Foundations of Microeconomics, 5e (Bade/Parkin)

Chapter 14 Perfect Competition

14.1 A Firm’s Profit-Maximizing Choices

1) A market with a large number of sellers

A) can only be a perfectly competitive market.

B) might be an oligopoly or a perfectly competitive market.

C) might be a monopolistically competitive or a perfectly competitive market.

D) might be a perfectly competitive, monopolistically competitive, oligopoly, or monopoly

market.

E) can only be a monopolistically competitive market.

2) What is the difference between perfect competition and monopolistic competition?

A) Perfect competition has a large number of small firms while monopolistic competition does

not.

B) Perfect competition has barriers to entry while monopolistic competition does not.

C) Perfect competition has no barriers to entry, while monopolistic competition does.

D) In perfect competition, firms produce identical goods, while in monopolistic competition,

firms produce slightly different goods.

E) In monopolistic competition, firms produce identical goods, while in perfect competition,

firms produce slightly different goods.

3) A perfectly competitive firm

A) sells a product that has perfect substitutes.

B) has a perfectly inelastic demand.

C) has a perfectly elastic supply.

D) Answer A and answer B are correct.

E) Answer A and answer C are correct.

4) In which market structure do firms exist in very large numbers, each firm produces an

identical product, and there is freedom of entry and exit?

A) monopoly

B) oligopoly

C) only perfect competition

D) only monopolistic competition

E) either perfect competition or monopolistic competition

5) The characteristics that describe a perfectly competitive industry include

A) many firms selling an identical product.

B) one firm selling to many buyers.

C) many firms selling a slightly differentiated product.

D) a few firms selling to many buyers.

E) None of the above answers is correct.

6) In part, perfect competition arises if

i. each firm’s minimum efficient scale is large relative to demand.

ii. each firm produces a good or service identical to those produced by its many competitors.

iii. there are significant barriers to entry.

A) i only

B) ii only

C) i and ii

D) iii only

E) ii and iii

7) In which of the following market types do all firms sell products so identical that buyers do

not care from which firm they buy?

A) perfect competition

B) monopolistic competition

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

8) A market in which many firms sell identical products is

A) a monopoly.

B) an oligopoly.

C) perfectly competition.

D) monopolistic competition.

E) perfect competition and monopolistic competition.

9) One requirement for an industry to be perfectly competitive is that in the industry there

A) are a few firms who control the market.

B) are many firms for whom the efficient scale of production is small.

C) is one firm that sells a product with no close substitutes.

D) are many firms selling different products.

E) is a barrier to entry that makes the entry of new firms difficult.

10) One requirement for an industry to be perfectly competitive is that

A) there are no restrictions on entry into or exit from the market.

B) there are multiple restrictions on entry into or exit from the market.

C) there are many firms selling different products.

D) sellers and buyers have imperfect information about prices.

E) the many firms sell slightly different products.

11) One requirement for an industry to be perfectly competitive is that

A) sellers and buyers have imperfect information about prices.

B) established firms have no advantage over new firms.

C) established firms have a significant advantage over new firms.

D) different firms produce widely different products.

E) many firms produce slightly different products.

12) A perfectly competitive market arises when

A) the market demand is small relative to the output of a firm.

B) there are many buyers but few sellers.

C) the market demand is very large relative to the output of one seller.

D) a firm has control over a unique resource.

E) each of the many firms produces a slightly different product.

13) Each firm in a perfectly competitive industry

A) produces a good that is slightly different from that of the other firms.

B) produces a good that is identical to that of the other firms.

C) attains economies of scale so that its efficient size is large compared to the market as a whole.

D) has control over at least one unique resource to separate themselves from their competitors.

E) has an important influence on the market price of the good or service being produced.

14) Perfect competition is characterized by all of the following EXCEPT

A) a large number of buyers and sellers.

B) no restrictions on entry into or exit from the industry.

C) considerable advertising by individual firms.

D) buyers and sellers are well informed about prices.

E) firms produce an identical product.

15) Which of the following is the best example of a perfectly competitive market?

A) farming

B) diamonds

C) athletic shoes

D) soft drinks

E) electricity distribution

16) Which of the following market types has the fewest number of firms?

A) perfect competition

B) monopolistic competition

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

17) A monopoly occurs when

A) each of many firms produces a product that is slightly different from that of the other firms.

B) one firm sells a good that has no close substitutes and a barrier blocks entry for other firms.

C) there are many firms producing the same product.

D) a few firms control the market.

E) one firm is larger than the many other firms that make an identical product.

18) In which market structure does one firm sell a good or service with no close substitutes and

there is a barrier blocking the entry of new firms?

