There tends to be a high positive correlation between the rate of productivity growth

and the rate of economic growth.

In the short run, a competitive firm will not produce unless price is equal to average

total costs.

By using the same ceteris paribus assumptions, economic principles are just as certain

and precise as those of the laboratory sciences.

In the long run, pure competition forces firms to produce at the minimum of average

total cost and charge a price consistent with that cost.

Variable costs are costs that vary directly with output.

The benefit-reduction rate is the rate at which government benefits increase as the

earned income of a family increases.

The Sherman Antitrust Act specifically prohibited tying contracts and interlocking

directorates.

Those who have been critical of welfare contend that it reduces motivation to work.

An increase in consumer wealth will decrease aggregate demand.

Per-unit production cost is determined by dividing output by total input cost.

As a monopolist increases its output, it finds that its total revenue at first increases, and

that after some output level is reached, its total revenue begins to decrease.

An increase in demand accompanied by an increase in supply will increase the

equilibrium quantity, but the effect on equilibrium price will be indeterminate.

The price level in the United States is more flexible downward than upward.

The less the elasticity of product demand, the greater the elasticity of resource demand.

The financing of the public debt can increase interest rates and reduce private

investment spending.

If a firm must pay a daily wage of $35 to hire 11 workers and a daily wage of $40 to

hire 12 workers, its marginal resource cost of hiring the 12th worker is $40.

Economic profit is found by subtracting accounting costs from total revenue.

A market system is characterized by the private ownership of resources and the use of

markets and prices to coordinate and direct economic activity.

The ownership of wealth is unequally distributed across households in the United

States.

In long-run equilibrium, a competitive firm produces where P = MR = MC = minimum

ATC and earns normal economic profits.

When commercial banks borrow from the Federal Reserve Banks, they decrease their

excess reserves and their money-creating potential.

In an uncontrolled or unregulated system commercial bank lending will tend to

intensify the business cycle.

Gross private domestic investment can be divided into replacement investment and net

investment.

The long-run aggregate supply curve slope is horizontal.

The basic argument for income inequality is that it is necessary if consumer satisfaction

(utility) is to be maximized.

The higher the reserve requirement, the lower the money multiplier.

Taxes on specific goods are a method to reduce negative externalities of polluting firms.

The supply curve for a monopolist is the upsloping portion of the marginal cost curve

that lies above the average variable cost curve.

The marginal revenue product curve for an input is downward sloping because of the

law of diminishing returns.

If MR > MC for a competitive firm, it should raise its price and increase its level of

output.

Government purchases exclude spending by the government for resources such as labor.

Economic growth is shown by a shift of the production possibilities curve outward and

to the right.

The benefits-received principle of taxation is used to support corporate and personal

income taxes.

The free-rider problem makes a good profitable to provide by a private firm.

If a monopolist discovers that it is operating at a level of output where price is less than

average variable costs, it will continue to operate in the short run.

If the rate of growth in labor productivity averages 2 percent a year, it will take about

20 years for the standard of living to double.

Automatic stabilizers will reduce tax revenues during recessions and increase tax

revenues during periods of strong economic growth.

The Mear Corporation finds that its total spending on machine parts increases after the

price of machine parts falls, other things being equal. Which of the following is true

about the Mear Corporation’s demand for machine parts with the price change?

