Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1. All other things equal (YTM = 10%), which of the following has the longest duration?

2. All other things equal(YTM = 10%), which of the following has the shortest duration?

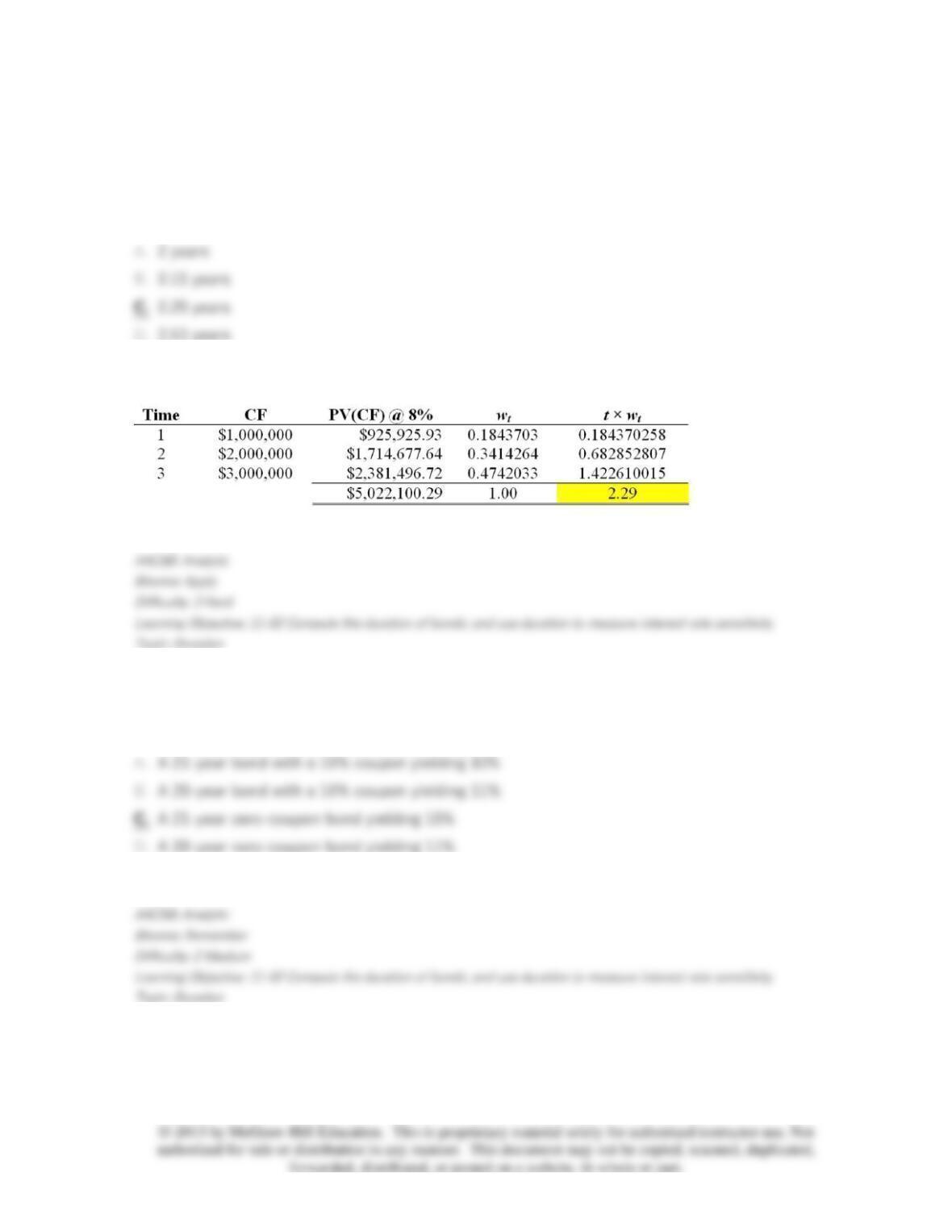

3. A pension fund must pay out $1 million next year, $2 million the following year, and then

$3 million the year after that. If the discount rate is 8%, what is the duration of this set of

payments?

4. All other things equal, which of the following has the longest duration?

5. The duration of a perpetuity varies _______ with interest rates.

6. Because of convexity, when interest rates change, the actual bond price will ____________

the bond price predicted by duration.

