15) A perfectly competitive market is in equilibrium and then demand decreases. The decrease in

demand means the market price will ________ and eventually there will be ________.

A) rise; entry by new firms

B) fall; exit by existing firms

C) fall; entry by new firms

D) rise; exit by existing firms

E) fall; neither entry nor exit because the market is perfectly competitive

16) Catfish farming is a perfectly competitive industry. Catfish farmers suffered tremendous

economic losses in the late 1990s. As a result,

A) some new catfish farmers entered the market.

B) some catfish farmers exited the market.

C) no catfish farmers entered or exited this market.

D) the supply of catfish increased in 2000.

E) new demanders entered the market after some firms had exited.

17) Keith is a perfectly competitive carnation grower. The market price is $2 per dozen

carnations. Keith’s average total cost to grow carnations is $2.50 per dozen. In the long run,

Keith will

A) raise his price to more than $2.50 per dozen carnations.

B) raise his price to $2.50 per dozen carnations.

C) exit the industry if the price and his costs do not change.

D) incur an economic loss.

E) continue to earn an economic profit.

18) If concerns about mad-cow disease impose economic losses on the perfectly competitive

cattle ranchers, exit by the ranchers combined with no further changes in the demand for beef

will force the price of beef to

A) decrease.

B) not change.

C) increase.

D) fluctuate, with the trend being lower prices.

E) probably change, but more information about the market supply of beef is needed to answer

the question.

19) Suppose a perfectly competitive market is in a short-run equilibrium. If some firms exit the

market, the profit of the remaining firms ________; if some firms enter the market, the profit of

each existing firm ________.

A) decreases; is unchanged

B) increases; decreases

C) increases; is unchanged

D) is unchanged; is unchanged

E) decreases; increases

20) In the long run, perfectly competitive firms produce at the output level that has the minimum

A) marginal cost.

B) average total cost.

C) average variable cost.

D) average fixed cost.

E) total revenue.

21) In a perfectly competitive industry,

i. entry by new firms shifts the market supply curve rightward.

ii. exit by existing firms shifts the market supply curve leftward.

iii. at all times existing firms make only zero economic profit.

A) ii and iii.

B) ii only.

C) i and iii.

D) i and ii.

E) i, ii, and iii.

22) If it does not shut down, a perfectly competitive firm produces where marginal cost is equal

to the marginal revenue

A) only in the short run.

B) only in the long run.

C) always to maximize its profit.

D) only if it is not possible to produce where price equals average variable cost.

E) only if it is not possible to produce where price is greater than average total cost.

23) In the long run, a perfectly competitive firm earns

A) a positive economic profit.

B) zero economic profit.

C) negative economic profit, that is, an economic loss.

D) zero accounting profit.

E) either a positive economic profit or a normal profit.

24) In the long run, a perfectly competitive firm will

A) be able to earn an economic profit.

B) produce but incur an economic loss.

C) make zero economic profit.

D) not produce and will have an economic loss equal to its total fixed cost.

E) not produce but not have an economic loss.

25) In the long run, a perfectly competitive firm

A) can make either an economic profit or a normal profit.

B) incurs an economic loss.

C) makes zero economic profit.

D) can make an economic profit, zero economic profit, or incur an economic loss.

E) makes an economic profit.

26) The cranberry market is perfectly competitive. Reports that consuming cranberries can lead

to improved health result in a permanent increase in the demand for cranberries and an

immediate upward jump in the price of cranberries. As time passes, the price of cranberries

________ and the initial firms’ economic ________.

A) falls; profit will be eliminated

B) rises still higher; loss will be eliminated

C) rises still higher; profit will not change

D) falls; loss will be increased

E) falls; profit will not change

27) Suppose a perfectly competitive market is in long-run equilibrium with a price of $12. Then

there is a permanent increase in demand. As a result, in the short run the market price ________

and in the long run the number of firms ________ and the price is ________ the price was in the

short run.

