Operations Management: Processes and Supply Chains, 12e (Krajewski)

Supplement A Decision Making

1) The break-even quantity is the volume at which the total revenue equals total cost.

2) The variable cost is the portion of total cost that remains constant regardless of changes in levels of

production.

3) Fixed cost is the portion of the total cost that remains constant regardless of changes in levels of output.

4) Sensitivity analysis is a technique for systematically changing parameters in a model to determine the

effects of such changes.

5) Which one of the following statements about break-even analysis for evaluating products or services is

true?

A) The break-even quantity will tend to increase as the variable cost per unit of production decreases.

B) As sales increase beyond the break-even quantity, total before-tax profits tend to decrease.

C) A restaurant’s opening of downsized facilities with only drive-through service is an example of

lowering fixed costs and the break-even quantity.

D) Increasing the unit selling price has the effect of increasing the break-even quantity.

6) Which one of the following statements about break-even analysis, as we applied it to evaluating

products or services, is best?

A) Break-even analysis assumes that the cost function is linear and consists of fixed costs plus variable

costs times volume.

B) The break-even quantity will increase when the change in variable cost per unit is identical to the

change in unit price.

C) Increasing the price, while keeping the variable cost per unit constant, increases the break-even

quantity.

D) Increasing the fixed costs tends to decrease the break-even quantity.

7) Which condition would result in invalidating an application of break-even analysis?

A) The variable cost to produce a unit is less than one percent of the fixed cost to run the plant.

B) The purchasing department both offers quantity discounts to customers and receives quantity

discounts from suppliers.

C) The variable cost to produce a unit is within one percent of the sale price.

D) The labor to manufacture the item is free.

8) Mantel Incorporated began producing its new line of dolls at its Connecticut plant in December of year

0. In year 1, it produced 30,000 dolls at a total cost of $385,000. In year 2, its production increased to 80,000

dolls at a total cost of $885,000. Assuming the cost structure was the same for both years, what must be

the variable cost (C) and the fixed cost (F) per doll?

A) F is less than $80,000, and C is greater than $7.

B) F is greater than $60,000, and C is less than $5.

C) F is less than $100,000, and C is greater than $9.

D) F is greater than $110,000, and C is less than $6.

9) The break-even quantity for a certain kitchen appliance is 6,000 units. The selling price is $10 per unit,

and the variable cost is $4 per unit. What must be the fixed cost to break even at 6,000 units?

A) less than $35,000

B) between $35,000 and $40,000

C) between $40,001 and $45,000

D) above $45,000

10) A “Little Sis” restaurant has been opened as a prototype to test the concept of a smaller facility with a

limited menu. Experience during the first two years was as follows:

The average sale is $10 per customer. Use the following partially completed graph to determine the

break-even quantity graphically. Then refine your solution by solving it algebraically.

A) The break-even quantity is fewer than or equal to 30,000 customer visits.

B) The break-even quantity is more than 30,000 customer visits and fewer than or equal to 50,000 visits.

C) The break-even quantity is more than 50,000 visits and fewer than or equal to 70,000 visits.

D) The break-even quantity is more than 70,000 customer visits.

11) Minor Video has opened a new store renting videocassettes. Fixed costs are $60,000, and the variable

cost per unit is $1.50. The average sale is $5 per customer. Use the following axes to determine the break–

even quantity graphically. Next, refine your solution by solving it algebraically.

A) The break-even quantity is fewer than or equal to 10,000 rentals.

B) The break-even quantity is more than 10,000 rentals and fewer than or equal to 20,000 rentals.

C) The break-even quantity is more than 20,000 rentals and fewer than or equal to 25,000 rentals.

D) The break-even quantity is more than 25,000 rentals.

12) In the hipster-beekeeper’s equation, 40 represents the:

A) variable cost.

B) fixed cost.

C) profit.

D) revenue.

13) In the hipster-beekeeper’s equation, 5 represents the:

A) variable cost.

B) fixed cost.

C) sales price.

D) per hive profit.

14) What is the total cost if the beekeeper keeps 8 hives?

