Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

Copyright © 2011 Pearson Education, Inc.

Foundations of Microeconomics, 5e (Bade/Parkin)

Chapter 14 Perfect Competition

14.1 A Firm's Profit-Maximizing Choices

1) A market with a large number of sellers

A) can only be a perfectly competitive market.

B) might be an oligopoly or a perfectly competitive market.

C) might be a monopolistically competitive or a perfectly competitive market.

D) might be a perfectly competitive, monopolistically competitive, oligopoly, or monopoly

market.

E) can only be a monopolistically competitive market.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

2) What is the difference between perfect competition and monopolistic competition?

A) Perfect competition has a large number of small firms while monopolistic competition does

not.

B) Perfect competition has barriers to entry while monopolistic competition does not.

C) Perfect competition has no barriers to entry, while monopolistic competition does.

D) In perfect competition, firms produce identical goods, while in monopolistic competition,

firms produce slightly different goods.

E) In monopolistic competition, firms produce identical goods, while in perfect competition,

firms produce slightly different goods.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

3) A perfectly competitive firm

A) sells a product that has perfect substitutes.

B) has a perfectly inelastic demand.

C) has a perfectly elastic supply.

D) Answer A and answer B are correct.

E) Answer A and answer C are correct.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

2

Copyright © 2011 Pearson Education, Inc.

4) In which market structure do firms exist in very large numbers, each firm produces an

identical product, and there is freedom of entry and exit?

A) monopoly

B) oligopoly

C) only perfect competition

D) only monopolistic competition

E) either perfect competition or monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

5) The characteristics that describe a perfectly competitive industry include

A) many firms selling an identical product.

B) one firm selling to many buyers.

C) many firms selling a slightly differentiated product.

D) a few firms selling to many buyers.

E) None of the above answers is correct.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

6) In part, perfect competition arises if

i. each firm's minimum efficient scale is large relative to demand.

ii. each firm produces a good or service identical to those produced by its many competitors.

iii. there are significant barriers to entry.

A) i only

B) ii only

C) i and ii

D) iii only

E) ii and iii

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

3

Copyright © 2011 Pearson Education, Inc.

7) In which of the following market types do all firms sell products so identical that buyers do

not care from which firm they buy?

A) perfect competition

B) monopolistic competition

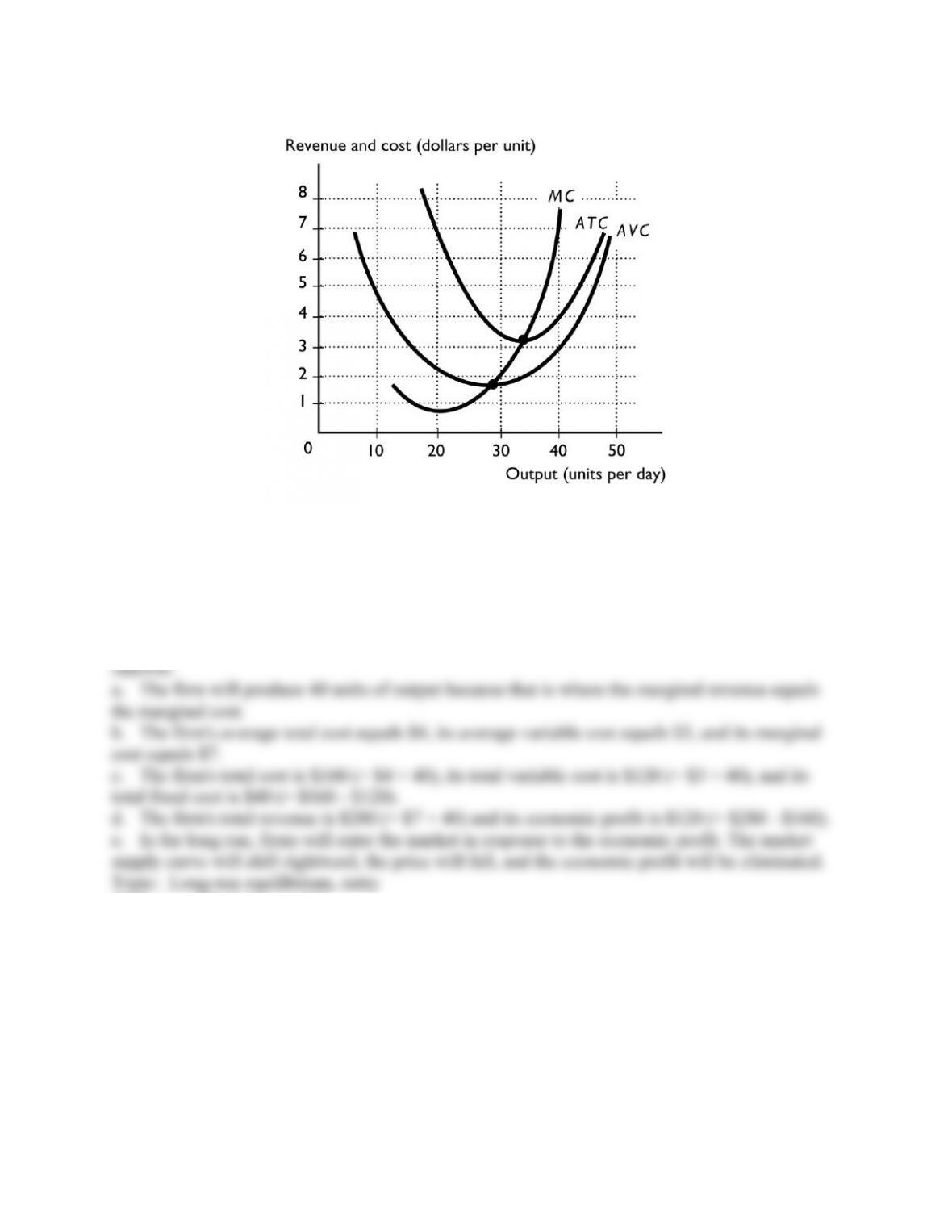

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

8) A market in which many firms sell identical products is

A) a monopoly.

B) an oligopoly.

C) perfectly competition.

D) monopolistic competition.

E) perfect competition and monopolistic competition.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: MR

AACSB: Reflective thinking

9) One requirement for an industry to be perfectly competitive is that in the industry there

A) are a few firms who control the market.

B) are many firms for whom the efficient scale of production is small.

C) is one firm that sells a product with no close substitutes.

D) are many firms selling different products.

E) is a barrier to entry that makes the entry of new firms difficult.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

4

Copyright © 2011 Pearson Education, Inc.

10) One requirement for an industry to be perfectly competitive is that

A) there are no restrictions on entry into or exit from the market.

B) there are multiple restrictions on entry into or exit from the market.

C) there are many firms selling different products.

D) sellers and buyers have imperfect information about prices.

E) the many firms sell slightly different products.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

11) One requirement for an industry to be perfectly competitive is that

A) sellers and buyers have imperfect information about prices.

B) established firms have no advantage over new firms.

C) established firms have a significant advantage over new firms.

D) different firms produce widely different products.

E) many firms produce slightly different products.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

12) A perfectly competitive market arises when

A) the market demand is small relative to the output of a firm.

B) there are many buyers but few sellers.

C) the market demand is very large relative to the output of one seller.

D) a firm has control over a unique resource.

E) each of the many firms produces a slightly different product.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

5

Copyright © 2011 Pearson Education, Inc.

13) Each firm in a perfectly competitive industry

A) produces a good that is slightly different from that of the other firms.

B) produces a good that is identical to that of the other firms.

C) attains economies of scale so that its efficient size is large compared to the market as a whole.

D) has control over at least one unique resource to separate themselves from their competitors.

E) has an important influence on the market price of the good or service being produced.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

14) Perfect competition is characterized by all of the following EXCEPT

A) a large number of buyers and sellers.

B) no restrictions on entry into or exit from the industry.

C) considerable advertising by individual firms.

D) buyers and sellers are well informed about prices.

E) firms produce an identical product.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

15) Which of the following is the best example of a perfectly competitive market?

A) farming

B) diamonds

C) athletic shoes

D) soft drinks

E) electricity distribution

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

6

Copyright © 2011 Pearson Education, Inc.

16) Which of the following market types has the fewest number of firms?

A) perfect competition

B) monopolistic competition

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

17) A monopoly occurs when

A) each of many firms produces a product that is slightly different from that of the other firms.

B) one firm sells a good that has no close substitutes and a barrier blocks entry for other firms.

C) there are many firms producing the same product.

D) a few firms control the market.

E) one firm is larger than the many other firms that make an identical product.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

18) In which market structure does one firm sell a good or service with no close substitutes and

there is a barrier blocking the entry of new firms?

A) only monopoly

B) only oligopoly

C) perfect competition

D) monopolistic competition

E) either monopoly or oligopoly

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

7

Copyright © 2011 Pearson Education, Inc.

19) When one firm sells a good or service that has no close substitutes and a barrier blocks the

entry of new firms, what type of market is this?

A) perfect competition

B) only monopoly

C) oligopoly

D) only monopolistic competition

E) either monopoly or monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

20) ________ a large number of firms competing by making similar but slightly different

products.

A) Monopoly requires

B) Perfect competition requires

C) Monopolistic competition requires

D) Oligopoly requires

E) Both perfect competition and monopolistic competition require

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

21) A market is classified as monopolistically competitive when

A) there is a barrier that blocks entry by other firms.

B) a small number of firms compete.

C) many firms produce the same product.

D) many firms produce a slightly differentiated product.

E) there is one firm that sells a good or service with no close substitutes.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

8

Copyright © 2011 Pearson Education, Inc.

22) In which market structure is there a large number of firms producing slightly differentiated

products?

A) monopoly

B) oligopoly

C) only perfect competition

D) only monopolistic competition

E) either perfect competition or monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

23) A market is classified as an oligopoly when

A) a few firms compete.

B) many firms produce a slightly differentiated product.

C) no matter how many firms are in the market, a barrier blocks entry by other new firms.

D) many firms produce the same product.

E) only one firm sells a product with no close substitutes.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

24) Which of the following market types has only a few competing firms?

A) perfect competition

B) monopolistic competition

C) oligopoly

D) monopoly

E) perfect competition and monopolistic competition

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

9

Copyright © 2011 Pearson Education, Inc.

25) In which market structure are there a small number of firms competing?

A) only monopoly

B) only oligopoly

C) perfect competition

D) monopolistic competition

E) either monopoly or oligopoly

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

26) A market is ________ when a small number of firms compete.

A) a monopoly

B) perfectly competitive

C) monopolistically competitive

D) an oligopoly

E) either monopolistically competitive or an oligopoly

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

27) The firm's over-riding objective is to

A) earn a normal profit.

B) maximize normal profit.

C) maximize economic profit.

D) maximize total revenue.

E) avoid an economic loss.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

10

Copyright © 2011 Pearson Education, Inc.

28) Normal profit is

A) the same thing as economic profit.

B) the return to entrepreneurship.

C) total revenue minus the total opportunity cost of production.

D) the point of profit when total revenue is maximized.

E) part of the firm's total revenue.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

29) In a perfectly competitive market, the type of decision a firm has to make is different in the

short run than in the long run. Which of the following is an example of a perfectly competitive

firm's short-run decision?

