If John drives more recklessly because he has good automobile insurance it is an

example of moral hazard.

The implementation of TANF helped reduce the number of people on welfare.

In a grim trigger strategy, a firm responds to underpricing by choosing a price forever

so low that each firm makes zero profit forever.

Part of the efficiency cost resulting from a switch from perfect competition to

monopoly is the loss of consumer surplus caused by the decrease in quantity produced.

The Federal Trade Commission may attempt to block a merger if they believe that the

merger will lead to greater competition and lower prices in a market.

It is possible for a merger to result in lower prices for consumers.

If marginal revenue is $10 and marginal costs is $8, the firm should increase its output.

In long-run equilibrium, a monopolistically competitive firm’s price is equal to its

marginal cost.

If firms in an oligopoly form a cartel, the outcome is the same as it would be under

monopolistic competition.

Discrimination cannot be easily measured by simply comparing average wage rates

across workers.

In a competitive market, a pollution tax increases the equilibrium price of the polluting

good, decreases the equilibrium quantity, and decreases the volume of waste.

A monopoly is a market that consists of one buyer and many sellers.

If one duopolist chooses the highest price it will maximize its profit.

A natural monopoly is the result of barriers such as patents and government licenses.

When applying the marginal principle, you should pick the level at which the activity’s

marginal benefit equals its marginal cost.

In an increasing-cost industry firms can enter and leave in the long run.

Positive economic profit encourages new firms to enter an industry.

If average cost is above marginal cost, average cost must be falling.

If Libby can produce 20 gallons of beer or 5 gallons of wine per hour, her opportunity

cost of one gallon of beer is 4 gallons of wine.

The opportunity cost of something is the nominal price paid for the product.

For a perfectly competitive firm, the marginal-revenue product curve is the same as the

firm’s short run demand for labor curve.

A market failure occurs when companies defraud the public.

Trade theory suggests that increased trade leads to increased wage equality.

If firm A and B do not have dominant strategies, the payoff matrix can be used to

predict the Nash equilibrium between firms A and B.

Producer surplus equals the market price less the producer’s willingness to accept or

marginal cost.

An increase in price would generate substitution and income effects that decrease the

quantity demanded of a particular good.

The prefrontal cortex uses both gut feelings and cognition in the decision-making

process.

Monopolists reduce producer surplus.

Price discrimination can be an effective way to increase a firm’s profit if the price

elasticity of demand is the same across all buyers the firm serves.

The market demand for school supplies is more elastic at the beginning of the semester

than it is at the start of summer vacation.

A clock tower is a private good if individuals pay for the tower to be built.

The lowest price found so far in a search process is a reservation price.

Positive relationships are also referred to as inverse relationships.

Rent control makes consumers who can find a place to rent worse off.

In the long-run perfectly competitive equilibrium, firms produce at the minimum of

average total cost.

The equilibrium price under an import quota is above the price that occurs with free

trade.

Governments sometime create an excess demand for a product by setting a maximum

price that is less than the equilibrium price, resulting in a permanent excess demand for

the product. This is known as a price floor.

Two parties engage in exchange when each one expects to be made better off by the

exchange.

A trust is an arrangement where the owners of several firms attempt to drive each other

out of business by lowering their prices.

Under a system of pollution taxes we expect firms to cut pollution until the marginal

benefit from tax savings equals the marginal increase in production costs due to

decreasing pollution.

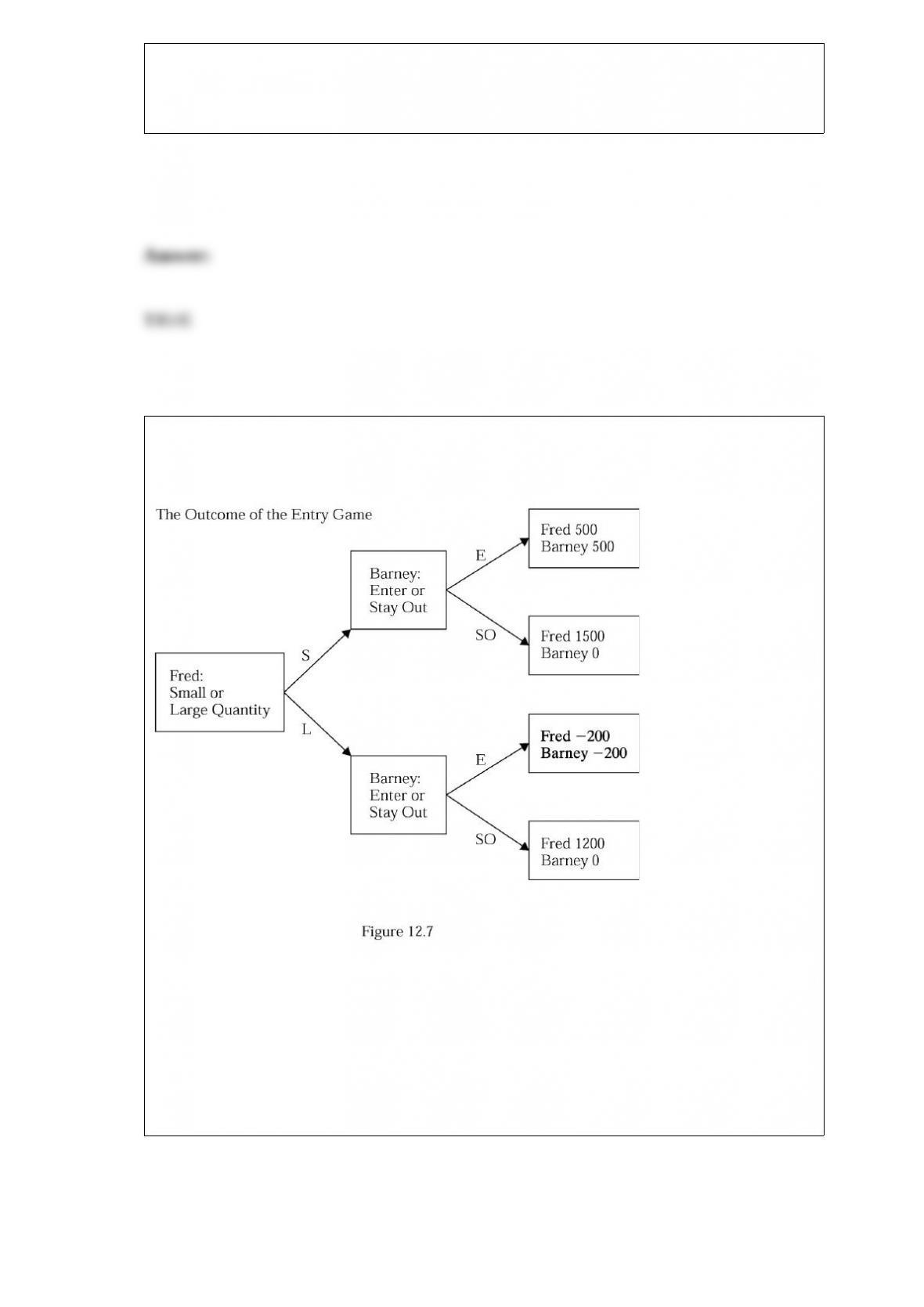

Refer to Figure 12.7. If Fred’s profit in the top rectangle were 1,300 instead of 500 then

the path of the game would be:

A) Fred chooses a small quantity and Barney enters.

B) Fred chooses a large quantity and Barney enters.

C) Fred chooses a small quantity and Barney stays out.

D) Fred chooses a large quantity and Barney stays out.

Resources are all of the following EXCEPT:

A) unlimited and in abundance.

B) the things we use to produce goods and services.

C) limited in quantity and can be used in different ways.

D) scarce and therefore require choices to be made.