A) $0

B) $40

C) $5

D) cannot be determined

15) Commodore is debating whether to produce the printed circuit boards for a new line of video

cameras or outsource their production to a company that specializes in this operation. Strictly from a cost

standpoint, production of the circuit boards would definitely be outsourced if:

A) the variable cost of producing the circuit boards is lower than the buy option.

B) the production volumes are greater than Commodore’s break-even quantity.

C) the production volumes are less than Commodore‘s break-even quantity.

D) the production volumes are the same for making and buying the circuit boards.

16) A poultry farmer is debating whether to acquire Rhode Island Reds or Buff Orpingtons to lay the eggs

he wants to sell. The fixed costs for the Buffs would be $7,500 and the variable costs per egg would be a

dime per egg. The Reds would have a fixed cost of $6,000 and a variable cost of fifteen cents. At what

level of egg production would the poultry farmer be indifferent between Rhode Island Reds and Buff

Orpingtons?

A) 20,000 eggs

B) 30,000 eggs

C) 50,000 eggs

D) 60,000 eggs

17) Zipco is in serious negotiations to purchase a chunking machine that will enable them to perform

their own chunking at $1 per unit. They currently have their chunking outsourced at a cost of $1.50 per

unit and a fixed cost of $45,000. Their marketing team feels that they can sustain an annual volume of

10,000 units. What is the maximum fixed cost that Zipco should be willing to bear in order to perform

their own chunking?

A) $50,000

B) $45,000

C) $40,000

D) $35,000

18) Demron is in serious negotiations to purchase a welding machine that will enable them to perform

their own welding. They currently have their welding outsourced at a cost of $1.50 per weld and a fixed

cost of $45,000. Their marketing team feels that they can sustain an annual sales volume sufficient to

require 35,000 welds. If a fancy new welding rig costs $13,500 what is the maximum variable cost per

weld that Demron should be willing to pay in order to bring this process in-house?

A) $3.00 per weld

B) $2.40 per weld

C) $2.00 per weld

D) $1.45 per weld

8

Copyright © 2019 Pearson Education, Inc.

Use this scenario to answer the following questions.

A company must decide if it will make or buy an item it needs. The company can make the item for $10

per unit, but must invest $15,000 in tooling to achieve that capability. Alex Rogo has quoted a total price

of $12 per unit to supply the quantity required (assume their fixed costs are included in the quoted price).

19) Refer to the instruction above. What is the break-even quantity in this situation?

A) 6,500 units

B) 7,000 units

C) 7,250 units

D) 7,500 units

20) Refer to the instruction above. Which alternative should be selected if annual requirements are 5,000

units?

A) Make

B) Buy

C) Either Make or Buy; costs are the same for either option at 5,000 units.

D) Can’t be determined with information given

21) Refer to the instruction above. What does the company save for the year by selecting this low-cost

option (for annual requirements of 5,000 units)?

A) $15,000

B) $60,000

C) $65,000

D) $5,000

Use the following to answer the questions below.

A company is considering two suppliers for the purchase of a part needed for manufacturing. Particulars

are as follows:

SUPPLIER A:

Fixed Costs = $9,000 / year

Variable Cost / Unit = $2

SUPPLIER B:

Fixed Costs = $3,000 / year

Variable Cost / Unit = $5

22) Refer to the instruction above. What is the annual break-even quantity for choosing between the two

suppliers?

A) 1,000 units

B) 2,000 units

C) 6,000 units

D) 12,000 units

23) Refer to the instruction above. For an annual volume of 3,000 units, which supplier should be chosen?

A) Supplier A

B) Supplier B

C) Either Supplier A or Supplier B, because costs are the same for either option at 3,000 units

D) Can’t be determined with information given

24) Refer to the instruction above. What does the company save for the year by selecting this low-cost

option (for annual requirements of 3,000 units)?

A) $1,000

B) $3,000

C) $6,000

D) $5,000

Use the following information to answer the questions below.

You currently make a part for old equipment at a cost of $20 / unit. The annual fixed cost for this

equipment is $50,000. You have found an outside supplier who will make the part for $15 / unit if you

will pay their annual fixed costs of $200,000 / year (see table).