A) the profit-maximizing level of output

B) how much to spend on advertising and sales promotion

C) what price to charge buyers for the product

D) whether or not to enter or exit an industry

E) whether or not to change its plant size

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

30) To maximize its profit, in the short run a perfectly competitive firm decides

A) what price to charge for its product.

B) what quantity of output to produce.

C) whether to exit the market.

D) whether to increase the size of its plant.

E) how much advertising it should undertake.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

11

Copyright © 2011 Pearson Education, Inc.

31) A perfectly competitive firm can

A) sell all of its output at the prevailing market price.

B) set a higher price to customers who are willing to pay more.

C) raise its price in order to increase its total revenue.

D) sell additional output only by lowering its price.

E) usually not sell all the output it produces, but still "over-produces" because there are some

periods when it can sell the extra output at very profitable prices.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

32) In a perfectly competitive market, one farmer's barley is

A) completely different from another farmer's barley.

B) a perfect substitute for another farmer's barley.

C) a monopolized product in that farmer's local market.

D) a monopolized product in the national market.

E) slightly different from another farmer's barley.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

33) A firm in perfect competition is a price taker because

A) there are no good substitutes for its good.

B) many other firms produce identical products.

C) it is very large.

D) its demand curves are downward sloping.

E) it's demand curve is vertical at the profit-maximizing quantity.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

12

Copyright © 2011 Pearson Education, Inc.

34) The price charged by a perfectly competitive firm is

A) the same as the market price.

B) different than the price charged by competing firms.

C) lower the more the firm produces.

D) higher the more the firm produces.

E) indeterminate.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

35) For a perfectly competitive firm, the price of its good is equal to the firm's marginal revenue

because

A) information about price changes is hard to come by for small sellers.

B) price and marginal revenue are the same economic concepts.

C) individual perfectly competitive firms cannot influence the market price by changing their

output.

D) the firm's total revenue cannot be changed by anything the firms can do.

E) there are only a small number of firms in the market.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SA

AACSB: Analytical reasoning

36) A large number of sellers all selling an identical product implies which of the following?

A) market chaos

B) the inability of any seller to change the price of the product

C) large losses incurred by all sellers

D) horizontal market supply curves

E) vertical market supply curves

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

13

Copyright © 2011 Pearson Education, Inc.

37) A firm that is a price taker faces

A) an elastic supply curve.

B) an inelastic supply curve.

C) a perfectly elastic demand curve.

D) a perfectly inelastic demand curve.

E) an elastic but not perfectly elastic demand curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

38) Suppose Pat's Paints is a perfectly competitive firm. If Pat's Paints' marginal revenue equals

$5 per can, and Pat decides to sell 100 cans of paint, Pat's total revenue equals

A) $5.

B) $100.

C) $500.

D) $20.

E) Information on the price of a can of paint is needed to answer the question.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Analytical reasoning

39) If demand for a seller's product is perfectly elastic, which of the following is true?

i. The firm will sell no output if it sets the price its product above the market price.

ii. There are many perfect substitutes for the seller's product.

iii. The firm will sell no output if it sets the price its product below the market price.

A) i only

B) ii only

C) iii only

D) i and ii

E) ii and iii

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

14

Copyright © 2011 Pearson Education, Inc.

40) A perfectly competitive firm's demand curve is horizontal because

i. the firm is so small, relative to the market, that it cannot affect the market price.

ii. there are many perfect substitutes for its product.

iii. the firm cannot sell any output at a price higher than the market price.

A) ii only

B) i and ii

C) iii only

D) i and iii

E) i, ii, and iii

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

41) Cynthia is an Oklahoma wheat farmer. The demand for her wheat is

A) perfectly inelastic.

B) inelastic but not perfectly inelastic.

C) elastic but not perfectly elastic.

D) perfectly elastic.

E) unit elastic.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

42) Because perfectly competitive firms are price takers, each firm faces a demand that is

A) perfectly inelastic.

B) perfectly elastic.

C) highly inelastic but never is it perfectly inelastic.

D) unit elastic.

E) highly elastic but never is it perfectly elastic.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

15

Copyright © 2011 Pearson Education, Inc.

43) If a perfectly competitive firm raised the price of its product,

A) its profits would increase.

B) the quantity of output it sells decreases to zero.

C) rival firms will follow suit and raise their prices also.

D) the firm will be forced to advertise more.

E) its total revenue would rise but its total cost would rise by more.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

44) If the wheat industry is perfectly competitive with a market price of $4 per bushel and

Farmer Brown charged $5 per bushel, how many bushels would Farmer Brown sell?

A) some, but fewer than he would at a price of $4

B) more than he would at a price of $4

C) just as many as he would at a price of $4

D) none

E) More information is needed about the prices charged by the other wheat farmers.

Skill: Level 4: Applying models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

45) How does the demand for any one seller's product in perfect competition compare to the

market demand for that product?

A) They are identical.

B) The demand for any one seller is proportionally smaller but otherwise identical to the market

demand.

C) The demand for any one seller's product is perfectly elastic while the market demand curve is

downward sloping.

D) There is no demand for any one seller's competitively sold product.

E) The demand for any one seller's product is not perfectly elastic while the market demand is

perfectly elastic.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

16

Copyright © 2011 Pearson Education, Inc.

46) For the perfectly competitive broccoli producers in California, the market demand curve for

broccoli is

A) a horizontal line.

B) downward sloping.

C) nonexistent.

D) upward sloping.

E) the same as the demand curve each firm faces.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

47) The market demand curve in a perfectly competitive market is ________ and the demand

curve for a perfectly competitive firm's output is ________.

A) downward sloping; downward sloping

B) downward sloping; horizontal

C) horizontal; downward sloping

D) horizontal; horizontal

E) downward sloping; upward sloping

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

48) Elsie is a perfectly competitive dairy farmer. If the market price of milk falls to $2.20 a

gallon from $2.40 a gallon, Elsie

A) can sell as much milk as she wants at $2.20 a gallon.

B) will have to charge some customers $2.40 a gallon to stay in business.

C) will produce the same amount of milk at both prices.

D) can sell more at the lower price because the quantity demanded is higher at lower prices.

E) will be able to charge her initial customers $2.40 a gallon.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

17

Copyright © 2011 Pearson Education, Inc.

49) For a perfectly competitive palm tree nursery in South Carolina, the total revenue curve is

A) downward sloping.

B) a horizontal line.

C) upward sloping.

D) U-shaped.

E) undefined because the firm is perfectly competitive.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

50) If the market price of a product is $14 and all sellers are price takers, then which of the

following is correct?

A) Each seller's total revenue line is graphed as an upward-sloping straight line.

B) The demand curve for each seller's product is a downward-sloping straight line.

C) Each seller can earn more total revenue by raising the price he or she charges above $14.

D) The demand curve for each seller's product is a downward-sloping but not necessarily a

straight line.

E) Each seller's total revenue is graphed as an upside-down U-shaped curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

51) Marginal revenue is

A) the change in total revenue from a one-unit increase in the quantity sold.

B) another name for total revenue.

C) the change in total cost from producing an additional unit of output.

D) the economic profit from producing an additional unit of output.

E) less than price for a perfectly competitive firm.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

18

Copyright © 2011 Pearson Education, Inc.

52) A firm's marginal revenue is

A) the change in total revenue that results from a one-unit increase in the quantity sold.

B) total revenue minus total cost.

C) the change in total revenue minus the change in total cost.

D) the change in total revenue that results from an increase in the demand for the good or

service.

E) less than the market price for a perfectly competitive firm.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

53) For a perfectly competitive firm, marginal revenue is

A) less than the price.

B) greater than the price.

C) equal to the price.

D) equal to the change in profit from selling one more unit.

E) undefined because the firm's demand curve is horizontal.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

54) In perfect competition, marginal revenue

A) increases as more is sold.

B) decreases as more is sold.

C) is equal to the market price.

D) is zero.

E) is always greater than marginal cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

19

Copyright © 2011 Pearson Education, Inc.

55) For a perfectly competitive firm, the market price of a good is

A) a given which the firm cannot change.

B) determined by the firm in order to maximize its profit.

C) equal to the firm's marginal revenue.

D) Answer A and answer B are correct.

E) Answer A and answer C are correct.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

56) The marginal revenue curve for a perfectly competitive firm is

A) horizontal.

B) vertical.

C) upward sloping.

D) downward sloping.

E) a straight line coming out of the origin with a 45 degree slope.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

20

Copyright © 2011 Pearson Education, Inc.

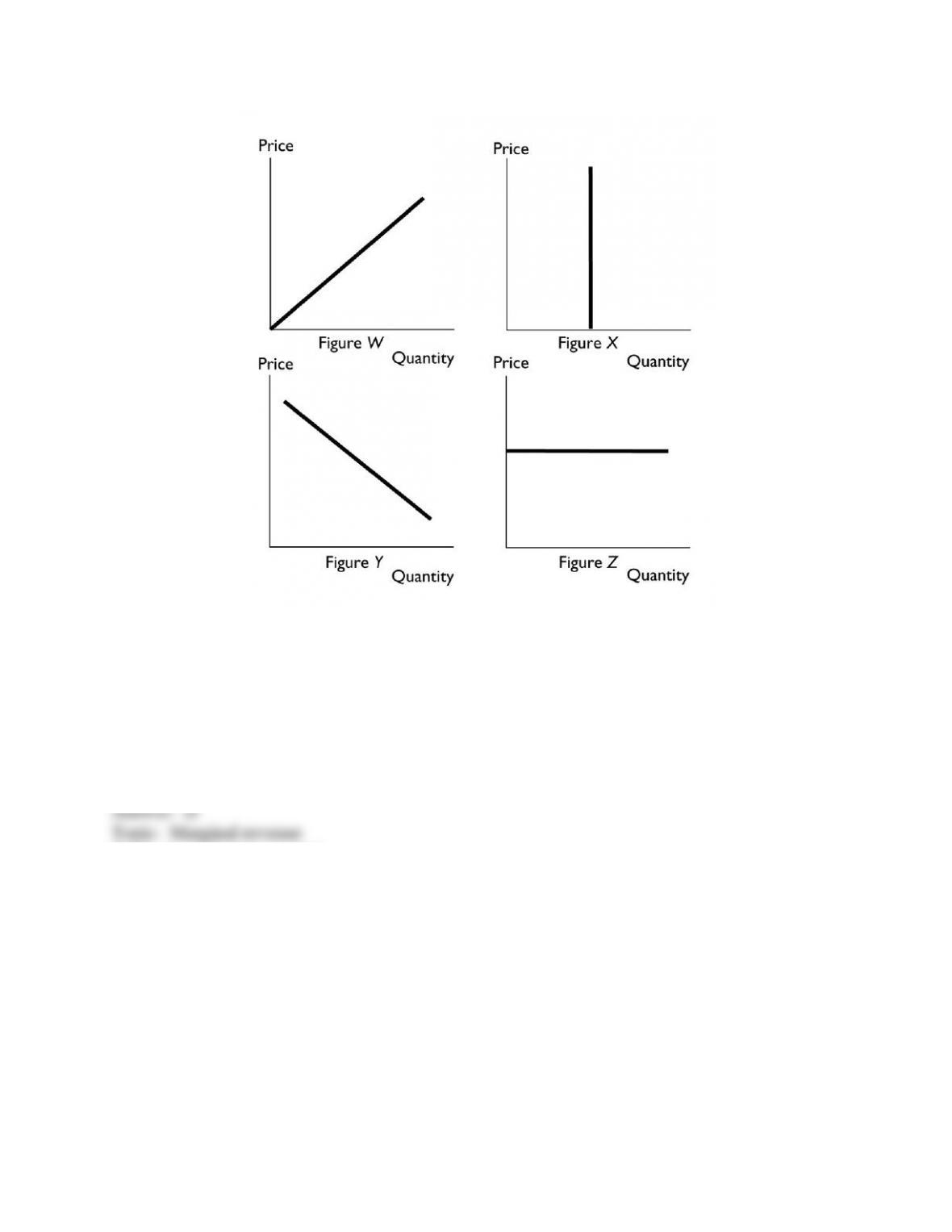

57) In the above, a marginal revenue curve for a perfectly competitive firm is shown in Figure

________.

A) W

B) X

C) Y

D) Z

E) X and Figure Z

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Analytical reasoning

21

Copyright © 2011 Pearson Education, Inc.