A) rises; does not change; is equal to

B) rises; increases; higher than

C) rises; does not change; lower than

D) falls; decreases; is equal to

E) rises; increases; lower than

28) If perfectly competitive firms are maximizing their profit and are making an economic profit,

the market ________ in a short-run equilibrium and ________ in a long-run equilibrium.

A) is; is

B) is; is not

C) is not; is

D) is not; is not

E) is; might be

29) A market is initially in a long-run equilibrium and there is a permanent increase in demand.

After the new long-run equilibrium is reached, there

A) are more firms in the market.

B) are fewer firms in the market.

C) are the same number of firms in the market.

D) probably is a different number of firms in the market, but more information is needed to

determine if the number of firms rises, falls, or perhaps does not change.

E) is no change in the market.

30) A permanent decrease in demand definitely

A) shifts a firm’s average total cost curve downward.

B) creates diseconomies for individual firms.

C) lowers the market price.

D) decreases the number of firms in the industry.

E) shifts a firm’s average total cost curve upward.

31) The rutabaga market is perfectly competitive. Research is published claiming that eating

rutabagas leads to gaining weight and so the demand for rutabagas permanently decreases. The

permanent decrease in demand results in a

A) lower price, economic losses by rutabaga farmers, and entry into the market.

B) lower price, economic losses by rutabaga farmers, and exit from the market.

C) higher price, economic profits for rutabaga farmers, and entry into the market.

D) higher price, economic losses by rutabaga farmers, and exit from the market.

E) lower price, economic profits for rutabaga farmers, and entry into the market.

32) Technological change

A) usually requires an investment in a new plant.

B) is implemented in the short run.

C) almost always increases the costs of production.

D) almost always increases the variable costs of production.

E) cannot help a firm to earn an economic profit in either the short run or the long run.

33) When a firm adopts new technology, generally its

A) cost curves shift upward.

B) cost curves shift downward.

C) cost curves are unaffected.

D) supply curve shifts leftward.

E) production permanently decreases.

34) In a market undergoing technological change, firms that

A) adopt the new technology temporarily incur an economic loss.

B) adopt the new technology temporarily earn an economic profit.

C) do not adopt the new technology temporarily earn an economic profit.

D) do not adopt the new technology increase their market share.

E) do not adopt the new technology continue to earn a normal profit.

35) If the technology associated with producing fiber-optic cable continues to advance, over time

the cost of producing fiber-optic cable will

A) decrease, firms that use the new technology will earn an economic profit, and in the long run

new firms will enter the market.

B) decrease, firms that use the new technology will incur an economic loss, and in the long run

some firms will exit the industry.

C) increase, firms that use the new technology will earn an economic profit, and in the long run

new firms will enter the market.

D) increase, firms that use the new technology will incur an economic loss, and in the long run

some firms will exit the industry.

E) decrease, firms that do not use the new technology will earn an economic profit, and in the

long run new firms will enter the market.

36) Technology reduces the average cost of production, so in the long run

i. perfectly competitive firms produce at a lower average cost.

ii. the market price of the good falls.

iii. firms with older plants either exit the market or adopt the new technology.

A) i only.

B) i and ii.

C) iii only.

D) i and iii.

E) i, ii, and iii.

37) In the long run, new firms enter a perfectly competitive market when

A) normal profit is greater than zero.

B) economic profit is equal to zero.

C) normal profit is equal to zero.

D) economic profit is greater than zero.

E) the existing firms are weak because they are incurring economic losses.

38) If perfectly firms are earning an economic profit, the economic profit

A) attracts entry by more firms, which lowers the price.

B) can be earned both in the short run and the long run.

C) is less than the normal profit.

D) leads to a decrease in market demand.

E) generally leads to firms exiting as they seek higher profit in other markets.

39) If perfectly firms are earning an economic profit, then

A) the market is in its long-run equilibrium.

