58) As a perfectly competitive firm produces more and more of a good, its economic profit

A) constantly increases.

B) constantly decreases.

C) first decreases, then increases.

D) first increases, then decreases.

E) does not change.

59) As a perfectly competitive firm’s output increases, its total revenue ________ and its total

cost ________.

A) increases; increases

B) increases; decreases

C) decreases; increases

D) decreases; decreases

E) does not change; increases

60) In a perfectly competitive industry, when a firm is producing so that its total revenue equals

its total cost, the firm is

A) earning an economic profit.

B) incurring an economic loss.

C) earning zero economic profit, that is, earning a normal profit.

D) definitely not maximizing its profit.

E) None of the above answers is correct because the relationship between total revenue and total

cost has nothing to do with the firm’s profit or loss.

61) For a syrup producer in central Vermont, profit is maximized at the level of output for which

total

A) revenue exceeds total cost by the largest amount.

B) revenue exceeds total cost by the smallest amount.

C) revenue is maximized.

D) cost is minimized.

E) revenue equals total cost.

62) A firm maximizes its profit by producing the amount of output such that

A) marginal revenue equals marginal cost.

B) marginal revenue exceeds marginal cost by some amount.

C) marginal revenue is maximized.

D) marginal cost is minimized.

E) marginal revenue exceeds marginal cost by the maximum amount possible.

63) For a perfectly competitive firm, profit maximization occurs when output is such that

A) total revenue (TR) is maximized.

B) total cost (TC) is minimized.

C) marginal revenue (MR) = marginal cost (MC).

D) average total cost (ATC) is minimized.

E) total revenue (TR) equals total cost (TC).

64) A perfectly competitive firm will maximize profit when the quantity produced is such that

the

A) firm’s total revenue is equal to total cost.

B) firm’s marginal revenue is equal to the price.

C) firm’s marginal revenue is equal to its marginal cost.

D) price exceeds the firm’s marginal cost by as much as possible.

E) firm’s marginal revenue exceeds its marginal cost by the maximum amount possible.

65) For a perfectly competitive firm, profit is maximized at the output level where

i. total revenue exceeds total cost by the largest amount.

ii. marginal revenue equals marginal cost.

iii. price equals marginal cost.

A) i only

B) ii only

C) ii and iii

D) i and ii

E) i, ii, and iii

66) If a perfectly competitive wheat farmer is maximizing its profit and then increases its output,

the farmer’s

A) total revenue increases, but total cost rises by more so that the farmer’s total profit decreases.

B) total revenue decreases and total cost increases, both thereby decreasing the farmer’s total

profit.

C) total revenue does not change but total cost increases, thereby decreasing the farmer’s total

profit.

D) marginal revenue increases, but so does marginal cost so that the farmer’s total profit

increases.

E) total revenue and total cost both rise but the effect on the farmer’s total profit is uncertain.

67) To increase its profit, a perfectly competitive firm will produce more output when

A) price is greater than average fixed cost.

B) price is greater than marginal cost.

C) marginal cost is less than average total cost.

D) average variable cost is greater than average fixed cost.

E) price is greater than average variable cost.

68) In a perfectly competitive market, the market price is $23. At the current level of output, a

firm has a marginal cost of $28. What should the firm do?

A) produce a larger output to earn more profit

B) nothing, it is currently maximizing profit

C) produce less output to earn more profit

D) shut down

E) raise the price of its product

69) A perfectly competitive firm is producing at the quantity where marginal cost is $6 and

average total cost is $4. The price of the good is $5. To maximize its profit, this firm should

A) raise its price.

B) lower its price.

C) increase its output.

D) decrease its output.

E) increase the price it charges for its product.

70) Suppose that a perfectly competitive firm’s marginal revenue equals $12 when it sells 10

units of output. If the marginal cost of producing the 10th unit is $14, to maximize its profit the

firm should

A) do nothing because it is already maximizing its profit.

B) decrease its production.

C) increase its production.

