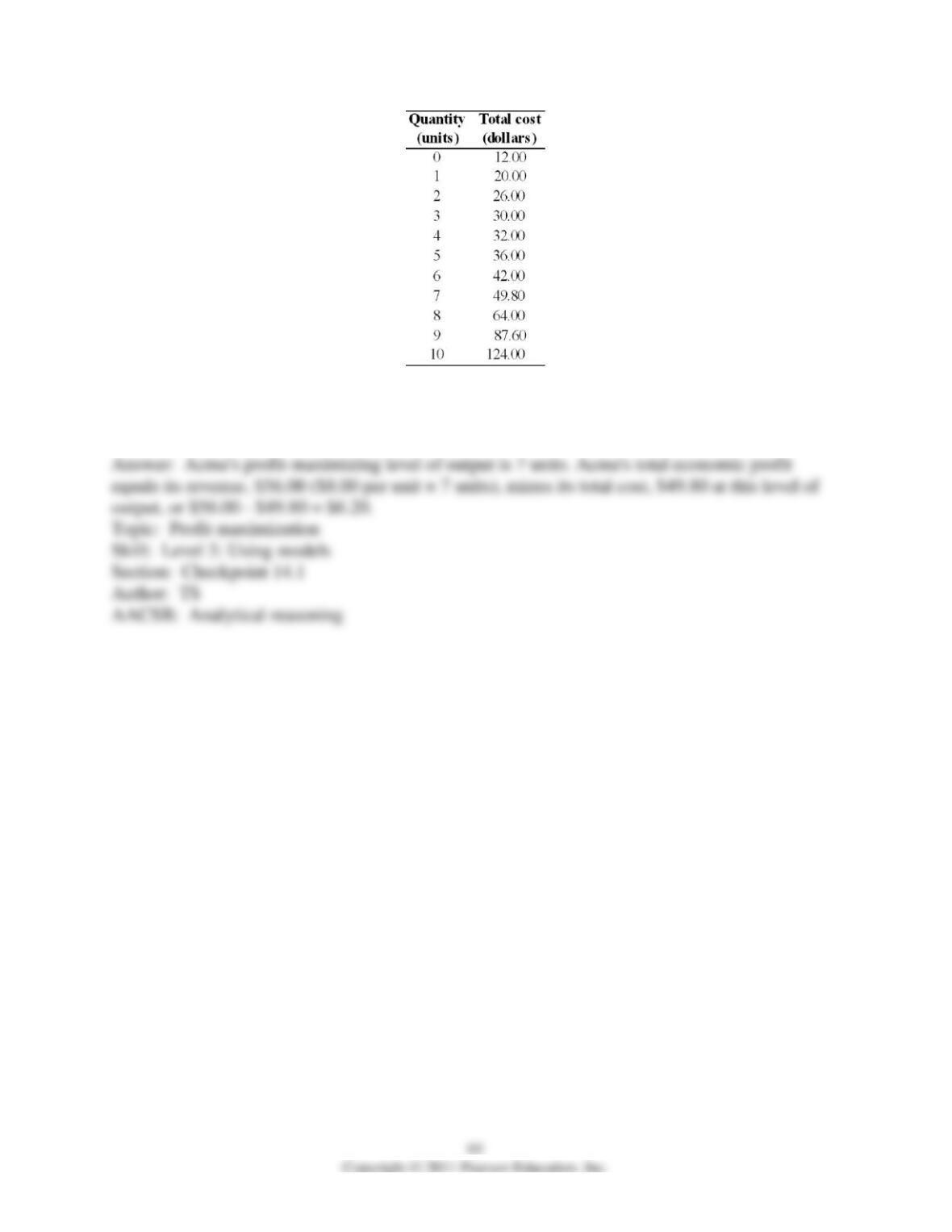

24) Acme is a perfectly competitive firm. It has the total cost schedule given in the above table.

Acme’s product sells for $8.00 per unit. What amount of output is the most profitable and what is

Acme’s economic profit or economic loss?