58) As a perfectly competitive firm produces more and more of a good, its economic profit

A) constantly increases.

B) constantly decreases.

C) first decreases, then increases.

D) first increases, then decreases.

E) does not change.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Analytical reasoning

59) As a perfectly competitive firm's output increases, its total revenue ________ and its total

cost ________.

A) increases; increases

B) increases; decreases

C) decreases; increases

D) decreases; decreases

E) does not change; increases

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

60) In a perfectly competitive industry, when a firm is producing so that its total revenue equals

its total cost, the firm is

A) earning an economic profit.

B) incurring an economic loss.

C) earning zero economic profit, that is, earning a normal profit.

D) definitely not maximizing its profit.

E) None of the above answers is correct because the relationship between total revenue and total

cost has nothing to do with the firm's profit or loss.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: PH

AACSB: Reflective thinking

22

Copyright © 2011 Pearson Education, Inc.

61) For a syrup producer in central Vermont, profit is maximized at the level of output for which

total

A) revenue exceeds total cost by the largest amount.

B) revenue exceeds total cost by the smallest amount.

C) revenue is maximized.

D) cost is minimized.

E) revenue equals total cost.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

62) A firm maximizes its profit by producing the amount of output such that

A) marginal revenue equals marginal cost.

B) marginal revenue exceeds marginal cost by some amount.

C) marginal revenue is maximized.

D) marginal cost is minimized.

E) marginal revenue exceeds marginal cost by the maximum amount possible.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

63) For a perfectly competitive firm, profit maximization occurs when output is such that

A) total revenue (TR) is maximized.

B) total cost (TC) is minimized.

C) marginal revenue (MR) = marginal cost (MC).

D) average total cost (ATC) is minimized.

E) total revenue (TR) equals total cost (TC).

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

23

Copyright © 2011 Pearson Education, Inc.

64) A perfectly competitive firm will maximize profit when the quantity produced is such that

the

A) firm's total revenue is equal to total cost.

B) firm's marginal revenue is equal to the price.

C) firm's marginal revenue is equal to its marginal cost.

D) price exceeds the firm's marginal cost by as much as possible.

E) firm's marginal revenue exceeds its marginal cost by the maximum amount possible.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

65) For a perfectly competitive firm, profit is maximized at the output level where

i. total revenue exceeds total cost by the largest amount.

ii. marginal revenue equals marginal cost.

iii. price equals marginal cost.

A) i only

B) ii only

C) ii and iii

D) i and ii

E) i, ii, and iii

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

66) If a perfectly competitive wheat farmer is maximizing its profit and then increases its output,

the farmer's

A) total revenue increases, but total cost rises by more so that the farmer's total profit decreases.

B) total revenue decreases and total cost increases, both thereby decreasing the farmer's total

profit.

C) total revenue does not change but total cost increases, thereby decreasing the farmer's total

profit.

D) marginal revenue increases, but so does marginal cost so that the farmer's total profit

increases.

E) total revenue and total cost both rise but the effect on the farmer's total profit is uncertain.

Skill: Level 4: Applying models

Section: Checkpoint 14.1

Author: MR

AACSB: Reflective thinking

24

Copyright © 2011 Pearson Education, Inc.

67) To increase its profit, a perfectly competitive firm will produce more output when

A) price is greater than average fixed cost.

B) price is greater than marginal cost.

C) marginal cost is less than average total cost.

D) average variable cost is greater than average fixed cost.

E) price is greater than average variable cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

68) In a perfectly competitive market, the market price is $23. At the current level of output, a

firm has a marginal cost of $28. What should the firm do?

A) produce a larger output to earn more profit

B) nothing, it is currently maximizing profit

C) produce less output to earn more profit

D) shut down

E) raise the price of its product

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

69) A perfectly competitive firm is producing at the quantity where marginal cost is $6 and

average total cost is $4. The price of the good is $5. To maximize its profit, this firm should

A) raise its price.

B) lower its price.

C) increase its output.

D) decrease its output.

E) increase the price it charges for its product.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

25

Copyright © 2011 Pearson Education, Inc.

70) Suppose that a perfectly competitive firm's marginal revenue equals $12 when it sells 10

units of output. If the marginal cost of producing the 10th unit is $14, to maximize its profit the

firm should

A) do nothing because it is already maximizing its profit.

B) decrease its production.

C) increase its production.

D) shut down.

E) increase the price it charges for its product.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

71) Shama is producing candles in a perfectly competitive market. When she produces 500

candles, her total cost is $250. If she produces one additional candle, her total cost increases to

$260. In order to maximize her profit, she should produce the additional candle

A) if the market price for a candle is $12.

B) only if the market price exceeds $260 for a candle.

C) only if the market price exceeds $250 for a candle.

D) if the market price for a candle exceeds $0.50.

E) if her price exceeds her average total cost.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Analytical reasoning

72) Jennifer's Bakery Shop produces baked goods in a perfectly competitive market. If Jennifer

decides to produce her 100th batch of cookies, the marginal cost is $120. She can sell this batch

of cookies at a market price of $110. To maximize her profit, Jennifer should

A) not produce this additional batch.

B) produce this batch of cookies because they will help lower her average fixed cost.

C) charge $120 for this batch.

D) shut down.

E) produce this batch of cookies because their MR exceeds their MC.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Reflective thinking

26

Copyright © 2011 Pearson Education, Inc.

73) Henry, a perfectly competitive lime grower in Southern California, notices that the market

price of limes is greater than his marginal cost. What should Henry do?

A) expand his output to increase profits

B) shut down and incur a loss equal to his total fixed cost

C) advertise his limes to be able to sell more output

D) look for the output level where marginal revenue minus marginal cost is maximized

E) shut down and earn no profit but also incur no loss

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

74) Jerry's Jellybean Factory produces 2,000 pounds of jellybeans per month and sells them in a

perfectly competitive market. The marginal cost is $3 per pound, the average variable cost is $2

per pound, and the beans sell for $4 per pound. Jerry

A) is maximizing profit.

B) is incurring an economic loss and should shut down.

C) could increase his profit by producing more beans.

D) could increase his profit by producing fewer beans.

E) could increase his profit by raising the price of his beans.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SB

AACSB: Analytical reasoning

75) If a perfectly competitive firm's marginal revenue is greater than its marginal cost, as it

increases its output, its profit ________ and the price it can charge for its product ________.

A) increases; does not change

B) decreases; falls

C) increases; falls

D) decreases; rises

E) decreases; does not change

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

27

Copyright © 2011 Pearson Education, Inc.

76) Mark owns a cattle ranch near Hugo, Oklahoma. Mark is currently producing beef at an

output level where marginal revenue exceeds marginal cost. In order to maximize his profit,

Mark should

A) not change his output.

B) decrease his output.

C) increase his output.

D) shut down his ranch.

E) probably change his output, but more information is needed to determine if he should

increase, decrease, or not change it.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

77) During the winter, theme parks in Orlando close earlier than in the summer. The reason the

theme parks close early during the winter is because during that season the marginal revenue

from staying open later is ________ the marginal cost.

A) greater than

B) less than

C) equal to

D) zero compared to

E) not comparable to

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

78) A perfectly competitive firm is earning an economic profit when total fixed costs increase.

Assuming the firm does not shut down, in the short run the firm will

A) charge a higher price.

B) produce more output so the extra revenue will cover the increased costs.

C) produce less output to decrease total costs.

D) continue producing the same quantity as before but will earn less economic profit.

E) continue producing the same quantity as before and continue earning the same economic

profit as before.

Skill: Level 4: Applying models

Section: Checkpoint 14.1

Author: TS

AACSB: Analytical reasoning

28

Copyright © 2011 Pearson Education, Inc.