D) shut down.

E) increase the price it charges for its product.

71) Shama is producing candles in a perfectly competitive market. When she produces 500

candles, her total cost is $250. If she produces one additional candle, her total cost increases to

$260. In order to maximize her profit, she should produce the additional candle

A) if the market price for a candle is $12.

B) only if the market price exceeds $260 for a candle.

C) only if the market price exceeds $250 for a candle.

D) if the market price for a candle exceeds $0.50.

E) if her price exceeds her average total cost.

72) Jennifer’s Bakery Shop produces baked goods in a perfectly competitive market. If Jennifer

decides to produce her 100th batch of cookies, the marginal cost is $120. She can sell this batch

of cookies at a market price of $110. To maximize her profit, Jennifer should

A) not produce this additional batch.

B) produce this batch of cookies because they will help lower her average fixed cost.

C) charge $120 for this batch.

D) shut down.

E) produce this batch of cookies because their MR exceeds their MC.

73) Henry, a perfectly competitive lime grower in Southern California, notices that the market

price of limes is greater than his marginal cost. What should Henry do?

A) expand his output to increase profits

B) shut down and incur a loss equal to his total fixed cost

C) advertise his limes to be able to sell more output

D) look for the output level where marginal revenue minus marginal cost is maximized

E) shut down and earn no profit but also incur no loss

74) Jerry’s Jellybean Factory produces 2,000 pounds of jellybeans per month and sells them in a

perfectly competitive market. The marginal cost is $3 per pound, the average variable cost is $2

per pound, and the beans sell for $4 per pound. Jerry

A) is maximizing profit.

B) is incurring an economic loss and should shut down.

C) could increase his profit by producing more beans.

D) could increase his profit by producing fewer beans.

E) could increase his profit by raising the price of his beans.

75) If a perfectly competitive firm’s marginal revenue is greater than its marginal cost, as it

increases its output, its profit ________ and the price it can charge for its product ________.

A) increases; does not change

B) decreases; falls

C) increases; falls

D) decreases; rises

E) decreases; does not change

76) Mark owns a cattle ranch near Hugo, Oklahoma. Mark is currently producing beef at an

output level where marginal revenue exceeds marginal cost. In order to maximize his profit,

Mark should

A) not change his output.

B) decrease his output.

C) increase his output.

D) shut down his ranch.

E) probably change his output, but more information is needed to determine if he should

increase, decrease, or not change it.

77) During the winter, theme parks in Orlando close earlier than in the summer. The reason the

theme parks close early during the winter is because during that season the marginal revenue

from staying open later is ________ the marginal cost.

A) greater than

B) less than

C) equal to

D) zero compared to

E) not comparable to

78) A perfectly competitive firm is earning an economic profit when total fixed costs increase.

Assuming the firm does not shut down, in the short run the firm will

A) charge a higher price.

B) produce more output so the extra revenue will cover the increased costs.

C) produce less output to decrease total costs.

D) continue producing the same quantity as before but will earn less economic profit.

E) continue producing the same quantity as before and continue earning the same economic

profit as before.

