5) In the short run, a perfectly competitive firm can experience which of the following?

i. an economic profit

ii. an economic loss but it continues to stay open

iii. an economic loss equal to its total fixed cost when it shuts down

A) only i

B) i and ii

C) i and iii

D) ii and iii

E) i, ii, and iii

6) If a perfectly competitive seller is maximizing profit and is earning zero economic profit,

which of the following will this seller do?

A) go to work in the next-best earning opportunity

B) shut down, with a loss equal to total fixed cost

C) continue at the current output, earning a normal profit

D) increase production in order to earn an economic profit

E) remain open but decrease production in order to earn an economic profit

7) If a perfectly competitive firm finds that the price exceeds its ATC, then the firm

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is earning an economic profit.

D) is incurring an economic loss.

E) is earning zero economic profit.

8) For a perfectly competitive sugar producer in Haiti, a short-run economic profit will occur if

the price of each ton of sugar sold is

A) greater than the average total cost of producing sugar.

B) equal to the average total cost of producing sugar.

C) less than the average total cost of producing sugar.

D) rising as more sugar is sold.

E) greater than the marginal revenue of each ton of sugar.

9) If Henry, a perfectly competitive lime grower in Southern California, can sell his limes at a

price greater than his average total cost, Henry will

A) incur an economic loss.

B) suffer an accounting loss.

C) have an incentive to shut down.

D) earn an economic profit.

E) make zero economic profit.

10) If a perfectly competitive firm’s average total cost is less than the price, then the firm

A) incurs an economic loss.

B) earns an economic profit.

C) earns a normal profit.

D) earns either a normal profit or an economic profit depending on whether the marginal revenue

is equal to or greater than the price.

E) None of the above answers is correct because the relationship between the price and average

total cost has nothing to do with the firm’s profit.

11) If the market price is $50 per unit for a good produced in a perfectly competitive market and

the firm’s average total cost is $52, then the firm

A) has an economic loss of $2 per unit.

B) has an economic profit of $2 per unit.

C) has a normal profit.

D) has a total economic loss of $52.

E) More information is needed to determine the firm’s economic profit or loss per unit.

12) Peter’s Pencils is a perfectly competitive company producing pencils. Suppose Peter is

producing 1,000 pencils an hour. If the total cost of 1,000 pencils is $500, the market price per

pencil is $2, and the marginal cost is $2, then Peter

A) has an economic profit because marginal revenue is equal to marginal cost at this output

level.

B) should decrease his output to increase his profit.

C) is maximizing his profit and is earning an economic profit.

D) should increase his output to increase his profit.

E) is not maximizing his profit but is earning a normal profit anyway.

13) Suppose that marginal revenue for a perfectly competitive firm is $20 . When the firm

produces 10 units, its marginal cost is $20, its average total cost is $22, and its average variable

cost is $17. Then to maximize its profit in the short run, the firm

A) should stay open and incur an economic loss of $20.

B) must increase its output to increase its profit.

C) must decrease its output to increase its profit.

D) should shut down.

E) should not change its production because it is already maximizing its profit and is earning a

normal profit.

14) A perfectly competitive firm is producing 50 units of output, which it sells at the market

price of $23 per unit. The firm’s average total cost is $20. What is the firm’s total revenue?

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

15) A perfectly competitive firm is producing 50 units of output and selling at the market price

of $23. The firm’s average total cost is $20. What is the firm’s total cost?

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

16) A perfectly competitive firm is producing 50 units of output and selling at the market price

of $23. The firm’s average total cost is $20. What is the firm’s economic profit?

A) $23

B) $150

C) $1,000

D) $1,150

E) $50

17) For a perfectly competitive syrup producer whose average total cost curve does not change,

an economic profit could turn into an economic loss if the

A) market demand for syrup decreases.

B) marginal cost curve shifts downward.

C) market demand for syrup does not change.

D) market demand for syrup increases.

E) price of syrup rises.

18) For a perfectly competitive rancher in Wyoming, if the price does not change, an economic

profit could turn into an economic loss if the

A) average total cost curve shifts downward.

