The Federal Reserve alters the amount of the nation’s money supply by:

A. reducing the liabilities of the banking system.

B. controlling the assets of the nation’s largest banks.

C. minting coins and printing currency that is distributed to banks.

D. manipulating the size of excess reserves held by commercial banks.

If total output in an economy is $600,000 and the total work-hours in the economy are

40,000, labor productivity is:

A. $7.

B. $9.

C. $13.

D. $15.

The U.S. supply of Japanese yen is:

A. downsloping because a lower dollar price of yen means U.S. goods are cheaper to

the Japanese.

B. upsloping because a higher dollar price of yen means U.S. goods are cheaper to the

Japanese.

C. upsloping because a lower dollar price of yen means U.S. goods are cheaper to the

Japanese.

D. downsloping because a higher dollar price of yen means U.S. goods are cheaper to

the Japanese.

An increase in taxes on consumers will most likely cause a(n):

A. decrease in aggregate supply.

B. decrease in aggregate demand.

C. increase in aggregate supply.

D. increase in aggregate demand.

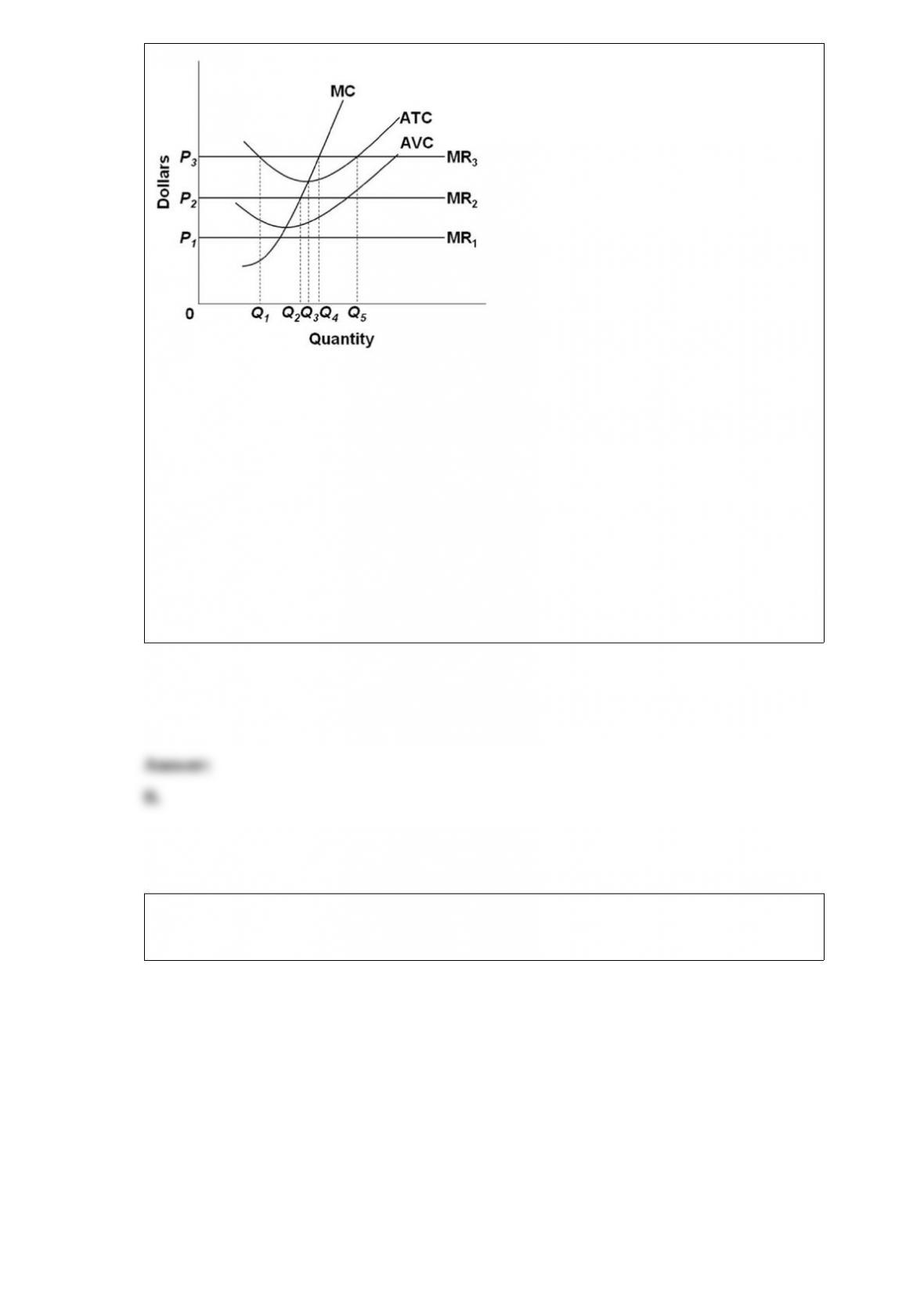

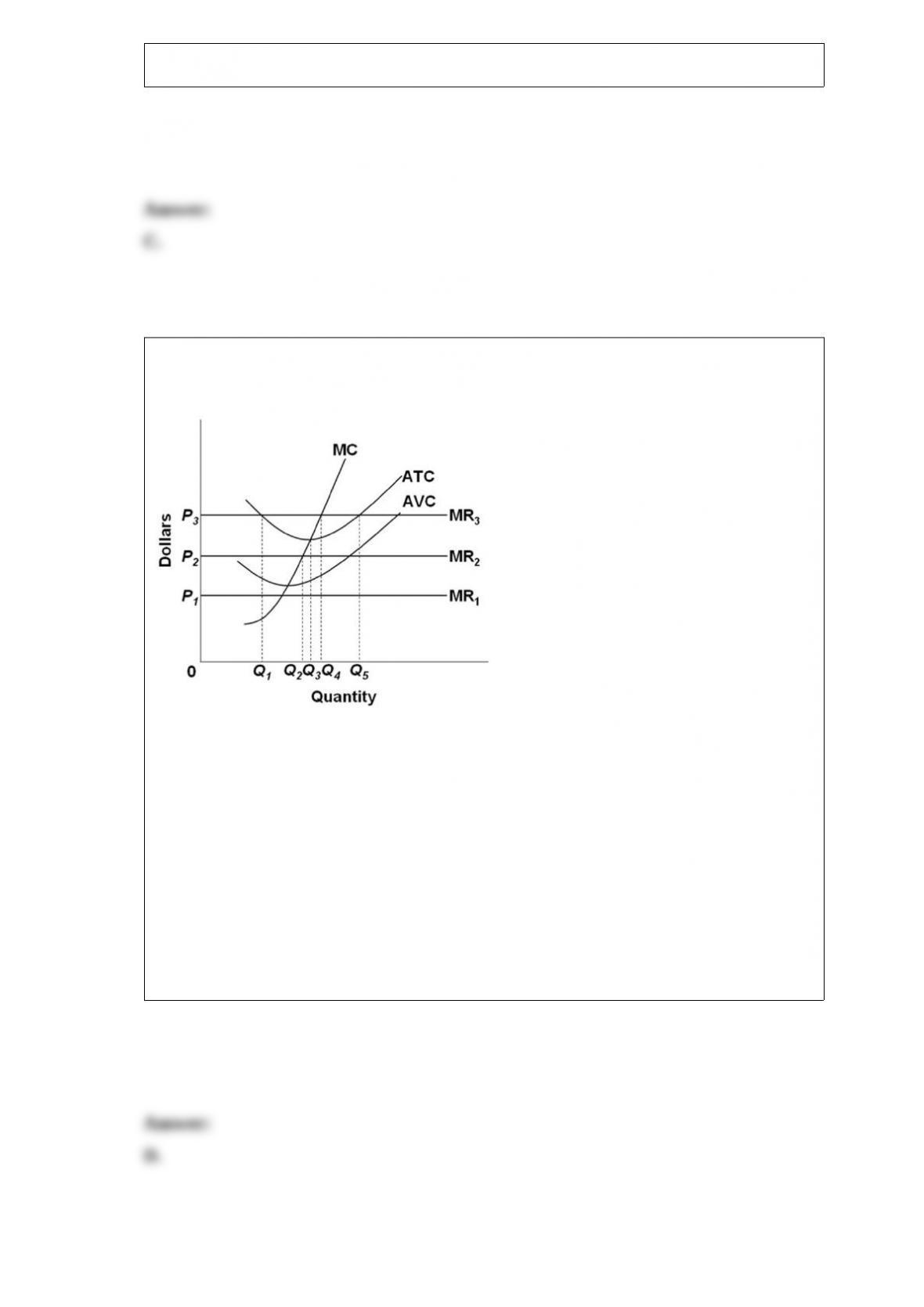

Refer to the above diagram. All data are for the short run. If product price is P3, the firm

will:

A. produce Q4 units and break even.

B. produce Q4 units and make an economic profit.

C. produce Q5 units and break even.

D. shut down.

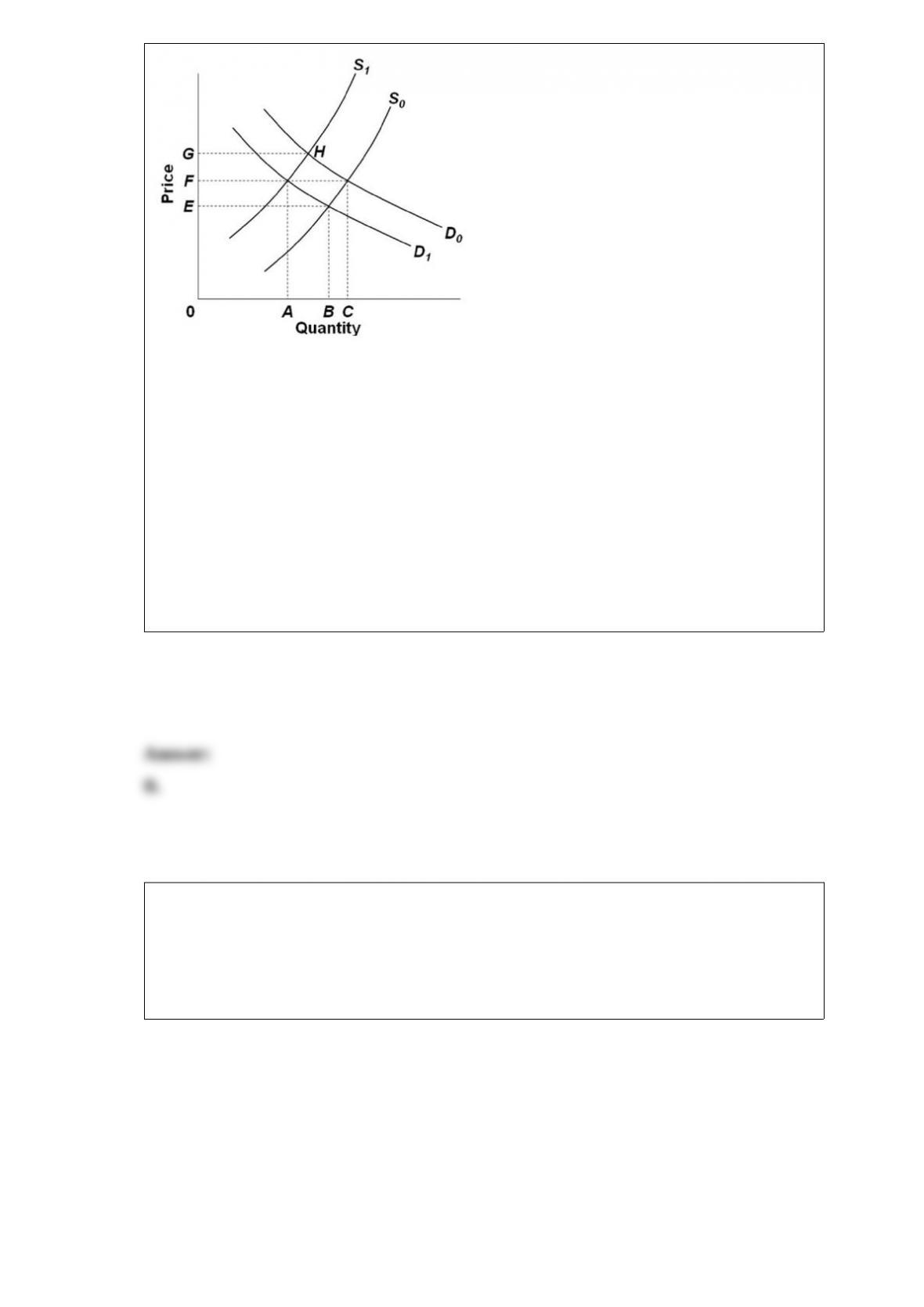

Refer to the above diagram, which shows demand and supply conditions in the

competitive market for product X. A shift in the demand curve from D0 to D1 might be

caused by a(n):