A. It is unit elastic.

B. It is price elastic.

C. It is price inelastic.

D. It is perfectly inelastic.

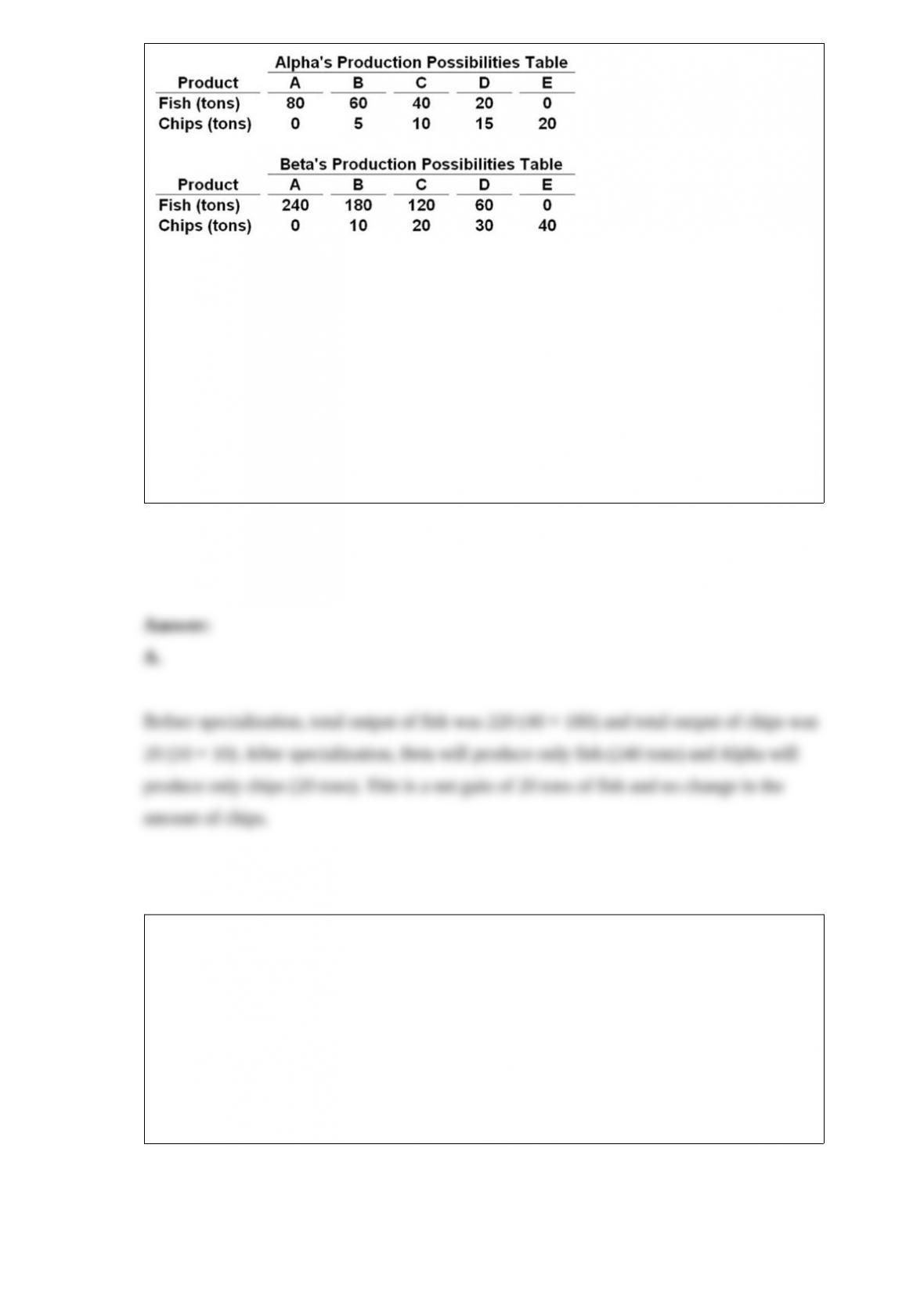

Answer the next question on the basis of the following production possibilities data for

two countries, Alpha and Beta, which have populations of equal size.

Suppose that before specialization and trade Alpha chose production alternative C and

Beta chose production alternative B. After specialization and trade the gains will be:

A. 20 tons of fish.

B. 20 tons of chips.

C. 20 tons of fish and 20 tons of chips.

D. 240 tons of fish and 20 tons of chips.

A flow of wages and salary earnings, along with rent, interest, and profits, is:

A. wealth.

B. income.

C. transfers.

D. utility.

A movement along the aggregate demand curve would be caused by a change in:

A. the quantity of real output demanded.

B. the price level.

C. an aggregate demand determinant.

D. an appreciation in the value of the U.S. dollar.

E. aggregate supply.

If you operated a small bakery, which of the following would be a variable cost in the

short run?

A. Baking ovens

B. Interest on business loans

C. Annual lease payment for use of the building

D. Baking supplies (flour, salt, etc.)

Use the following balance sheet for the ABC National Bank in answering the next

question. Assume the required reserve ratio is 20 percent.

Refer to the above data. This bank can safely expand its loans by a maximum of:

A. $7000.

B. $25,000.

C. $12,000.

D. $5000.

Suppose that Jennifer earns $10,000 in year 1 and $40,000 in year 2, while Shawna

earns $40,000 in year 1 and only $10,000 in year 2. Is there income inequality for the

two individuals?

A. The yearly data and the data over the two years indicate equality.

B. The yearly data and the data over the two years indicate inequality.

C. The yearly data indicate equality, but the data over the two years indicate inequality.

D. The yearly data indicate inequality, but the data over the two years indicate equality.

At the current price there is a shortage of a product. We would expect price to:

A. increase, quantity demanded to increase, and quantity supplied to decrease.

B. increase, quantity demanded to decrease, and quantity supplied to increase.

C. increase, quantity demanded to increase, and quantity supplied to increase.

D. decrease, quantity demanded to increase, and quantity supplied to decrease.

A profit-maximizing firm in the short run will expand output:

A. until marginal cost begins to rise.

B. until total revenue equals total cost.

C. until marginal cost equals average variable cost.

D. as long as marginal revenue is greater than marginal cost.

In the long run, a representative firm in a monopolistically competitive industry will

typically:

A. have an elasticity of demand that will be less than it was in the short run.

B. have a larger number of competitors than it will in the short run.

C. produce a level of output at which marginal cost and price are equal.

D. earn a normal profit, but not an economic profit.

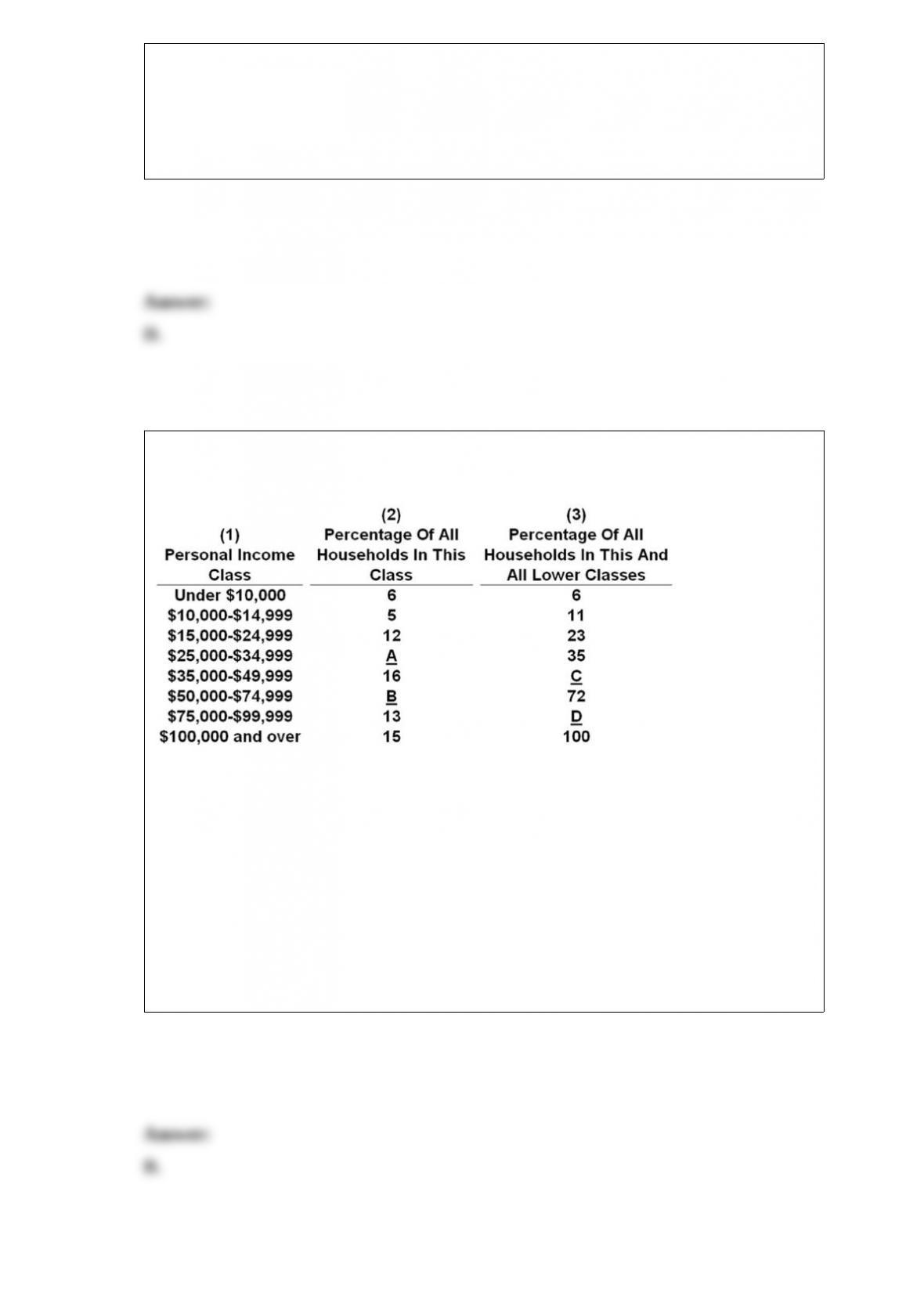

Using the data in the above table, what percentage of households made

$75,000-$99,999?

A. 11 percent

B. 13 percent

C. 16 percent

D. 85 percent

The most important of the Federal Reserve district banks is the:

A. Boston bank.

B. Chicago bank.

C. New York bank.

D. San Francisco bank.

Which is necessarily true for a purely competitive firm in short-run equilibrium?

A. Marginal revenue less marginal cost equals zero.

B. Price less average total cost equals zero.

C. Total revenue less total cost equals zero.

D. Marginal revenue is zero.

The alternative combinations of two goods that a consumer can purchase with a given

money income is:

A. a production possibilities curve.

B. a demand curve.

C. consumer equilibrium.

D. a budget line.

A craft union:

A. creates a bilateral monopoly of unskilled and skilled workers in an industry.

B. organizes workers who have similar skills or jobs in an industry.

C. is most concerned with increasing the supply for workers.

D. is most effective in a purely competitive industry.

Tennis rackets and ballpoint pens are:

A. substitute goods.

B. complementary goods.

C. inferior goods.

D. independent goods.

One condition for individual bargaining to occur, according to the Coase theorem, is

that there must be:

A.clearly defined property rights.

B.many people affected and involved.

C.government intervention to establish bargaining.

D.government creation of a market for externalities.