B) average total cost curve does not change.

C) average total cost curve shifts upward.

D) marginal cost curve shifts downward.

E) average fixed cost decreases.

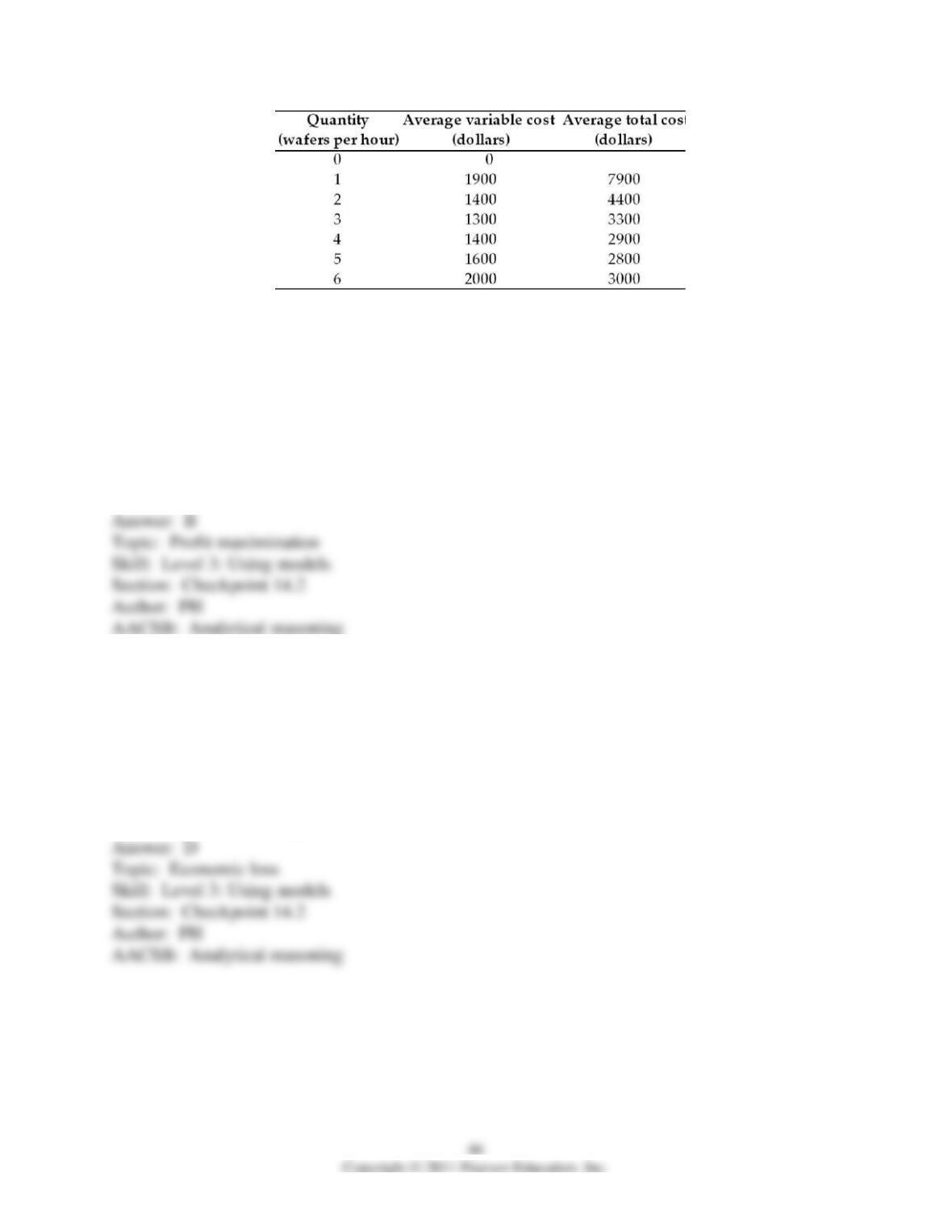

19) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. If the market price of a wafer is $2,400 dollars, how many wafers will

the firm produce?