A. decrease in income if X is an inferior good.

B. increase in the price of complementary good Y.

C. increase in money incomes if X is a normal good.

D. increase in the price of substitute product Y.

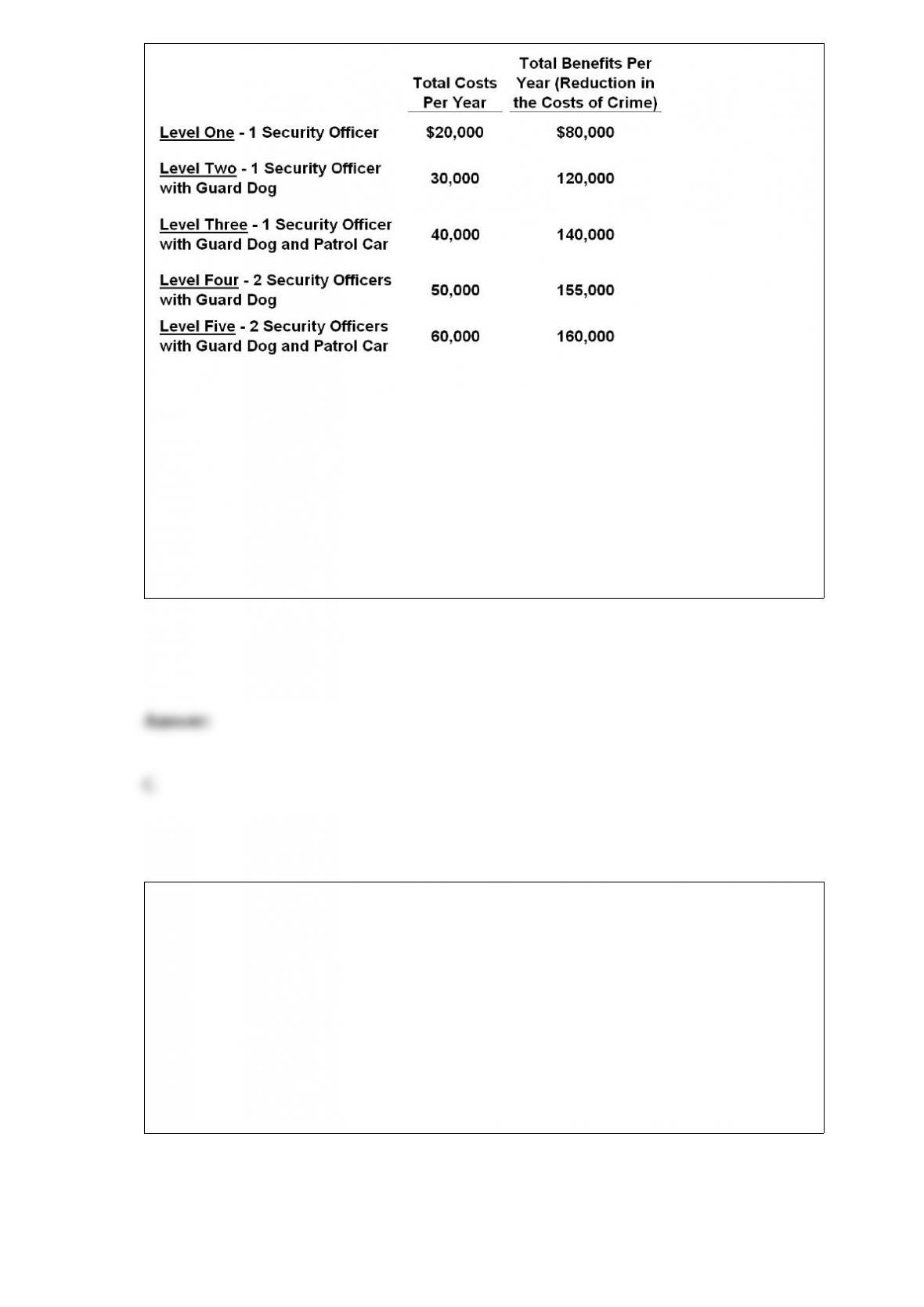

Waybelow Normal University has found it necessary to institute a crime-control

program on its campus to deal with the high costs of theft and vandalism. The

university is now considering several alternative levels of crime control. This table

shows the expected annual costs and benefits of these alternatives.

Refer to the above information. If Waybelow undertakes Level Three:

A.total benefits will be less than total costs.

B.marginal costs will exceed marginal benefits.

C.there would be an underallocation of resources to crime control.

D.there would be an overallocation of resources to crime control.

Monopolists are said to be allocatively inefficient because:

A. they produce where MR > MC.

B. at the profit-maximizing output, price is greater than AVC.

C. they produce only the type of product they desire and do not consider the consumer.

D. at the profit-maximizing output, the marginal benefit to society from increasing

output is greater than the marginal cost to society.