B) new firms enter the market and the equilibrium profit of the firms already in the market

decreases.

C) new firms enter the market and the equilibrium profit of the firms already in the market

increases.

D) firms exit the market and the economic profit of the surviving firms in the market decreases.

E) firms exit the market and the economic profit of the surviving firms in the market increases.

40) As a result of firms leaving the perfectly competitive frozen yogurt market in the early

2000s, the market

A) supply curve shifted leftward.

B) supply curve did not change.

C) demand curve shifted rightward.

D) supply curve shifted rightward.

E) demand curve shifted leftward.

41) Firms exit a competitive market when they incur an economic loss. In the long run, this exit

means that the economic losses of the surviving firms

A) increase.

B) decrease until they equal zero.

C) decrease until economic profits are earned.

D) do not change.

E) might change but more information is needed about what happens to the price of the good as

the firms exit.

42) If firms in a perfectly competitive market have economic losses, then as time passes firms

________ and the market ________.

A) enter; demand curve shifts leftward

B) enter; supply curve shifts rightward

C) exit; demand curve shifts leftward

D) exit; supply curve shifts rightward

E) exit; supply curve shifts leftward

43) In the long run, a firm in a perfectly competitive market will

A) earn zero economic profit, so that its owners earn a normal profit.

B) earn zero normal profit but its owners will make an economic profit.

C) remove all competitors and become a monopolistically competitive firm.

D) incur an economic normal loss but not earn a positive economic profit.

E) remove all competitors and become a monopoly.

44) Technological change brings a ________ to firms that adopt the new technology.

