Foundations of Microeconomics, 5e (Bade/Parkin)

Chapter 17 Oligopoly

17.1 What Is Oligopoly?

1) A firm faces a small number of competitors. This firm is competing in

A) a monopoly.

B) monopolistic competition.

C) an oligopoly.

D) perfect competition.

E) a perfect multi-firm monopoly.

2) Sammy’s Inc. competes with a few other firms because there are natural barriers to entry.

Sammy’s operates in

A) a perfectly competitive market.

B) an oligopoly.

C) a monopolistically competitive market.

D) a monopoly.

E) a natural monopolistically competitive market.

3) Herb’s Inc. has a large share of its market and is tempted to collude with the few firms that are

in its market. Herb’s operates in

A) an oligopoly.

B) a monopolistically competitive market.

C) a monopoly market.

D) a perfectly competitive market.

E) collusively protected market.

4) Which of the following is found ONLY in oligopoly?

A) producers who sell identical products

B) one firm’s actions affect another firm’s profit

C) entry into the industry is blocked

D) sellers face a downward sloping demand curve for their product

E) the firm’s demand curve is horizontal

5) Firms in an oligopoly

i. are independent of each others’ actions.

ii. can each influence the market price.

iii. charge a price equal to marginal revenue.

A) i only

B) ii only

C) iii only

D) i and iii

E) i, ii, and iii

6) In an oligopoly, there are

A) many firms and barriers to entry.

B) many firms and no barriers to entry.

C) few firms and barriers to entry.

D) few firms and no barriers to entry.

E) barriers to entry and only one firm.

7) A cartel is

A) a market structure with a small number of large firms.

B) a market structure with a large number of small firms.

C) a group of firms acting together to raise price, decrease output, and increase economic profit.

D) a market with only two firms.

E) another name for an oligopoly.

8) A group of firms acting together to limit output, raise price, and increase economic profit is a

called a

A) duopoly.

B) monopolistic oligopoly.

C) competitive oligopoly.

D) cartel.

E) multi-firm competitive monopoly.

9) A cartel is a collusive agreement among a number of firms that is designed to

A) expand output and lower prices but not to a predatory level.

B) restrict output and lower prices to a predatory level.

C) restrict output and raise prices.

D) expand output and raise prices.

E) expand output and lower prices to a predatory level.

10) A cartel is

A) a group of firms selling identical products but at slightly different prices.

B) an agreement among firms to limit output, raise prices, and increase economic profit.

C) the automobile producing industry.

D) the only firm selling a particular product.

E) an illegal agreement among firms which most often arises in monopolistically competitive

markets.

11) A group of firms that has entered into an agreement to restrict output and increase prices and

profits is called

A) a compliance.

B) a cartel.

C) an oligopoly.

D) a duopoly.

E) a multi-firm monopoly.

12) If a few oil-producing countries in the Middle East decide to jointly limit the production of

oil,

A) they are forming a cartel.

B) they would like the price of oil to be the same as if the market were perfectly competitive.

C) game theory does not apply to their actions because they are nations, not firms.

D) they will try to operate as a large, monopolistically competitive firm.

E) they will agree to lower the price of oil in order to increase their profits.

13) Daryl’s Inc. has formed a cartel with the two other firms in its industry. In which of the

following market structures does Daryl’s operate?

A) monopolistic competition.

B) oligopoly.

C) perfect competition.

D) monopoly.

E) legally protected monopoly.

14) A cartel is most likely to occur in

A) perfect competition as firms compete by reducing cost.

B) oligopoly as firms act together to raise prices and increase profits.

C) monopolistic competition where firms collude to increase profits.

D) oligopoly as firms compete to lower price and increase their own profits.

E) monopoly because it faces no competition.

15) “Duopoly” is

A) another name for monopoly.

B) a special type of monopolistic competition.

C) a two-firm oligopoly.

D) a game with three players.

E) the situation when a firm sets a duo (two) of different prices for its customers.

16) A two-firm oligopoly is called a

A) double monopoly.

B) cartel.

C) duopoly.

D) monopolistic oligopoly.

E) dual-market.

17) An oligopoly created because of economies of scale is called a

A) natural oligopoly.

B) legal oligopoly.

C) public oligopoly.

D) monopolistic oligopoly.

E) scale oligopoly.