A) 0

B) 4 or 5

C) 3 or 4

D) 1 or 2

E) 6

20) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. If the market price of a wafer is $2,400 dollars, the firm is

A) earning a normal profit.

B) earning an economic profit of $12,000 an hour.

C) incurring an economic loss of $2,800 an hour.

D) incurring an economic loss of $2,000 an hour.

E) earning an economic profit of $2,400 an hour.

21) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. This firm will produce as long as the market price of a wafer is above

A) $1,300.

B) $1,400.

C) $7,900.

D) $2,800.

E) $9,800.

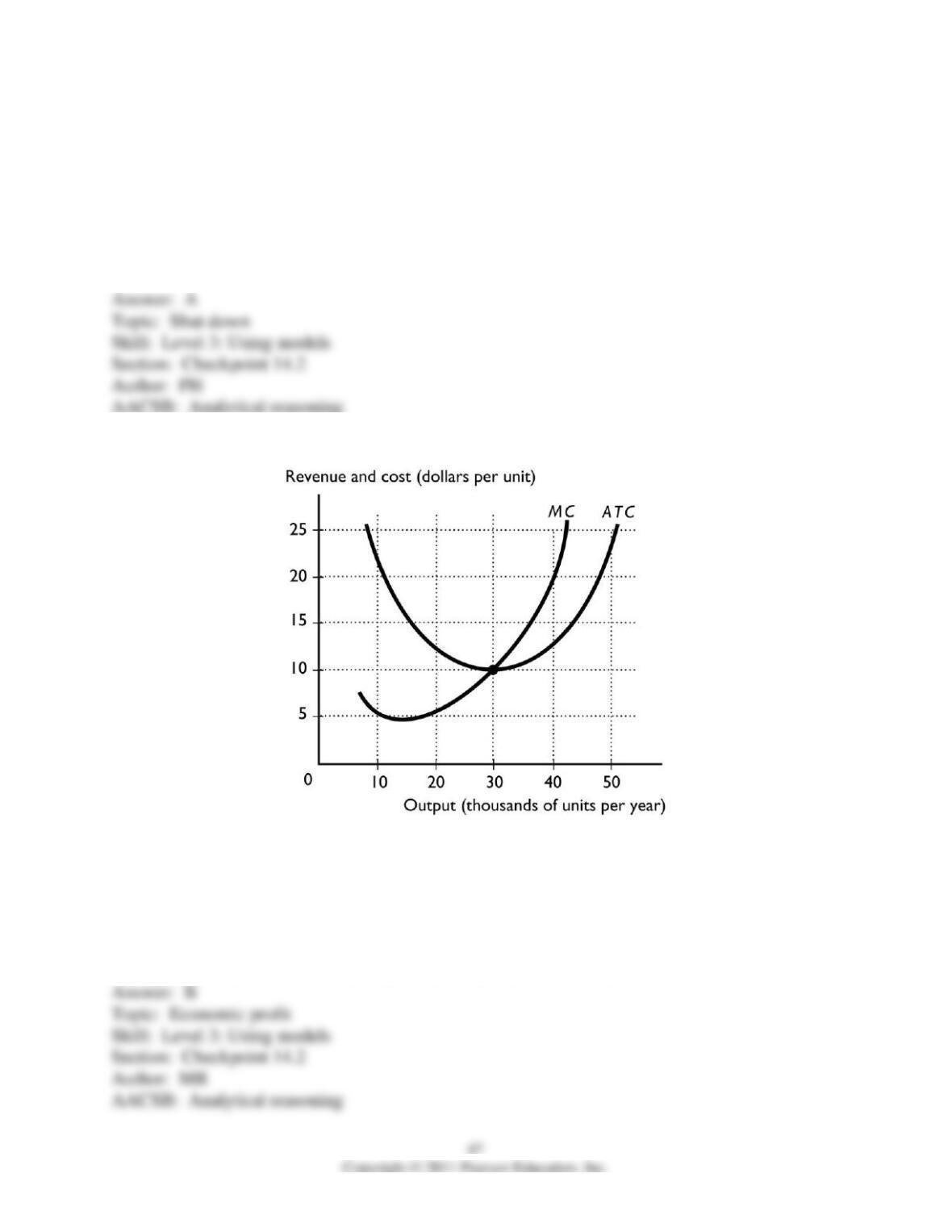

22) The above figure shows a perfectly competitive firm. If the market price is $15, the firm

A) is incurring an economic loss.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) might shut down but more information is needed about the AVC.