7. You find a 5-year AA Xerox bond priced to yield 6%. You find a similar-risk 5-year Canon

bond priced to yield 6.5%. If you expect interest rates to rise, which of the following should you

do?

8. A forecast of bond returns based largely on a prediction of the yield curve at the end of

the investment horizon is called a _________.

9. A bond's price volatility _________ at _________ rate as maturity increases.

10. As a result of bond convexity, an increase in a bond's price when yield to maturity falls is

________ the price decrease resulting from an increase in yield of equal magnitude.

11. All else equal, bond price volatility is greater for __________.

12. ______________ is an important characteristic of the relationship between bond prices and

yields.

13. Bond prices are _______ sensitive to changes in yield when the bond is selling at a _______

initial yield to maturity.

14. The pioneer of the duration concept was _________.

15. A portfolio manager sells Treasury bonds and buys corporate bonds because the spread

between corporate- and Treasury-bond yields is higher than its historical average. This is an

example of __________ swap.

16. The duration of a 5-year zero-coupon bond is ____ years.

17. A portfolio manager believes interest rates will drop and decides to sell short-duration

bonds and buy long-duration bonds. This is an example of __________ swap.

18. Target date immunization would primarily be of interest to _________.

19. Duration is a concept that is useful in assessing a bond's _________.

20. A pension fund has an average duration of its liabilities equal to 15 years. The fund is

looking at 5-year maturity zero-coupon bonds and 4% yield perpetuities to immunize its interest

rate risk. How much of its portfolio should it allocate to the zero-coupon bonds to immunize if

there are no other assets funding the plan?

21. You own a bond that has a duration of 6 years. Interest rates are currently 7%, but you

believe the Fed is about to increase interest rates by 25 basis points. Your predicted price change

on this bond is ________.

22. Given its time to maturity, the duration of a zero-coupon bond is _________.

23. An increase in a bond's yield to maturity results in a price decline that is ________ the

price increase resulting from a decrease in yield of equal magnitude.

24. All other things equal, a bond's duration is _________.

25. A bank has an average duration of its liabilities equal to 2 years. The bank's average

duration of its assets is 3.5 years. The bank's market value of equity is at risk if

_______________________.

26. All other things equal, a bond's duration is _________.

27. Banks and other financial institutions can best manage interest rate risk by

_____________.

28. In the context of a bond portfolio, price risk and reinvestment rate risk exactly cancel out

at a time horizon equal to the ____.

29. Bond portfolio immunization techniques balance ________ and ________ risk.

30. You have purchased a guaranteed investment contract (GIC) from an insurance firm that

promises to pay you a 5% compound rate of return per year for 6 years. If you pay $10,000 for the

GIC today and receive no interest along the way, you will get __________ in 6 years (to the nearest

dollar).

31. The duration of a portfolio of bonds can be calculated as _______________.

32. Pension fund managers can generally best bring about an effective reduction in their

interest rate risk by holding ___________________.

33. Which of the following is

not

a type of bond swap used in active portfolio management?

34. The exchange of one bond for a bond that has similar attributes but is more attractively

priced is called ______________.

35. Rank the interest sensitivity of the following from the most sensitive to an interest rate

change to the least sensitive:

I. 8% coupon, noncallable 20-year maturity par bond

II. 9% coupon, currently callable 20-year maturity premium bond

III. Zero-coupon 30-year maturity bond

36. A bond swap made in response to forecasts of interest rate changes is called ______.

37. Moving to higher-yield bonds, usually with longer maturities, is called ________.

38. In a pure yield pickup swap, ________ bonds are exchanged for _________ bonds.

39. The duration rule always ________ the value of a bond following a change in its yield.

40. Where

y

= yield to maturity, the duration of a perpetuity would be _________.

41. A bond currently has a price of $1,050. The yield on the bond is 6%. If the yield increases

25 basis points, the price of the bond will go down to $1,030. The duration of this bond is ____

years.

42. A bond has a current price of $1,030. The yield on the bond is 8%. If the yield changes

from 8% to 8.1%, the price of the bond will go down to $1,025.88. The modified duration of this

bond is _________.

43. A bank has $50 million in assets, $47 million in liabilities, and $3 million in shareholders'

equity. If the duration of its liabilities is 1.3 and the bank wants to immunize its net worth against

interest rate risk and thus set the duration of equity equal to zero, it should select assets with an

average duration of _________.