18) When economies of scale limit the number of firms in an industry to 3, there is a

A) natural monopoly.

B) natural oligopoly.

C) legal oligopoly.

D) legal cartel.

E) natural monopolistic competition.

19) There are two bookstores in a college town. If another bookstore opened, each of the stores

would incur an economic loss. This bookstore market is

A) a natural monopoly.

B) a monopoly.

C) monopolistic competition.

D) a natural oligopoly.

E) a legal oligopoly.

20) A firm faces a small number of competitors. This firm is competing in

A) a monopoly.

B) monopolistic competition.

C) an oligopoly.

D) perfect competition.

E) a perfect multi-firm monopoly.

21) If an industry has an HHI of 2,500, the market structure is that of

A) a monopoly.

B) monopolistic competition.

C) an oligopoly.

D) perfect competition.

E) either monopoly or perfect competition, depending on the existence or absence of barriers to

entry.

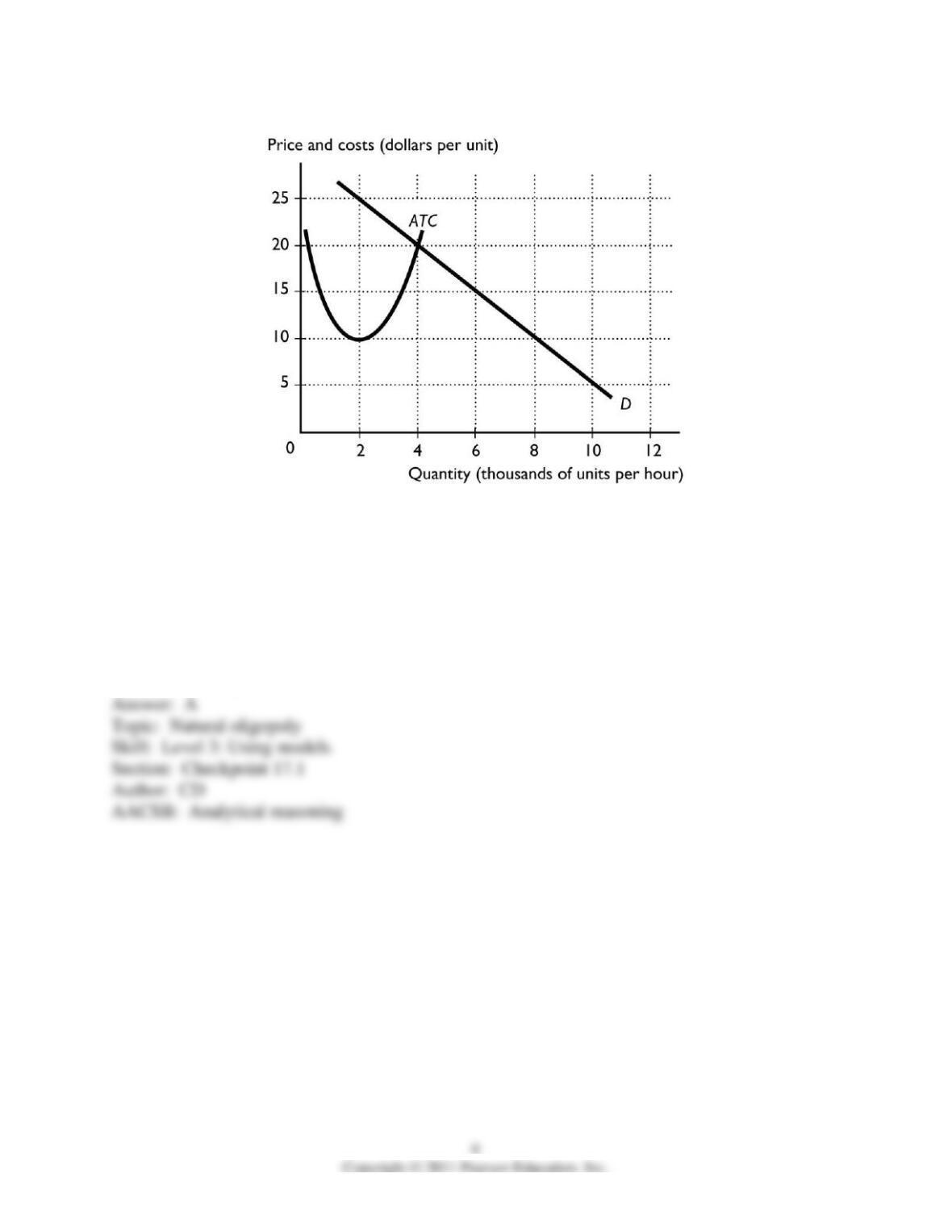

22) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the efficient scale for one firm is ________ units per

hour.