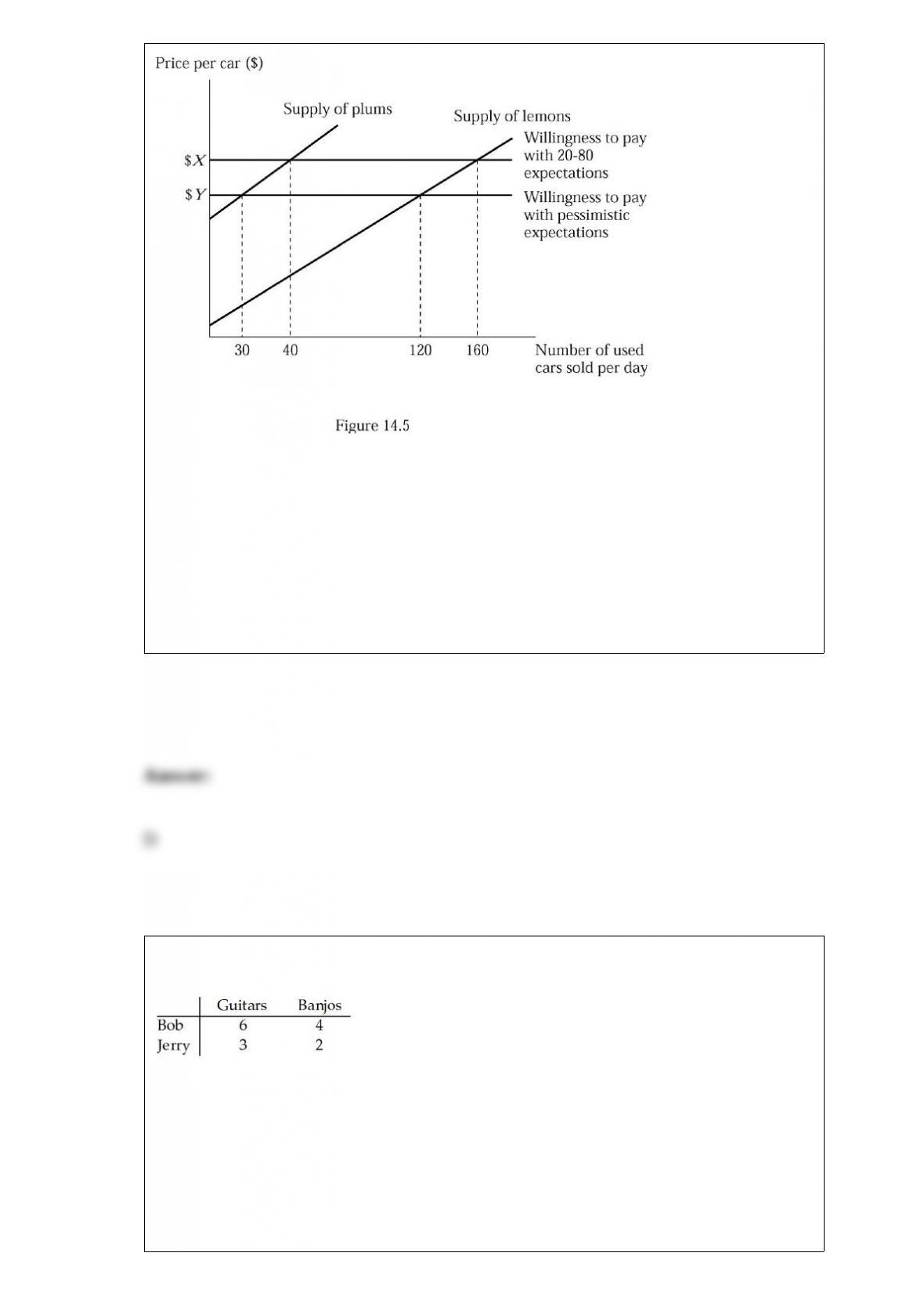

Figure 14.5 represents the market for used cars. Suppose buyers are willing to pay

$5,000 for a plum (high-quality) used car and $3,000 for a lemon (low-quality) used

car. Initially buyers believe that 80% of used cameras in the market are lemons (low

quality). Compared to the outcome with these initial expectations, how many fewer cars

are sold in equilibrium?

A) 50

B) 80

C) 110

D) The number of cars sold in equilibrium is the same as the outcome with neutral

expectations.

Consider two individuals, Bob and Jerry, who produce guitars and banjos. Bob and

Jerry’s weekly productivity are shown in Table 3.3. Which of the following is true?

Table 3.3

A) Bob has a comparative advantage in producing guitars but not banjos.

B) Bob has a comparative advantage in producing banjos but not guitars.

C) Bob has a comparative advantage in producing both goods.

D) Bob does not have a comparative advantage in producing either good.

Adam Smith used the metaphor of the “invisible hand” to explain how:

A) markets mismatch buyers and sellers.

B) business owners are benevolent.

C) people acting on their own self-interest promote the interest of society as a whole.

D) the production possibilities frontier illustrates efficient outcomes.

In the case of perfectly inelastic demand, the demand curve is:

A) upward sloping.

B) downward sloping.

C) vertical.

D) horizontal.

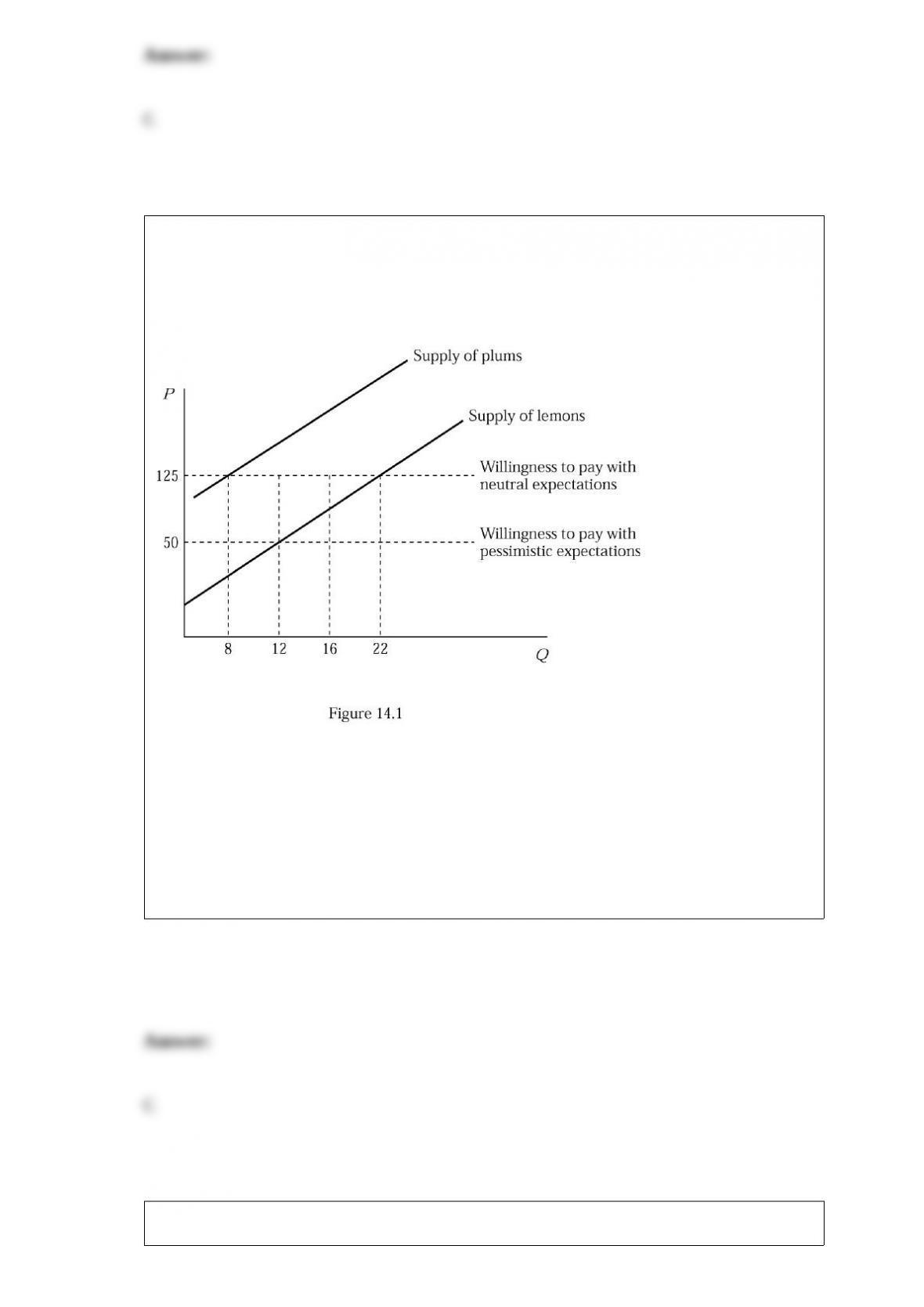

Figure 14.1 represents the market for used bikes. Suppose buyers are willing to pay

$200 for a plum (high-quality) used bike and $50 for a lemon (low-quality) used bike.