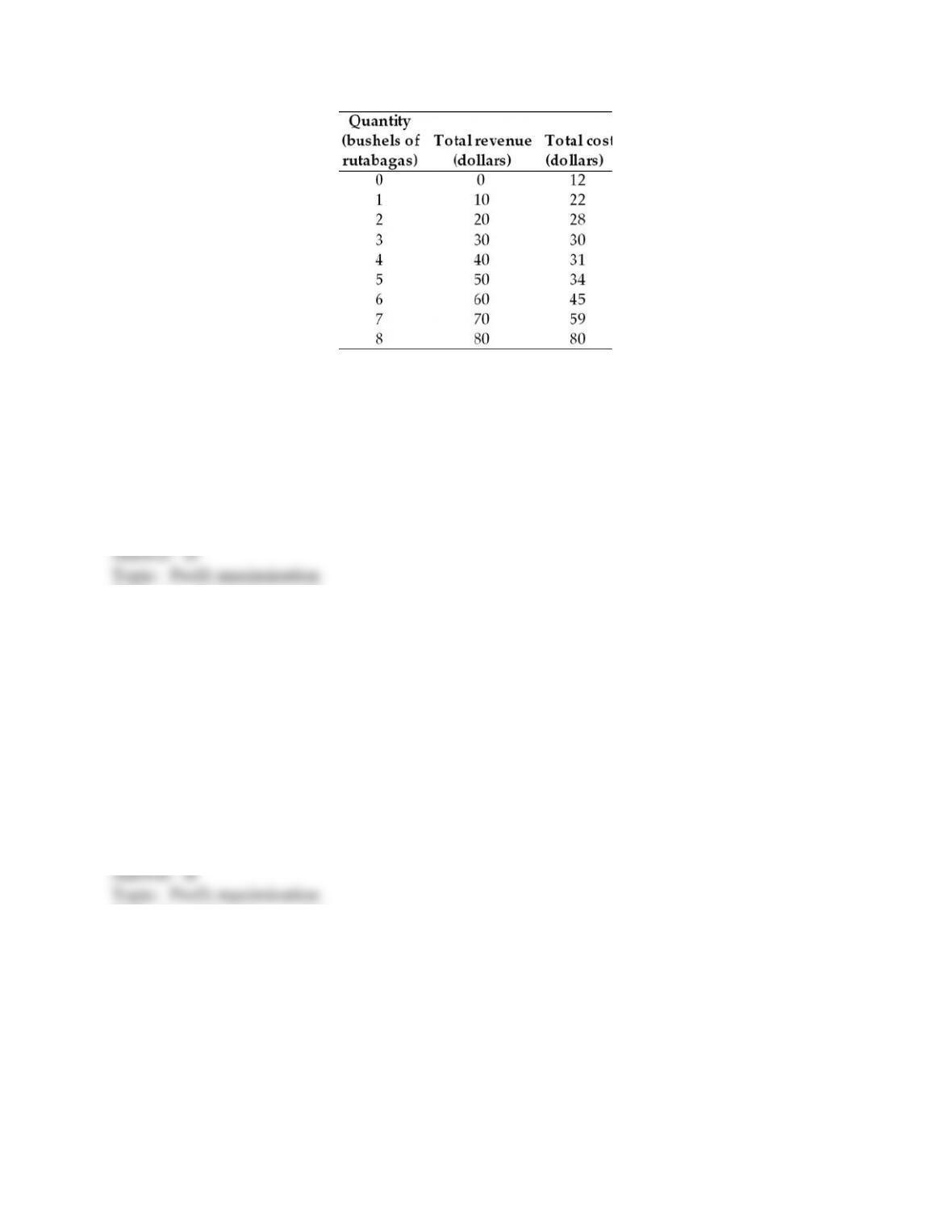

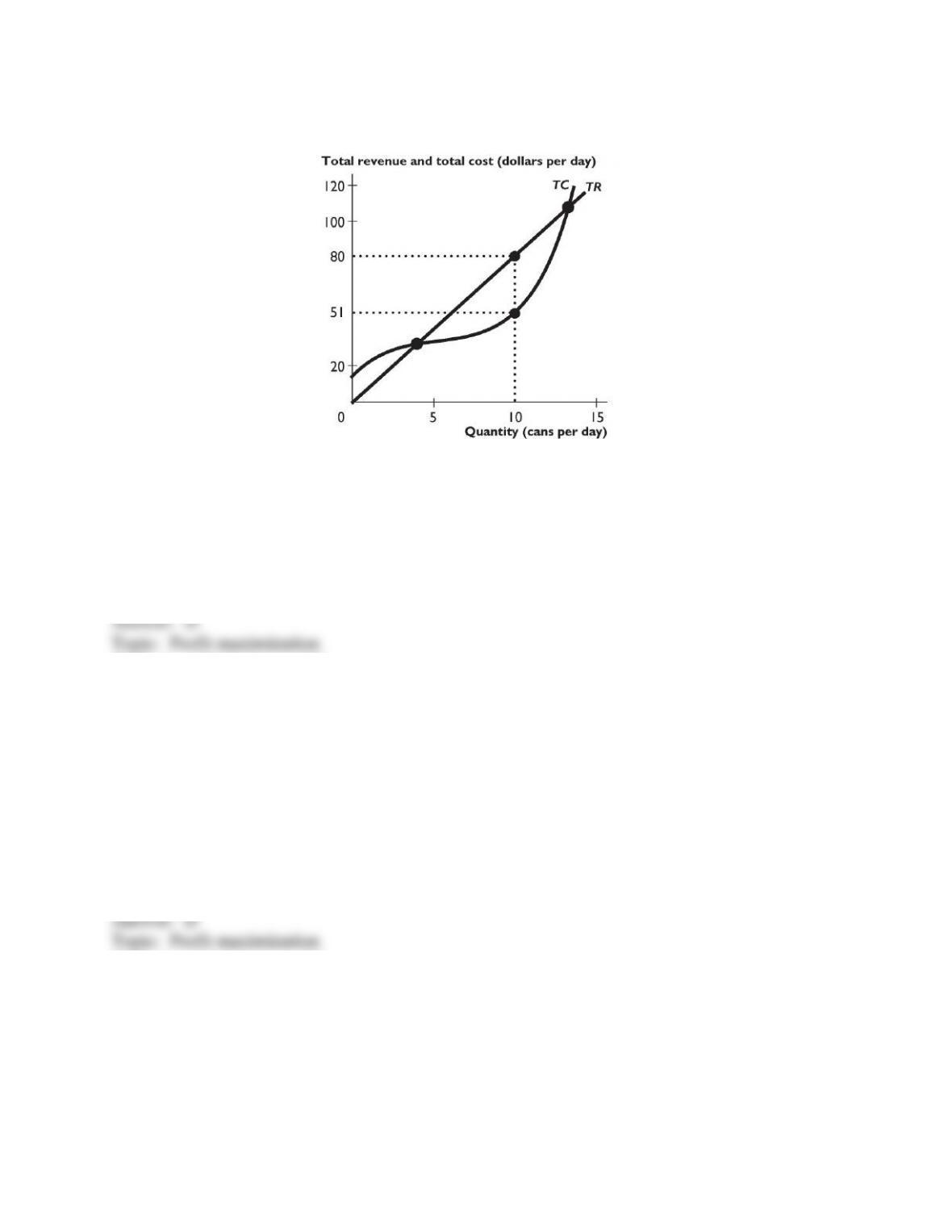

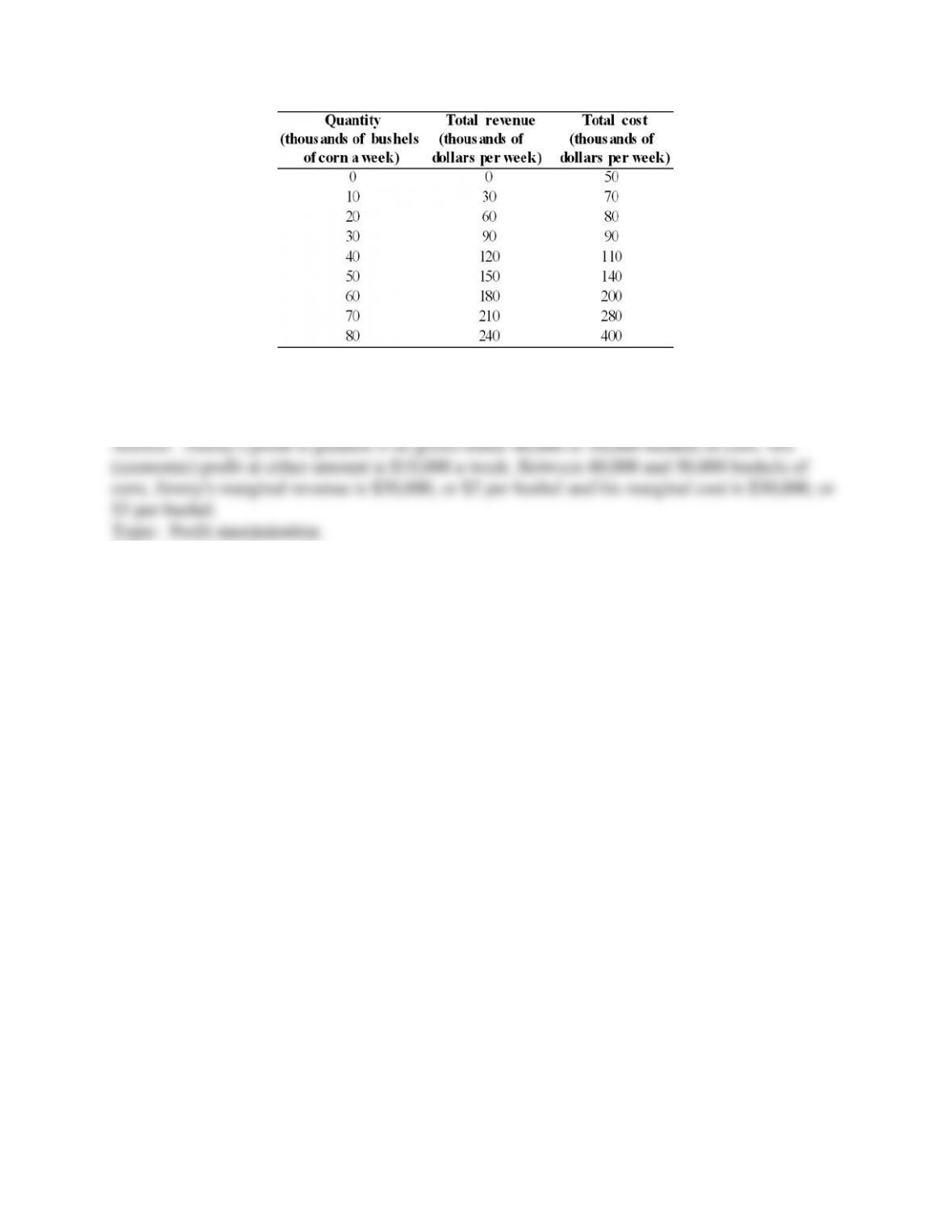

79) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. When Omar produces 2 bushels of rutabagas, his total profit

equals

A) $0.

B) $20.

C) $28.

D) -$8.

E) $48.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Analytical reasoning

80) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. Omar's total profit is maximized when he produces ________

bushels of rutabagas.

A) 3

B) 5

C) 6

D) 8

E) 7

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Analytical reasoning

29

Copyright © 2011 Pearson Education, Inc.

81) The above table has the total revenue and total cost schedule for Omar, a perfectly

competitive grower of rutabagas. When Omar maximizes his profit, Omar's profit equals

A) $80.

B) $11.

C) $30.

D) $16.

E) $105.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Analytical reasoning