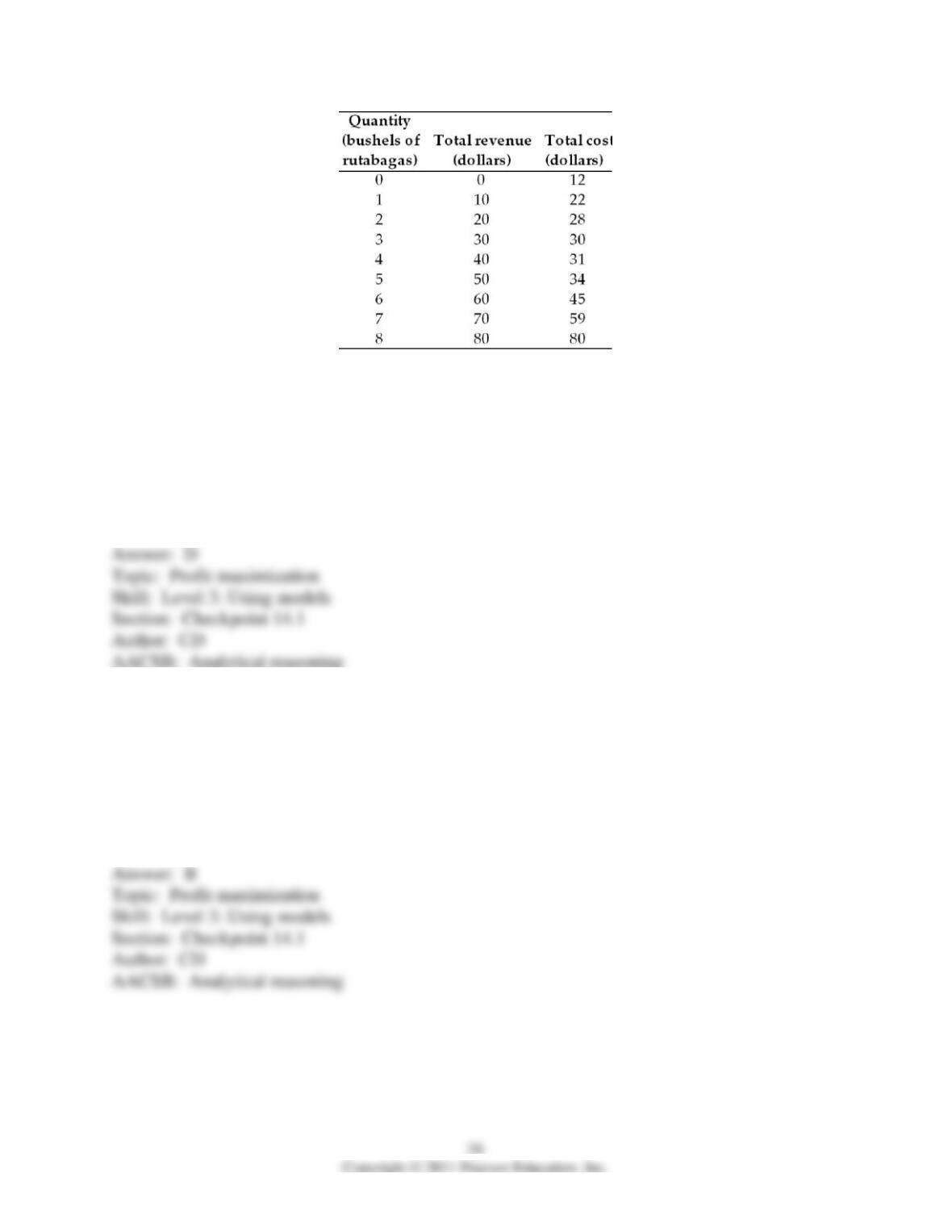

79) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. When Omar produces 2 bushels of rutabagas, his total profit

equals

A) $0.

B) $20.

C) $28.

D) -$8.

E) $48.

80) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. Omar’s total profit is maximized when he produces ________

bushels of rutabagas.

A) 3

B) 5

C) 6

D) 8

E) 7

81) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. When Omar maximizes his profit, Omar’s profit equals

A) $80.

B) $11.

C) $30.

D) $16.

E) $105.