If buyers believe that 50% of the used bikes are lemons (low quality), how much will

they be willing to pay for a used bike?

A) $50

B) $80

C) $125

D) $200

A market in which firms sell a homogeneous product and cannot influence market price

is most likely:

A) a perfectly competitive market.

B) an oligopoly.

C) a monopolistically competitive market.

D) a monopoly market.

Recall Application 4, “Chinese Demand and Pecan Pies,” to answer the following

questions:

According to the Application, which determinant of demand is responsible for the

increase in the demand for pecans?

A) preferences

B) income

C) price of substitutes

D) price of complements

Deadweight loss is

A) the reduction in surplus that results from a tax.

B) an excess burden of a tax.

C) a loss of economic efficiency.

D) the excess supply that occurs when a tax is imposed on a product.

Recall the Application about finding estimates on elasticities of demand, which of the

following Web sites provides estimates of demand elasticities for hundreds of food

products in different countries?

A) the United Nations

B) the World Bank

C) the U.S. Department of Commerce

D) the U.S Department of Agriculture

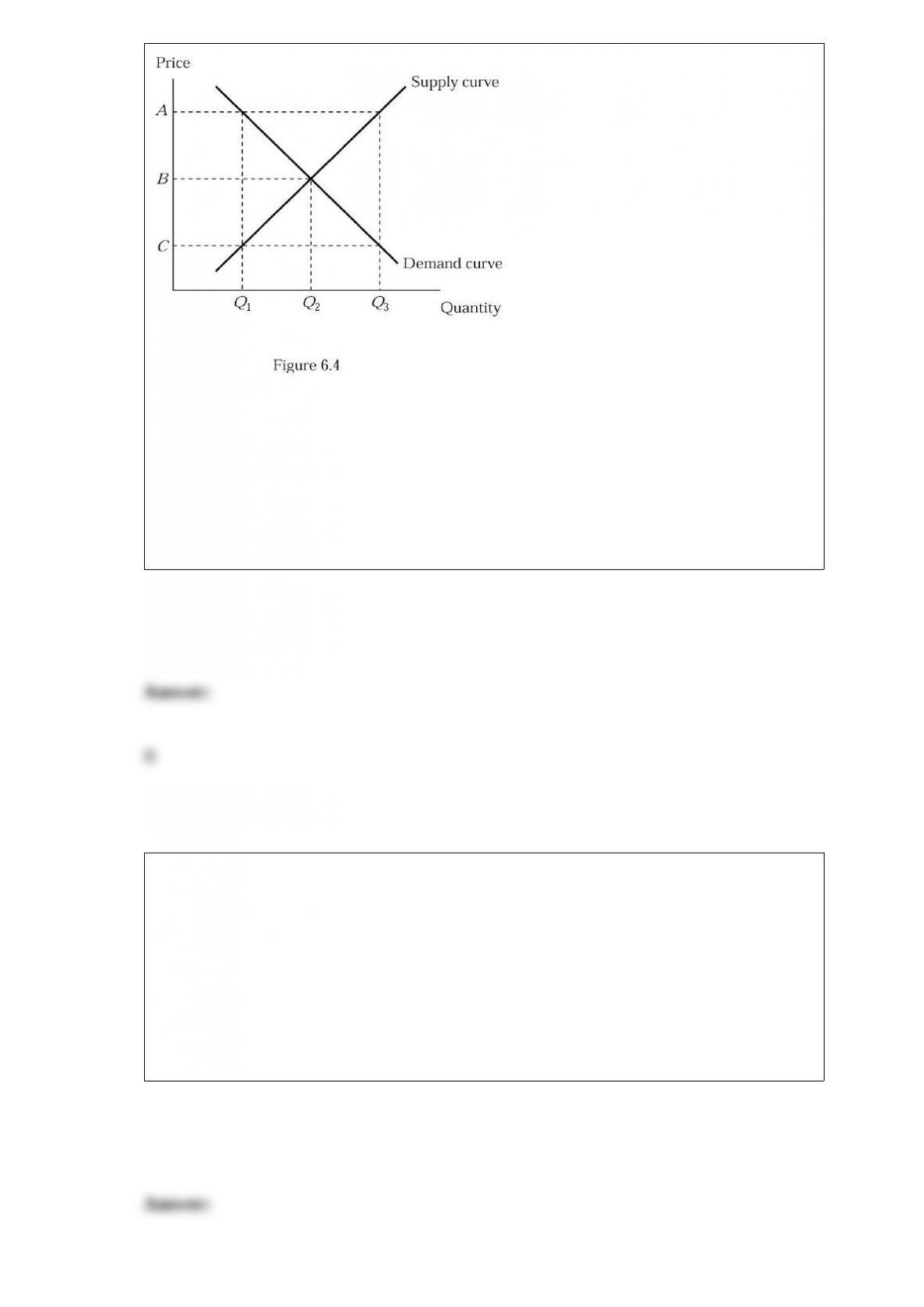

Refer to Figure 6.4. If the current market transactions occur only over the output level

where a buyer’s willingness to pay is greater than a seller’s willingness to accept, the

government could have set:

A) a maximum price at A.

B) a minimum price at A.

C) a minimum price at C.

D) There is not sufficient information.

Relative to a market with perfect information, in a market with imperfect information:

A) some goods will be sold in small quantities or not at all.

B) more than the equilibrium quantity of goods will be sold.

C) the equilibrium quantity will be sold, but at a price higher than the equilibrium price.

D) the equilibrium quantity will be sold for the equilibrium price.