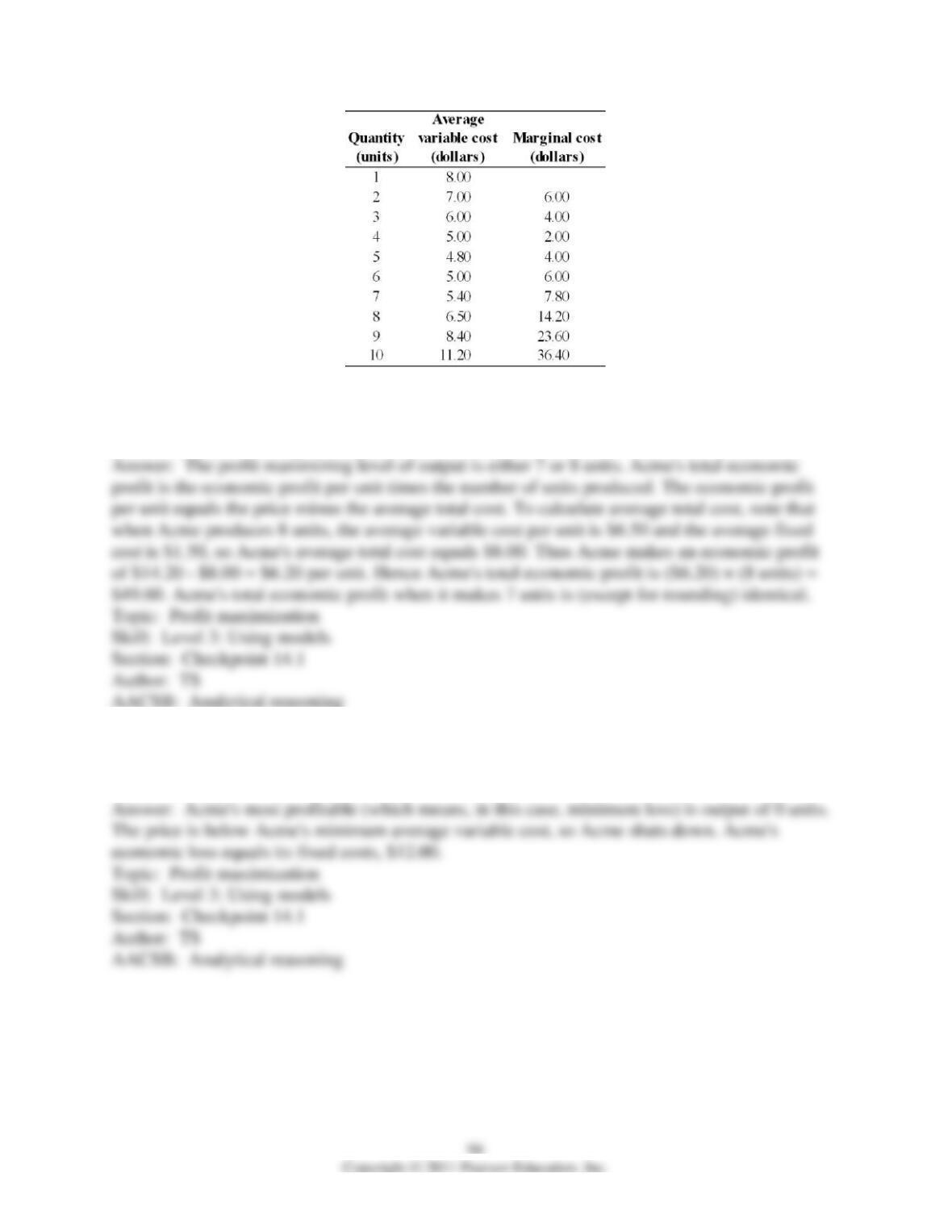

25) Acme is a perfectly competitive firm. It has the cost schedules given in the above table and

has a fixed cost of $12.00. The price of Acme’s product is $14.20. What is Acme’s most

profitable amount of output? What is Acme’s total economic profit or loss?