A) permanent economic profit

B) temporary economic profit

C) permanent economic loss

D) temporary economic loss

E) temporary normal profit

14.4 Chapter Figures

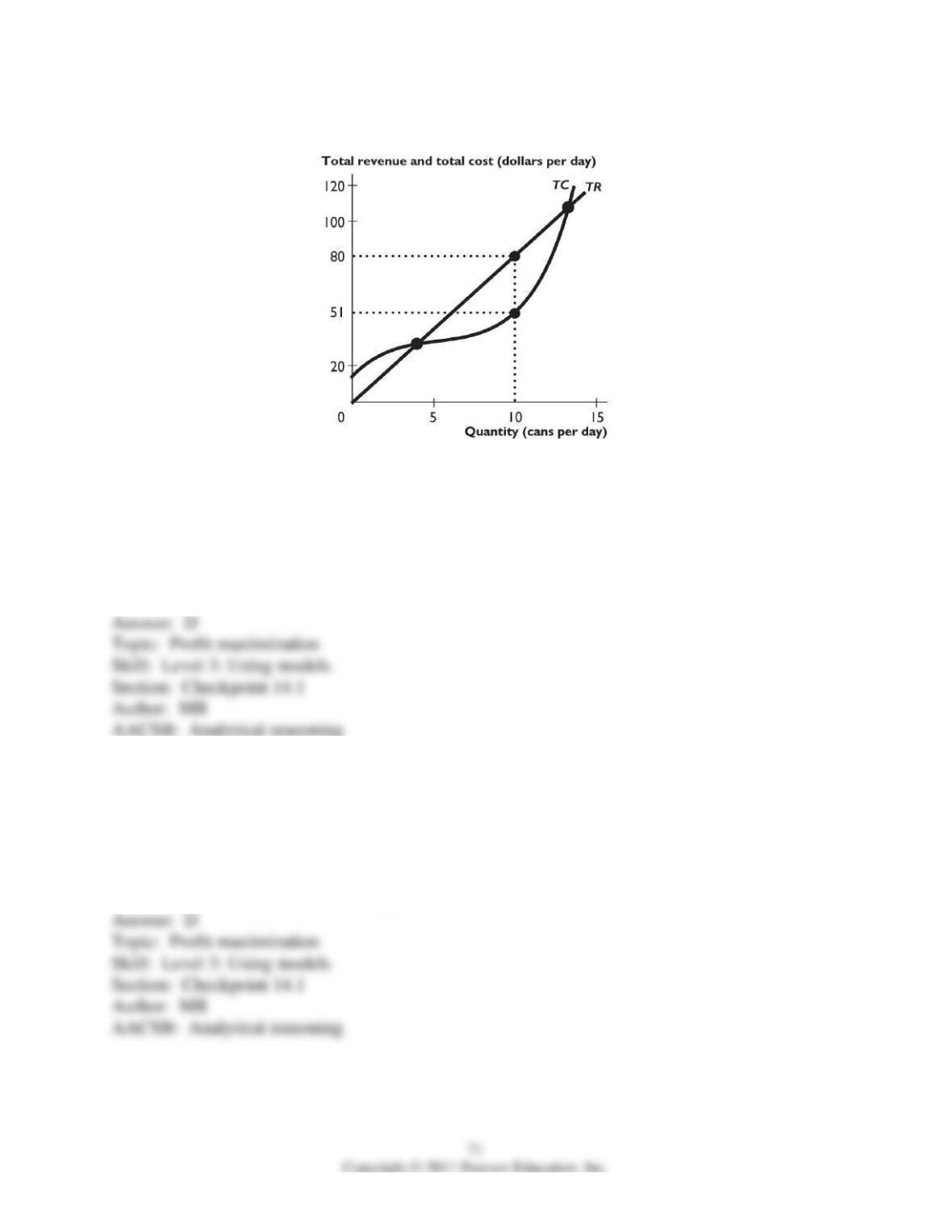

The figure above shows a firm’s total revenue and total cost curves.

1) When the firm maximizes its profit, it produces ________ cans per day.

A) 0

B) more than 0 and less than 5

C) 5 or more but less than 10

D) 10

E) more than 10

2) To maximize its profit, the firm in the figure above produces ________ cans per day and