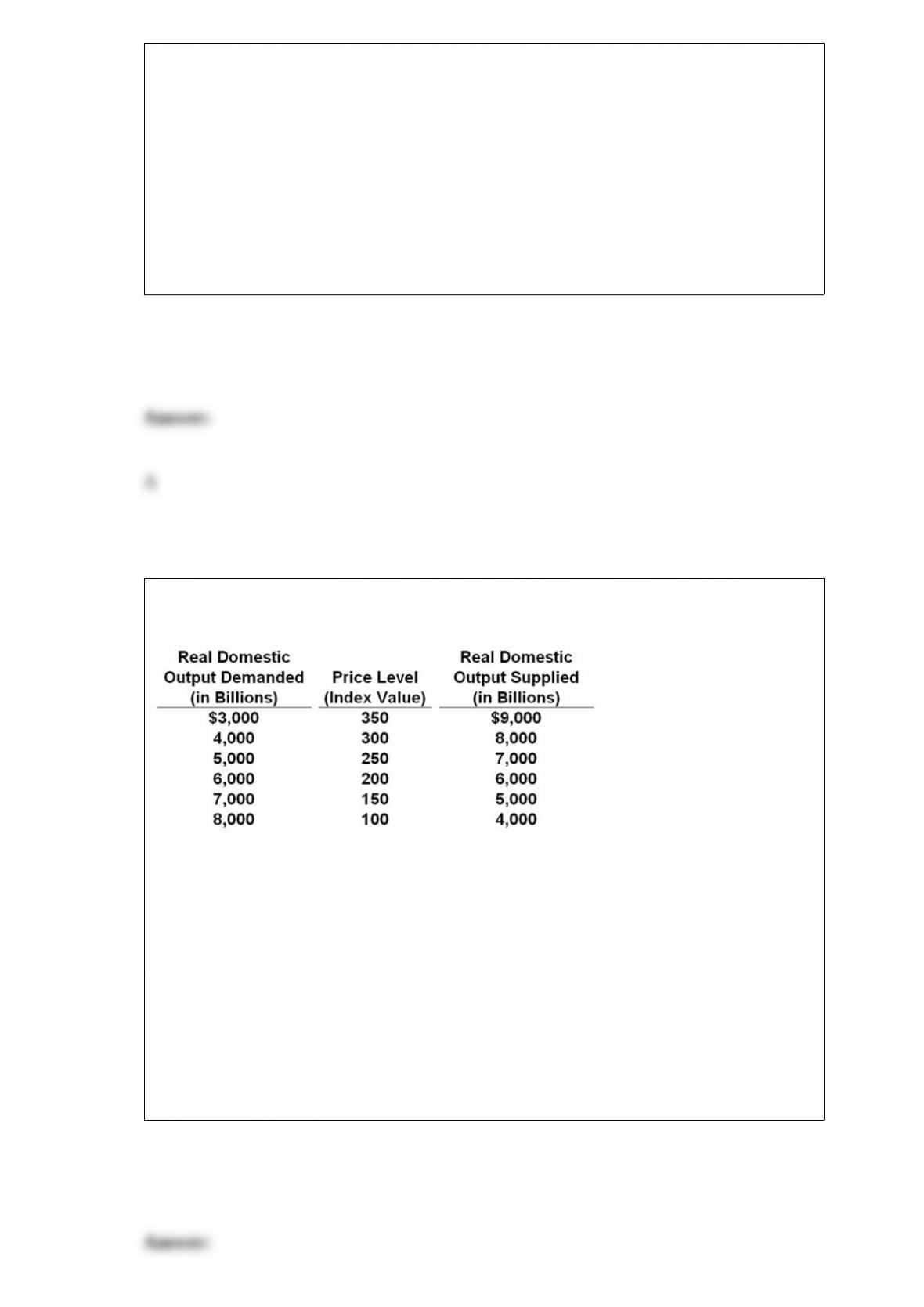

The table shows the aggregate demand and aggregate supply schedule for a

hypothetical economy.

Refer to the above table. If the quantity of real domestic output demanded increased by

$2000 at each price level, the new equilibrium price level and quantity of real domestic

output would be:

A. 350 and $8000.

B. 300 and $8000.

C. 250 and $7000.

D. 200 and $6000.

In the graph above, A is the initial budget line and B is the new budget line. Which of

the following changes might have occurred?