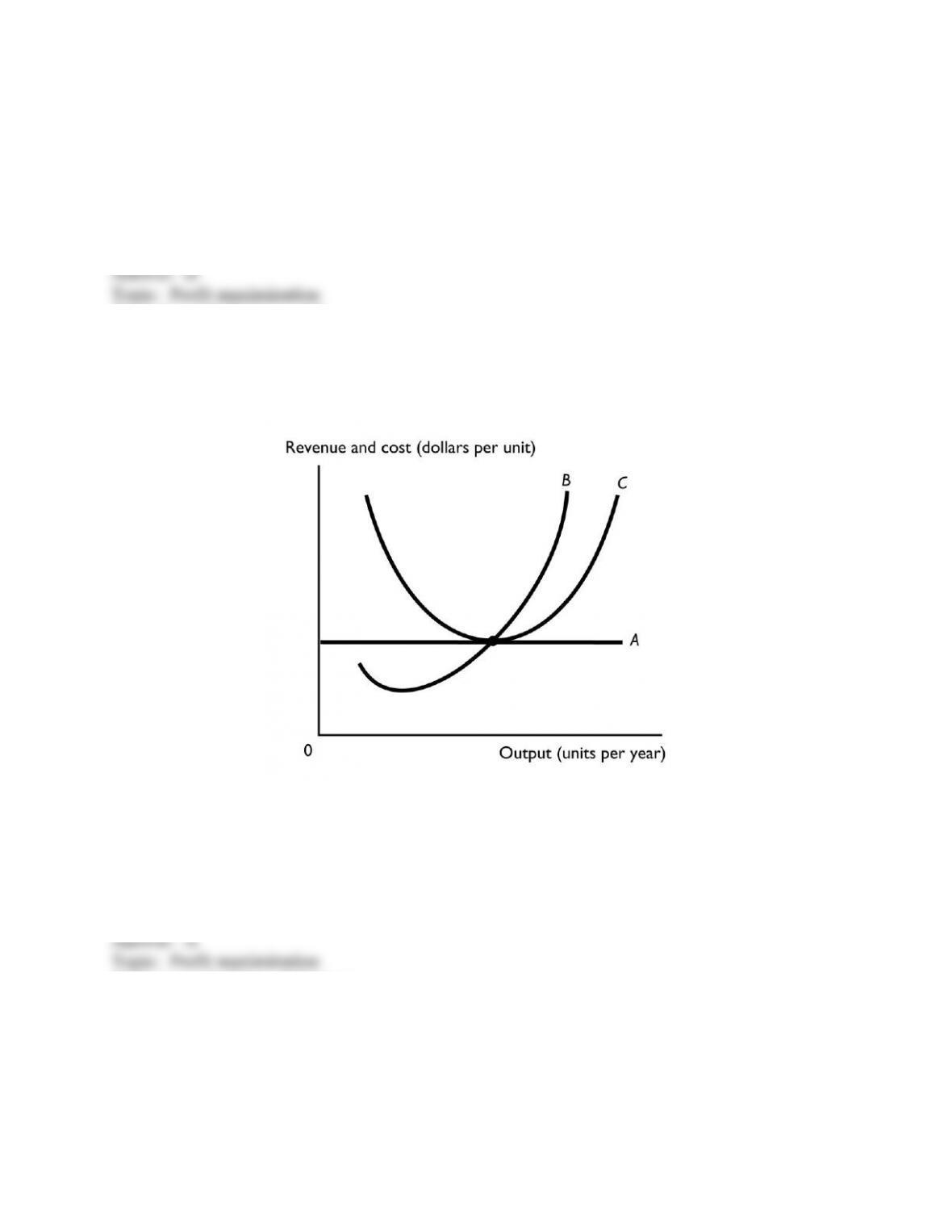

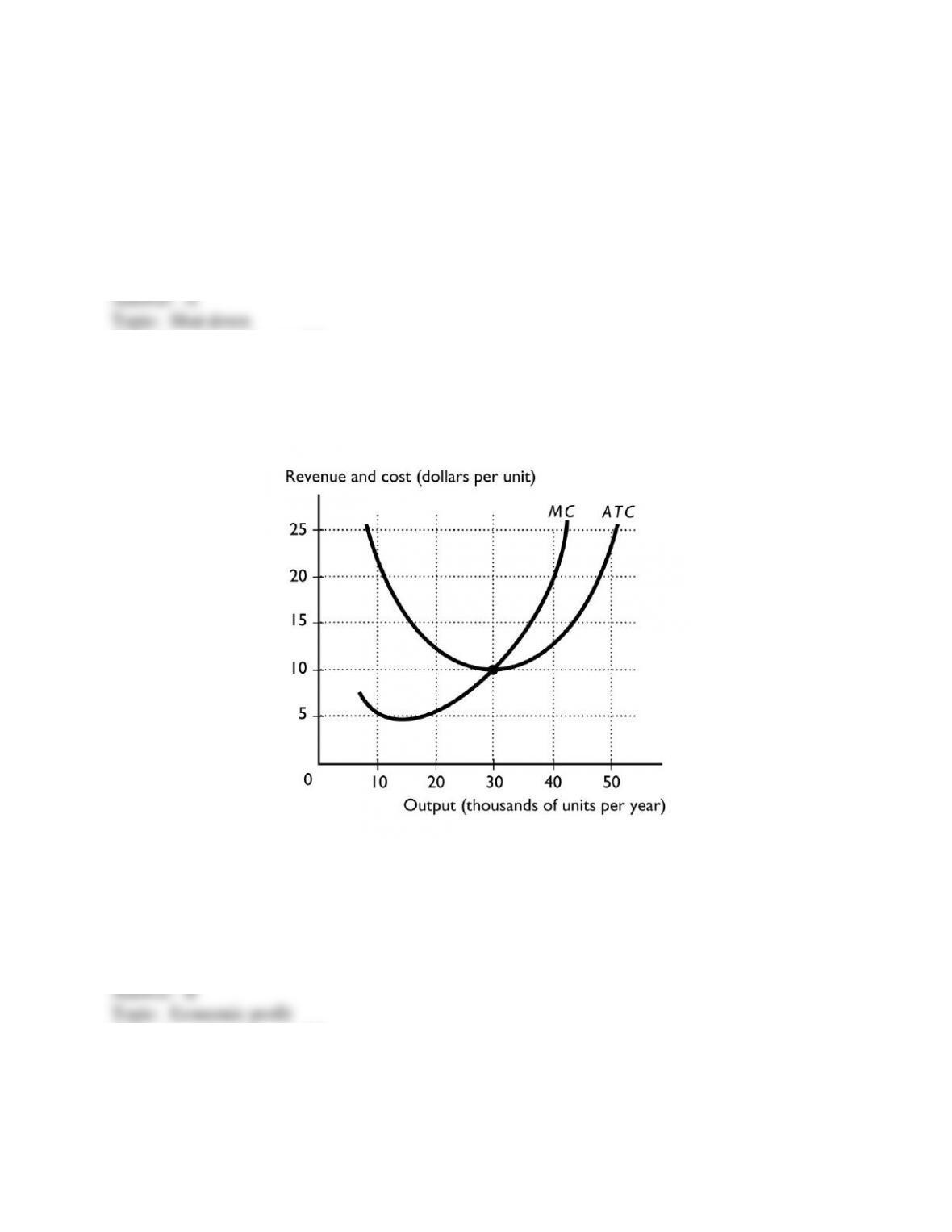

82) The above figure illustrates a perfectly competitive firm. Curve A represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: MR

AACSB: Reflective thinking

30

Copyright © 2011 Pearson Education, Inc.

83) The above figure illustrates a perfectly competitive firm. Curve B represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: MR

AACSB: Reflective thinking

84) The above figure illustrates a perfectly competitive firm. Curve C represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) market demand curve.

E) AFC curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: MR

AACSB: Reflective thinking

31

Copyright © 2011 Pearson Education, Inc.

85) The above figure illustrates a perfectly competitive firm. If the market price is $40 a unit, to

maximize its profit (or minimize its loss) the firm should

A) shut down.

B) produce more than 10 and less than 30 units.

C) produce 30 units.

D) produce more than 30 units and less than 40 units..

E) produce 40 units.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Analytical reasoning

86) The above figure illustrates a perfectly competitive firm. If the market price is $10 a unit, to

maximize its profit (or minimize its loss) the firm should

A) shut down.

B) produce between 10 and less than 30 units.

C) produce 30 units.

D) produce more than 30 units and less than 40 units.

E) produce 40 units.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Analytical reasoning

32

Copyright © 2011 Pearson Education, Inc.

87) If a firm shuts down, it

A) earns zero economic profit.

B) incurs an economic loss equal to its total variable cost.

C) incurs an economic loss equal to its total fixed cost.

D) earns a normal profit.

E) might earn an economic profit, a normal profit, or incur an economic loss.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

88) If a struggling perfectly competitive furniture store in Detroit shuts down, it incurs an

economic loss equal to its

A) marginal cost.

B) total fixed cost.

C) total variable cost.

D) average variable cost.

E) average total cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

89) A perfectly competitive firm will shutdown when the price is just below the minimum point

on the

A) average fixed cost curve.

B) average total cost curve.

C) marginal cost curve.

D) average variable cost curve.

E) marginal revenue curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

33

Copyright © 2011 Pearson Education, Inc.

90) Under which of the following conditions will a profit-maximizing perfectly competitive firm

shut down in the short run?

A) when it is earning a normal profit

B) whenever its marginal cost is less than its marginal revenue

C) when the price is less than its minimum average variable cost

D) whenever its total cost is greater than its total revenue

E) when the price is less than its minimum average total cost

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

91) A perfectly competitive firm will continue to operate in the short run when the market price

is below its average total cost if the

A) marginal revenue is greater than marginal cost.

B) price is at least equal to the minimum average variable cost.

C) total fixed costs are less than total revenue.

D) marginal cost is minimized.

E) price is also less than the minimum average variable cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

92) If the price is less than a perfectly competitive firm's minimum average variable cost, the

firm

A) earns an economic profit.

B) operates and incurs an economic loss equal to total fixed cost.

C) operates and incurs an economic loss equal to average variable cost.

D) shuts down and incurs an economic loss equal to total fixed cost.

E) shuts down and incurs an economic loss equal to average variable cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

34

Copyright © 2011 Pearson Education, Inc.

93) Which of the following is true if a firm shuts down?

i. The price is less than minimum average variable cost.

ii. The firm is able to avoid an economic loss.

iii. The firm incurs a loss equal to its total variable cost.

A) i only

B) i and ii

C) i and iii

D) iii only

E) ii only

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: CD

AACSB: Reflective thinking

94) If the market price is $50 for a unit of a good produced in a perfectly competitive market and

the firm's minimum average variable cost is $52, then to maximize its profit (or minimize its

loss) the firm should

A) definitely produce the unit.

B) shut down.

C) not produce the unit but remain open.

D) not produce the unit. Whether the firm should shut down or remain open cannot be

determined without more information.

E) produce the unit only if the price exceeds the average fixed cost.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: SA

AACSB: Analytical reasoning

95) Suppose a perfectly competitive firm's minimum average variable cost is $3 when it

produces 50. If the price is $2 and the firm's marginal cost is $2, the firm should

A) continue to produce, but produce more than 50.

B) continue to produce 50.

C) continue to produce, but produce less than 50.

D) shut down.

E) continue to operate, but to determine the amount of production needs more information than is

given.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: MR

AACSB: Analytical reasoning

35

Copyright © 2011 Pearson Education, Inc.

96) Under what conditions would a perfectly competitive cotton farmer who is incurring an

economic loss temporarily stay in business?

A) if the total revenue exceeds the total fixed cost

B) if the total revenue exceeds the total variable cost

C) if the total revenue is positive

D) if the total revenue is increasing

E) if the marginal revenue exceeds the price.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: JC

AACSB: Reflective thinking

97) The largest loss a profit-maximizing perfectly competitive firm can incur in the short run

equals its

A) average variable cost multiplied by output.

B) total fixed cost.

C) marginal cost multiplied by the number of units produced.

D) average total cost multiplied by the number of units produced.

E) total variable cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

98) The rutabaga market is perfectly competitive and the price of a ton of rutabagas rises. As a

result, Rudy, a rutabaga farmer, will

A) decrease his output of rutabagas.

B) not change his output of rutabagas because Rudy's firm is a price taker.

C) increase his output of rutabagas.

D) at first decrease and then increase his output of rutabagas.

E) probably change his output of rutabagas, but more information is needed about the change in

the marginal revenue of a ton of rutabagas.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

36

Copyright © 2011 Pearson Education, Inc.

99) A perfectly competitive firm's short-run supply curve is

A) horizontal at the market price.

B) its total cost curve above the AVC.

C) its marginal cost curve below the marginal revenue curve.

D) its marginal cost curve above the AVC curve.

E) its marginal revenue curve below the ATC curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: WM

AACSB: Reflective thinking

100) The firm's supply curve is its

A) marginal cost curve above the average variable cost curve.

B) marginal cost curve below the average variable cost curve.

C) average variable cost curve above the marginal cost curve.

D) average total cost curve above the marginal cost curve.

E) marginal revenue curve above the average total cost curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: SB

AACSB: Reflective thinking

101) Which of the following will increase a perfectly competitive seller's short-run supply and

shift the firm's short-run supply curve rightward?

A) an increase in the market price

B) a decrease in average fixed costs

C) a decrease in marginal cost

D) Both answers A and B are correct.

E) Both answers A and C are correct.

Skill: Level 3: Using models

Section: Checkpoint 14.1

Author: TS

AACSB: Reflective thinking

37

Copyright © 2011 Pearson Education, Inc.

102) The four market types are

A) perfect competition, imperfect competition, monopoly, and oligopoly.