________.

A) 0; incurs an economic loss of less than $20

B) between 3 to 5 cans; earns a normal profit

C) 10; earns an economic profit of $2.90

D) 10; earns an economic profit of $29

E) more than 10; earns an economic profit

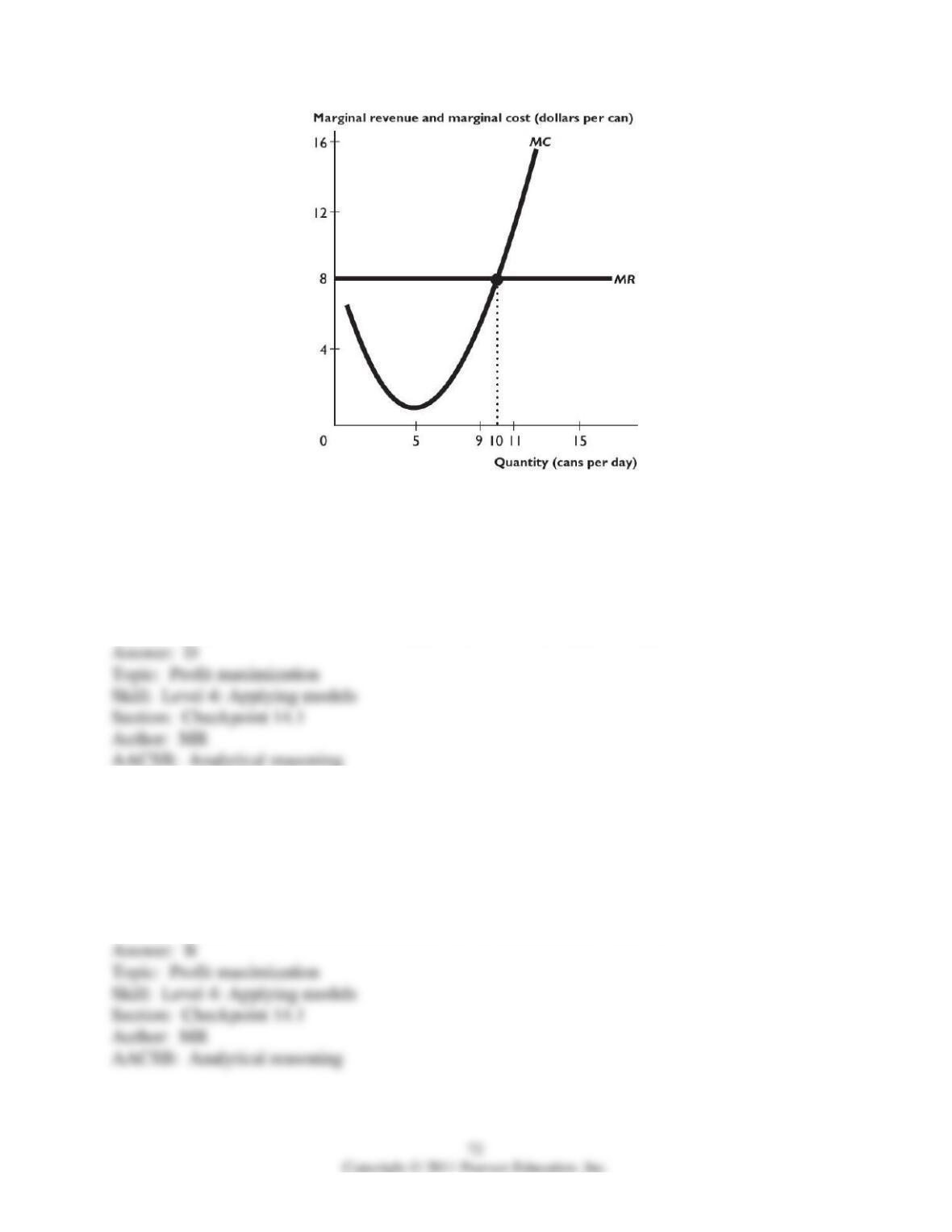

The figure above shows a firm’s marginal revenue and marginal cost curves.

3) The price of a can is $8; if the price increased to $12, then the firm would

A) produce zero cans.

B) decrease the amount of cans produces it but not to zero.

C) not change the amount of cans it produces.

D) increase the amount of cans it produces.

E) More information is needed to determine what action the firm will take.

4) Suppose the firm’s marginal cost of producing a can increases by $1 per can. Then the firm

would

A) produce zero cans.

B) decrease the amount of cans it produces but not to zero cans.

C) not change the amount of cans it produces.

D) increase the amount of cans it produces.

E) More information is needed to determine what action the firm will take.