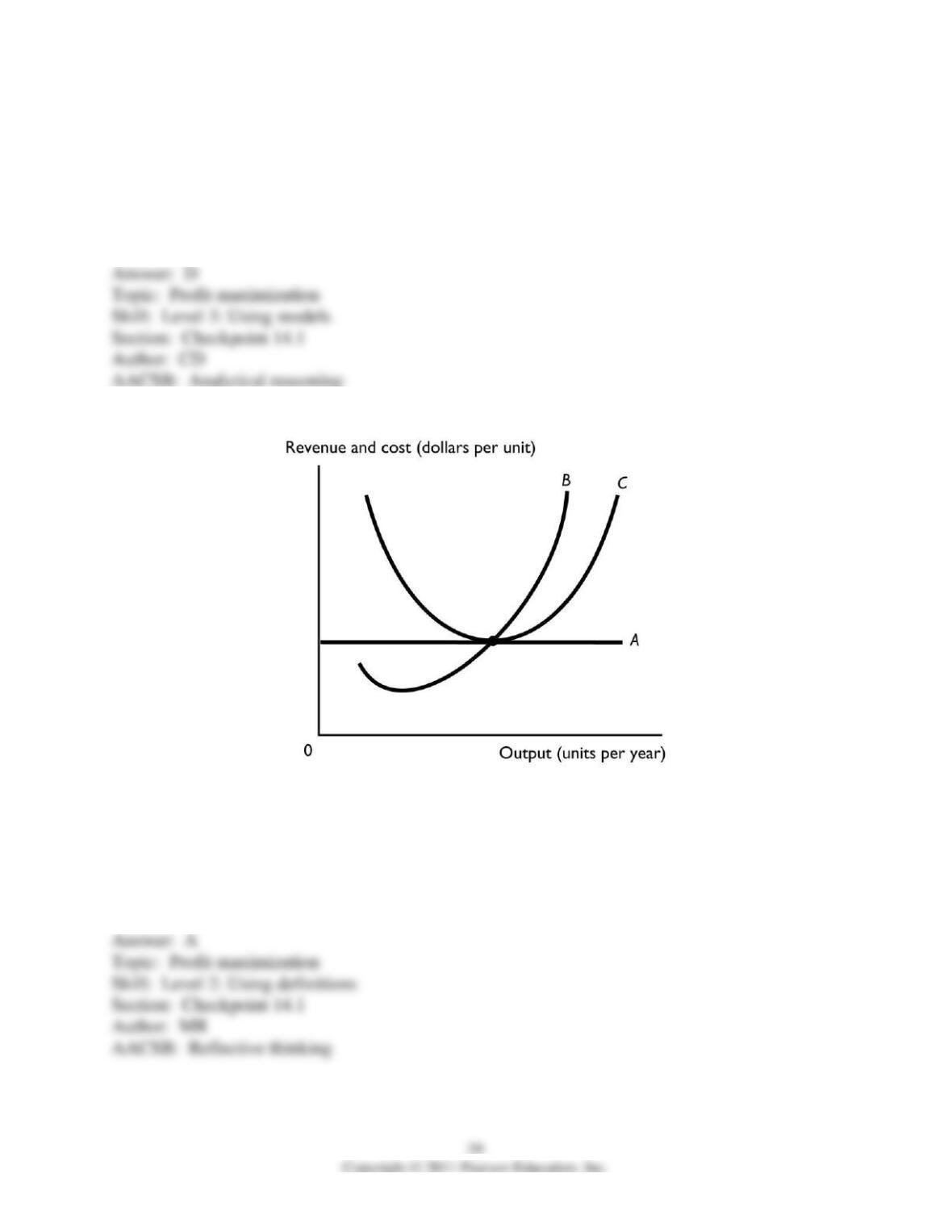

82) The above figure illustrates a perfectly competitive firm. Curve A represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

83) The above figure illustrates a perfectly competitive firm. Curve B represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

84) The above figure illustrates a perfectly competitive firm. Curve C represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) market demand curve.

E) AFC curve.

85) The above figure illustrates a perfectly competitive firm. If the market price is $40 a unit, to

maximize its profit (or minimize its loss) the firm should

A) shut down.

B) produce more than 10 and less than 30 units.

C) produce 30 units.

D) produce more than 30 units and less than 40 units..

E) produce 40 units.

86) The above figure illustrates a perfectly competitive firm. If the market price is $10 a unit, to

maximize its profit (or minimize its loss) the firm should

A) shut down.

B) produce between 10 and less than 30 units.

C) produce 30 units.