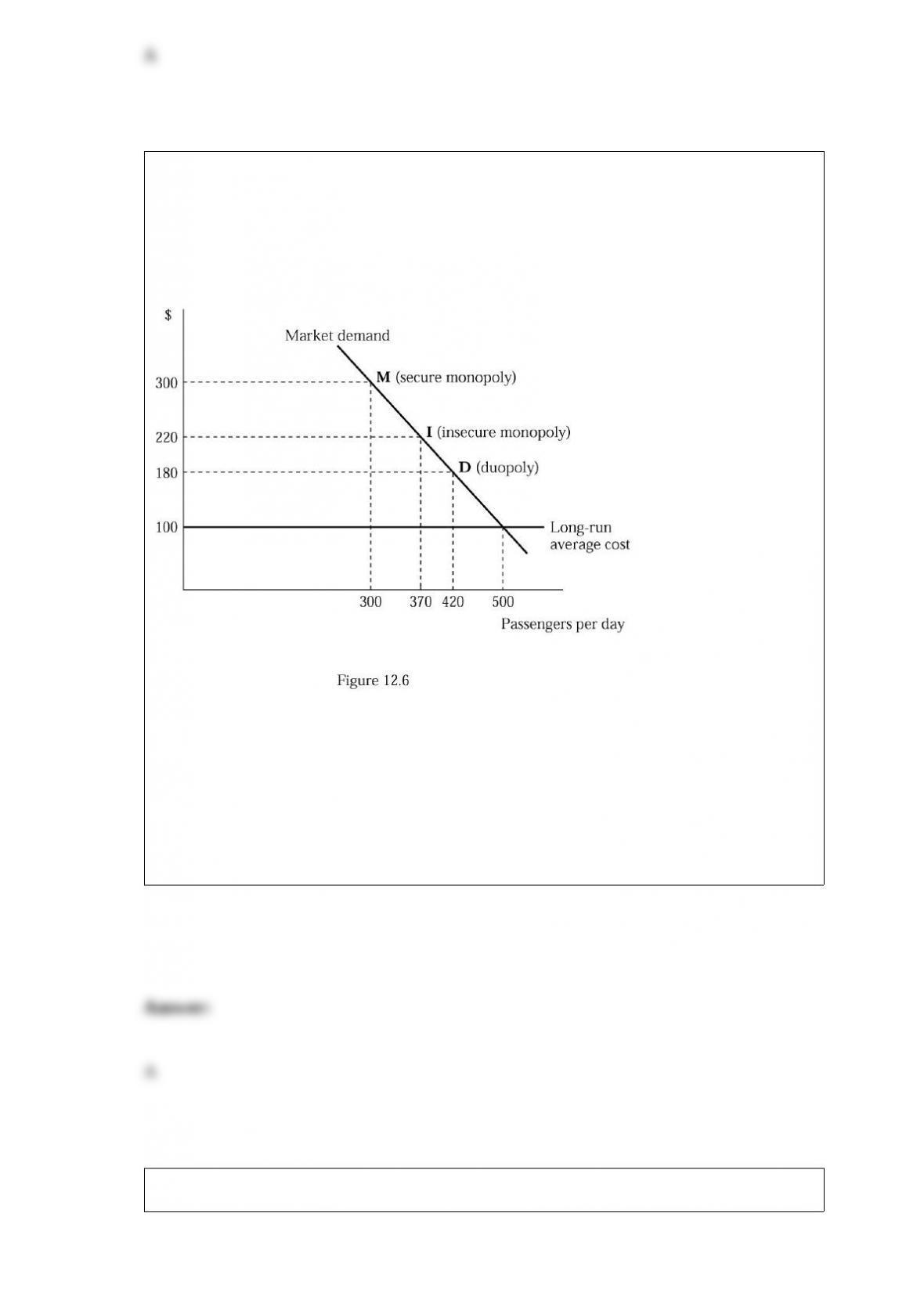

In Figure 12.6, airline Fly Smart is initially a secure monopoly between two cities X

and Y at point M, serving 300 passengers per day at the profit maximizing price of $300

per ticket. Suppose that Fly Smart discovers that a second airline is contemplating

entering the market. If the minimum market entry quantity is 130 passengers per day,

which is more profitable, entry deterrence or the passive duopoly outcome?

A) entry deterrence outcome

B) passive duopoly outcome

C) Fly Smart would earn the same profit.

D) There is not sufficient information.

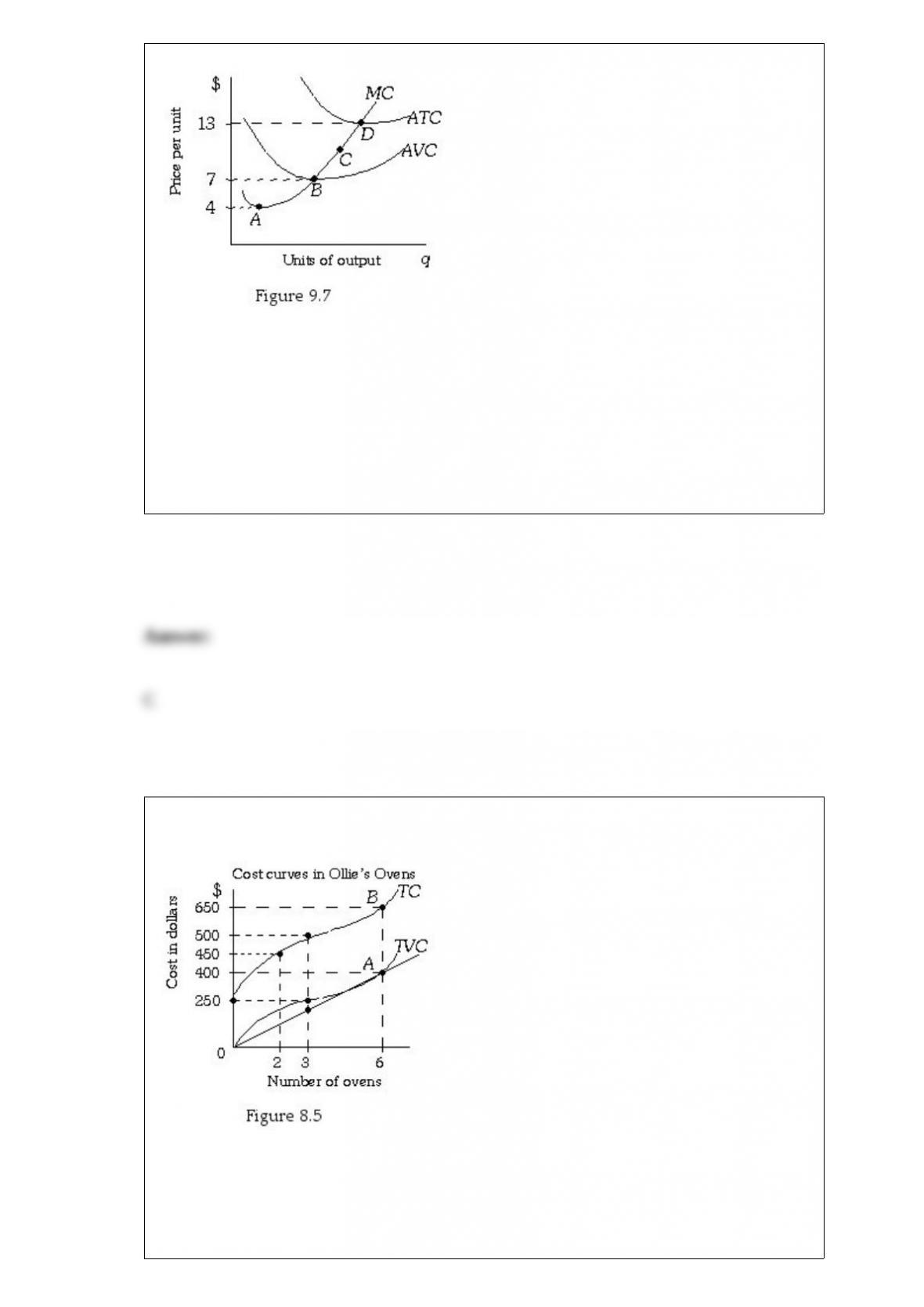

Refer to Figure 9.7. This firm’s short-run supply curve is the firm’s:

A) AVC curve to the left of Point B.

B) marginal cost curve above Point A.

C) marginal cost curve above Point B.

D) marginal cost curve above Point D.

Refer to Figure 8.5. The marginal cost of the third oven is:

A) $100.

B) $150.

C) $50.

D) indeterminate from this information.

Jason and Lauren live in the countryside 30 minutes from a main city in Virginia. They

moved there because they wanted to enjoy the fresh air. After a year of living in their

house, the 200 acres that surround their neighbor were zoned for an industrial property.

A paper mill was built in the zoning and now emits strong gases that can be smelt from

miles away, the paper mill’s emission of gases are an example of a (an):

A) public good.

B) good that imposes an external cost.

C) good that provides an external benefit.

D) efficient good.

Import bans, import quotas, voluntary export restraints, and tariffs on goods all:

A) increase imports and raise prices for consumers.

B) reduce imports and reduce prices for consumers.

C) reduce imports and raise prices for consumers.

D) increase imports and reduce prices for consumers.

Which of the following is true?