ALTERNATIVE

FIXED COST

VARIABLE COST

Buy

$200,000 per year

$15 per unit

Make

$50,000 per year

$20 per unit

25) Refer to the instruction above. What is the break even quantity between buying and making?

A) 30,000 units per year

B) 40,000 units per year

C) 50,000 units per year

D) 60,000 units per year

26) Refer to the instruction above. What are total costs to buy an annual quantity of 40,000 units?

A) $400,000

B) $500,000

C) $800,000

D) $850,000

27) Refer to the instruction above. What are total costs to make a quantity of 40,000 units per year?

A) $400,000

B) $450,000

C) $800,000

D) $850,000

28) Refer to the instruction above. For what range of output would you prefer to buy?

A) 0 – 30,000 units per year

B) 30,000 or more units per year

C) 40,000 or more units per year

D) 0 – 40,000 units per year

29) Refer to the instruction above. For what range of output would you prefer to make?

A) 30,000 or more units per year

B) 0 – 30,000 units per year

C) 0 – 40,000 units per year

D) 40,000 or more units per year

30) Refer to the instruction above. What does the company save for the year by selecting the low-cost

option (for annual requirements of 40,000 units)?

A) $150,000

B) $300,000

C) $50,000

D) $40,000

12

Copyright © 2019 Pearson Education, Inc.

Use the following to answer the questions below.

A proposal for implementing a new product line has an annual fixed cost of $60,000, variable cost of $35

per unit of output, and revenue (selling price) of $55 per unit of output.

31) Refer to the instruction above. What is the break-even quantity?

A) 2,000 units per year

B) 3,000 units per year

C) 6,000 units per year

D) 20,000 units per year

32) Refer to the instruction above. What volume of output will be necessary for an annual profit of

$60,000?

A) 2,000 units

B) 3,000 units

C) 6,000 units

D) 20,000 units

33) Refer to the instruction above. What selling price would be necessary to generate an annual profit of

$90,000, if expected volume is 6,000 units per year (assume fixed costs remain at $60,000, and variable cost

per unit at $35)?

A) $30 / unit

B) $40 / unit

C) $50 / unit

D) $60 / unit

34) The ________ is the volume at which total revenues equal total costs.

35) ________ is the portion of total cost that remains constant regardless of changes in levels of output.

36) ________ is a technique for systematically changing parameters in a model to determine the effects of

such changes.

37) What assumptions are made when using break-even analysis?

38) Why should a decision maker engage in sensitivity analysis?

39) A single factory produces two different products during each half of the year with equivalent fixed

cost; from January through June they produce Product A and from July through December they produce

Product B. Product A costs twice as much to produce and is sold at twice the price of Product B. Derive

an expression relating the break-even quantity of Product A to that of Product B.