D) produce more than 30 units and less than 40 units.

E) produce 40 units.

87) If a firm shuts down, it

A) earns zero economic profit.

B) incurs an economic loss equal to its total variable cost.

C) incurs an economic loss equal to its total fixed cost.

D) earns a normal profit.

E) might earn an economic profit, a normal profit, or incur an economic loss.

88) If a struggling perfectly competitive furniture store in Detroit shuts down, it incurs an

economic loss equal to its

A) marginal cost.

B) total fixed cost.

C) total variable cost.

D) average variable cost.

E) average total cost.

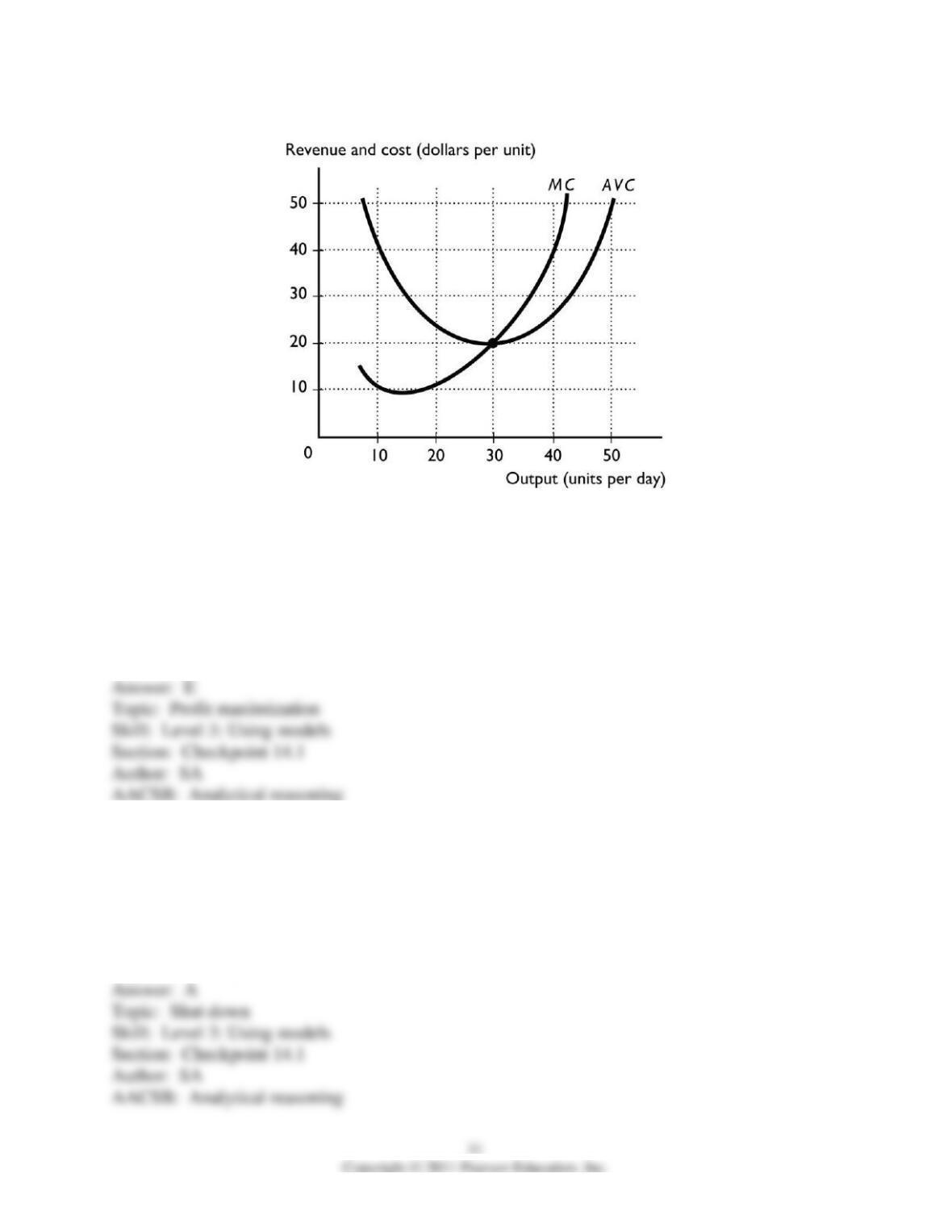

89) A perfectly competitive firm will shutdown when the price is just below the minimum point

on the

A) average fixed cost curve.