A) 2,000

B) 4,000

C) 8,000

D) 10,000

E) more than 10,000

23) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the lowest price at which a firm could stay in business in

the long run is ________ per unit and the quantity demanded in the market at that price is

________ units per hour.

A) $20; 4,000

B) $10; 8,000

C) $10; 4,000

D) $20; 2,000

E) $20; 8,000

24) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the figure shows a ________ can profitably operate.

A) natural monopoly in which 1 firm

B) natural oligopoly in which 2 firms

C) natural oligopoly in which 3 firms

D) natural oligopoly in which 4 firms

E) natural oligopoly in which 5 more firms

25) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, economies of scale limit the market to ________

firm(s).

A) 1

B) 2

C) 3

D) 4

E) 8

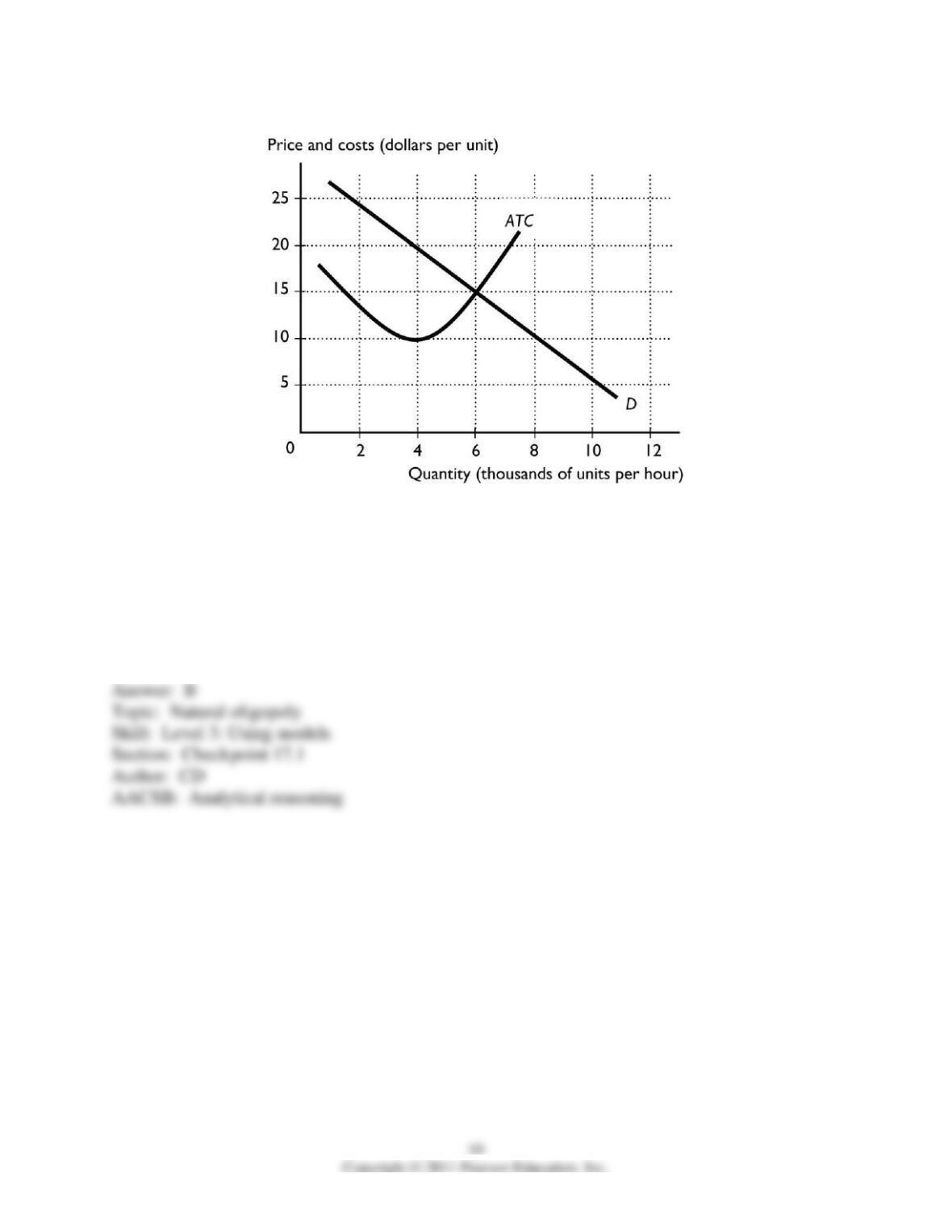

26) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the efficient scale for one firm is ________ units per

hour.

A) 2,000

B) 4,000

C) 8,000

D) 6,000

E) 10,000

27) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the lowest price at which a firm could stay in business in

the long run is ________ per unit and the quantity demanded in the market at that price is

________ units per hour.

A) $15; 6,000

B) $10; 8,000

C) $10; 6,000

D) $25; 2,000

E) $10; 4,000

28) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, the figure shows a ________ can profitably operate.

A) natural monopoly in which 1 firm

B) natural monopoly in which 2 firms

C) natural oligopoly in which 3 firms

D) natural oligopoly in which 2 firms

E) natural oligopoly in which 8 firms

29) The figure above shows the market demand curve and the ATC curve for a firm. If all firms

in the market have the same ATC curve, economies of scale limit the market to ________

firm(s).

A) 1

B) 2

C) 3

D) 4

E) 8

30) When a city licenses only 3 taxi firms to serve the market, the city has created a

A) cartel.

B) legal monopoly.

C) monopolistically competitive market.

D) legal oligopoly.

E) natural oligopoly.

31) Oligopoly is a market structure in which

A) many firms each produce a slightly differentiated product.

B) one firm produces a unique product.

C) a small number of firms compete.

D) many firms produce an identical product.

E) the number of firms is so small that they do not compete with each other.

32) The fact that firms in oligopoly are interdependent means that

A) there are barriers to entry.