The interest rate will fall when the:

A. quantity of money demanded exceeds the quantity of money supplied.

B. quantity of money supplied exceeds the quantity of money demanded.

C. demand for money increases.

D. supply of money decreases.

An expansionary fiscal policy may be:

A. offset by lowering tax rates.

B. reinforced by raising tax rates.

C. reinforced by the crowding-out effect.

D. partially offset by the crowding-out effect.

In a capitalistic economy:

A. consumers are not sovereign.

B. markets are not competitive.

C. there is a reliance on the market system.

D. the government owns the means of production.

Pa and Pb represent the prices that citizens (a) and (b), the only two people in this

nation, are willing to pay for additional units of a quantity (Qc) of the public good. Qs

represents the quantity of the public good supplied by government at each of the

collective prices.

Refer to the above information. If only 1 unit of this public good is produced, then the

marginal benefit is:

A.$3 and the marginal cost is $9.

B.$4 and the marginal cost is $7.

C.$6 and the marginal cost is $3.

D.$9 and the marginal cost is $3.

Which is true of a purely competitive firm in long-run equilibrium?

A. Average fixed cost equals price.

B. Marginal cost equals marginal product.

C. Price equals marginal cost.

D. Average variable cost equals marginal cost.

Which phrase would be most characteristic of pure monopoly?

A. Close substitutes

B. Efficient advertiser

C. Price taker

D. Single seller

The United States is experiencing a recession and Congress decides to adopt an

expansionary fiscal policy to stimulate the economy. In this case, the crowding-out

effect suggests that investment spending would:

A. increase, thus decreasing aggregate demand and partially offsetting the fiscal policy.

B. increase, thus increasing aggregate demand and partially reinforcing the fiscal policy.

C. decrease, thus decreasing aggregate demand and partially offsetting the fiscal policy.

D. decrease, thus increasing aggregate demand and partially offsetting the fiscal policy.

Refer to the above diagram. All data are for the short run. If product price is P2, the firm

will:

A. close down to avoid a loss.

B. produce Q2 units and make an economic profit.

C. produce Q5 units and break even.

D. produce Q2 units and suffer a loss.

Assume a purely competitive increasing-cost industry is in long-run equilibrium. Now

suppose that an increase in consumer demand occurs. After all the resulting adjustments

have been completed, the new equilibrium price:

A. and industry output will be less than the initial price and output.

B. and industry output will be greater than the initial price and output.

C. will be greater, but the new output will be less than initially.

D. will be less, but the new output will be greater than initially.

When national income in other nations increases:

A. aggregate demand increases.

B. aggregate demand decreases.

C. the quantity of real domestic output demanded decreases.

D. the quantity of real domestic output demanded increases.

The GDP deflator or price index equals:

A. gross private domestic investment less the consumption of fixed capital.

B. gross national product less net foreign factor income earned in the United States.

C. nominal GDP divided by real GDP.

D. real GDP divided by nominal GDP.

Refer to the above diagrams that show identical marginal utility from income curves for

Singer and Catalano. If a given income of $20,000 is initially distributed so that Singer

receives $15,000 and Catalano $5000, the marginal utility:

A. of the last dollar of income will be greater for Catalano than for Singer.

B. derived from the last dollar will not be comparable between the two income

receivers.

C. of the last dollar of income will be the same for both Singer and Catalano.

D. of the last dollar of income will be greater for Singer than for Catalano.

Dumping is the sale of a product in a foreign market:

A. at a price below its domestic price or cost of production.

B. that does not meet the quality standards in the domestic market.

C. and is the principal means used to enforce nontariff barriers.

D. and is encouraged by voluntary export restraints.

Which of the following will cause a decrease in market equilibrium price and an

increase in equilibrium quantity?

A. An increase in supply

B. An increase in demand

C. A decrease in supply

D. A decrease in demand

An expected rise in the rate of inflation for consumer goods will:

A. decrease current aggregate demand.

B. increase current aggregate supply.

C. increase current aggregate demand.

D. decrease current aggregate supply.

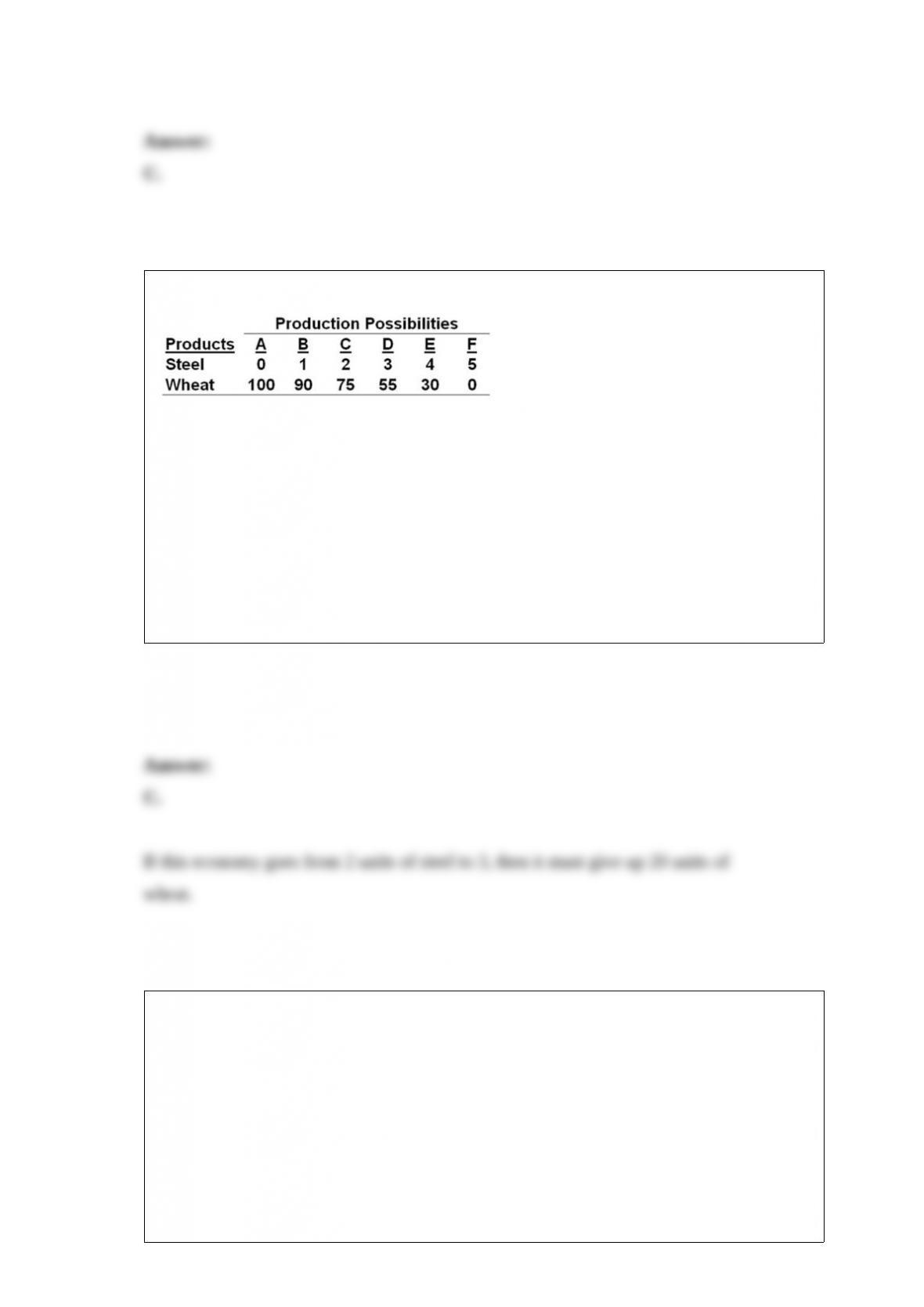

The following economy produces two products.

Refer to the above table. The marginal opportunity cost of the third unit of steel is:

A. 10 units of wheat.

B. 15 units of wheat.

C. 20 units of wheat.

D. 30 units of wheat.

A firm sells a product in a purely competitive market. The marginal cost of the product

at the current output is $5.00 and the market price is $5.00. What should the firm do?

A. Shut down if the minimum possible average variable cost is $5.25.

B. Shut down if the minimum possible average variable cost is $4.75.

C. Increase output if the minimum possible average variable cost is $5.25.

D. Decrease output if the minimum possible average variable cost is $4.75.

What is the main problem with mild inflation according to some economists?