B) average total cost curve.

C) marginal cost curve.

D) average variable cost curve.

E) marginal revenue curve.

90) Under which of the following conditions will a profit-maximizing perfectly competitive firm

shut down in the short run?

A) when it is earning a normal profit

B) whenever its marginal cost is less than its marginal revenue

C) when the price is less than its minimum average variable cost

D) whenever its total cost is greater than its total revenue

E) when the price is less than its minimum average total cost

91) A perfectly competitive firm will continue to operate in the short run when the market price

is below its average total cost if the

A) marginal revenue is greater than marginal cost.

B) price is at least equal to the minimum average variable cost.

C) total fixed costs are less than total revenue.

D) marginal cost is minimized.

E) price is also less than the minimum average variable cost.

92) If the price is less than a perfectly competitive firm’s minimum average variable cost, the

firm

A) earns an economic profit.

B) operates and incurs an economic loss equal to total fixed cost.

C) operates and incurs an economic loss equal to average variable cost.

D) shuts down and incurs an economic loss equal to total fixed cost.

E) shuts down and incurs an economic loss equal to average variable cost.

93) Which of the following is true if a firm shuts down?

i. The price is less than minimum average variable cost.

ii. The firm is able to avoid an economic loss.

iii. The firm incurs a loss equal to its total variable cost.

A) i only

B) i and ii

C) i and iii

D) iii only

E) ii only

94) If the market price is $50 for a unit of a good produced in a perfectly competitive market and

the firm’s minimum average variable cost is $52, then to maximize its profit (or minimize its

loss) the firm should

A) definitely produce the unit.

B) shut down.

C) not produce the unit but remain open.

D) not produce the unit. Whether the firm should shut down or remain open cannot be

determined without more information.

E) produce the unit only if the price exceeds the average fixed cost.

95) Suppose a perfectly competitive firm’s minimum average variable cost is $3 when it

produces 50. If the price is $2 and the firm’s marginal cost is $2, the firm should

A) continue to produce, but produce more than 50.

B) continue to produce 50.

C) continue to produce, but produce less than 50.

D) shut down.

E) continue to operate, but to determine the amount of production needs more information than is

given.

96) Under what conditions would a perfectly competitive cotton farmer who is incurring an

economic loss temporarily stay in business?

A) if the total revenue exceeds the total fixed cost

B) if the total revenue exceeds the total variable cost

C) if the total revenue is positive

D) if the total revenue is increasing

E) if the marginal revenue exceeds the price.

97) The largest loss a profit-maximizing perfectly competitive firm can incur in the short run

equals its

A) average variable cost multiplied by output.

B) total fixed cost.

C) marginal cost multiplied by the number of units produced.

D) average total cost multiplied by the number of units produced.

E) total variable cost.

98) The rutabaga market is perfectly competitive and the price of a ton of rutabagas rises. As a

result, Rudy, a rutabaga farmer, will

A) decrease his output of rutabagas.

B) not change his output of rutabagas because Rudy’s firm is a price taker.

C) increase his output of rutabagas.

D) at first decrease and then increase his output of rutabagas.

E) probably change his output of rutabagas, but more information is needed about the change in

the marginal revenue of a ton of rutabagas.

99) A perfectly competitive firm’s short-run supply curve is

A) horizontal at the market price.

B) its total cost curve above the AVC.

C) its marginal cost curve below the marginal revenue curve.

D) its marginal cost curve above the AVC curve.