23) The above figure shows a perfectly competitive firm. If the market price is $10, the firm

A) is incurring an economic loss.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) might shut down but more information is needed about the AVC.

24) The above figure shows a perfectly competitive firm. If the market price is $5, the firm

A) might shut down but more information is needed about the AVC.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) will not shut down.

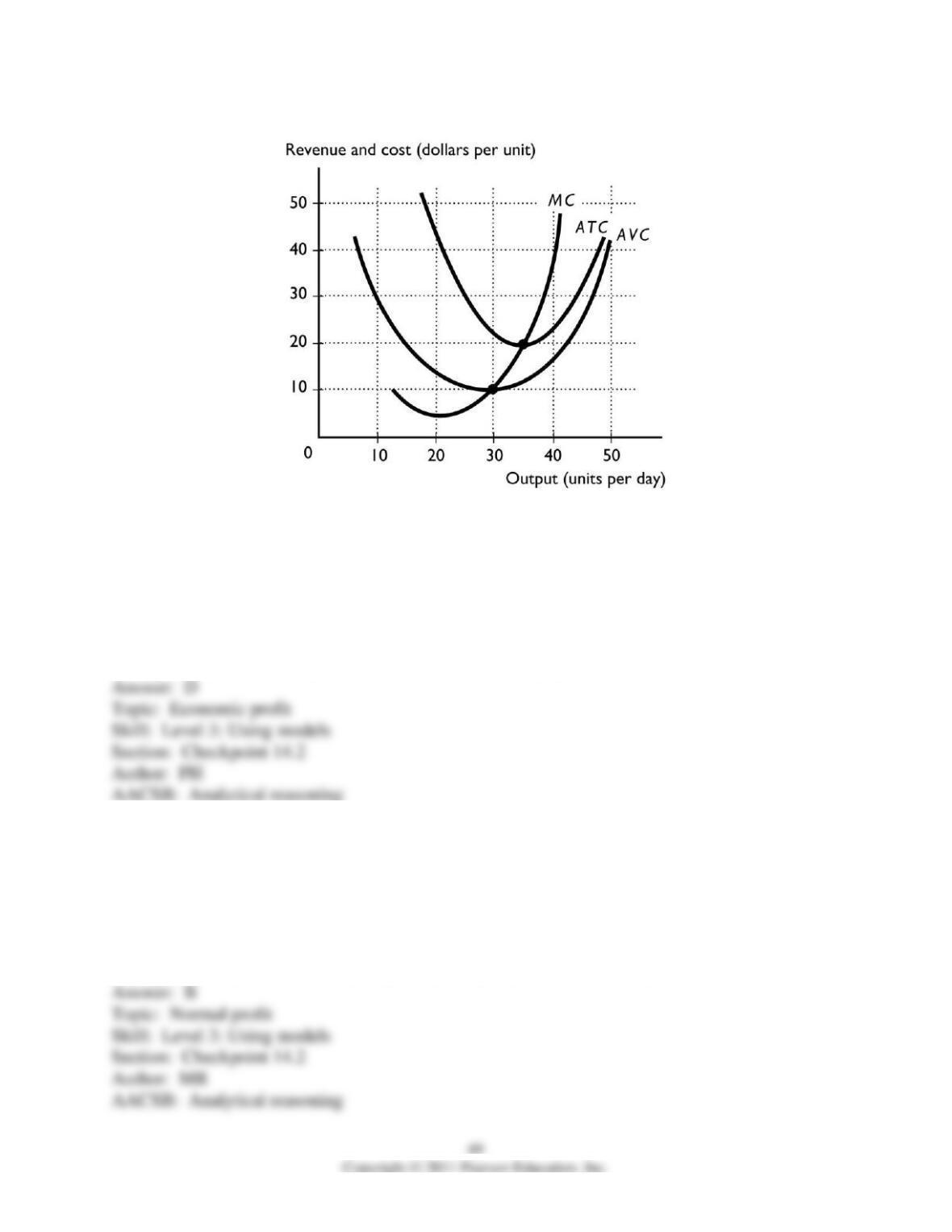

25) The above figure shows a perfectly competitive firm. If the market price is more than $20 per

unit, the firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

26) The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

27) The above figure shows a perfectly competitive firm. If the market price is $15 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