B) oligopoly, monopsony, monopoly, and imperfect competition.

C) perfect competition, monopoly, monopolistic competition, and oligopoly.

D) oligopoly, oligopolistic competition, monopoly, and perfect competition.

E) perfect competition, imperfect competition, monopoly, and duopoly.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

103) A requirement of perfect competition is that

i. many firms sell an identical product to many buyers.

ii. there are no restrictions on entry into (or exit from) the market, and established firms have no

advantage over new firms

iii. sellers and buyers are well informed about prices.

A) i only

B) i and ii

C) iii only

D) i and iii

E) i, ii, and iii

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

104) A perfectly competitive firm is a price taker because

A) many other firms produce the same product.

B) only one firm produces the product.

C) many firms produce a slightly differentiated product.

D) a few firms compete.

E) it faces a vertical demand curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

38

Copyright © 2011 Pearson Education, Inc.

105) The demand curve faced by a perfectly competitive firm is

A) horizontal.

B) vertical.

C) downward sloping.

D) upward sloping.

E) U-shaped.

Skill: Level 1: Definition

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

106) For a perfectly competitive corn grower in Nebraska, the marginal revenue curve is

A) downward sloping.

B) the same as its demand curve.

C) upward sloping.

D) U-shaped.

E) vertical at the profit maximizing quantity of production.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

107) A perfectly competitive firm maximizes its profit by producing at the point where

A) total revenue equals total cost.

B) marginal revenue is equal to marginal cost.

C) total revenue is equal to marginal revenue.

D) total cost is at its minimum.

E) total revenue is at its maximum.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

39

Copyright © 2011 Pearson Education, Inc.

108) If the market price is lower than a perfectly competitive firm's average total cost, the firm

will

A) immediately shut down.

B) continue to produce if the price exceeds the average fixed cost.

C) continue to produce if the price exceeds the average variable cost.

D) shut down if the price exceeds the average fixed cost.

E) shut down if the price is less than the average fixed cost.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Reflective thinking

109) One part of a perfectly competitive trout farm's supply curve is its

A) marginal cost curve below the shutdown point.

B) entire marginal cost curve.

C) marginal cost curve above the shutdown point.

D) average variable cost curve above the shutdown point.

E) marginal revenue curve above the demand curve.

Skill: Level 2: Using definitions

Section: Checkpoint 14.1

Author: STUDY GUIDE

AACSB: Analytical reasoning

14.2 Output, Price, and Profit in the Short Run

1) The market supply in the short run for the perfectly competitive industry is

A) the same as each producer's supply.

B) the sum of the supply schedules of all firms.

C) divided up according to each firm's selling price.

D) set at the maximum price a buyer will pay for one unit.

E) equal to the average of each firm's supply schedule.

Skill: Level 1: Definition

Section: Checkpoint 14.2

Author: WM

AACSB: Reflective thinking

40

Copyright © 2011 Pearson Education, Inc.

2) If there are 1,000 identical rice farmers who are each willing to supply 200 bushels of rice at

$2 per bushel, what price and quantity combination is a point on the market supply curve for

rice?

A) $2 and 200 bushels

B) $2 and 200,000 bushels

C) $2,000 and 200,000 bushels

D) $2,000 and 1,000 bushels

E) $2 and 1,000 farmers

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SB

AACSB: Analytical reasoning

3) In the short run, a perfectly competitive firm ________ earn an economic profit and ________

incur an economic loss.

A) might; will never

B) will never; might

C) might; might

D) will never; will never

E) will definitely; will never

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: SA

AACSB: Reflective thinking

4) In the short run, a perfectly competitive firm

A) can earn only a normal profit.

B) can possibly earn an economic profit or possibly incur an economic loss.

C) produces the level of output that sets the average total cost equal to the market price.

D) can vary all its inputs.

E) can change only its fixed inputs.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: SA

AACSB: Reflective thinking

41

Copyright © 2011 Pearson Education, Inc.

5) In the short run, a perfectly competitive firm can experience which of the following?

i. an economic profit

ii. an economic loss but it continues to stay open

iii. an economic loss equal to its total fixed cost when it shuts down

A) only i

B) i and ii

C) i and iii

D) ii and iii

E) i, ii, and iii

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: TS

AACSB: Reflective thinking

6) If a perfectly competitive seller is maximizing profit and is earning zero economic profit,

which of the following will this seller do?

A) go to work in the next-best earning opportunity

B) shut down, with a loss equal to total fixed cost

C) continue at the current output, earning a normal profit

D) increase production in order to earn an economic profit

E) remain open but decrease production in order to earn an economic profit

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: TS

AACSB: Reflective thinking

7) If a perfectly competitive firm finds that the price exceeds its ATC, then the firm

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is earning an economic profit.

D) is incurring an economic loss.

E) is earning zero economic profit.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: WM

AACSB: Reflective thinking

42

Copyright © 2011 Pearson Education, Inc.

8) For a perfectly competitive sugar producer in Haiti, a short-run economic profit will occur if

the price of each ton of sugar sold is

A) greater than the average total cost of producing sugar.

B) equal to the average total cost of producing sugar.

C) less than the average total cost of producing sugar.

D) rising as more sugar is sold.

E) greater than the marginal revenue of each ton of sugar.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: JC

AACSB: Reflective thinking

9) If Henry, a perfectly competitive lime grower in Southern California, can sell his limes at a

price greater than his average total cost, Henry will

A) incur an economic loss.

B) suffer an accounting loss.

C) have an incentive to shut down.

D) earn an economic profit.

E) make zero economic profit.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: TS

AACSB: Reflective thinking

10) If a perfectly competitive firm's average total cost is less than the price, then the firm

A) incurs an economic loss.

B) earns an economic profit.

C) earns a normal profit.

D) earns either a normal profit or an economic profit depending on whether the marginal revenue

is equal to or greater than the price.

E) None of the above answers is correct because the relationship between the price and average

total cost has nothing to do with the firm's profit.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: SA

AACSB: Reflective thinking

43

Copyright © 2011 Pearson Education, Inc.

11) If the market price is $50 per unit for a good produced in a perfectly competitive market and

the firm's average total cost is $52, then the firm

A) has an economic loss of $2 per unit.

B) has an economic profit of $2 per unit.

C) has a normal profit.

D) has a total economic loss of $52.

E) More information is needed to determine the firm's economic profit or loss per unit.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SA

AACSB: Analytical reasoning

12) Peter's Pencils is a perfectly competitive company producing pencils. Suppose Peter is

producing 1,000 pencils an hour. If the total cost of 1,000 pencils is $500, the market price per

pencil is $2, and the marginal cost is $2, then Peter

A) has an economic profit because marginal revenue is equal to marginal cost at this output

level.

B) should decrease his output to increase his profit.

C) is maximizing his profit and is earning an economic profit.

D) should increase his output to increase his profit.

E) is not maximizing his profit but is earning a normal profit anyway.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SA

AACSB: Analytical reasoning

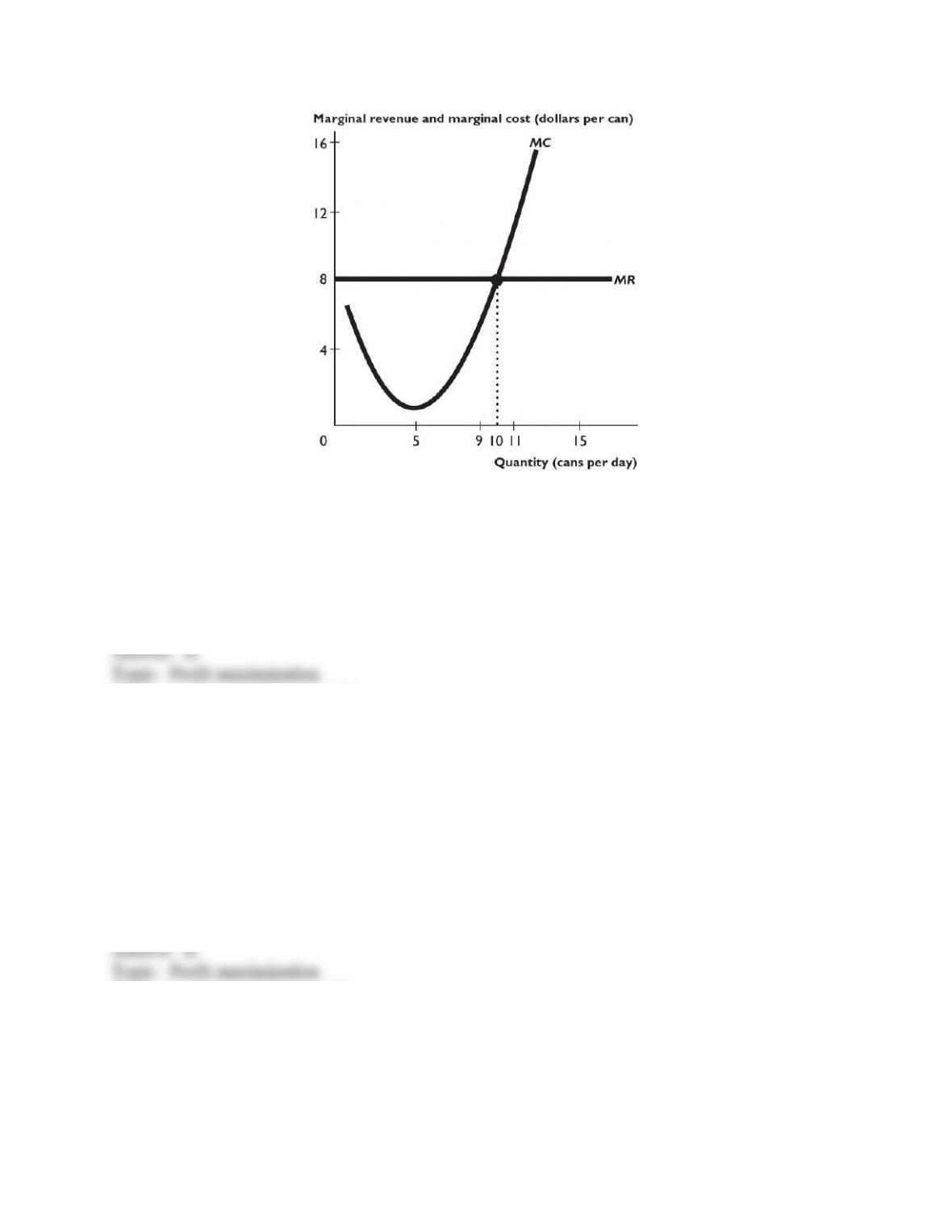

13) Suppose that marginal revenue for a perfectly competitive firm is $20 . When the firm

produces 10 units, its marginal cost is $20, its average total cost is $22, and its average variable

cost is $17. Then to maximize its profit in the short run, the firm

A) should stay open and incur an economic loss of $20.

B) must increase its output to increase its profit.

C) must decrease its output to increase its profit.

D) should shut down.

E) should not change its production because it is already maximizing its profit and is earning a

normal profit.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: CD

AACSB: Analytical reasoning

44

Copyright © 2011 Pearson Education, Inc.

14) A perfectly competitive firm is producing 50 units of output, which it sells at the market

price of $23 per unit. The firm's average total cost is $20. What is the firm's total revenue?