B) one firm’s profits are affected by other firms’ actions.

C) they can produce either identical or differentiated goods.

D) there are too many of them for any one firm to influence price.

E) they definitely compete with each other so that the price is driven down to the monopoly

level.

33) Collusion results when a group of firms

i. act separately to limit output, lower prices, and decrease economic profits.

ii. act together to limit output, raise prices, and increase economic profits.

iii. in the United States legally fix prices.

A) i only

B) ii only

C) iii only

D) i and iii

E) ii and iii

34) A cartel is a group of firms

A) acting separately to limit output, lower price, and decrease economic profit.

B) acting together to limit output, raise price, and increase economic profit.

C) legally fixing prices.

D) acting together to erect barriers to entry.

E) that compete primarily with each other rather than the other firms in the market.

35) A market with only two firms is called a

A) duopoly.

B) two-firm monopolistic competition.

C) two-firm monopoly.

D) cartel.

E) two-firm quasi monopoly.

36) The efficient scale of one firm is 20 units and the average total cost at the efficient scale is

$30. The quantity demanded in the market as a whole at $30 is 40 units. This market is

A) a natural duopoly.

B) a legal duopoly.

C) a natural monopoly.

D) a legal monopoly.

E) monopolistically competitive.

37) Even though four firms can profitably sell hotdogs downtown, the government licenses only

two firms. This market is a

A) natural duopoly.

B) legal duopoly.

C) natural monopoly.

D) legal monopoly.

E) market-limited oligopoly.

38) To determine if a market is an oligopoly, we need to determine if

A) the market’s HHI is less than 900.

B) there are many firms in the market.

C) the firms are so few that they recognize their mutual interdependencies.

D) the firms make identical or differentiated products.

E) cartels are legal in their market.

17.2 The Oligopolist’s Dilemma

1) When oligopolies seek to operate as a single-price monopoly, the firms produce at the point

where:

A) P = MC.

B) MR = MC.

C) P < ATC.

D) P = MR.

E) MC = ATC.

2) When firms in an oligopoly successfully collude and do not cheat on a cartel agreement, they

can achieve long-run economic profit similar to

A) perfect competition.

B) monopoly.

C) monopolistic competition.

D) non-colluding oligopolies.

E) the firms in regulated industries.