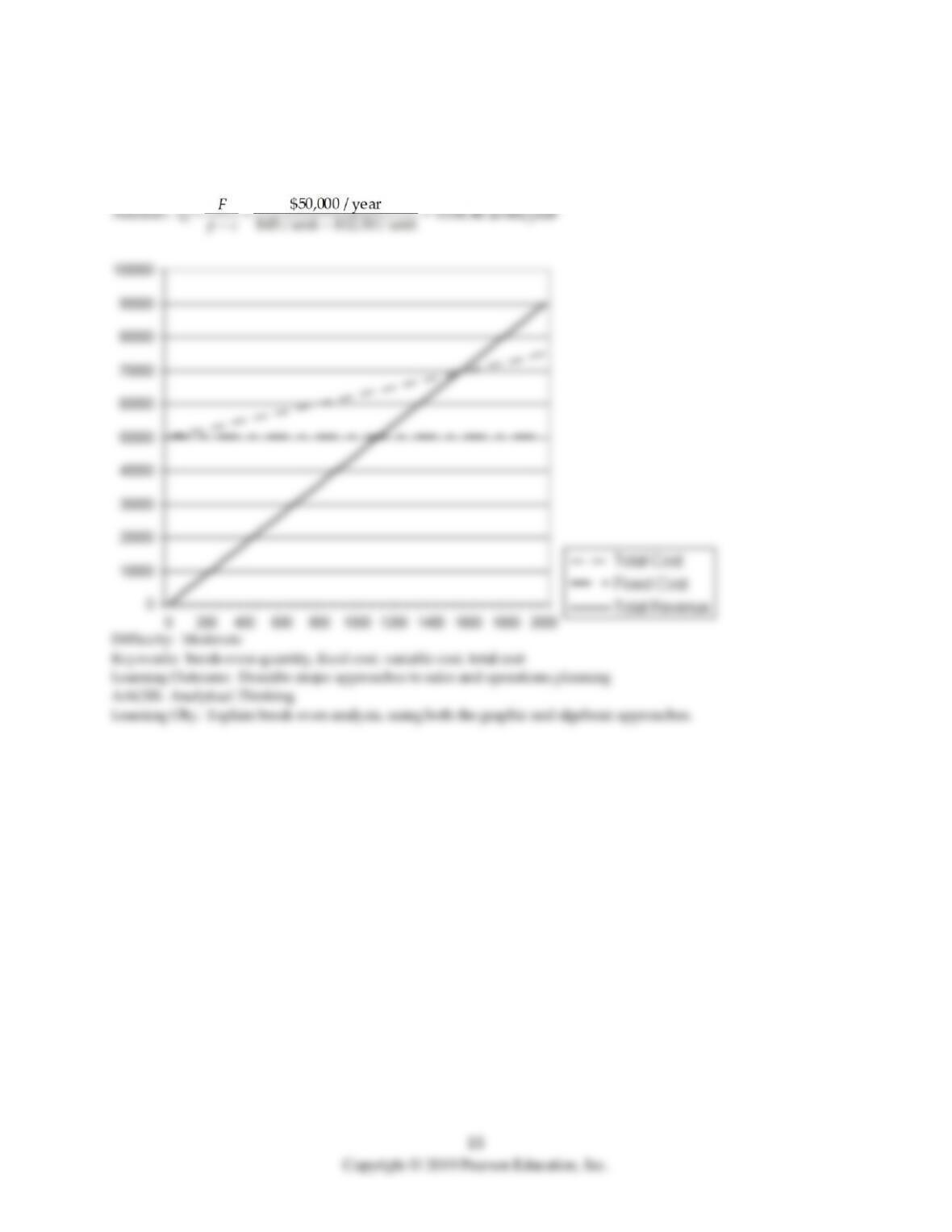

40) A manufacturing firm is considering an entirely new product that will require additional capital

equipment, training, and an addition to their existing facility that will cost $50,000 per year. The projected

retail price is $45 per unit, and the variable cost of production is $12.50. What is the break-even for this

product? Solve using both the graphical and algebraic approaches.