A. It reduces the size of the GDP gap.

B. It leads to unanticipated deflation.

C. It increases frictional and structural unemployment in the economy.

D. It diverts productive time towards activities to hedge against inflation.

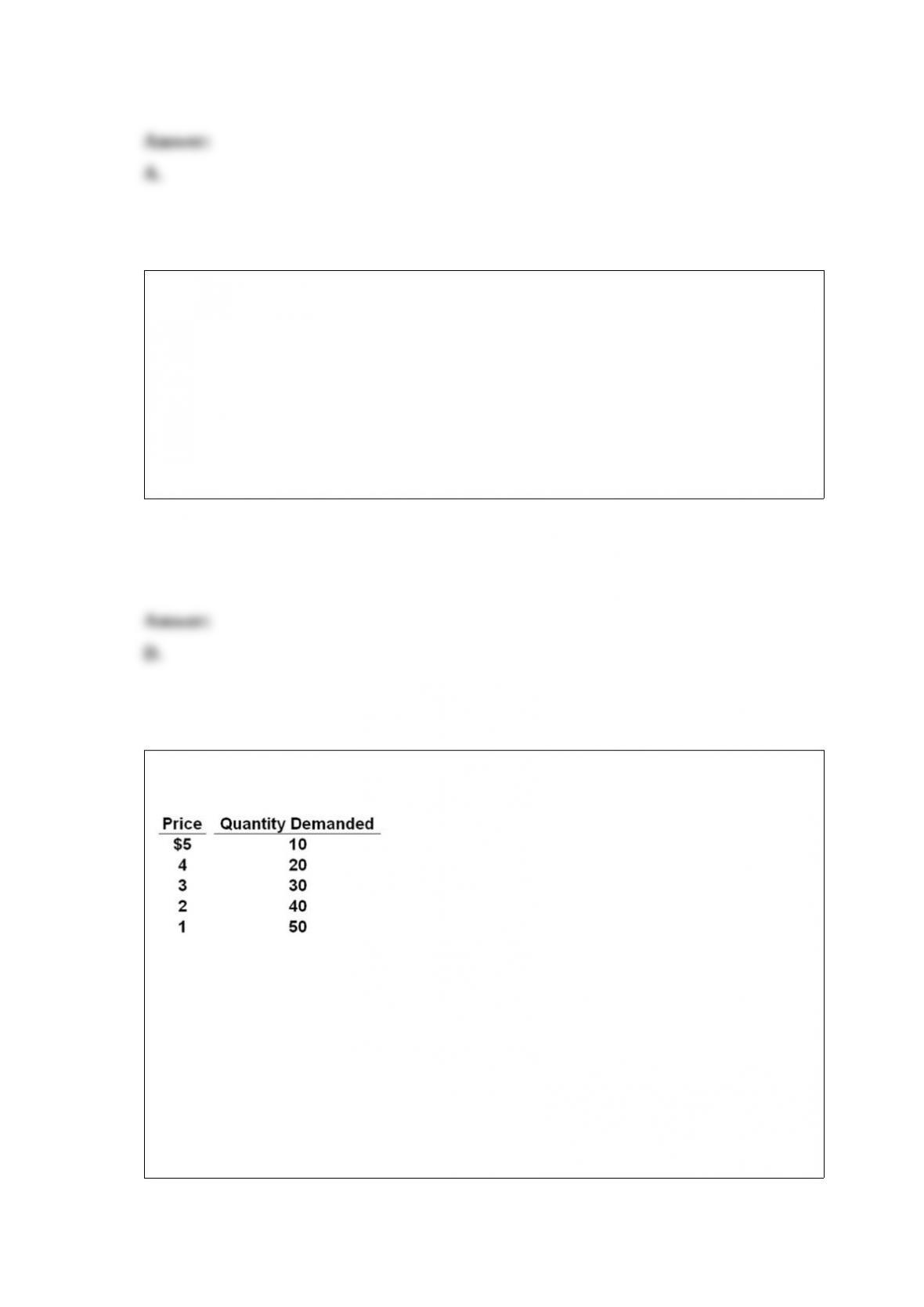

Refer to the table above. What is the price with the maximum total revenue?

A. $2

B. $3

C. $4

D. $5

The long-run equilibrium position of a monopolistically competitive firm is where

average costs are:

A. constant.

B. increasing.

C. decreasing.

D. at their minimum point.

A nation’s infrastructure refers to:

A. its ability to realize economies of scale.

B. its stock of technological knowledge.

C. public capital goods such as highways and sanitation systems.

D. the productivity of its labor force.

The incentive to cheat is strong in a cartel because:

A. each firm can increase its output and thus its profits by cutting price.

B. the marginal revenue for an individual firm is greater than marginal cost at the

profit-maximizing price set by the cartel.

C. there is a significant lack of government regulation of cartels, especially those in

worldwide production.

D. the costs of production are the same for each firm, but the product demand differs.

The price elasticity of demand increases with the length of the period to which the

demand curve pertains because:

A. consumers’ incomes will increase.

B. the demand curve will shift outward.

C. all prices will increase over time.

D. consumers will be better able to find substitutes.

If the value of the dollar is falling, then it follows that:

A. the price index is falling.

B. the price index is rising.

C. real incomes are falling.

D. interest rates are rising.

If a good that generates negative externalities were priced to account for spillover costs,

then its:

A.price would decrease and its output would increase.