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: TS

AACSB: Analytical reasoning

15) A perfectly competitive firm is producing 50 units of output and selling at the market price

of $23. The firm's average total cost is $20. What is the firm's total cost?

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: TS

AACSB: Analytical reasoning

16) A perfectly competitive firm is producing 50 units of output and selling at the market price

of $23. The firm's average total cost is $20. What is the firm's economic profit?

A) $23

B) $150

C) $1,000

D) $1,150

E) $50

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: TS

AACSB: Analytical reasoning

45

Copyright © 2011 Pearson Education, Inc.

17) For a perfectly competitive syrup producer whose average total cost curve does not change,

an economic profit could turn into an economic loss if the

A) market demand for syrup decreases.

B) marginal cost curve shifts downward.

C) market demand for syrup does not change.

D) market demand for syrup increases.

E) price of syrup rises.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: JC

AACSB: Reflective thinking

18) For a perfectly competitive rancher in Wyoming, if the price does not change, an economic

profit could turn into an economic loss if the

A) average total cost curve shifts downward.

B) average total cost curve does not change.

C) average total cost curve shifts upward.

D) marginal cost curve shifts downward.

E) average fixed cost decreases.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: JC

AACSB: Analytical reasoning

46

Copyright © 2011 Pearson Education, Inc.

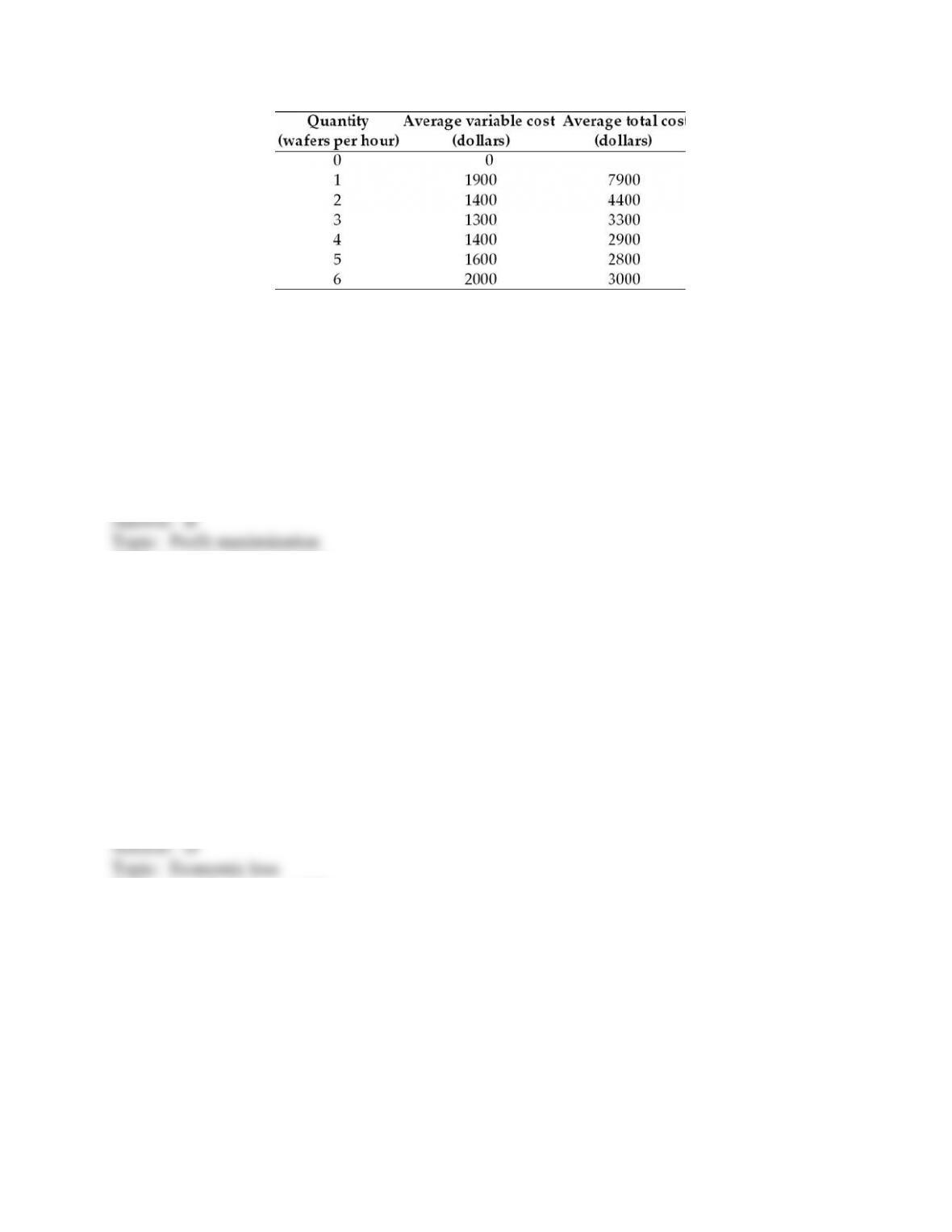

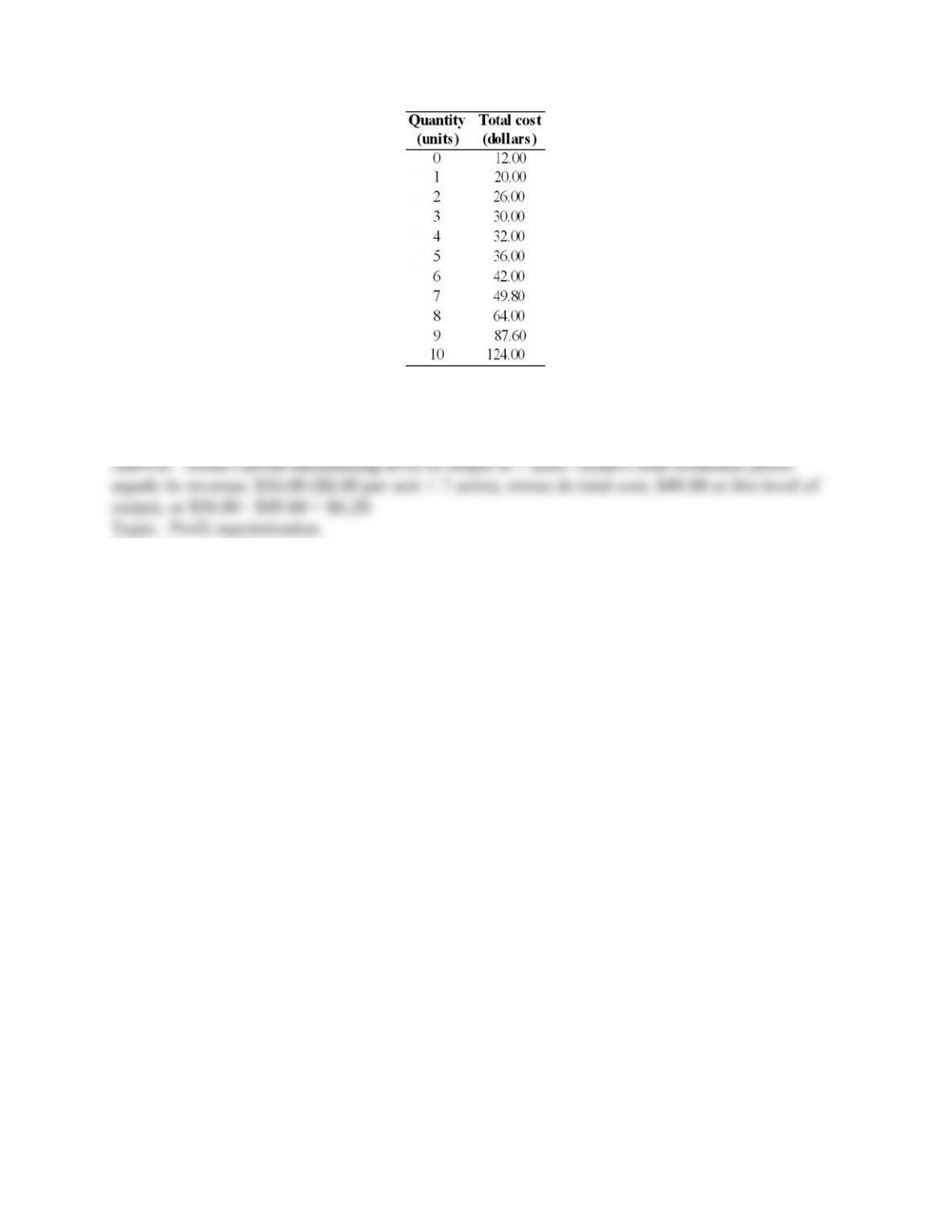

19) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. If the market price of a wafer is $2,400 dollars, how many wafers will

the firm produce?

A) 0

B) 4 or 5

C) 3 or 4

D) 1 or 2

E) 6

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

20) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. If the market price of a wafer is $2,400 dollars, the firm is

A) earning a normal profit.

B) earning an economic profit of $12,000 an hour.

C) incurring an economic loss of $2,800 an hour.

D) incurring an economic loss of $2,000 an hour.

E) earning an economic profit of $2,400 an hour.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

47

Copyright © 2011 Pearson Education, Inc.

21) Computer memory chips are produced on wafers, each wafer having many separate chips

that are separated and sold. The above table shows costs for a perfectly competitive producer of

computer memory chips. This firm will produce as long as the market price of a wafer is above

A) $1,300.

B) $1,400.

C) $7,900.

D) $2,800.