26) Acme is a perfectly competitive firm. It has the cost schedules given in the above table and

has a fixed cost of $12.00. The price of Acme’s product is $4.00. What is Acme’s most profitable

amount of output? What is Acme’s total economic profit or loss?

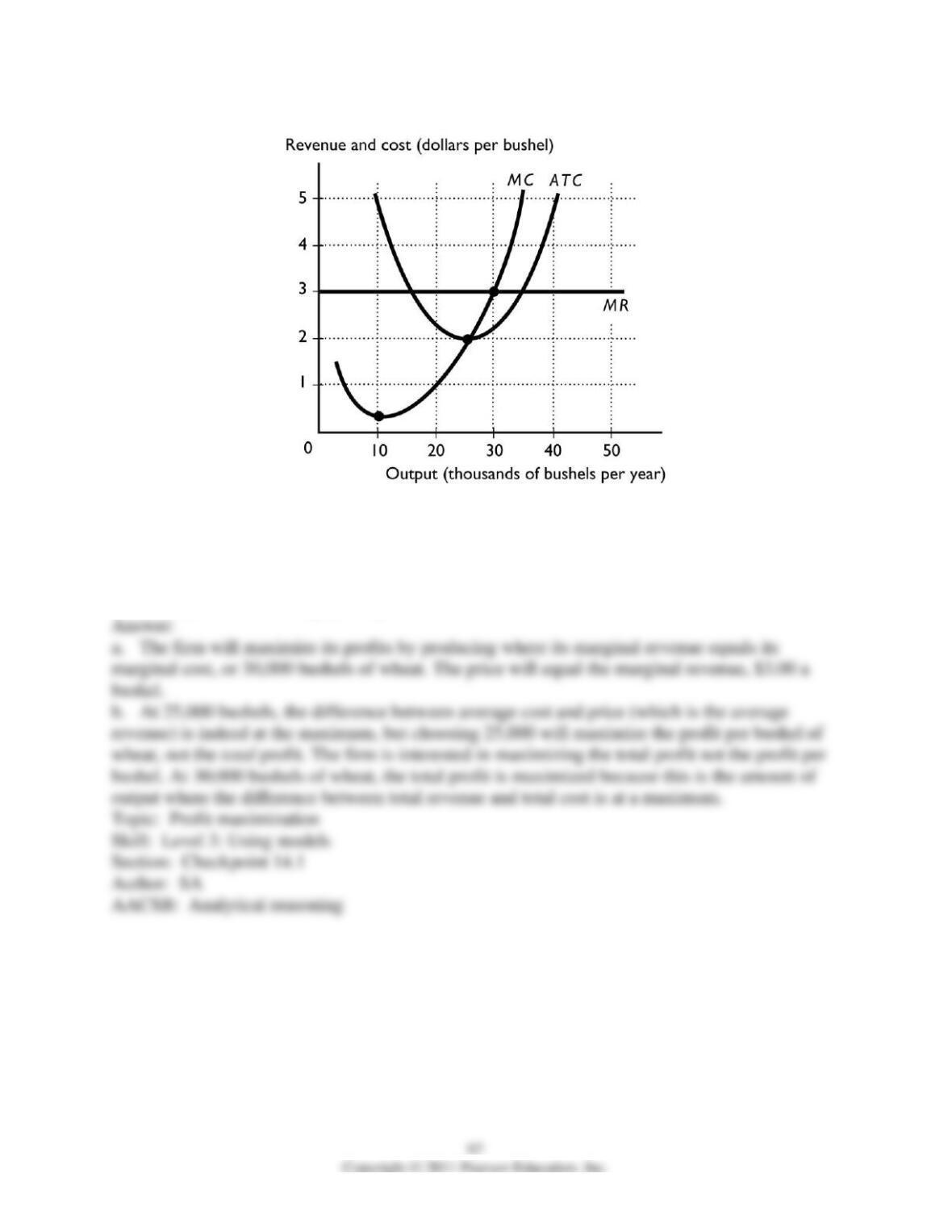

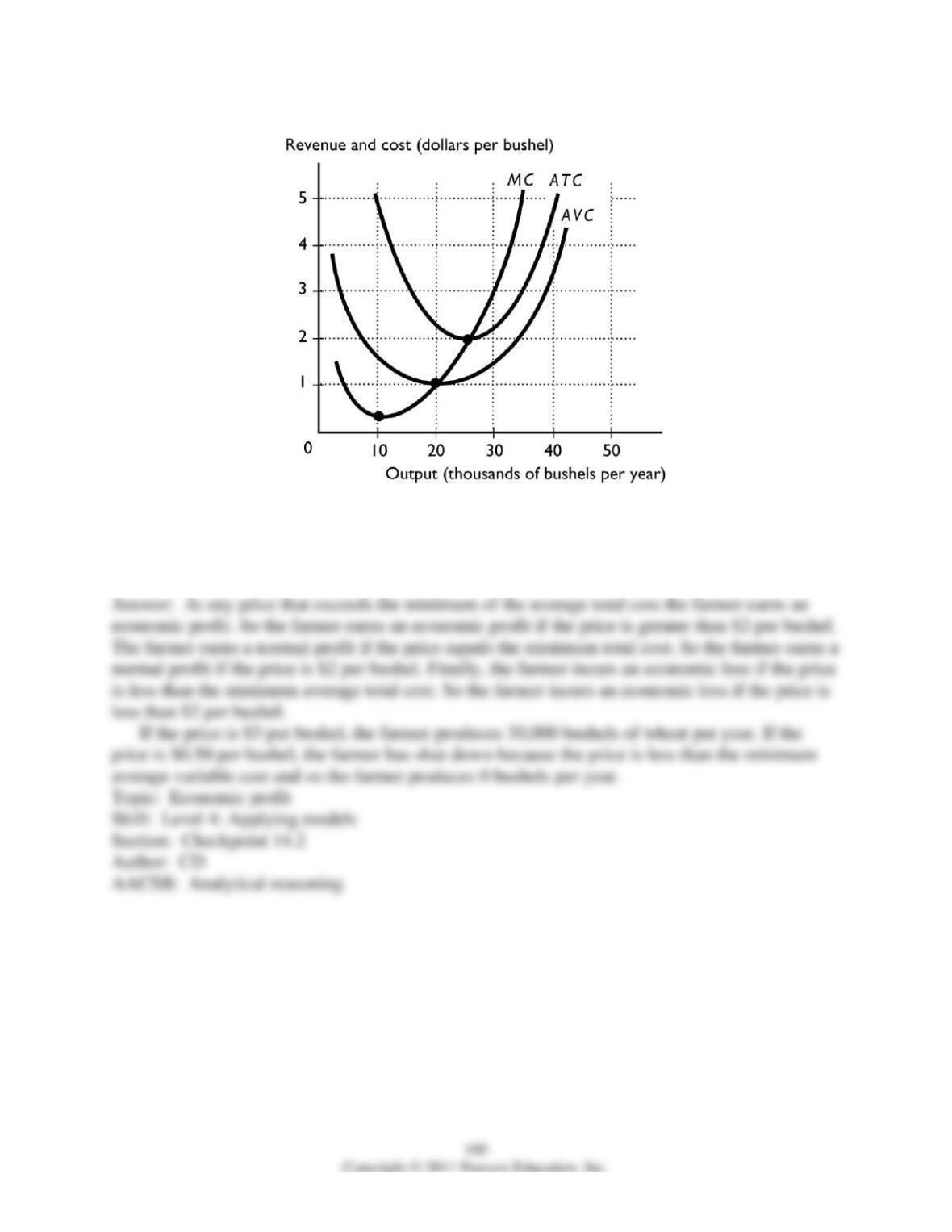

27) The above figure illustrates a perfectly competitive wheat farmer.

a. What will be the firm’s profit-maximizing price and output?

b. When the farmer produces 25,000 bushels of wheat, the difference between the firm’s

average total cost and the price is at its maximum. Explain why this amount of wheat either is or

is not the profit-maximizing quantity.

