns 15% of your investment in year 1,

12% in year 2, 9% in year 3, and the remainder in year 4. What is the duration of this investment?

71. If an investment returns a higher percentage of your money back sooner, it will ______.

72. Which one of the following statements correctly describes the weights used in the

Macaulay duration calculation? The weight in year

t

is equal to ____________.

73. The duration is independent of the coupon rate only for which one of the following?

74. You have an investment horizon of 6 years. You choose to hold a bond with a duration of

10 years. Your realized rate of return will be larger than the promised yield on the bond if

___________________.

75. A bond portfolio manager notices a hump in the yield curve at the 5-year point. How might

a bond manager take advantage of this event?

76. Market economists all predict a rise in interest rates. An astute bond manager wishing to

maximize her capital gain might employ which strategy?

77. You have an investment horizon of 6 years. You choose to hold a bond with a duration of 4

years. Your realized rate of return will be larger than the promised yield on the bond if

___________________.

78. What strategy might an insurance company employ to ensure that it will be able to meet

the obligations of annuity holders?

79. You have an investment horizon of 6 years. You choose to hold a bond with a duration of 6

years and continue to match your investment horizon and duration throughout your holding period.

Your realized rate of return will be the same as the promised yield on the bond if:

I. Interest rates increase.

II. Interest rates stay the same.

III. Interest rates fall.

80. Immunization of coupon-paying bonds does not imply that the portfolio manager is

inactive because:

I. The portfolio must be rebalanced every time interest rates change.

II. The portfolio must be rebalanced over time even if interest rates don't change.

III. Convexity implies duration-based immunization strategies don't work.

81. Advantages of cash flow matching and dedicated strategies include:

I. Once the cash flows are matched, there is no need for rebalancing.

II. Cash flow matching typically earns a higher rate of return than active bond portfolio

management.

III. Financial institutions' liabilities often exceed the maturity of available bonds, making cash

matching even more desirable.

82. Convexity implies that duration predictions:

I. Underestimate the percentage increase in bond price when the yield falls.

II. Underestimate the percentage decrease in bond price when the yield rises.

III. Overestimate the percentage increase in bond price when the yield falls.

IV. Overestimate the percentage decrease in bond price when the yield rises.

83. You have a 25-year maturity, 10% coupon, 10% yield bond with a duration of 10 years and

a convexity of 135.5. If the interest rate were to fall 125 basis points, your predicted new price for

the bond (including convexity) is _________.

84. You have a 15-year maturity, 4% coupon, 6% yield bond with duration of 10.5 years and a

convexity of 128.75. The bond is currently priced at $805.76. If the interest rate were to increase

200 basis points, your predicted new price for the bond (including convexity) is _________.

85. Convexity of a bond is ___________.