B.output would increase, but its price would remain constant.

C.price would increase and its output would decrease.

D.price would increase, but its output would remain constant.

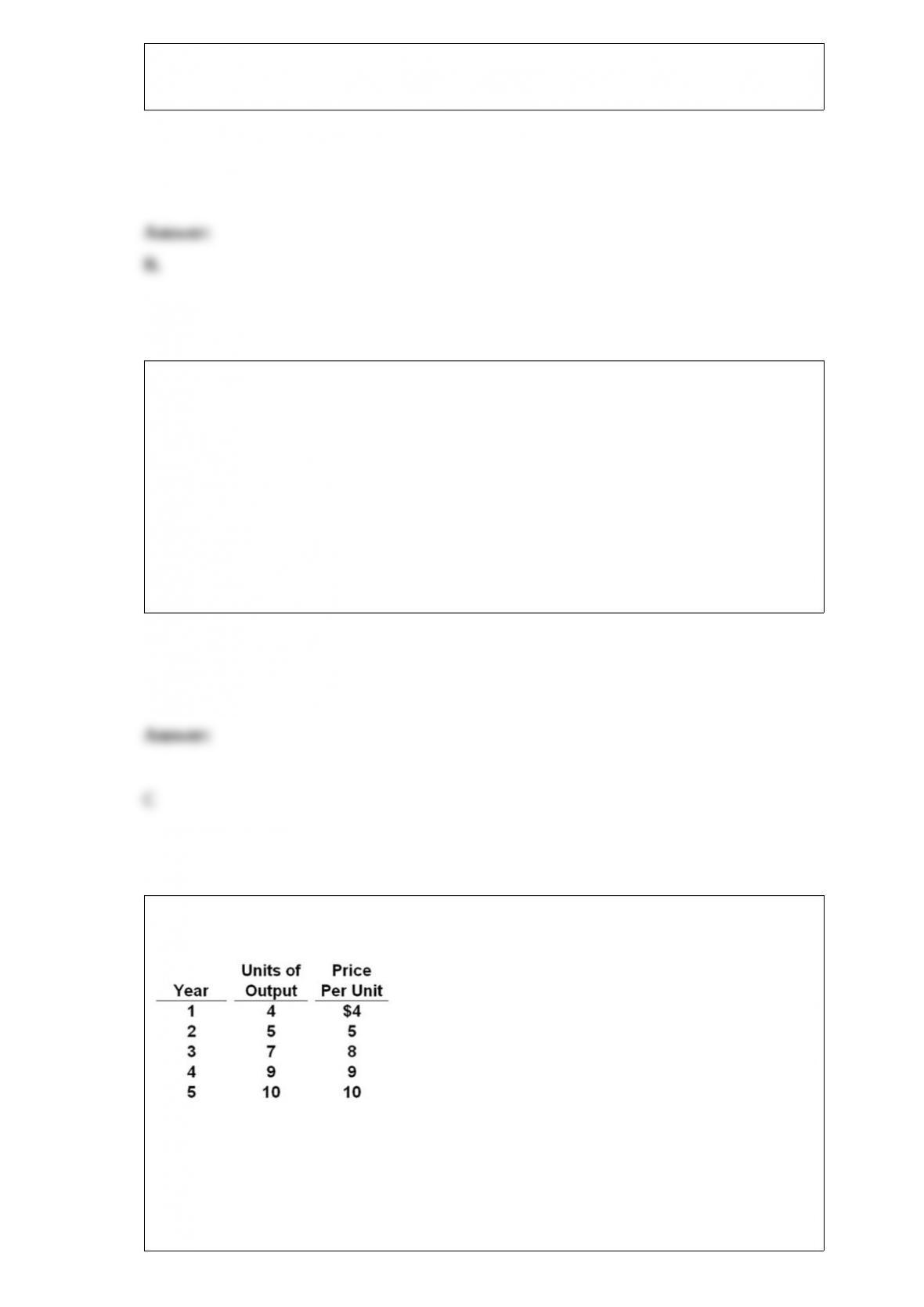

Assume an economy is producing only one product. Year 2 is the base year. Output and

price data for a five-year period are given.

Refer to the above data. If year 2 is chosen as the base year, the price index for year 1

is:

A. 70.

B. 80.

C. 95.

D. 125.

An aggregate supply curve represents the relationship between the:

A. price level and the buying of real domestic output.

B. price level and the production of real domestic output.

C. real domestic output bought and the real domestic output sold.

D. price level that producers are willing to accept and the price level buyers are willing

to pay.