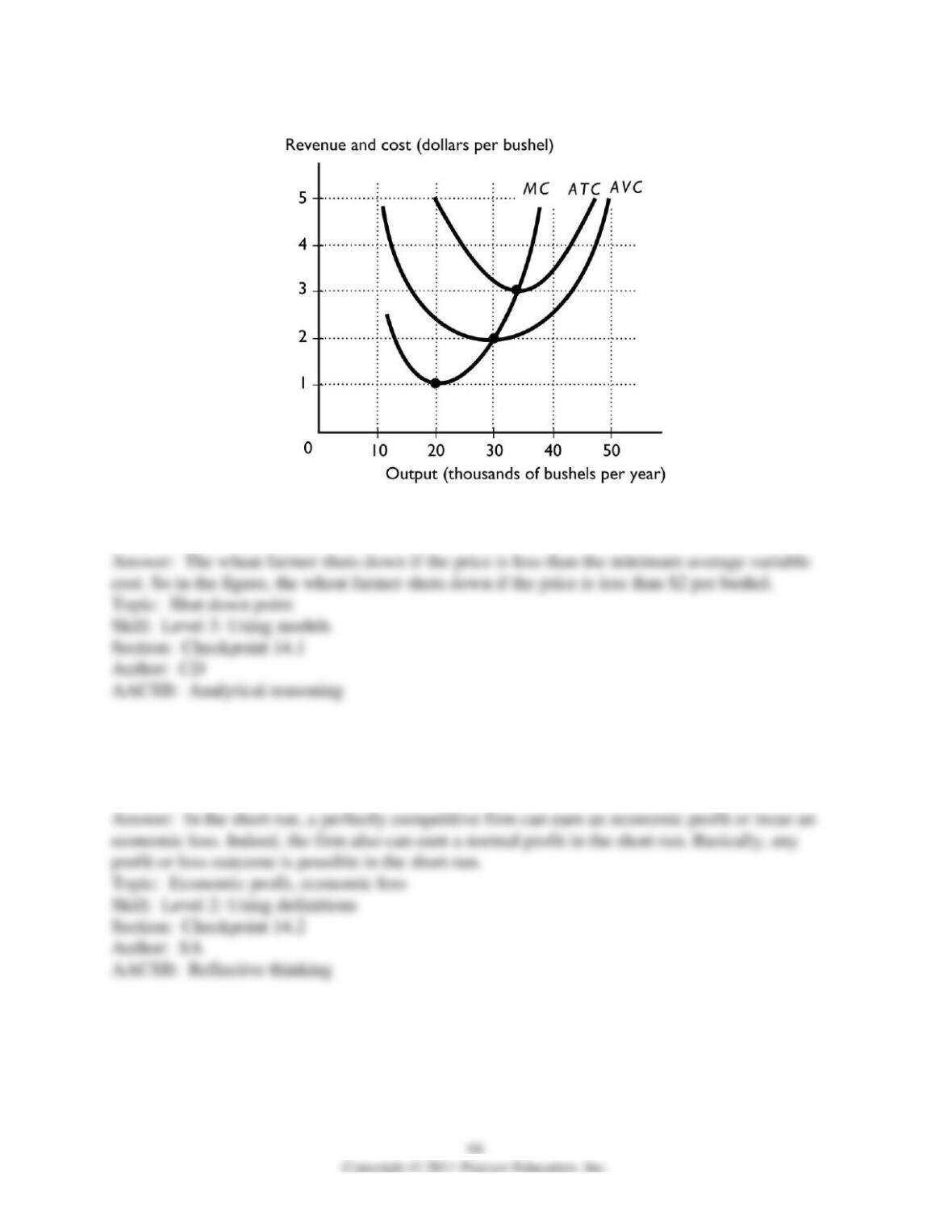

28) The above diagram shows the cost curves for a perfectly competitive wheat farmer. At what

price does the wheat farmer shut down?