3) If firms in an oligopolistic industry successfully collude and form a cartel, what price and

output will result?

A) the monopoly price and output

B) the competitive price and output

C) the monopolistically competitive price and output

D) a price higher than the monopoly price and, because there is more than one firm in the

industry, more output than the monopoly amount

E) a price lower than the competitive price and, because there are only a few firms in the

industry, less output than the competitive amount

4) When oligopolies operate like firms in perfect competition, the firms produce at the point

where the

A) price is less than the marginal cost.

B) marginal cost equals the price.

C) price exceeds the marginal cost by the greatest amount.

D) price exceeds the average total cost by the greatest amount.

E) marginal cost equals the average total cost.

5) If firms in an oligopolistic industry consistently cut their price to sell more output, what price

and output will result?

A) the monopoly price and output

B) the competitive price and output

C) the monopolistically competitive price and output

D) a price lower than the competitive price and less output than the competitive amount

E) a price lower than the competitive price and more output than the competitive amount

6) The range in which a duopoly’s output falls is less than or equal to the output level in

________ and more than or equal to the output level in ________.

A) monopolistic competition; monopoly

B) monopolistic competition; perfect competition

C) perfect competition; monopoly

D) monopoly; monopolistic competition

E) monopoly; perfect competition

7) In an oligopoly, output is

A) less than the output in monopoly.

B) greater than the output in perfect competition.

C) in all circumstances the same as the output in perfect competition.

D) somewhere between the output in monopoly and that in perfect competition outcomes.

E) in all circumstances the same as the output in monopoly.

8) The possible alternatives for an oligopoly range from the monopoly case with ________ to the

perfectly competitive case with ________.