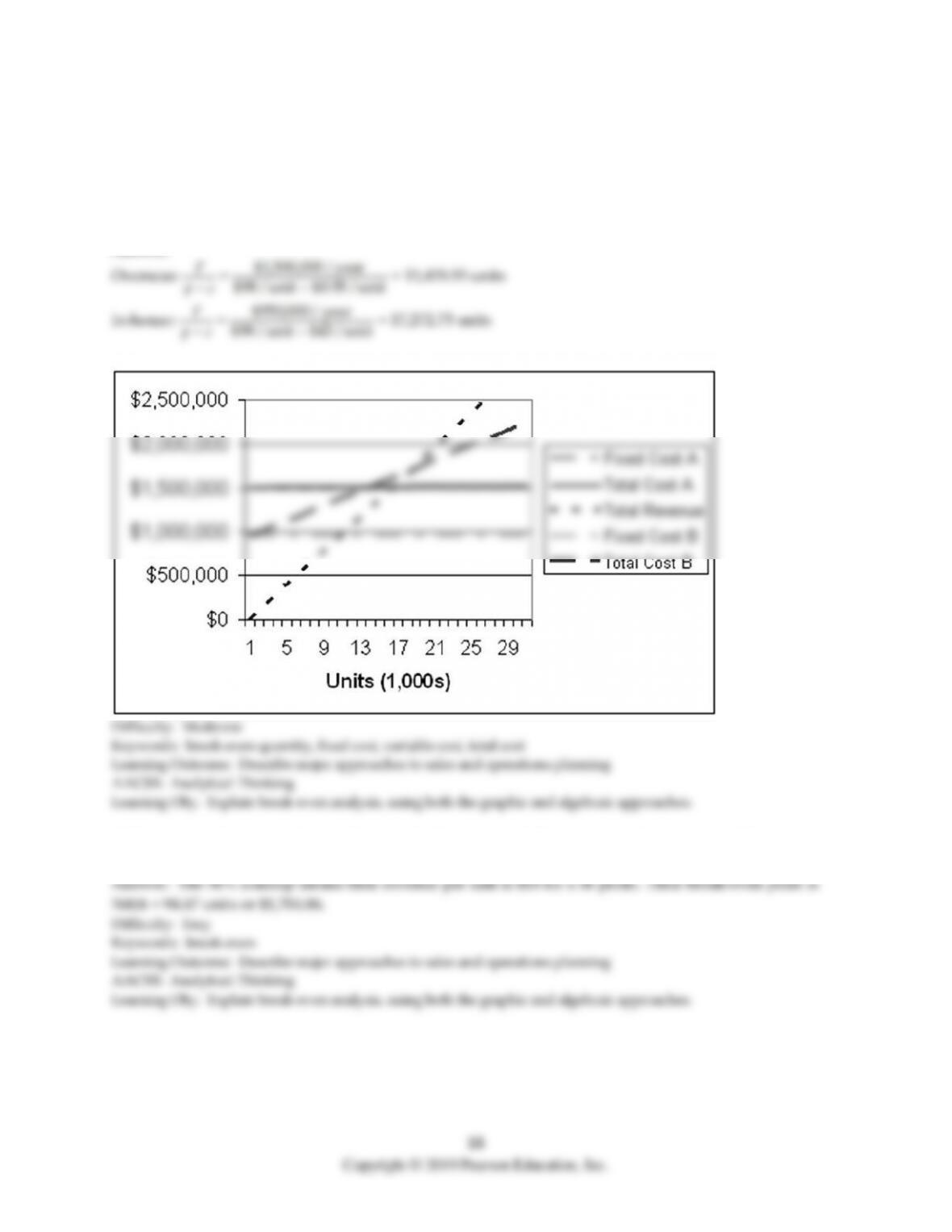

41) A manufacturing firm is considering whether to produce or outsource the production of a new

product. If they produce the item themselves, they will incur a fixed cost of $950,000 per year, but if they

outsource overseas there will be a $1.5 million cost per year. The advantage of outsourcing overseas is the

variable cost of 95¢ per unit, which is a fraction of their $43/unit cost in their own union shop. Regardless

of where these devices are made, they will sell for $98 each. What is the break-even quantity for each

alternative? Solve this problem graphically and algebraically.

Answer:

42) A company faces a fixed cost of $568 and sells items at a 50% markup on their cost of $12. What is

their break-even point in both units and dollar sales?

43) Pops has a cost function of 3x2-25x + 34,374.74 and a revenue function of 5x2. Using Excel (or algebra),

determine a break-even point. What is their fixed cost? What is their break-even point in both units and

dollar sales?

1) A preference matrix is a table that allows the manager to rate an alternative according to one

performance criterion.

2) The preference matrix technique can be used only with quantitative factors to consider.