28) The above figure shows a perfectly competitive firm. If the market price is $5 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

29) The figure above shows a perfectly competitive firm. If the market price is $40 per unit, then

the firm produces ________ units and has an economic profit that is ________.

A) more than 45; more than $400

B) 40; more than $400

C) 40; less than $400

D) 30; equal to zero because the firm earns a normal profit

E) 30; more than $250

30) The figure above shows a perfectly competitive firm. If the market price is $20 per unit, then

the firm produces ________ units and has an economic profit that is ________.

A) more than 30; more than $100

B) 30; more than $100

C) 20; less than $400

D) 0; zero because the firm earns a normal profit

E) 30; zero because the firm earns a normal profit

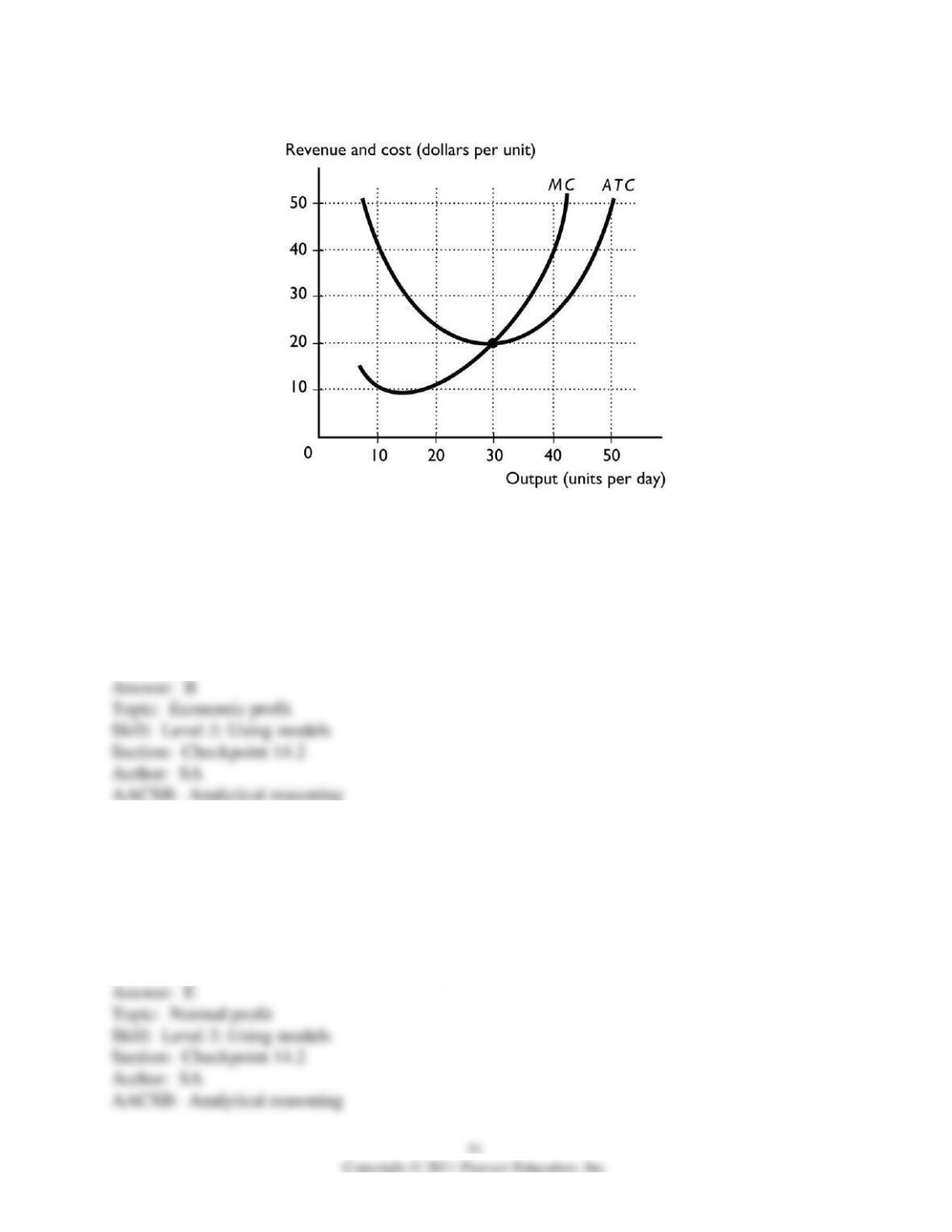

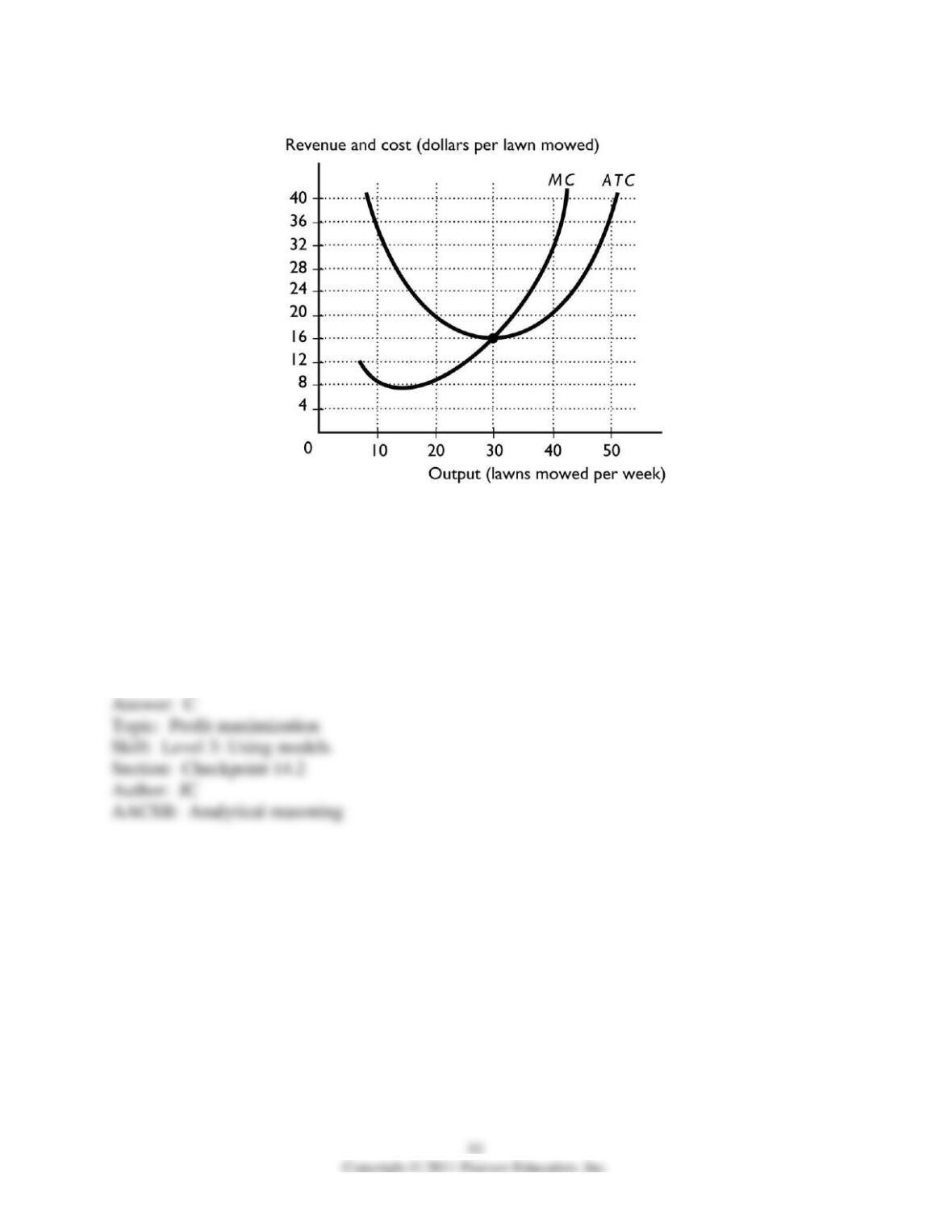

31) Bill owns a lawn-care company in Windermere, Florida, whose cost curves are illustrated in

the above figure. The market equilibrium price in this perfectly competitive market equals $32

per lawn mowed. At this price, how many lawns will Bill mow per week?

A) more than 10 and less than 30

B) 30

C) 40

D) 50

E) 0

32) Bill owns a lawn-care company in Windermere, Florida, whose cost curves are illustrated in

the above figure. The market equilibrium price in this perfectly competitive market equals $32

per lawn mowed. Bill’s average total cost curve is ATC, so his total cost of production equals

A) $0 because Bill shuts down.