A) only monopoly

B) only oligopoly

C) perfect competition

D) monopolistic competition

E) either monopoly or oligopoly

19) When one firm sells a good or service that has no close substitutes and a barrier blocks the

entry of new firms, what type of market is this?

A) perfect competition

B) only monopoly

C) oligopoly

D) only monopolistic competition

E) either monopoly or monopolistic competition

20) ________ a large number of firms competing by making similar but slightly different

products.

A) Monopoly requires

B) Perfect competition requires

C) Monopolistic competition requires

D) Oligopoly requires

E) Both perfect competition and monopolistic competition require

21) A market is classified as monopolistically competitive when

A) there is a barrier that blocks entry by other firms.

B) a small number of firms compete.

C) many firms produce the same product.

D) many firms produce a slightly differentiated product.

E) there is one firm that sells a good or service with no close substitutes.

22) In which market structure is there a large number of firms producing slightly differentiated

products?

A) monopoly

B) oligopoly

C) only perfect competition

D) only monopolistic competition

E) either perfect competition or monopolistic competition

23) A market is classified as an oligopoly when

A) a few firms compete.

B) many firms produce a slightly differentiated product.

C) no matter how many firms are in the market, a barrier blocks entry by other new firms.

D) many firms produce the same product.

E) only one firm sells a product with no close substitutes.

24) Which of the following market types has only a few competing firms?

A) perfect competition

B) monopolistic competition

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

25) In which market structure are there a small number of firms competing?

A) only monopoly

B) only oligopoly

C) perfect competition

D) monopolistic competition

E) either monopoly or oligopoly

26) A market is ________ when a small number of firms compete.

A) a monopoly

B) perfectly competitive

C) monopolistically competitive

D) an oligopoly

E) either monopolistically competitive or an oligopoly

27) The firm’s over-riding objective is to

A) earn a normal profit.

B) maximize normal profit.

C) maximize economic profit.

D) maximize total revenue.

E) avoid an economic loss.

28) Normal profit is

A) the same thing as economic profit.

B) the return to entrepreneurship.

C) total revenue minus the total opportunity cost of production.

D) the point of profit when total revenue is maximized.

E) part of the firm’s total revenue.

29) In a perfectly competitive market, the type of decision a firm has to make is different in the

short run than in the long run. Which of the following is an example of a perfectly competitive

firm’s short-run decision?

A) the profit-maximizing level of output

B) how much to spend on advertising and sales promotion

C) what price to charge buyers for the product

D) whether or not to enter or exit an industry

E) whether or not to change its plant size

30) To maximize its profit, in the short run a perfectly competitive firm decides

A) what price to charge for its product.

B) what quantity of output to produce.

C) whether to exit the market.

D) whether to increase the size of its plant.

E) how much advertising it should undertake.

31) A perfectly competitive firm can

A) sell all of its output at the prevailing market price.

B) set a higher price to customers who are willing to pay more.

C) raise its price in order to increase its total revenue.

D) sell additional output only by lowering its price.

E) usually not sell all the output it produces, but still “over-produces” because there are some

periods when it can sell the extra output at very profitable prices.

32) In a perfectly competitive market, one farmer’s barley is

A) completely different from another farmer’s barley.

B) a perfect substitute for another farmer’s barley.

C) a monopolized product in that farmer’s local market.

D) a monopolized product in the national market.

E) slightly different from another farmer’s barley.

33) A firm in perfect competition is a price taker because

A) there are no good substitutes for its good.

B) many other firms produce identical products.

C) it is very large.

D) its demand curves are downward sloping.

E) it’s demand curve is vertical at the profit-maximizing quantity.

34) The price charged by a perfectly competitive firm is

A) the same as the market price.

B) different than the price charged by competing firms.

C) lower the more the firm produces.

D) higher the more the firm produces.

E) indeterminate.

35) For a perfectly competitive firm, the price of its good is equal to the firm’s marginal revenue

because

A) information about price changes is hard to come by for small sellers.

B) price and marginal revenue are the same economic concepts.

C) individual perfectly competitive firms cannot influence the market price by changing their

output.

D) the firm’s total revenue cannot be changed by anything the firms can do.

E) there are only a small number of firms in the market.

36) A large number of sellers all selling an identical product implies which of the following?

A) market chaos

B) the inability of any seller to change the price of the product

C) large losses incurred by all sellers

D) horizontal market supply curves

E) vertical market supply curves

37) A firm that is a price taker faces

A) an elastic supply curve.

B) an inelastic supply curve.

C) a perfectly elastic demand curve.

D) a perfectly inelastic demand curve.

E) an elastic but not perfectly elastic demand curve.

38) Suppose Pat’s Paints is a perfectly competitive firm. If Pat’s Paints’ marginal revenue equals

$5 per can, and Pat decides to sell 100 cans of paint, Pat’s total revenue equals

A) $5.