A. P1 was unchanged, P2 increased, income decreased.

B. P1 decreased, P2 increased, income was unchanged.

C. P1 increased, P2 decreased, income was unchanged.

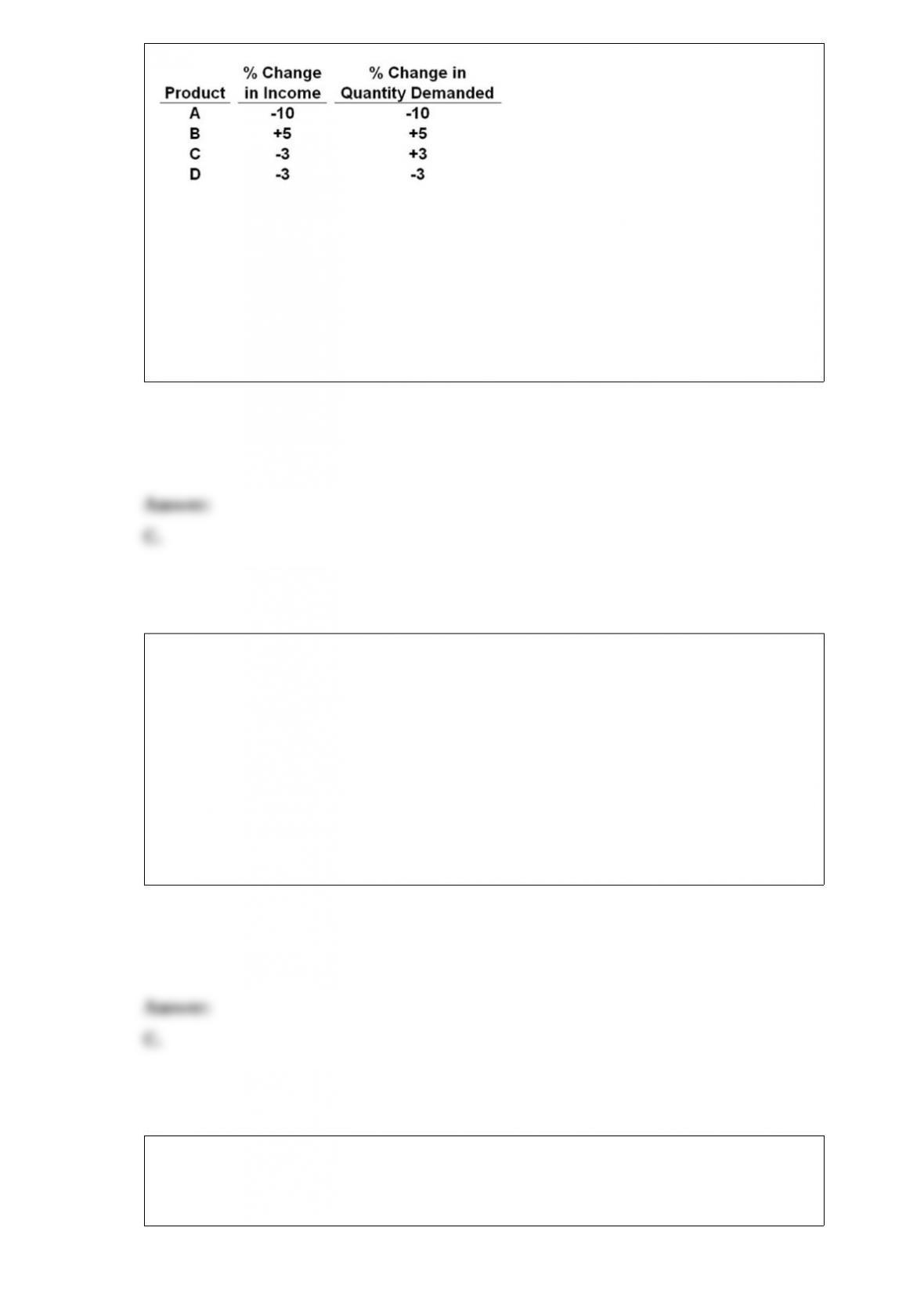

Based on the information in the table, which product would be an inferior good?

A. Product A

B. Product B

C. Product C

D. Product D

Which would be considered to be one of the factors that shift the aggregate supply

curve? A change in:

A. consumer spending.

B. net export spending.

C. government regulation.

D. consumer expectations on investment projects.

The Sunshine Corporation finds its costs are $40 when it produces no output. Its total

variable costs (TVC) change with output as shown in the accompanying table. Use this

information to answer the following question.

Refer to the above information. The average fixed cost of 3 units of output is:

A. $13.33.

B. $12.50.

C. $40.

D. $18.50.

Wage contracts, menu costs, and the minimum wage are explanations for why:

A. competition results in price wars.

B. wages tend to be inflexible downward.

C. the aggregate demand curve slopes downward.

D. there is little support for the existence of a real-balances effect.

Given a downsloping demand curve and an upsloping supply curve for a product, an

increase in the price of a substitute good will:

A. increase equilibrium price and quantity.

B. decrease equilibrium price and quantity.

C. increase equilibrium price and decrease equilibrium quantity.

D. decrease equilibrium price and increase equilibrium quantity.

In a typical graph for a purely competitive firm, the intersection of the total cost and

total revenue curves would be:

A. a point of maximum economic profit.

B. a point of minimum economic loss.

C. a point where MR = MC.

D. a break-even point.

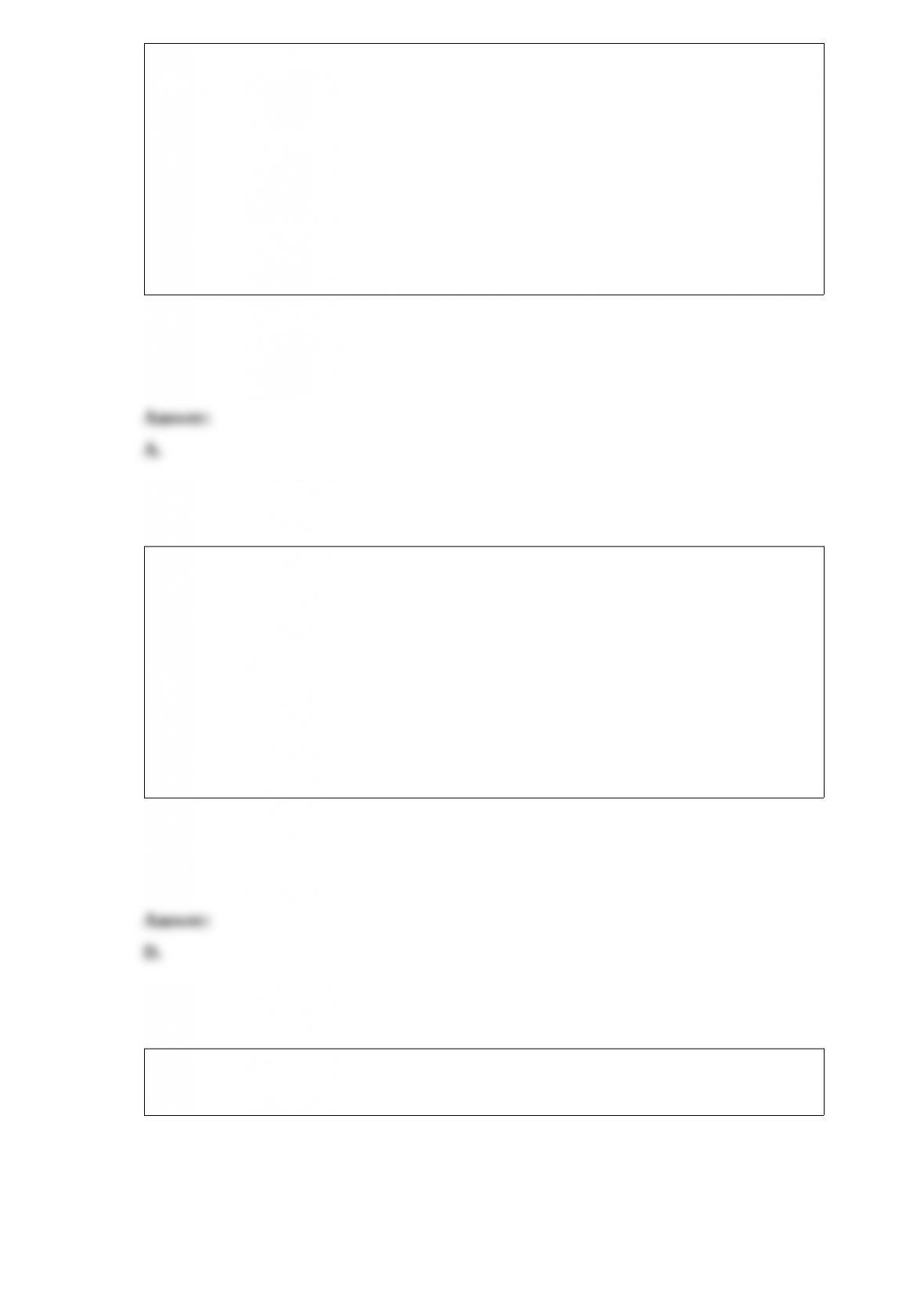

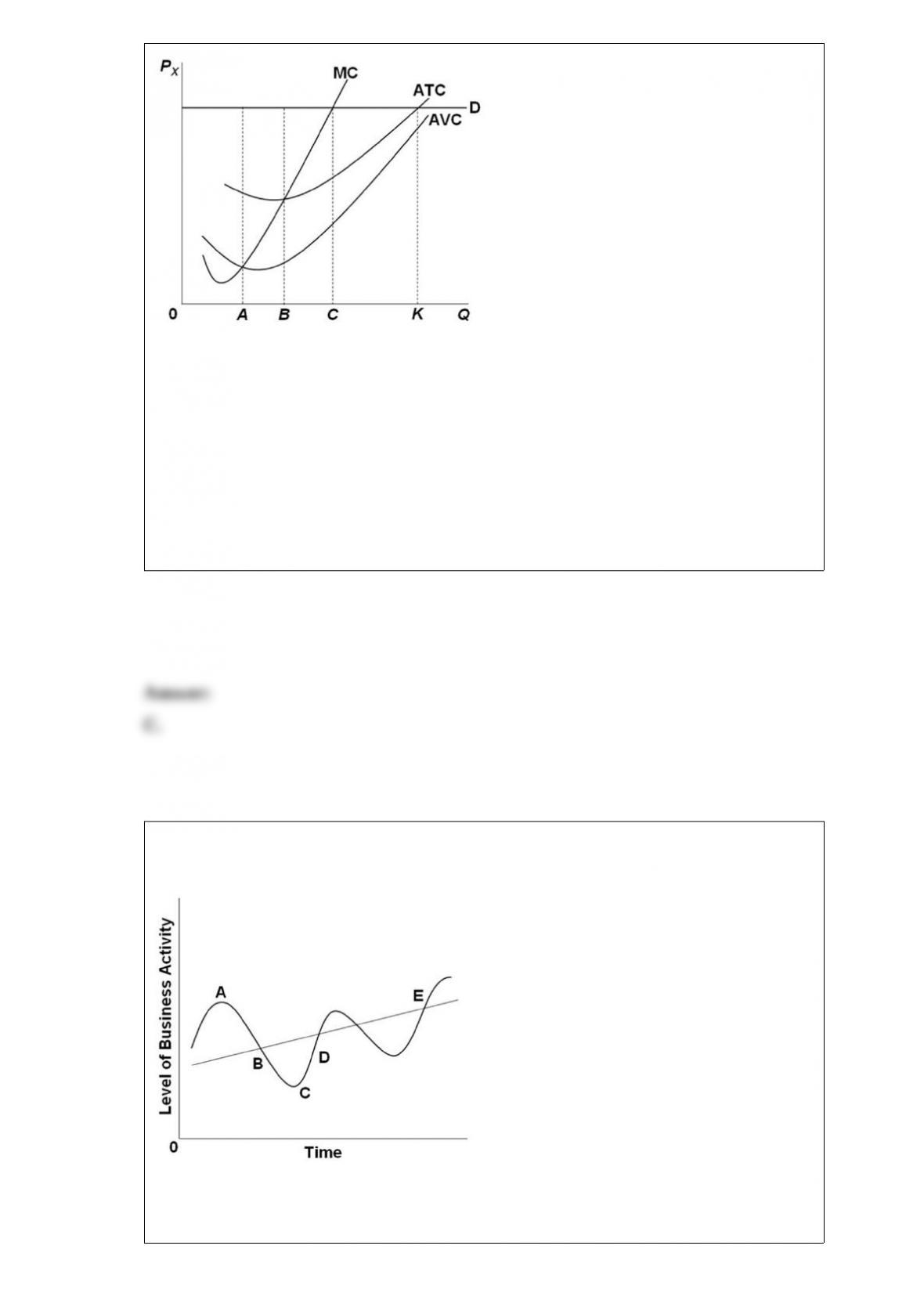

Refer to the above graph. The profit-maximizing level of output for the firm is:

A. 0A.

B. 0B.