14.7 Essay: Output, Price, and Profit in the Short Run

1) Can a perfectly competitive firm earn an economic profit in the short run? Can it incur an

economic loss?

2) If the market price is less than a perfectly competitive firm’s average total cost, what sort of

profit or loss is the firm earning?

3) What is the relationship between the price, P, and the average total cost, ATC, for a firm in

perfect competition that earns an economic profit? That earns a normal profit? That incurs an

economic loss?

4) John keeps beehives and sells 100 quarts of honey per month. The honey market is perfectly

competitive, and the price of a quart of honey is $10. John has an average variable cost of $5 and

an average fixed cost of $3. At 100 quarts per month, John’s marginal cost is $10.

a. Is John maximizing his profit? If not, what should John do?

b. Calculate John’s total revenue, total cost, and total economic profit or economic loss when he

produces 100 quarts of honey.

5) The above diagram shows the cost curves for a perfectly competitive wheat farmer. At what

price(s) does the wheat farmer earn an economic profit? Earn a normal profit? Incur an economic

loss? How many bushels of wheat does the farmer produce if the price is $3 per bushel? If the

price is $0.50 per bushel?

14.8 Essay: Output, Price, and Profit in the Long Run

1) “For a perfectly competitive market, an economic profit attracts new firms. But when these

firms enter the market, the price falls and the economic profit is eliminated.” Are the previous

statements correct or incorrect? What is the long-run profit or loss outcome for firms in a

perfectly competitive market?

2) In the long run, perfectly competitive firms cannot earn an economic profit. Why?

3) The U-pick berry market is perfectly competitive. Suppose that all U-pick blueberry farms

have the same cost curves and all are earning an economic profit. What happens as time passes?

What is the long-run equilibrium outcome?

4) When will new firms enter a perfectly competitive market? When does entry stop?

5) Describe how economic losses are eliminated in a perfectly competitive industry.

6) Pumpkin growing is a perfectly competitive industry. Suppose that pumpkin growers are all

suffering an economic loss. What happens as time passes? What is the long-run equilibrium

outcome?

7) Suppose a farmer raising beef is earning a normal profit. Then, because of a scare about mad

cow disease, the demand for beef decreases drastically. What happens to the profits of the beef

farmer in the short run and in the long run?

8) How does a decrease in the demand for wheat ultimately lead to normal profits for wheat

growers in the long run?

9) Entry by competitive firms decreases the market price, while exit by competitive firms

increases the market price. Explain why firms enter or exit an industry and why these price

changes occur.

10) In the long run, a perfectly competitive firm earns zero economic profit. What incentive does

the firm have to stay in business if it is making zero economic profit?

11) With regard to its profits and losses, how is the short run different from the long run for a

perfectly competitive firm?

12) During the middle of the 2000s, the price of gasoline soared and there was a movement to

switch to fuels made from a mixture of gasoline and ethanol. Ethanol can be made from corn.

The price of corn skyrocketed and then, after a couple of years, the price decreased. What might

have led to these price changes in the corn market?