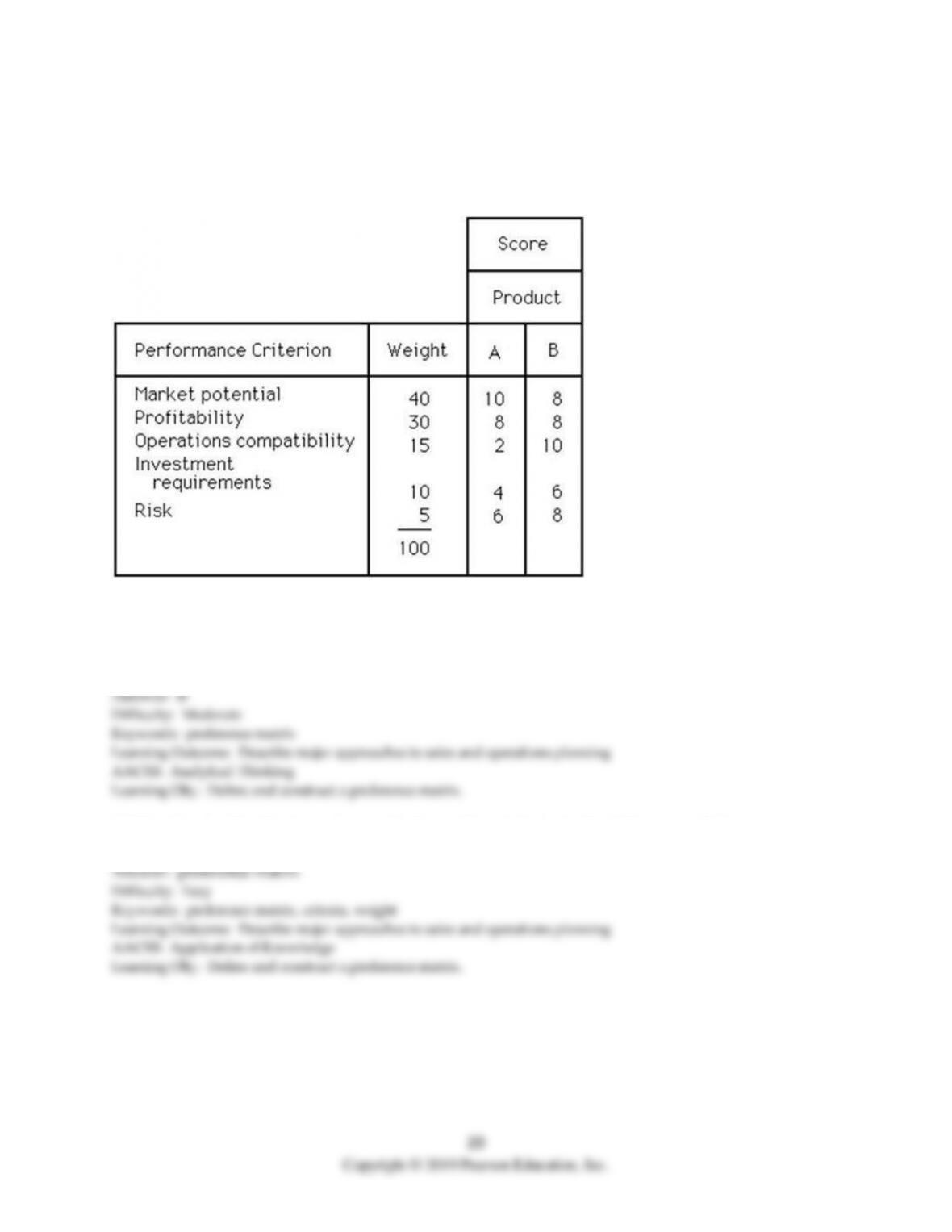

3) A company is screening ideas for new services. Five alternative service ideas are being considered.

Management identified four criteria and weighted them as follows: A = 30, B = 10, C = 20, and D = 40.

They have also come up with scored values for the five alternatives and the four criteria as shown below.

Management has decided that if an alternative has less than a total scored value of 600, it should

automatically be rejected. Use the preference matrix technique to determine which idea should be

accepted.