A) ATC = AVC – AFC

B) TVC/Q = TC/Q + TFC/Q

C) ΔTC/ΔQ = ΔAVC/ΔQ

D) ΔTVC/ΔQ = MC

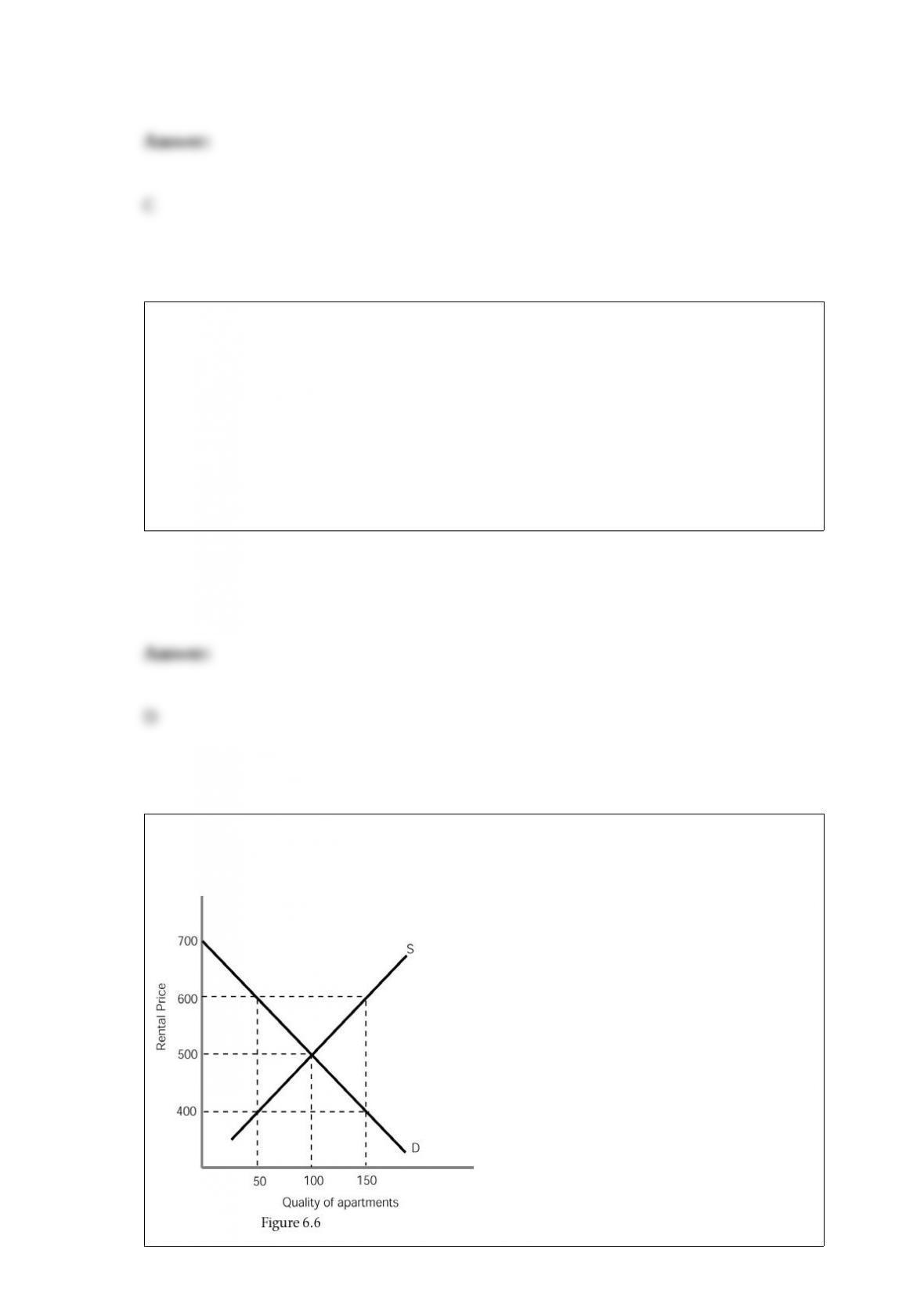

Refer to Figure 6.6. Suppose that the equilibrium quantity is 100. Consumer surplus is

equal to:

A) $20,000.

B) $10,000.

C) $200.

D) $30,000.

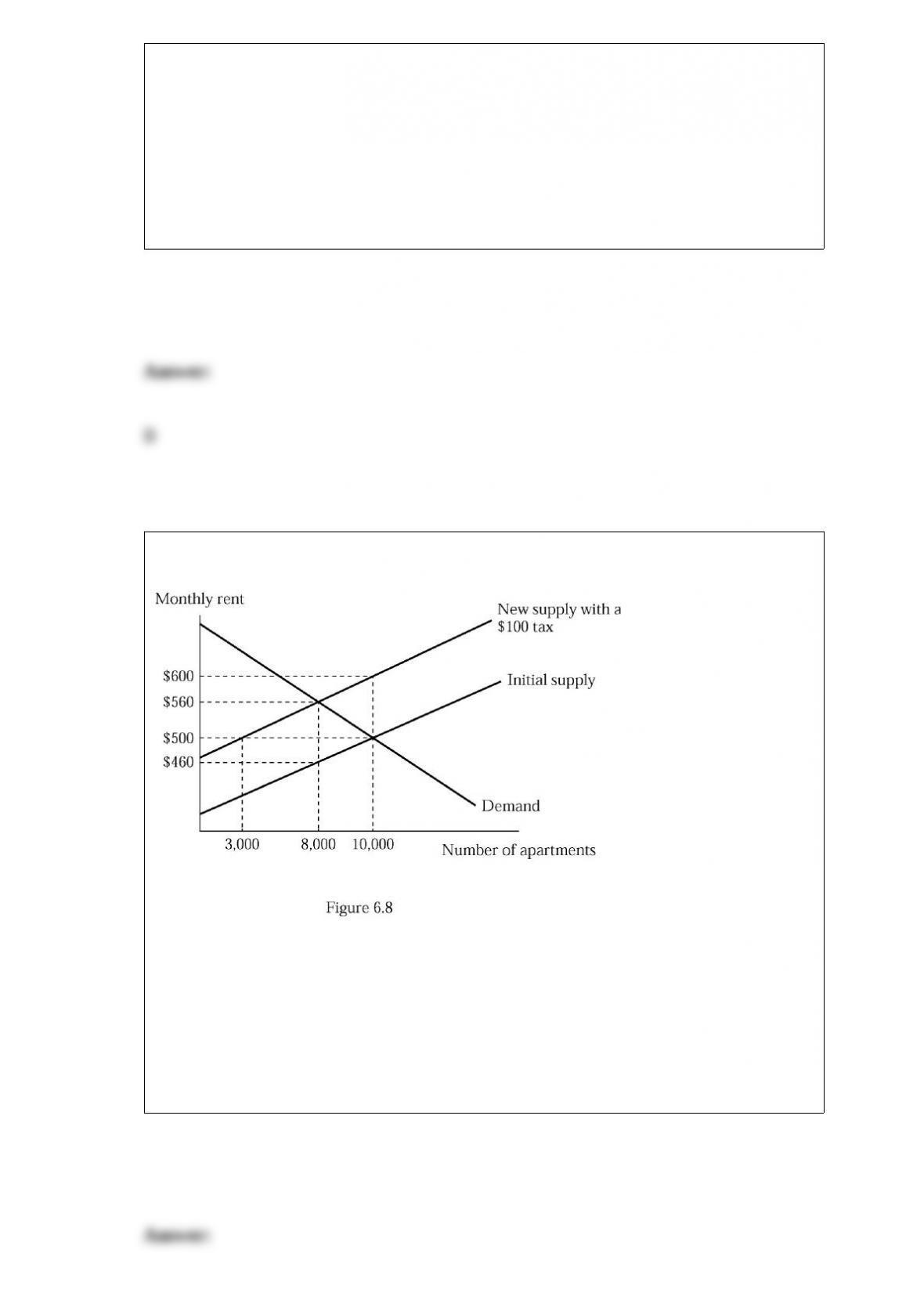

Refer to Figure 6.8. If your city imposes a tax of $100 per apartment:

A) consumers take the entire burden of the tax.