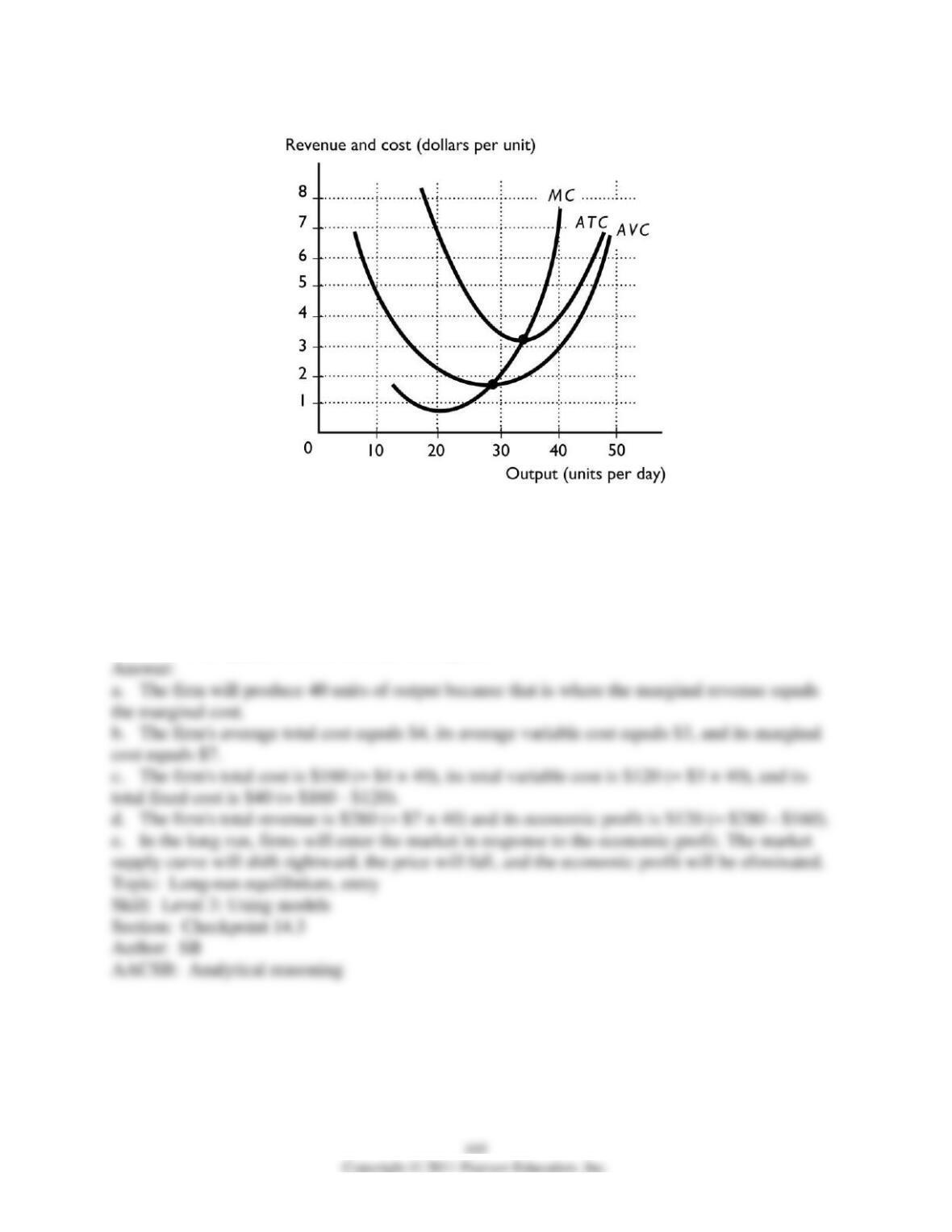

13) The above figure shows the cost curves of a profit-maximizing perfectly competitive firm. If

the price equals $7,

a. how much will the firm produce?

b. how much is the firm’s average total, average variable, and marginal costs?

c. how much is the firm’s total, total variable, and total fixed costs?

d. how much is the firm’s total revenue and economic profit?

e. what will happen in this market in the long run?