A) service #1 or #2

B) service #3 or #4

C) service #5

D) none

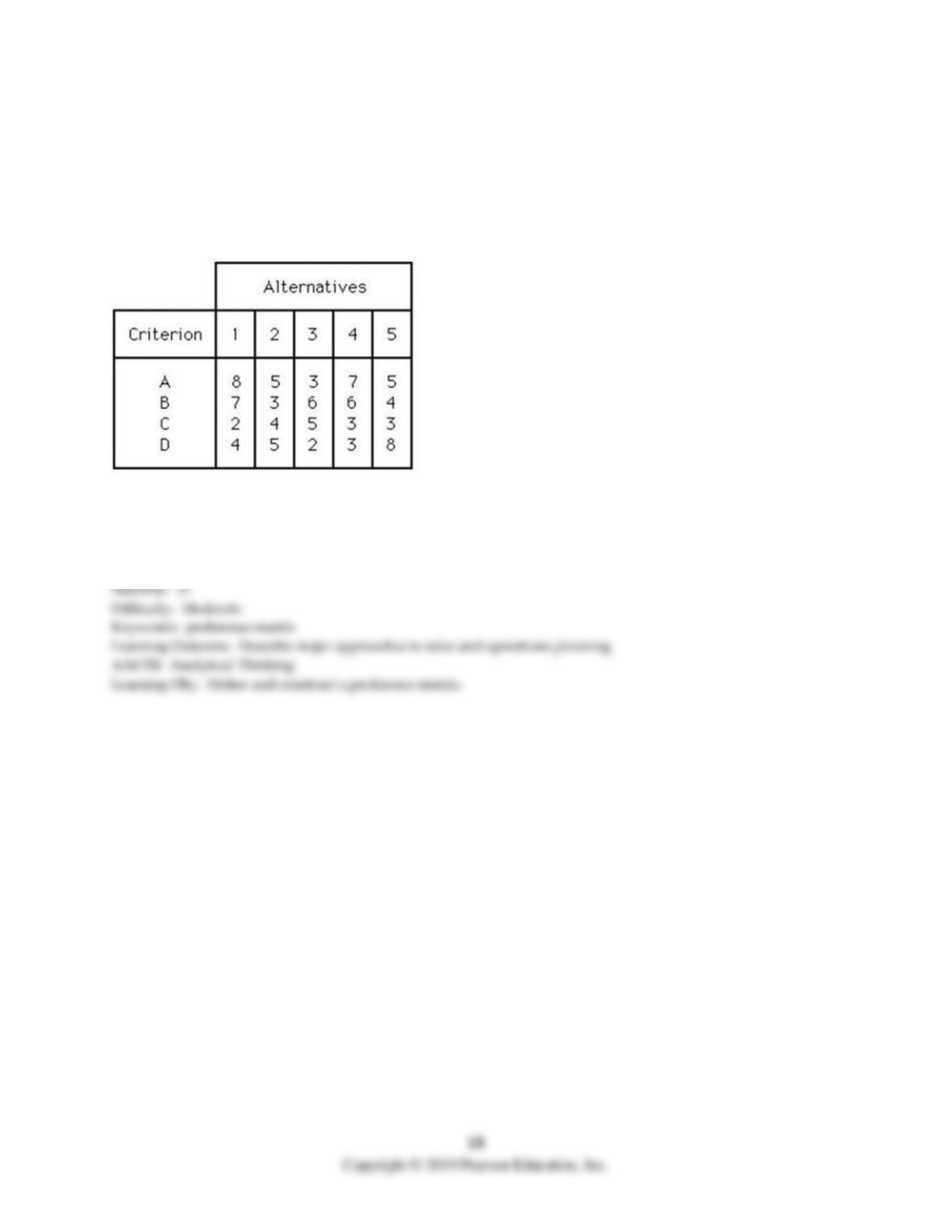

4) The Forsite Company is screening three new product ideas. Resource constraints allow only one idea to

be commercialized at the present time. The following estimates have been made for the five performance

criteria that management feels are most important. If the five criteria are equally weighted, what are the

best and worst alternatives?

A) A is best, and B is worst.

B) B is best, and C is worst.

C) B is best, and A is worst.

D) C is best, and A is worst.