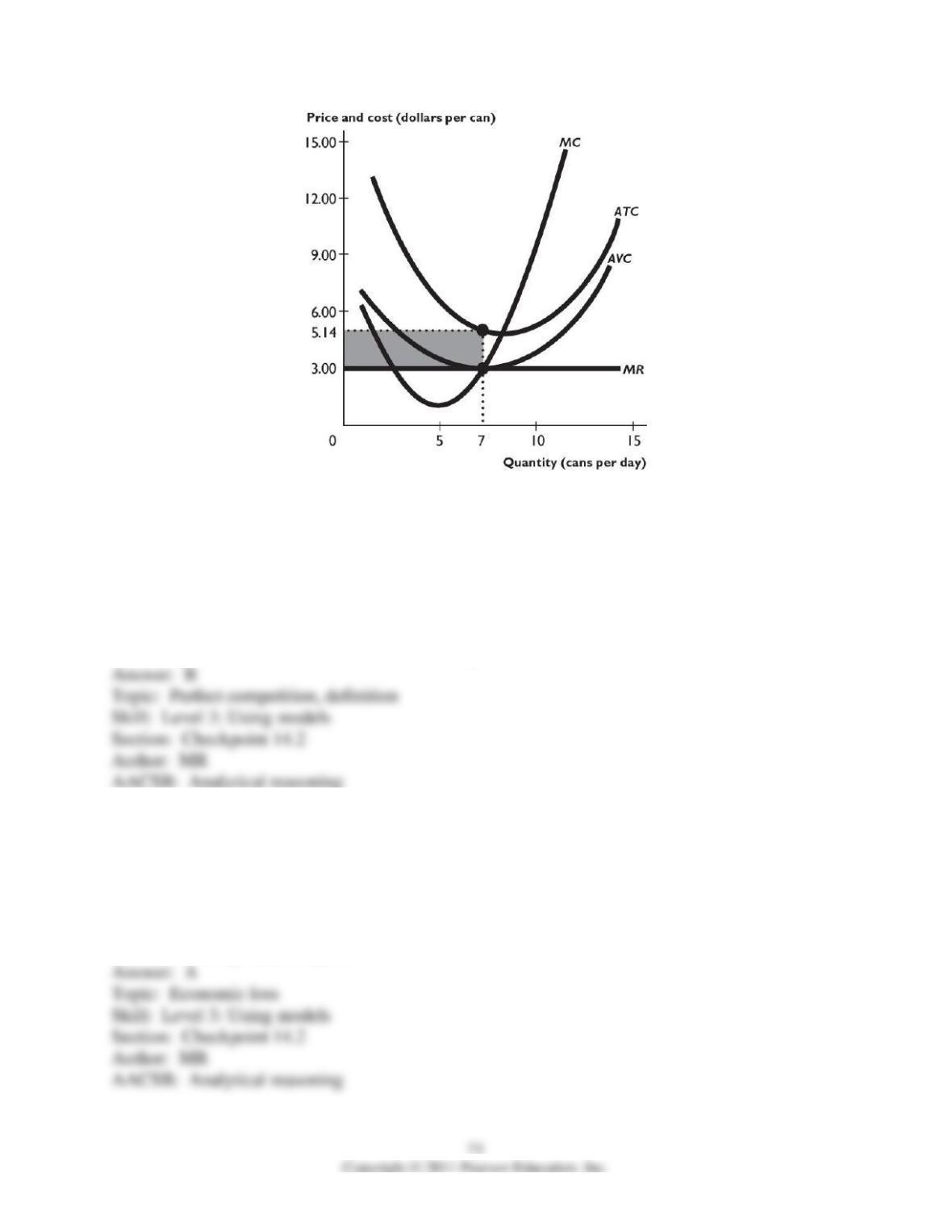

The figure above shows the cost curves and marginal revenue curve for a perfectly competitive

firm.

5) Based on the figure above, what is the price of a can?

A) $0.

B) $3.00 per can

C) $5.14 per can

D) None of the above prices is correct.

E) More information is needed to determine the price of a can.

6) Based on the figure above, if the firm produces 7 cans per day, the firm ________ maximizing

its profit and is ________.

A) is; incurring an economic loss

B) is; earning a normal profit

C) is; earning an economic profit

D) is not; incurring an economic loss

E) is not; earning a normal profit

7) Suppose the price of a can was $5.14. In this case, to maximize its profit the firm illustrated in

the figure above would

A) increase its production and would earn an economic profit.

B) not change its production and would earn a normal profit.

C) not change its production and would earn an economic profit.

D) increase its production and would incur an economic loss.

E) not change its production and would incur an economic loss.

8) The firm in the figure above is ________ that is equal to ________.

A) earning an economic profit; $5.14 × 7

B) earning an economic profit; $3.00 × 7

C) incurring an economic loss; $5.14 × 7

D) incurring an economic loss; ($5.14 – $3.00) × 7

E) earning an economic profit; ($5.14 – $3.00) × 7

The figure above shows some of a firm’s cost curves and its marginal revenue curve.

9) Based on the figure above, what is the price of a can?