106

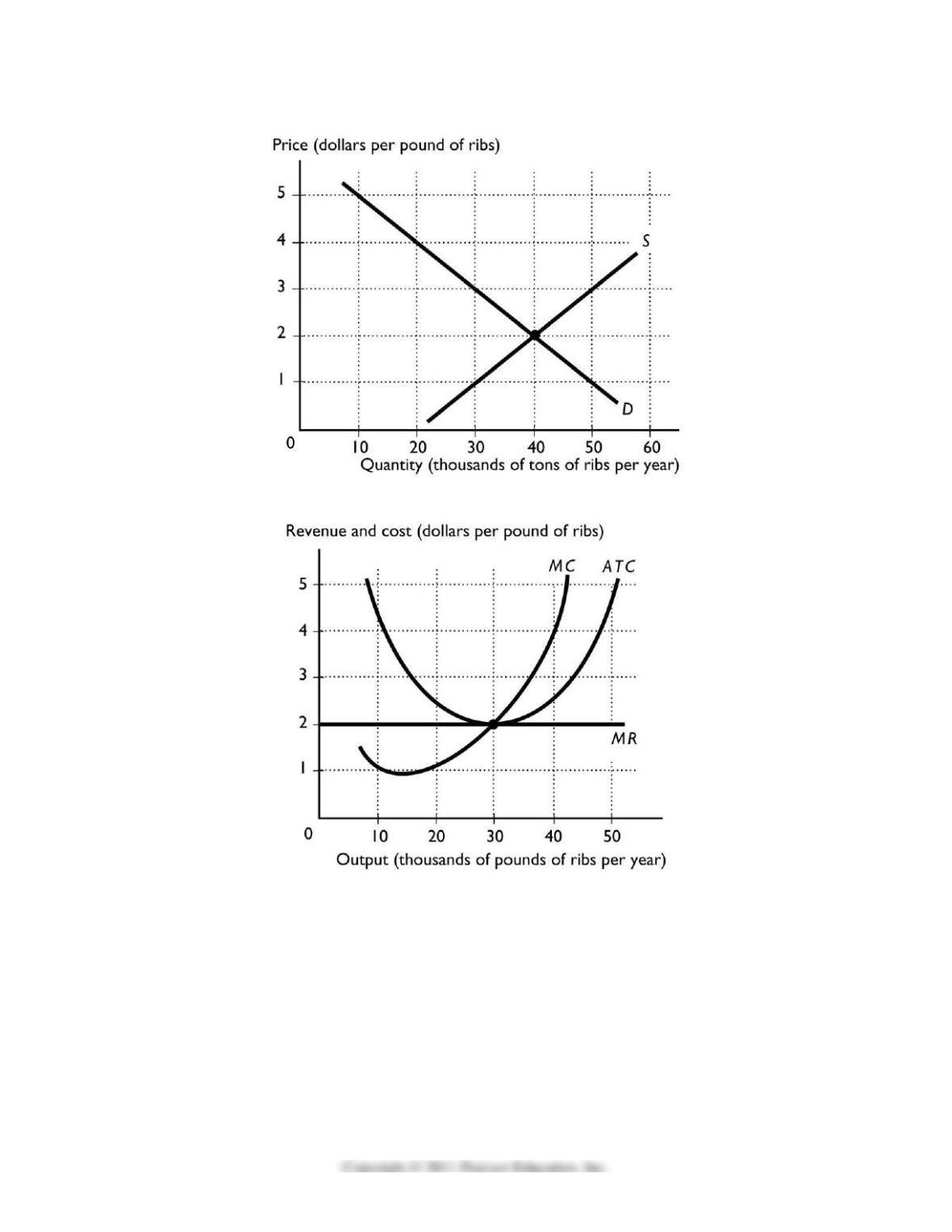

14) American restaurants receive their supply of baby back-ribs from American farms and from

farms in Denmark. In the figures above, the left diagram shows the perfectly competitive market

for baby back ribs in the United States. The right figure shows the situation at Premium Standard

Farm in Kansas, one of the many U.S. farms supplying these ribs.

Now assume that the United States imposes a ban on European meat in response to the foot-

and-mouth disease that has infected livestock in Europe. (Which the United States did a few

years ago.) In particular, suppose that the U.S. ban decreases the supply by 40 tons a year. Using

the figure on the left, show the impact of this ban on the baby back rib market. Using the figure

on the right, show the impact on Premium Standard Farm in Kansas.

15) Suppose the bobby pin industry is perfectly competitive. The price of a packet of bobby pins

is $2.00. Pins and Needles, Inc. is a firm in this industry and is producing 1,000 packets of bobby

pins per day at the point where the MC = MR. The average cost of production at this output level

is $1.50 per packet.

a. What is the marginal cost of the 1,000th packet?

b. Is this firm making an economic profit, a normal profit, or an economic loss? How much?

c. Is the firm in long-run equilibrium? Why or why not?