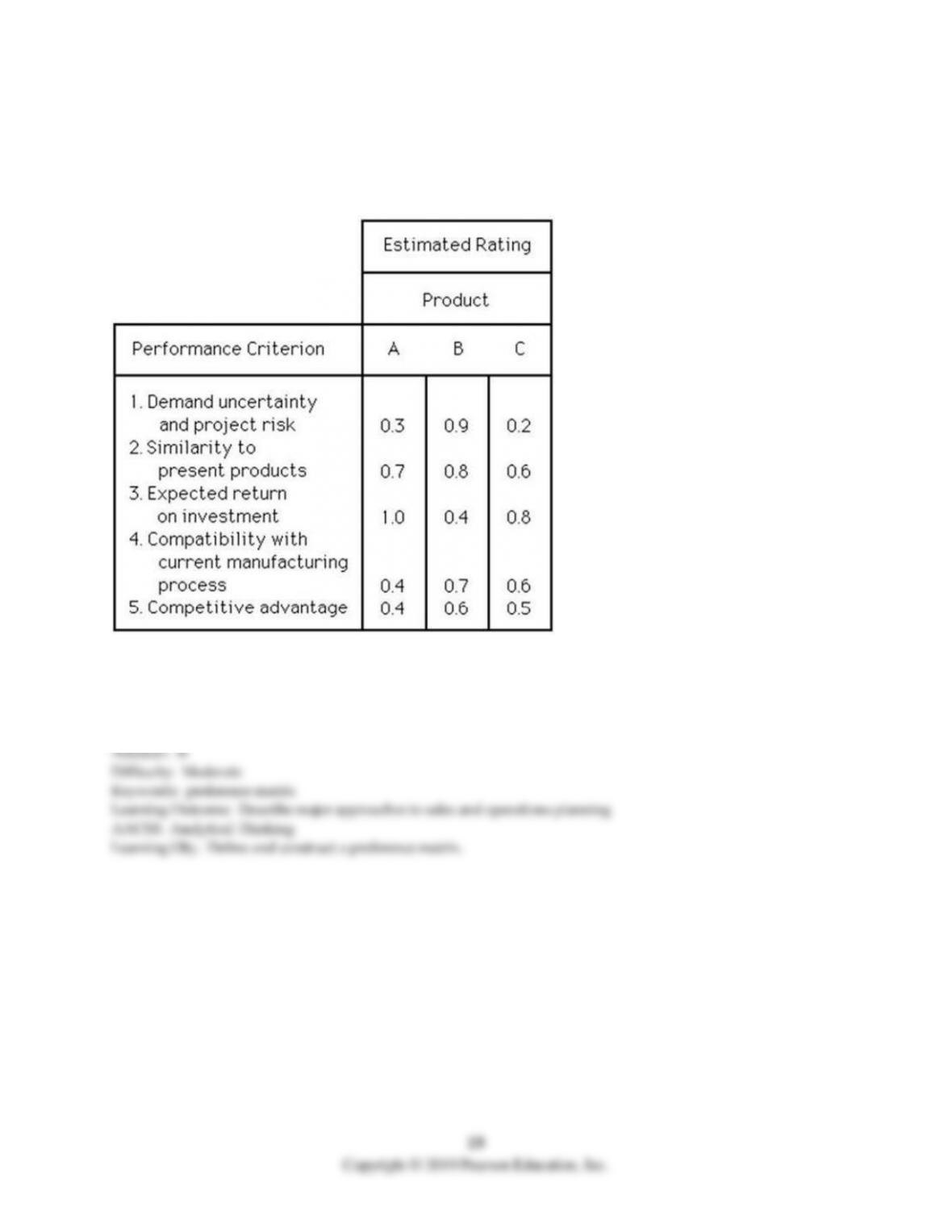

5) California Manufacturing, Inc. is now evaluating two new product ideas, and management has

decided to apply the preference matrix method. The following table shows five criteria with different

weights and individual scores of each product idea. If management has established a threshold of 800,

which product(s) should be accepted for further development?

A) product A

B) product B

C) Both products A and B

D) Neither product A nor B

6) When faced with a decision where multiple non-financial criteria should be assessed, the savvy

manager should employ a(n) ________ as a decision tool.