C. 0C.

D. 0K.

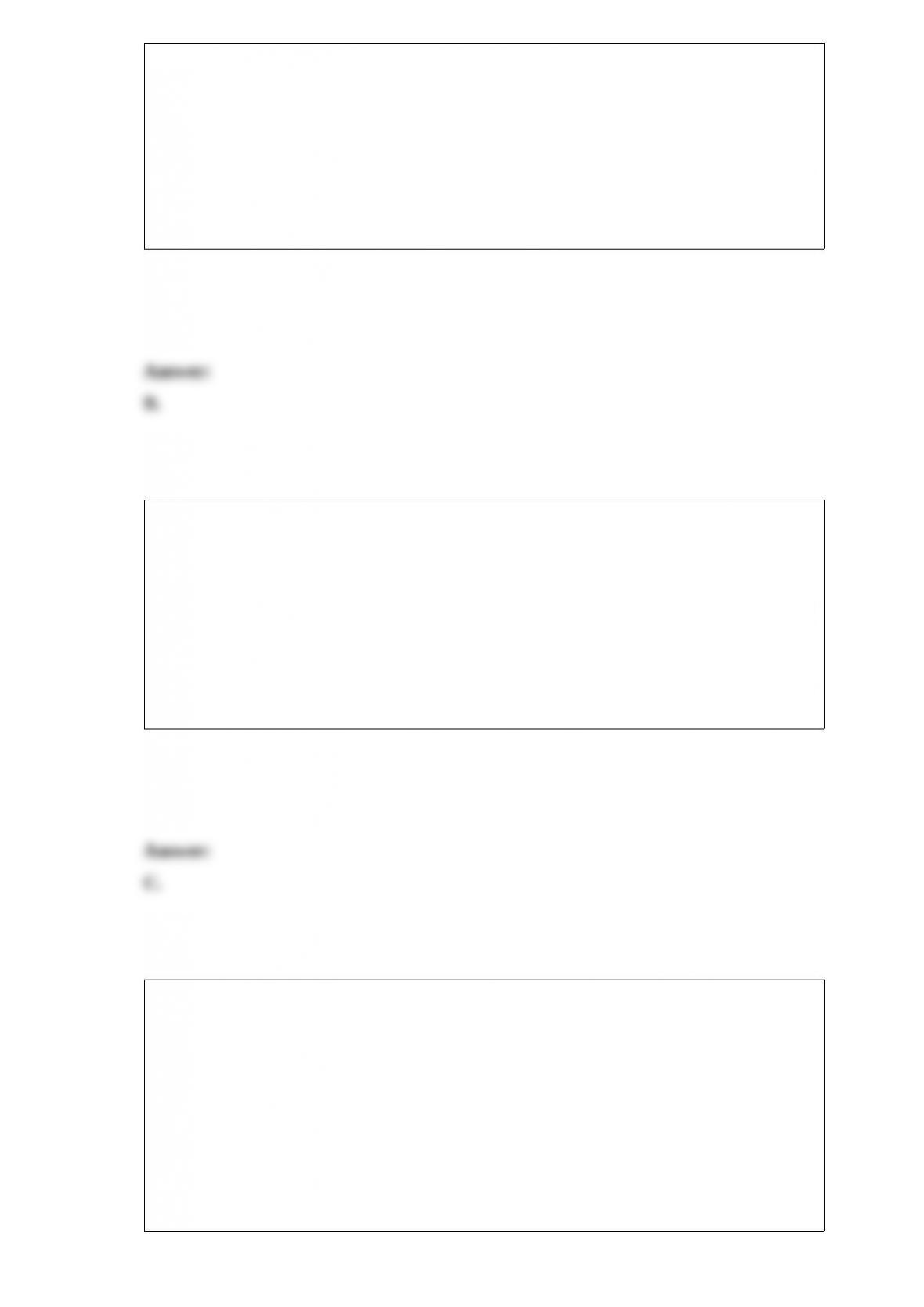

Refer to the above diagram. The straight line E drawn through the wavy lines would

provide an estimate of the:

A. recession fluctuation.

B. growth trend.

C. natural rate of unemployment.

D. recovery trend.

The GDP gap measures the amount by which:

A. nominal GDP exceeds real GDP.

B. actual GDP exceeds potential GDP.

C. potential GDP exceeds actual GDP.

D. actual GDP exceeds national income.

A tax that takes a larger proportion of income from low-income groups than from

high-income groups is a:

A. stabilizing tax.

B. regressive tax.

C. progressive tax.

D. proportional tax.

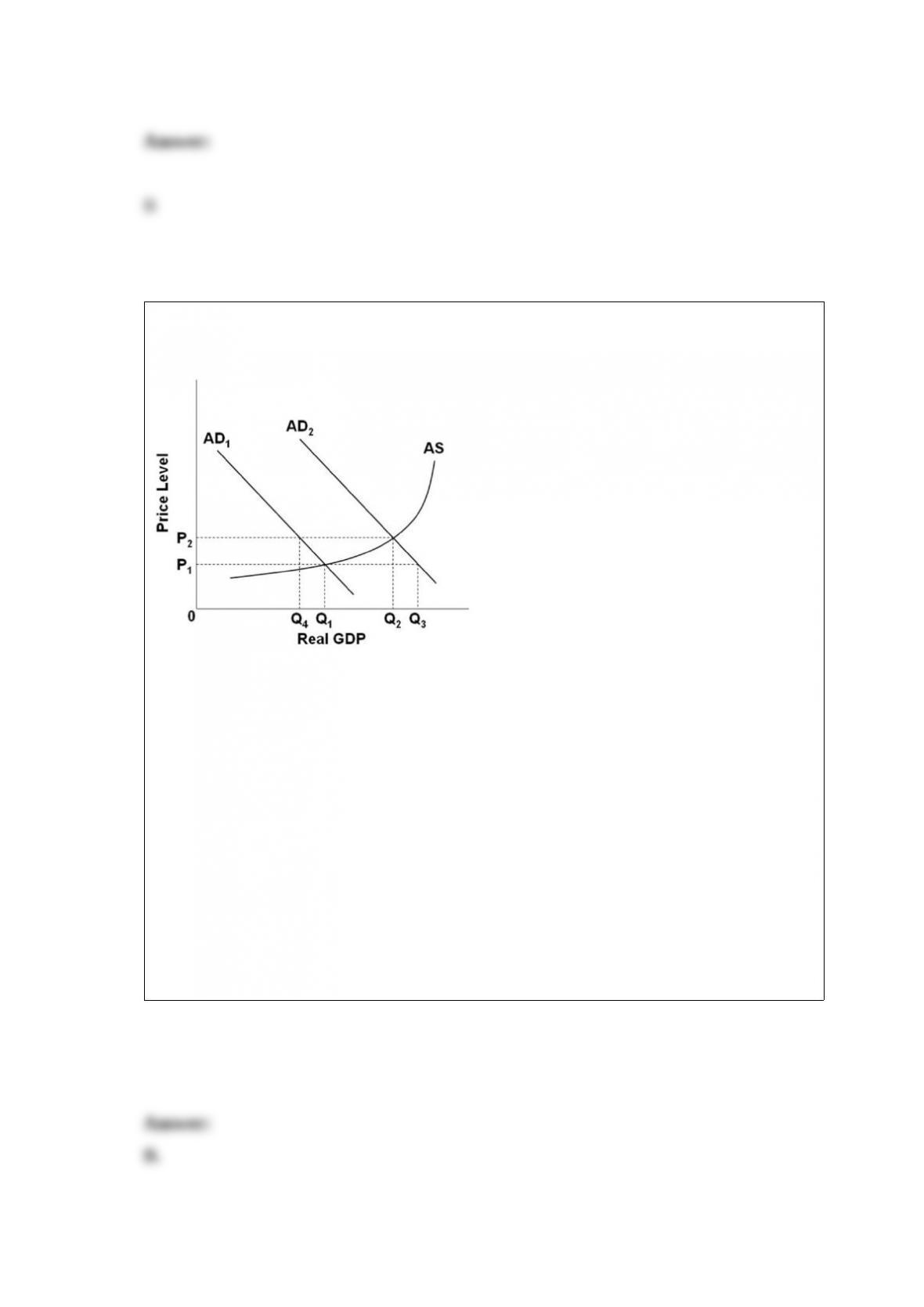

Refer to the above graph. Assume that the economy initially has a price level of P2 and

output level Q2. The price level is flexible and the government decides to adopt a

contractionary fiscal policy. What would most likely be the new equilibrium price level

and output?

A. P2 and Q4

B. P1 and Q1

C. P2 and Q2

D. P1 and Q3

The historical reallocation of labor from agriculture to manufacturing in the United

States has:

A. been inflationary.

B. had no effect on the average productivity of labor.

C. increased the average productivity of labor.

D. reduced the average productivity of labor.

The statement that “the unemployment rate will increase as the economy moves into a

recession” is an example of:

A. a normative statement.

B. a microeconomic statement.

C. marginal analysis.

D. a generalization.

If the price elasticity of demand for automobiles is 2:

A. a 10 percent decrease in price would result in a 20 percent decrease in quantity

demanded.

B. a 10 percent decrease in price would result in a 20 percent increase in quantity

demanded.

C. a 10 percent increase in price would result in a 20 percent increase in quantity

demanded.

D. a 10 percent increase in price would result in a 10 percent decrease in quantity

demanded.