B) more than $0 and less than $1,200 per week.

C) more than $1,200 and less than $1,400 per week.

D) more than $1,400 per week and less than $1,800 per week.

E) more than $1,800 per week.

33) Bill owns a lawn-care company in Windermere, Florida, Florida, whose cost curves are

illustrated in the above figure. The market equilibrium price in this perfectly competitive market

equals $32 per lawn mowed. If Bill’s average total cost curve is ATC, his total economic

________ equals ________.

A) loss; $800 per week

B) profit; $1,280 per week

C) profit; $480 per week

D) loss; $1,280 per week

E) profit; $32 per week

34) If the market supply curve and market demand curve for a good intersect at 600,000 units

and there are 10,000 identical firms in the market, then each firm is producing

A) 600,000 units.

B) 60,000,000,000 units.

C) 60,000 units.

D) 60 units.

E) 10,000 units.

35) In the short run, a perfectly competitive firm

A) must make an economic profit.

B) must incur an economic loss.

C) must make zero economic profit.

D) might make an economic profit, an economic loss, or a normal profit.

E) None of the above answers is correct.

36) A perfectly competitive firm definitely earns an economic profit in the short run if price is

A) equal to marginal cost.

B) equal to average total cost.

C) greater than average total cost.

D) greater than marginal cost.

E) greater than average variable cost.

37) If a perfectly competitive firm is maximizing its profit and is earning an economic profit,

which of the following is correct?

i. price equals marginal revenue