B) landlords take the entire burden of the tax.

C) consumers pay $60 and landlords pay $40 tax per apartment.

D) consumers pay $40 and landlords pay $60 tax per apartment.

Since a large or a small wind turbine have the same installation, operating and

maintenance costs, but a large turbine has four times the generating capacity but costs

less than three times as much as a small turbine, the wind power industry faces:

A) constant economies of scale.

B) economies of scale.

C) diseconomies of scale.

D) a hump shaped cost curve.

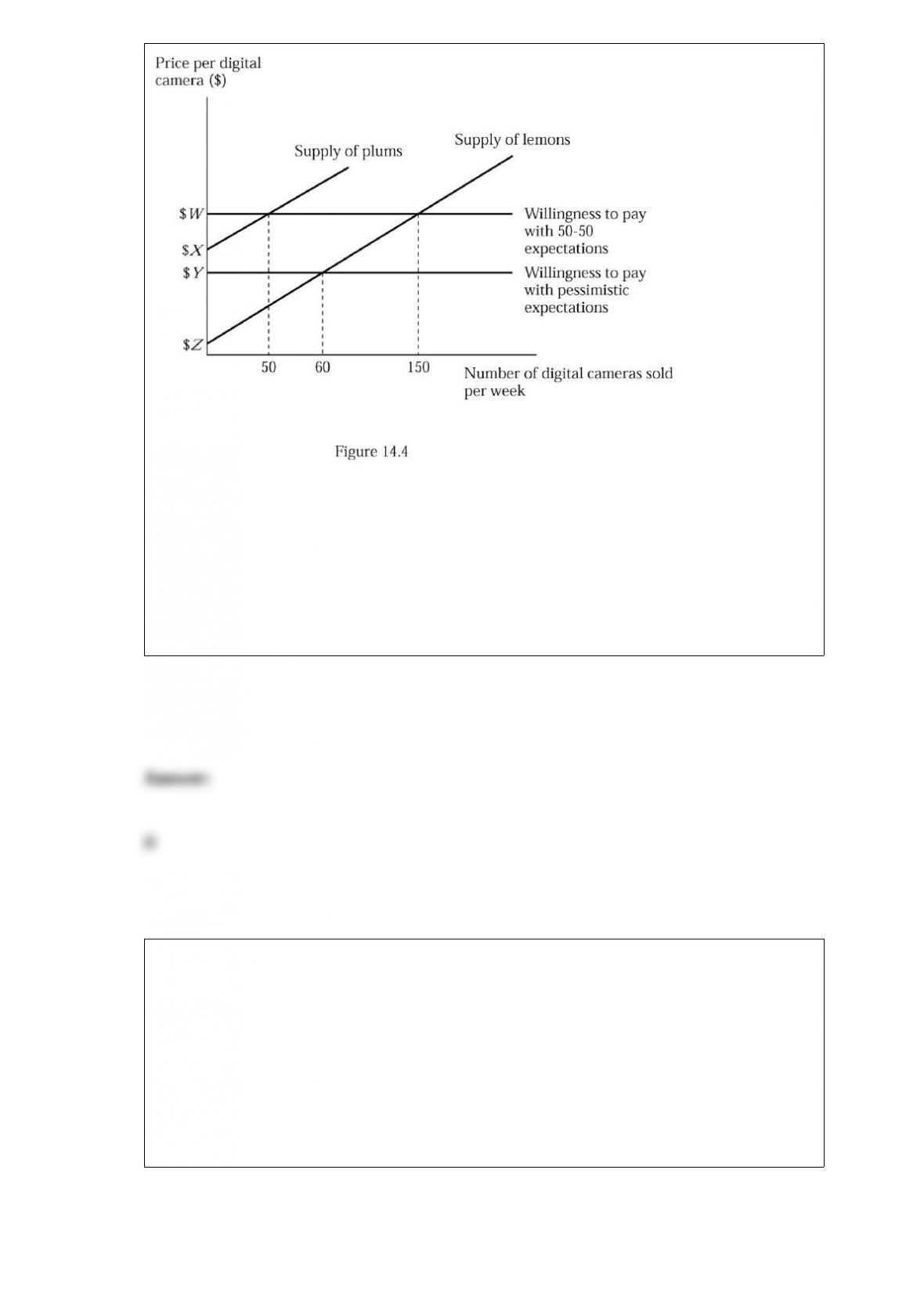

Figure 14.4 represents the market for used 12 megapixel digital cameras. Suppose

buyers are willing to pay $400 for a plum (high-quality) used digital camera and $200

for a lemon (low-quality) used digital camera. At any price between $X and $Z:

A) only plums will be supplied.

B) only lemons will be supplied.

C) both plums and lemons will be supplied

D) neither plums nor lemons will be supplied.

A person with a low level of glucose is more likely to:

A) make an impulsive decision.

B) make a cognitive decision.

C) avoid gut feelings.

D) base decisions on both gut feelings and cognition.

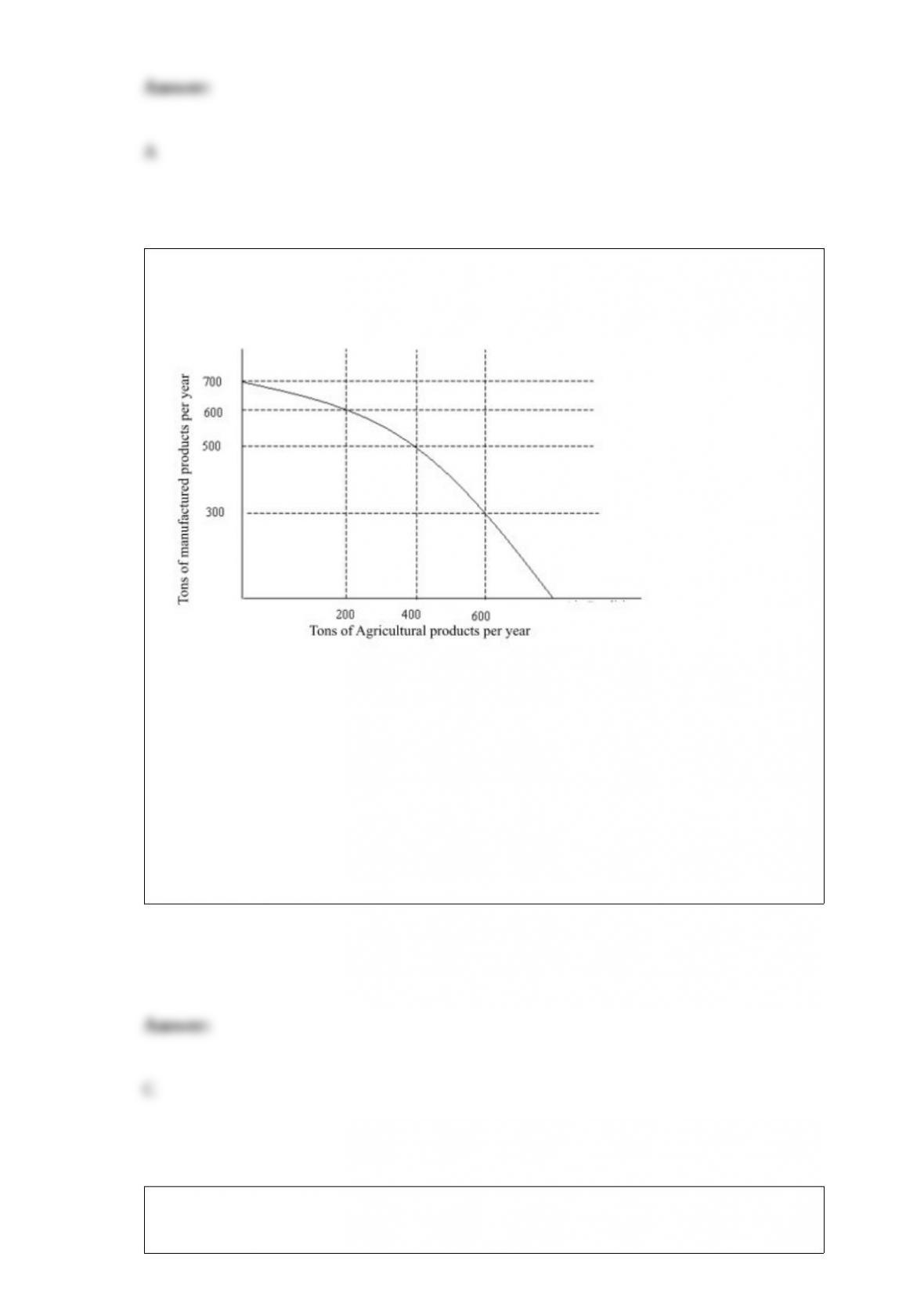

On the production possibilities curve in Figure 2.1 the gain from decreasing

manufacturing production from 500 tons to 300 tons is:

Figure 2.1

A) 700 tons of agriculture.

B) 500 tons of agriculture.

C) 200 tons of agriculture.

D) 100 tons of agriculture.

If the demand for illegal drugs is inelastic, then a government policy to cause their price

to increase would cause total revenue from drug sales to:

A) rise.

B) fall.

C) stay the same.

D) drop to zero.

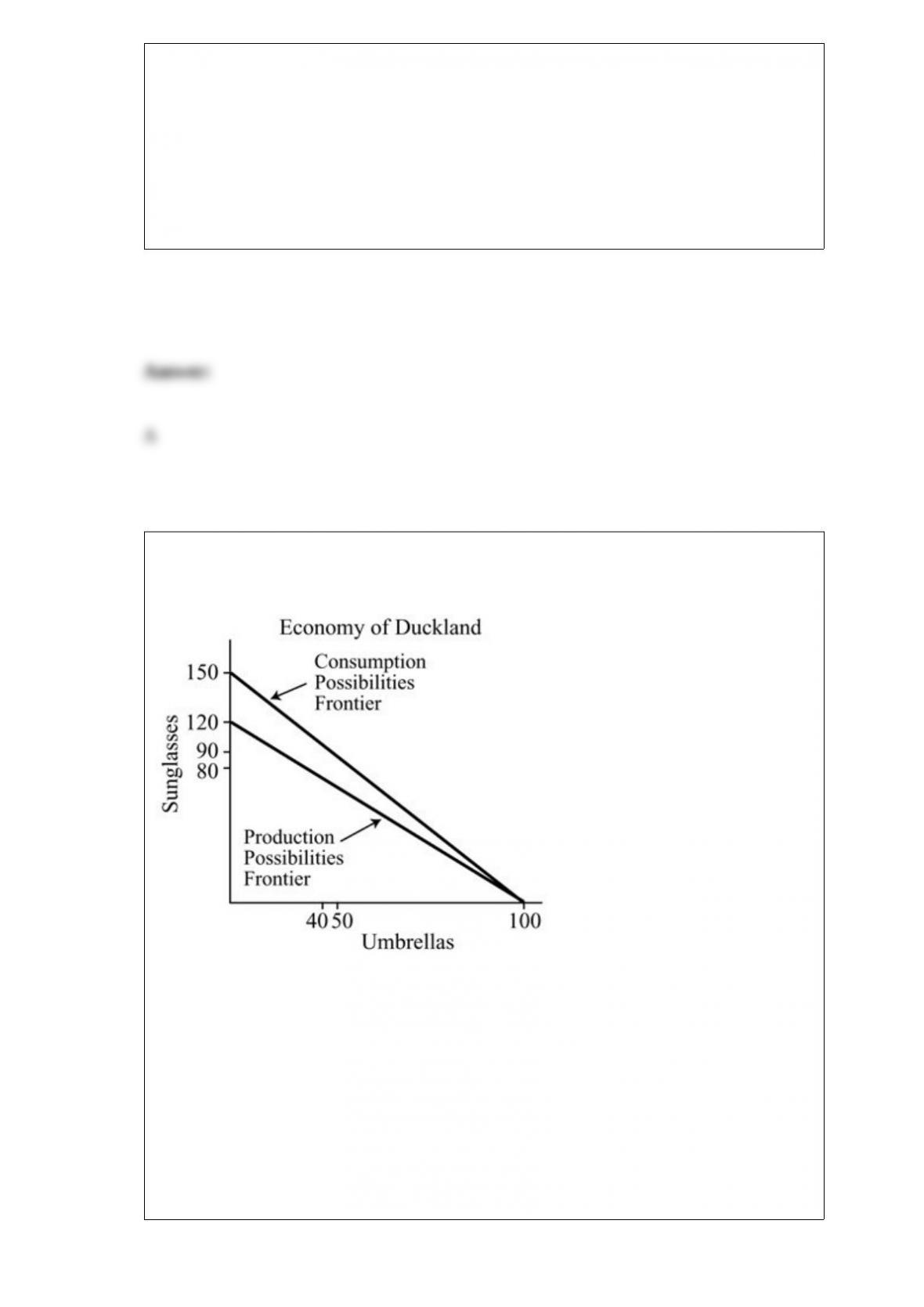

Figure 18.1

Refer to Figure 18.1. The opportunity cost of producing sunglasses in Duckland is:

A) 6/5 umbrellas.

B) 2/3 umbrellas.

C) 5/6 umbrellas.

D) 3/2 umbrellas.

Which of the following is an example of moral hazard?

A) a person who drives more recklessly after obtaining automobile insurance

B) a person who engages in unrisky behavior after enrolling in his firm’s health

insurance plan

C) a driver who reduces his level of insurance coverage after his premiums rise

D) all of the above

Which of the following is the best example of an oligopolistic industry?

A) cleaning services

B) airline services

C) local water utility

D) designer shoes

What are the two largest categories in federal government spending?

A) national defense and income security

B) Social Security and income security

C) national defense and medicare

D) Social Security and national defense

Using figures from the Application, the opportunity cost of running your business:

A) should only include the opportunity cost of the invested capital.

B) should include your invested capital.

C) should not include the invested capital.

D) should only include the opportunity cost of your time.