A) high output; low output

B) low prices; high prices

C) low profits; high profits

D) low output; high output

E) no cooperation among the firms; much cooperation among the firms

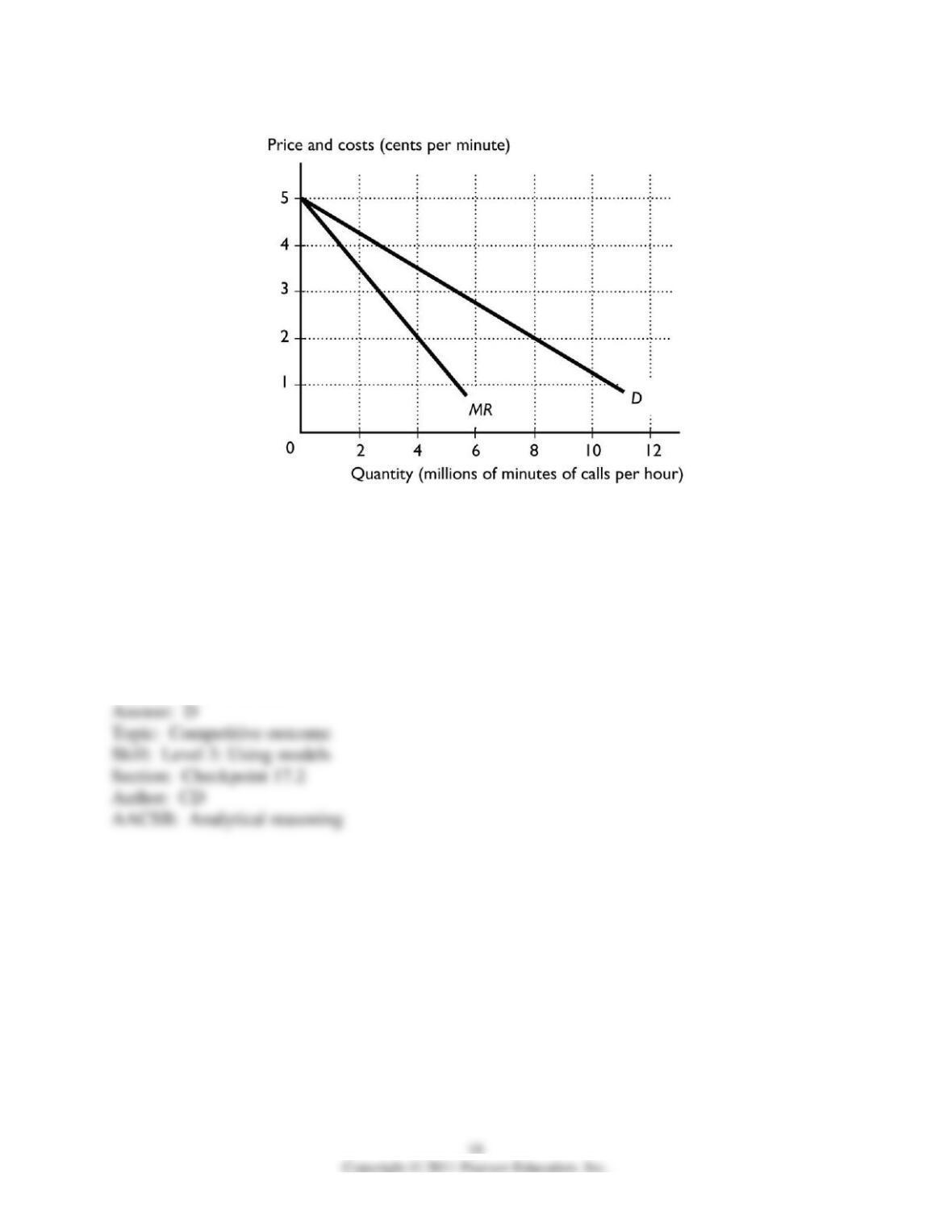

9) The above figure shows the market demand curve for long-distance telephone calls. Suppose

the marginal cost of a long-distance telephone call is 2¢ a minute for a call no matter how many

minutes of calls are made and there are 3 firms in the industry. If the firms in the industry operate

as perfect competitors, there are ________ minutes of calls made per hour.

A) between 0 and 3 million

B) more than 3 million and less than or equal to 5 million

C) more than 5 million and less than or equal to 7 million

D) more than 7 million and less than or equal to 9 million

E) more than 9 million

10) The above figure shows the market demand curve for long-distance telephone calls. Suppose

the marginal cost of a long-distance telephone call is 2¢ a minute for a call no matter how many

minutes of calls are made and there are 3 firms in the industry. If the firms in the industry operate

as a monopoly, there are ________ minutes of calls made per hour.

A) between 0 and 3 million

B) more than 3 million and less than or equal to 5 million

C) more than 5 million and less than or equal to 7 million

D) more than 7 million and less than or equal to 9 million

E) more than 9 million

11) The above figure shows the market demand curve for long-distance telephone calls. Suppose

the marginal cost of a long-distance telephone call is 2¢ a minute for a call no matter how many

minutes of calls are made and there are 3 firms in the industry. If the firms in the industry operate

as perfect competitors, the price of a call is ________ per minute and if the firms in the industry

operate as a monopoly, the price of a call is ________ per minute.

A) 2 cents; more than 3 cents and less than 4 cents

B) more than 3 cents and less than 4 cents; more than 3 cents and less than 4 cents

C) 1 cents; 2 cents

D) 2 cents; either equal to 4 cents or more than 4 cents

E) either equal to 4 cents or more than 4 cents; 2 cents

12) Which of the following statements is correct?

A) A firm in oligopoly will charge a price that is lower than the price charged in perfect

competition.

B) If firms in oligopoly look only at their own self-interest in deciding the output they should

produce, the total market output will exceed that of a monopoly.

C) If one oligopolist reduces the price of its product, its demand curve shifts leftward.

D) Because many producers join to form a cartel, the market becomes monopolistic competition.

E) It is in the self-interest of each firm in an oligopoly to take the actions that maximize all the

firms’ joint profit.

13) The major dilemma facing Boeing and Airbus is the

A) fact that neither will respond to the behavior of the other.

B) certainty surrounding the reaction of each firm to the behavior of the other firm.

C) fact that if each firm separately tries to maximize its profit, it might wind up with less profit

that otherwise.

D) competition from other firms that drives their economic profit to zero.

E) fact that when they collude to maximize their profit, the other firm’s profit might be larger

than its profit.

14) Imagine a duopoly in which two firms, A and B, produce the monopoly profit-maximizing

output and equally share the economic profit. If firm A increases output,

A) both firms’ profits increase.

B) firm A’s profits increase and firm B’s profits decrease.

C) firm B’s profits increase and firm A’s profits decrease.

D) both firms’ profits decrease.

E) firm A’s profits increase and firm B’s profits do not change.