ii. marginal revenue equals marginal cost

iii. price is greater than average total cost

A) i only

B) i and ii only

C) ii and iii only

D) i and iii only

E) i, ii, and iii

38) The market for watermelons in Alabama is perfectly competitive. A watermelon producer

earning zero economic profit could earn an economic profit if the

A) average total cost of selling watermelons does not change.

B) average total cost of selling watermelons rises.

C) average total cost of selling watermelons falls.

D) marginal cost of selling watermelons does not change.

E) marginal cost of selling watermelons rises.

39) Juan’s Software Service Company is in a perfectly competitive market. Juan has total fixed

cost of $25,000, average variable cost for 1,000 service calls is $45, and marginal revenue is $75.

Juan’s makes 1,000 service calls a month. What is his economic profit?

A) $5,000

B) $25,000

C) $45,000

D) $75,000

E) $50,000

40) If a perfectly competitive firm finds that price is less than its ATC, then the firm

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is earning an economic profit.

D) is incurring an economic loss.

E) is earning zero economic profit.

41) A perfectly competitive video-rental firm in Phoenix incurs an economic loss if the average

total cost of each video rental is

A) greater than the marginal revenue of each rental.

B) less than the marginal revenue of each rental.

C) equal to the marginal revenue of each rental.

D) equal to the price of each rental.

E) greater than the average variable cost of each video.