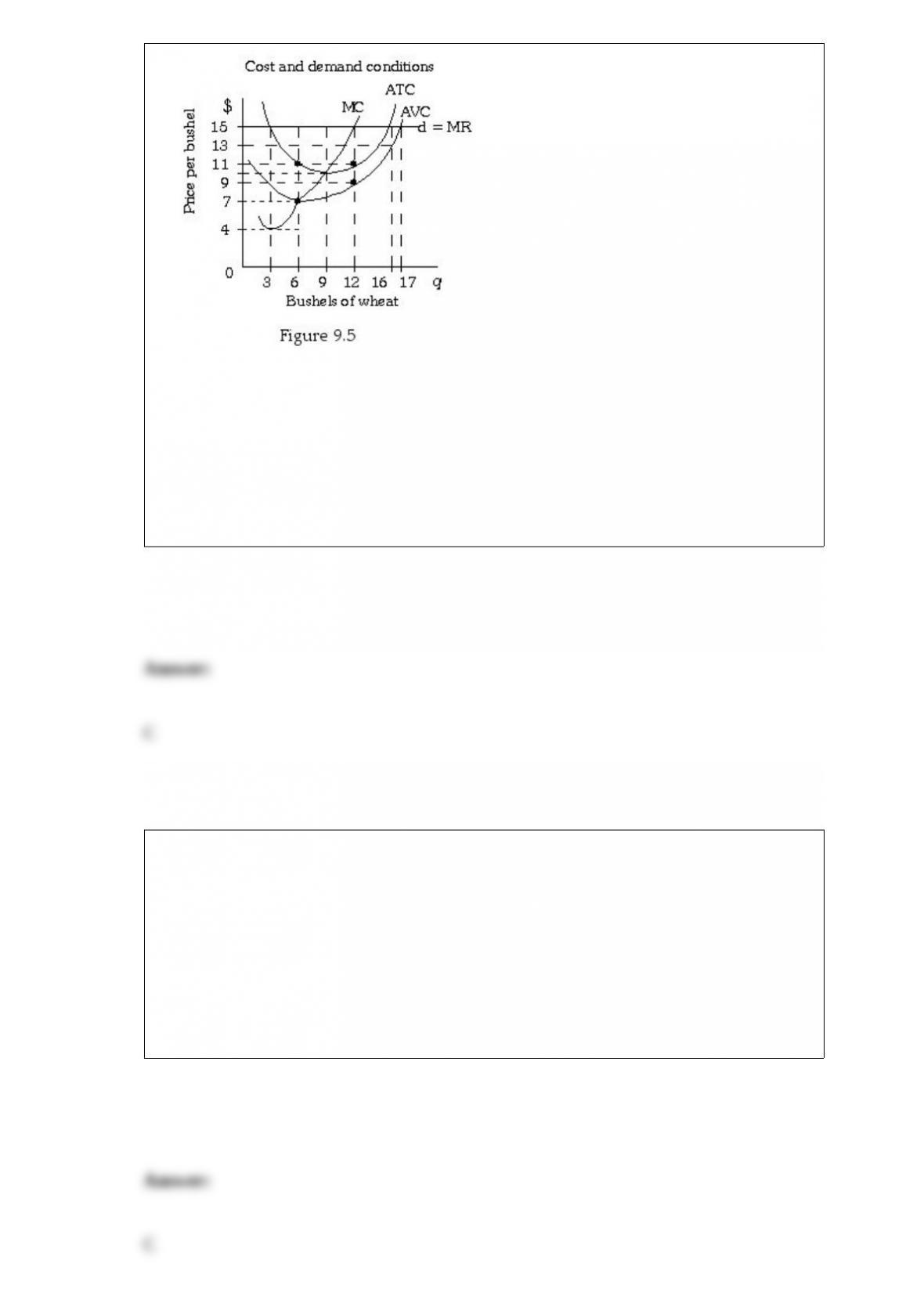

Refer to Figure 9.5. If this farmer is maximizing profits, his profit will be:

A) -$24.

B) $45.

C) $48.

D) $72.

The free-rider problem occurs for:

A) private goods and public goods.

B) private goods but not public goods.

C) public goods but not private goods.

D) neither public nor private goods.

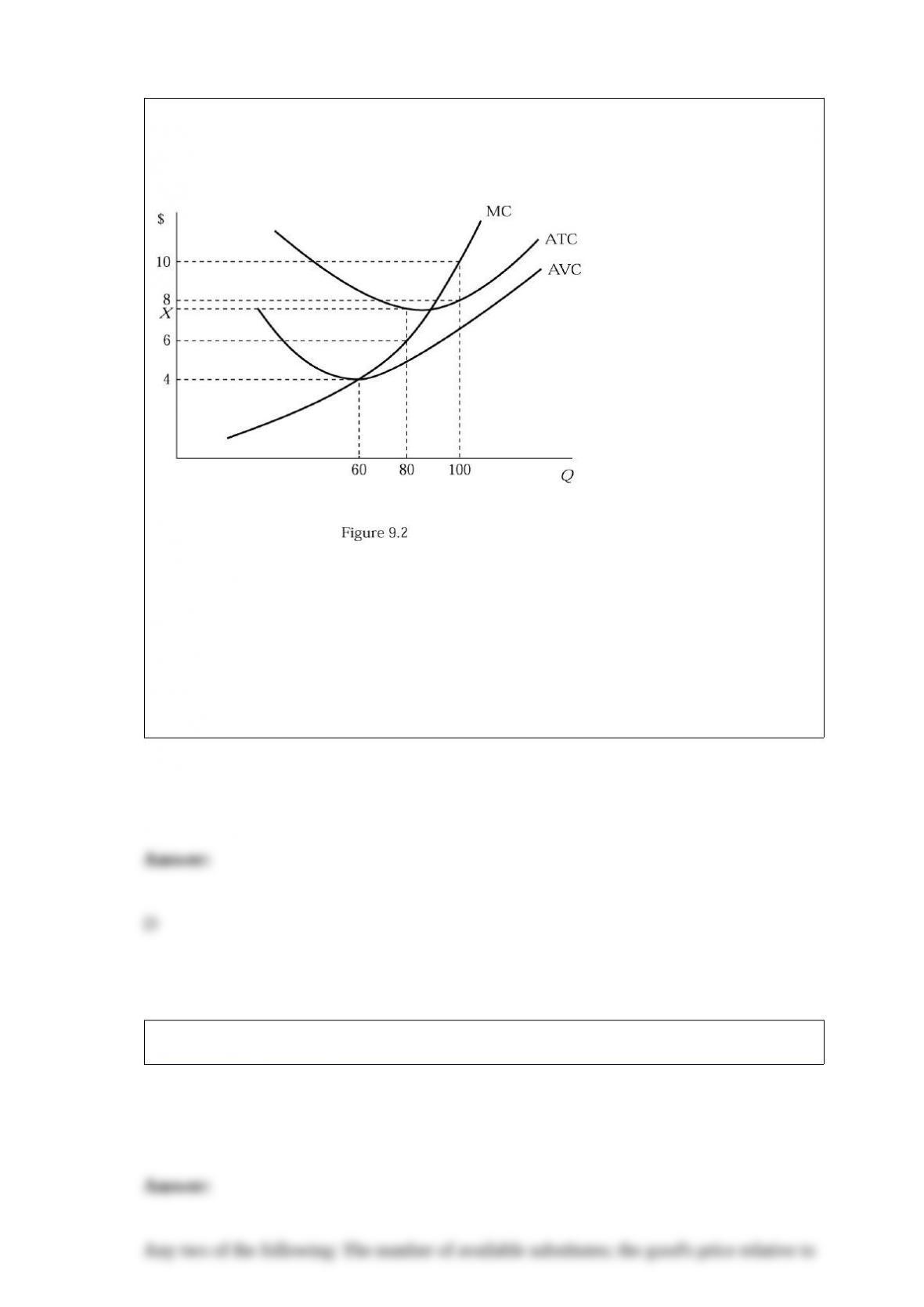

Figure 9.2 shows the cost structure of a firm in a perfectly competitive market. If the

market price is $10 and the firm chooses the profit maximizing output level, its profit

is:

A) $1,000.

B) $800.

C) $720.

D) $200.

List two determinants of price elasticity of demand.

When an electronics company advertises on the local newspaper a 10% discount

coupon , is this an example of price discrimination? Why or why not?

Explain how the “invisible hand” makes sure that markets reach equilibrium more

quickly than they would if the government sets prices for goods.

You are running a small yard maintenance business for the summer. What do you

expect to happen to the number of yards you can maintain in a day as you add workers

if you don’t purchase more capital equipment (like mowers and leaf blowers)?

Richard runs a pizza delivery restaurant. List the three basic types of decisions studied

in economics and give an example from Richard’s restaurant.

Why can car insurance companies charge higher auto rates for new customers than for

established customers, all else held constant?

What countries are members of the DR-CAFTA?

Consider a nation that has a comparative advantage in the production of goods using

unskilled labor. What types of workers will benefit from increased trade, and what type

will lose?

What are the explicit and implicit cost?

As a result of advances in technology, cellular telephones have become cheaper to

produce. Illustrate the effect of this change on the market for cellular telephones.

What is meant by utility?

Explain how an excess supply would lead to a decrease in prices in an unregulated

market.

Define price elasticity of demand. What does it measure?

What is the relationship between price elasticity of demand and total revenue for the

firm?

What did Adam Smith mean when he wrote that individuals rationally act in their own

self-interest?