B) $100.

C) $500.

D) $20.

E) Information on the price of a can of paint is needed to answer the question.

39) If demand for a seller’s product is perfectly elastic, which of the following is true?

i. The firm will sell no output if it sets the price its product above the market price.

ii. There are many perfect substitutes for the seller’s product.

iii. The firm will sell no output if it sets the price its product below the market price.

A) i only

B) ii only

C) iii only

D) i and ii

E) ii and iii

40) A perfectly competitive firm’s demand curve is horizontal because

i. the firm is so small, relative to the market, that it cannot affect the market price.

ii. there are many perfect substitutes for its product.

iii. the firm cannot sell any output at a price higher than the market price.

A) ii only

B) i and ii

C) iii only

D) i and iii

E) i, ii, and iii

41) Cynthia is an Oklahoma wheat farmer. The demand for her wheat is

A) perfectly inelastic.

B) inelastic but not perfectly inelastic.

C) elastic but not perfectly elastic.

D) perfectly elastic.

E) unit elastic.

42) Because perfectly competitive firms are price takers, each firm faces a demand that is

A) perfectly inelastic.

B) perfectly elastic.

C) highly inelastic but never is it perfectly inelastic.

D) unit elastic.

E) highly elastic but never is it perfectly elastic.

43) If a perfectly competitive firm raised the price of its product,

A) its profits would increase.

B) the quantity of output it sells decreases to zero.

C) rival firms will follow suit and raise their prices also.

D) the firm will be forced to advertise more.

E) its total revenue would rise but its total cost would rise by more.

44) If the wheat industry is perfectly competitive with a market price of $4 per bushel and

Farmer Brown charged $5 per bushel, how many bushels would Farmer Brown sell?

A) some, but fewer than he would at a price of $4

B) more than he would at a price of $4

C) just as many as he would at a price of $4

D) none

E) More information is needed about the prices charged by the other wheat farmers.

45) How does the demand for any one seller’s product in perfect competition compare to the

market demand for that product?

A) They are identical.

B) The demand for any one seller is proportionally smaller but otherwise identical to the market

demand.

C) The demand for any one seller’s product is perfectly elastic while the market demand curve is

downward sloping.

D) There is no demand for any one seller’s competitively sold product.

E) The demand for any one seller’s product is not perfectly elastic while the market demand is

perfectly elastic.

46) For the perfectly competitive broccoli producers in California, the market demand curve for

broccoli is

A) a horizontal line.

B) downward sloping.

C) nonexistent.

D) upward sloping.

E) the same as the demand curve each firm faces.

47) The market demand curve in a perfectly competitive market is ________ and the demand

curve for a perfectly competitive firm’s output is ________.

A) downward sloping; downward sloping

B) downward sloping; horizontal

C) horizontal; downward sloping

D) horizontal; horizontal

E) downward sloping; upward sloping

48) Elsie is a perfectly competitive dairy farmer. If the market price of milk falls to $2.20 a

gallon from $2.40 a gallon, Elsie

A) can sell as much milk as she wants at $2.20 a gallon.

B) will have to charge some customers $2.40 a gallon to stay in business.

C) will produce the same amount of milk at both prices.

D) can sell more at the lower price because the quantity demanded is higher at lower prices.

E) will be able to charge her initial customers $2.40 a gallon.

49) For a perfectly competitive palm tree nursery in South Carolina, the total revenue curve is

A) downward sloping.

B) a horizontal line.

C) upward sloping.

D) U-shaped.

E) undefined because the firm is perfectly competitive.

50) If the market price of a product is $14 and all sellers are price takers, then which of the

following is correct?

A) Each seller’s total revenue line is graphed as an upward-sloping straight line.

B) The demand curve for each seller’s product is a downward-sloping straight line.

C) Each seller can earn more total revenue by raising the price he or she charges above $14.

D) The demand curve for each seller’s product is a downward-sloping but not necessarily a

straight line.

E) Each seller’s total revenue is graphed as an upside-down U-shaped curve.

51) Marginal revenue is

A) the change in total revenue from a one-unit increase in the quantity sold.

B) another name for total revenue.

C) the change in total cost from producing an additional unit of output.

D) the economic profit from producing an additional unit of output.

E) less than price for a perfectly competitive firm.

52) A firm’s marginal revenue is

A) the change in total revenue that results from a one-unit increase in the quantity sold.

B) total revenue minus total cost.

C) the change in total revenue minus the change in total cost.

D) the change in total revenue that results from an increase in the demand for the good or

service.

E) less than the market price for a perfectly competitive firm.

53) For a perfectly competitive firm, marginal revenue is

A) less than the price.