14.3 Output, Price, and Profit in the Long Run

1) When new firms enter the perfectly competitive Miami bagel market, the market

A) supply curve shifts leftward.

B) supply curve does not change.

C) demand curve shifts rightward.

D) supply curve shifts rightward.

E) demand curve shifts leftward.

2) If new firms enter a perfectly competitive industry, the market supply

A) does not change.

B) becomes more price elastic.

C) becomes more price inelastic.

D) increases.

E) decreases because each firm produces less than before the entry.

3) Alice, Bud, and Celia can produce rubber bands in a perfectly competitive market. If they

enter the market, the minimum average total cost for a bundle of rubber bands, for the three of

them is $2, $3, and $4, respectively. If the market price is $2.10 per bundle, then

A) all three of them will enter the market.

B) only Alice will enter the market.

C) Alice and Bud will enter the market.

D) Bud and Celia will enter the market.

E) Alice and Celia will enter the market.

4) Suppose a perfectly competitive market is in long-run equilibrium and then there is a

permanent increase in the demand for that product. The new long-run equilibrium will have

A) fewer firms in the market.

B) more firms in the market.

C) the same number of firms in the market.

D) probably a different number of firms, but it is not possible to determine if there will be more

or fewer firms.

E) a permanent decrease in supply.

5) When firms in a perfectly competitive market are earning an economic profit, in the long run

A) no new firms will enter the market.

B) new firms will enter the market.

C) firms will exit the market.

D) the long-run average cost curve shifts downward.

E) the initial firms continue to earn an economic profit.

6) If perfectly competitive firms are making an economic profit, then

A) the market must be in long-run equilibrium but cannot be in a short-run equilibrium.

B) some firms will exit the market.

C) new firms will enter the market.

D) the market might be in a long-run equilibrium but not a short-run equilibrium.

E) the market cannot be in either a short-run or a long-run equilibrium.

7) The corn market is perfectly competitive, with thousands of corn farmers. In the 2000s, the

price of corn soared so that new farmers entered the corn market. Initially, entry ________ the

economic profit of the initial corn farmers and in the long run the initial corn farmers ________.

A) increased; earned an even greater economic profit than initially

B) decreased; earned zero economic profit

C) increased; earned zero economic profit

D) decreased; incurred an economic loss

E) increased; earned an economic profit

8) If firms in a perfectly competitive industry are earning an economic profit, then in the

________ firms will ________ the industry.

A) short run; enter

B) long run; enter

C) short run; exit

D) long run; exit

E) More information about the firms’ costs and the price of the product is needed to determine if

firms enter or exit the industry.

9) When new firms enter a perfectly competitive market, the market supply curve shifts

________ and the price ________.

A) rightward; falls

B) rightward; rises

C) leftward; falls

D) leftward; rises

E) rightward; does not change

10) When firms in a perfectly competitive market incur economic losses, exit by some firms

means the market supply will

A) increase.

B) decrease.

C) not change.

D) become vertical.

E) become the same as the individual producers’ supplies.

11) To eliminate losses in a perfectly competitive market, firms exit the industry. This exit

results in

A) an increase in market supply.

B) a decrease in market supply.

C) an increase in market demand.

D) a decrease in market demand.

E) a decrease in both the market supply and the market demand.

12) Suppose a perfectly competitive market is in short-run equilibrium. Firms that are incurring a

________ economic loss ________.

A) persistent; increase their output to increase their profit

B) temporary; exit the industry

C) temporary; decrease their production but definitely stay open

D) persistent; exit the industry and shift the market supply curve leftward

E) persistent; exit the industry and shift the market supply curve rightward

13) In the long run, existing firms exit a perfectly competitive market

A) only if economic profits are zero.

B) if they earn a positive economic profit.

C) if normal profits are greater than zero.

D) only if they incur an economic loss.

E) if they either earn only a normal profit or if they incur an economic loss.

14) In the long run, perfectly competitive firms will exit the market if the price is

A) higher than average variable cost.

B) equal to average total cost.

C) less than average total cost.

D) equal to average fixed cost.

E) equal to marginal revenue.