E) its marginal revenue curve below the ATC curve.

100) The firm’s supply curve is its

A) marginal cost curve above the average variable cost curve.

B) marginal cost curve below the average variable cost curve.

C) average variable cost curve above the marginal cost curve.

D) average total cost curve above the marginal cost curve.

E) marginal revenue curve above the average total cost curve.

101) Which of the following will increase a perfectly competitive seller’s short-run supply and

shift the firm’s short-run supply curve rightward?

A) an increase in the market price

B) a decrease in average fixed costs

C) a decrease in marginal cost

D) Both answers A and B are correct.

E) Both answers A and C are correct.

102) The four market types are

A) perfect competition, imperfect competition, monopoly, and oligopoly.

B) oligopoly, monopsony, monopoly, and imperfect competition.

C) perfect competition, monopoly, monopolistic competition, and oligopoly.

D) oligopoly, oligopolistic competition, monopoly, and perfect competition.

E) perfect competition, imperfect competition, monopoly, and duopoly.

103) A requirement of perfect competition is that

i. many firms sell an identical product to many buyers.

ii. there are no restrictions on entry into (or exit from) the market, and established firms have no

advantage over new firms

iii. sellers and buyers are well informed about prices.

A) i only

B) i and ii

C) iii only

D) i and iii

E) i, ii, and iii

104) A perfectly competitive firm is a price taker because

A) many other firms produce the same product.

B) only one firm produces the product.

C) many firms produce a slightly differentiated product.

D) a few firms compete.

E) it faces a vertical demand curve.

105) The demand curve faced by a perfectly competitive firm is

A) horizontal.

B) vertical.

C) downward sloping.

D) upward sloping.

E) U-shaped.

106) For a perfectly competitive corn grower in Nebraska, the marginal revenue curve is

A) downward sloping.

B) the same as its demand curve.

C) upward sloping.

D) U-shaped.

E) vertical at the profit maximizing quantity of production.

107) A perfectly competitive firm maximizes its profit by producing at the point where

A) total revenue equals total cost.

B) marginal revenue is equal to marginal cost.

C) total revenue is equal to marginal revenue.

D) total cost is at its minimum.

E) total revenue is at its maximum.

108) If the market price is lower than a perfectly competitive firm’s average total cost, the firm

will

A) immediately shut down.

B) continue to produce if the price exceeds the average fixed cost.

C) continue to produce if the price exceeds the average variable cost.

D) shut down if the price exceeds the average fixed cost.

E) shut down if the price is less than the average fixed cost.

109) One part of a perfectly competitive trout farm’s supply curve is its

A) marginal cost curve below the shutdown point.

B) entire marginal cost curve.

C) marginal cost curve above the shutdown point.

D) average variable cost curve above the shutdown point.

E) marginal revenue curve above the demand curve.

14.2 Output, Price, and Profit in the Short Run

1) The market supply in the short run for the perfectly competitive industry is

A) the same as each producer’s supply.

B) the sum of the supply schedules of all firms.

C) divided up according to each firm’s selling price.

D) set at the maximum price a buyer will pay for one unit.

E) equal to the average of each firm’s supply schedule.

2) If there are 1,000 identical rice farmers who are each willing to supply 200 bushels of rice at

$2 per bushel, what price and quantity combination is a point on the market supply curve for

rice?

A) $2 and 200 bushels

B) $2 and 200,000 bushels

C) $2,000 and 200,000 bushels

D) $2,000 and 1,000 bushels

E) $2 and 1,000 farmers

3) In the short run, a perfectly competitive firm ________ earn an economic profit and ________

incur an economic loss.

A) might; will never

B) will never; might

C) might; might

D) will never; will never

E) will definitely; will never

4) In the short run, a perfectly competitive firm

A) can earn only a normal profit.

B) can possibly earn an economic profit or possibly incur an economic loss.

C) produces the level of output that sets the average total cost equal to the market price.

D) can vary all its inputs.

E) can change only its fixed inputs.