B) greater than the price.

C) equal to the price.

D) equal to the change in profit from selling one more unit.

E) undefined because the firm’s demand curve is horizontal.

54) In perfect competition, marginal revenue

A) increases as more is sold.

B) decreases as more is sold.

C) is equal to the market price.

D) is zero.

E) is always greater than marginal cost.

55) For a perfectly competitive firm, the market price of a good is

A) a given which the firm cannot change.

B) determined by the firm in order to maximize its profit.

C) equal to the firm’s marginal revenue.

D) Answer A and answer B are correct.

E) Answer A and answer C are correct.

56) The marginal revenue curve for a perfectly competitive firm is

A) horizontal.

B) vertical.

C) upward sloping.

D) downward sloping.

E) a straight line coming out of the origin with a 45 degree slope.

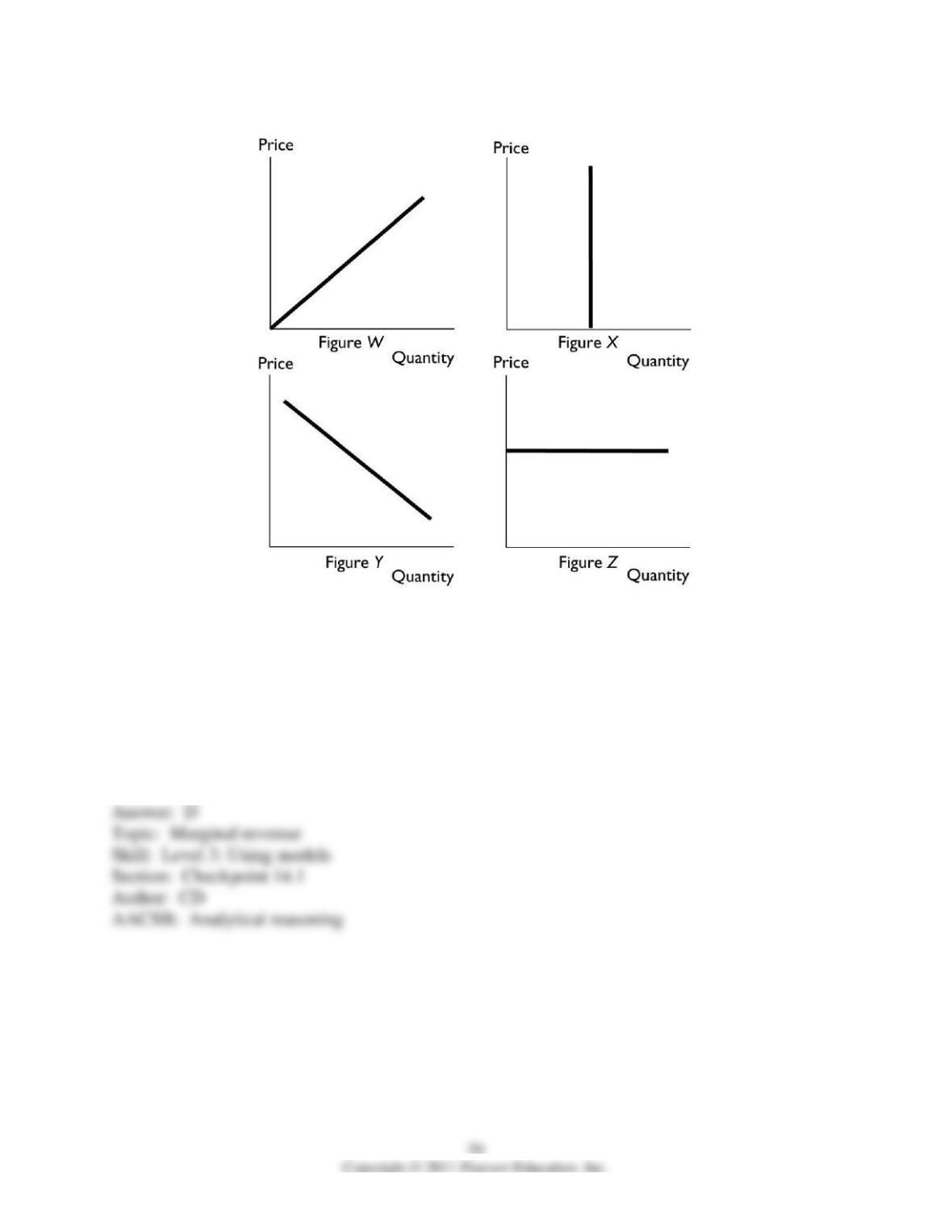

57) In the above, a marginal revenue curve for a perfectly competitive firm is shown in Figure

________.

A) W

B) X

C) Y

D) Z

E) X and Figure Z