A) $0

B) $8.00 per can

C) $5.10 per can

D) None of the above prices is correct.

E) More information is needed to determine the price of a can.

10) Based on the figure above, if the firm produces 10 cans per day, the firm ________

maximizing its profit and is ________.

A) is; incurring an economic loss

B) is; earning a normal profit

C) is; earning an economic profit

D) is not; incurring an economic loss

E) is not; earning a normal profit

11) Suppose the price of a can was $5.10. In this case, to maximize its profit the firm illustrated

in the figure above would

A) decrease its production and would earn an economic profit.

B) not change its production and would earn a normal profit.

C) not change its production and would earn an economic profit.

D) decrease its production and would incur an economic loss.

E) not change its production and would incur an economic loss.

12) The firm in the figure above has a total cost equal to ________ .

A) $5.10 × 10

B) $8.00 × 10

C) ($5.10 – $8.00) × 10

D) ($8.00 – $5.10) × 10

E) None of the above answers are correct because more information is needed.

13) The firm in the figure above has a total revenue equal to ________.

A) $5.10 × 10

B) $8.00 × 10

C) ($5.10 – $8.00) × 10

D) ($8.00 – $5.10) × 10

E) None of the above answers are correct because more information is needed.

14) The firm in the figure above is ________ that is equal to ________.

A) earning an economic profit; $8.00 × 10

B) earning an economic profit; $5.10 × 10

C) incurring an economic loss; $5.10 × 10

D) incurring an economic loss; ($8.00 – $5.10) × 10

E) earning an economic profit; ($8.00 – $5.10) × 10

The above figure shows some a firm’s cost curves and its marginal revenue curve.

15) Based on the figure above, what is the price of a can?

A) $0

B) $3.00 per can

C) $5.15 per can

D) None of the above prices is correct.

E) More information is needed to determine the price of a can.

16) Based on the figure above, if the firm produces 7 cans per day, the firm ________

maximizing its profit and is ________.

A) is; incurring an economic loss

B) is; earning a normal profit

C) is; earning an economic profit

D) is not; incurring an economic loss

E) is not; earning a normal profit

17) Suppose the price of a can was $5.14. In this case, to maximize its profit the firm illustrated

in the figure above would

A) increase its production and would earn an economic profit.

B) not change its production and would earn a normal profit.

C) not change its production and would earn an economic profit.

D) increase its production and would incur an economic loss.

E) not change its production and would incur an economic loss.

18) The price for the shutdown point ________.

A) $5.14

B) between $3.01 and $5.13

C) $3.00

D) between $0 and $2.99

E) greater than $5.15

19) The firm in the figure above has a total cost equal to ________.

A) $5.14 × 7

B) $3.00 × 7

C) ($5.14 – $3.00) × 7

D) ($3.00 – $5.14) × 7

E) None of the above answers are correct because more information is needed.

20) The firm in the figure above has a total revenue equal to ________.

A) $5.14 × 7

B) $3.00 × 7

C) ($5.14 – $3.00) × 7

D) ($3.00 – $5.14) × 7

E) None of the above answers are correct because more information is needed.

21) The firm in the figure above is ________ that is equal to ________.

A) earning an economic profit; $5.14 × 7

B) earning an economic profit; $3.00 × 7

C) incurring an economic loss; $5.14 × 7

D) incurring an economic loss; ($5.14 – $3.00) × 7

E) earning an economic profit; ($5.14 – $3.00) × 7

14.5 Integrative Questions

1) Consider a short-run equilibrium in a perfectly competitive market. Suppose that the firms’

average total cost and marginal cost schedules differ. In the short run,

A) all firms in the market must be able to earn an economic profit.

B) all firms produce equal amounts of output.

C) some firms might incur an economic loss, but still produce output.

D) some firms might earn an economic profit and, as a result, shut down.

E) all firms in the market must be able to earn either an economic profit or a n normal profit.