E) $9,800.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

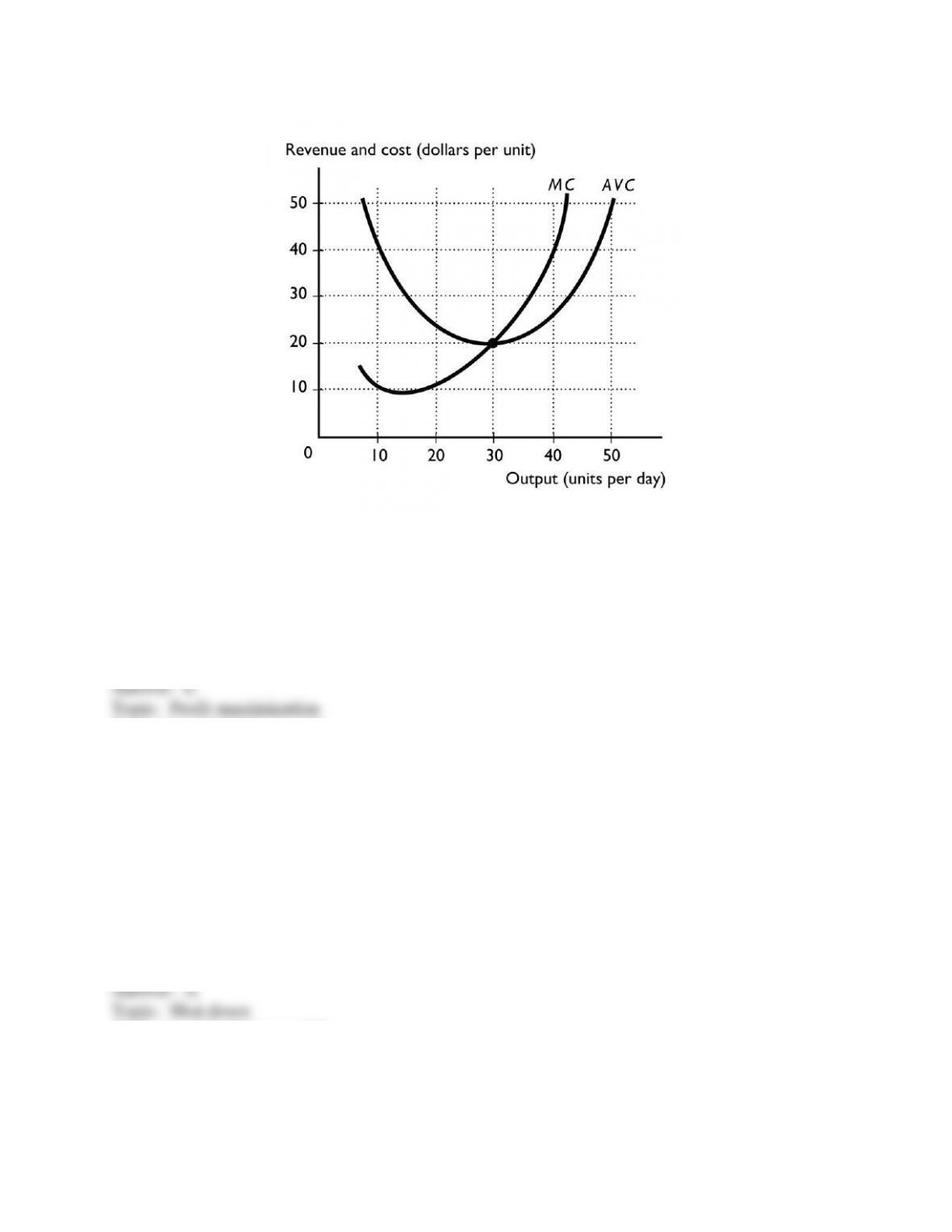

22) The above figure shows a perfectly competitive firm. If the market price is $15, the firm

A) is incurring an economic loss.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) might shut down but more information is needed about the AVC.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: MR

AACSB: Analytical reasoning

48

Copyright © 2011 Pearson Education, Inc.

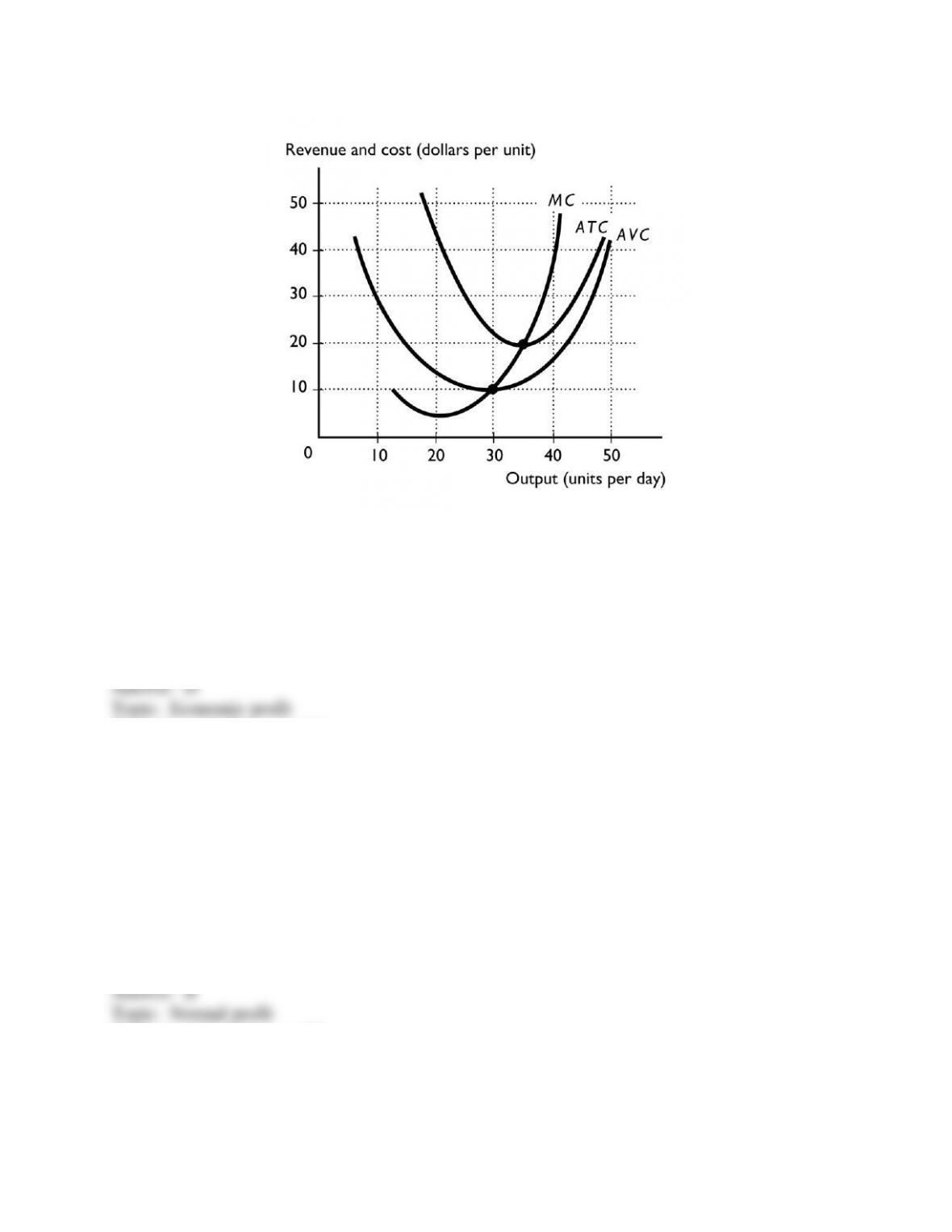

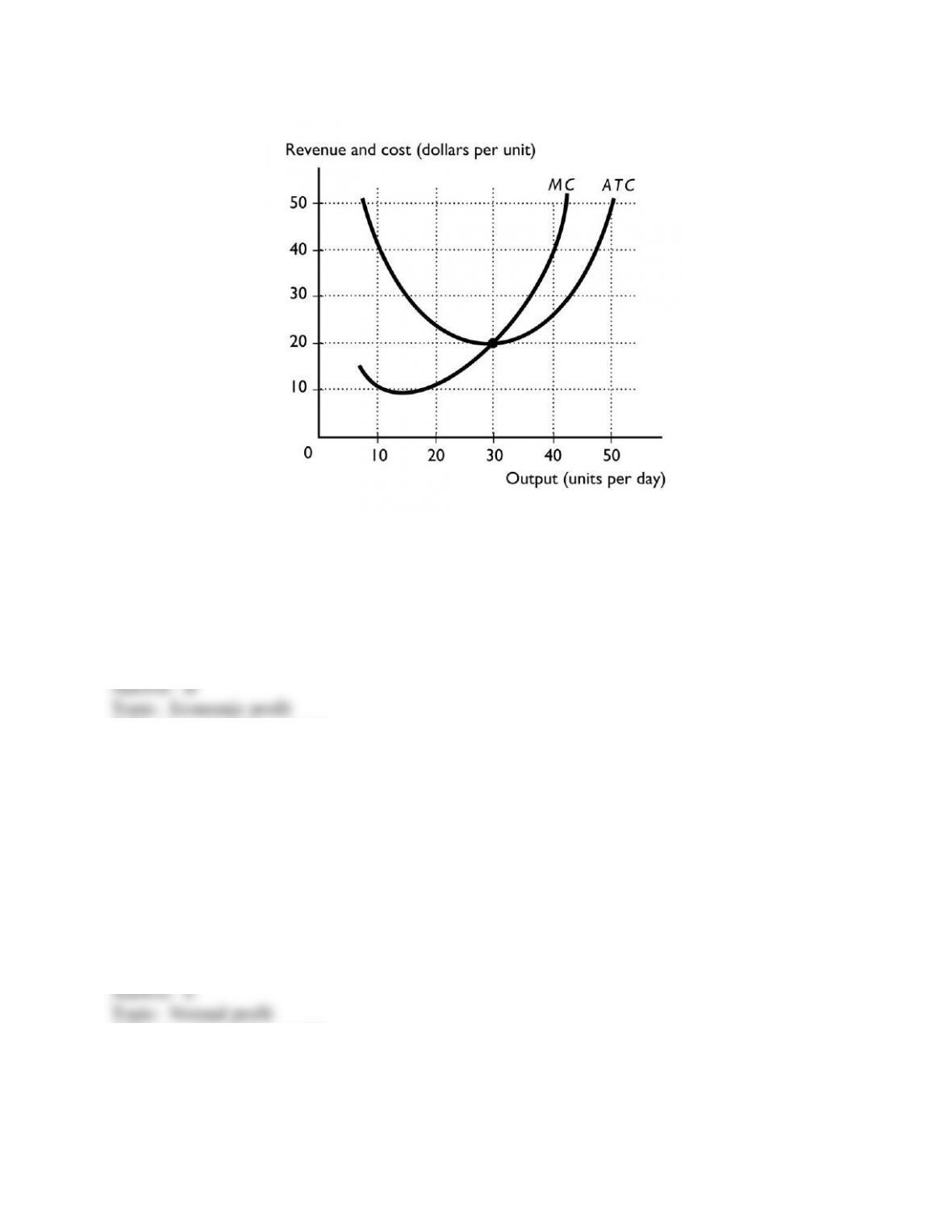

23) The above figure shows a perfectly competitive firm. If the market price is $10, the firm

A) is incurring an economic loss.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) might shut down but more information is needed about the AVC.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: MR

AACSB: Analytical reasoning

24) The above figure shows a perfectly competitive firm. If the market price is $5, the firm

A) might shut down but more information is needed about the AVC.

B) is earning an economic profit.

C) is earning a normal profit.

D) will immediately shut down.

E) will not shut down.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SA

AACSB: Analytical reasoning

49

Copyright © 2011 Pearson Education, Inc.

25) The above figure shows a perfectly competitive firm. If the market price is more than $20 per

unit, the firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

26) The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: MR

AACSB: Analytical reasoning

50

Copyright © 2011 Pearson Education, Inc.

27) The above figure shows a perfectly competitive firm. If the market price is $15 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

28) The above figure shows a perfectly competitive firm. If the market price is $5 per unit, the

firm

A) will definitely shut down to minimize its losses.

B) will stay open to produce and will earn a normal profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will earn an economic profit.

E) might shut down but more information is needed about the fixed cost.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: PH

AACSB: Analytical reasoning

51

Copyright © 2011 Pearson Education, Inc.

29) The figure above shows a perfectly competitive firm. If the market price is $40 per unit, then

the firm produces ________ units and has an economic profit that is ________.

A) more than 45; more than $400

B) 40; more than $400

C) 40; less than $400

D) 30; equal to zero because the firm earns a normal profit

E) 30; more than $250

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SA

AACSB: Analytical reasoning

30) The figure above shows a perfectly competitive firm. If the market price is $20 per unit, then

the firm produces ________ units and has an economic profit that is ________.

A) more than 30; more than $100

B) 30; more than $100

C) 20; less than $400

D) 0; zero because the firm earns a normal profit

E) 30; zero because the firm earns a normal profit

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: SA

AACSB: Analytical reasoning

52

Copyright © 2011 Pearson Education, Inc.

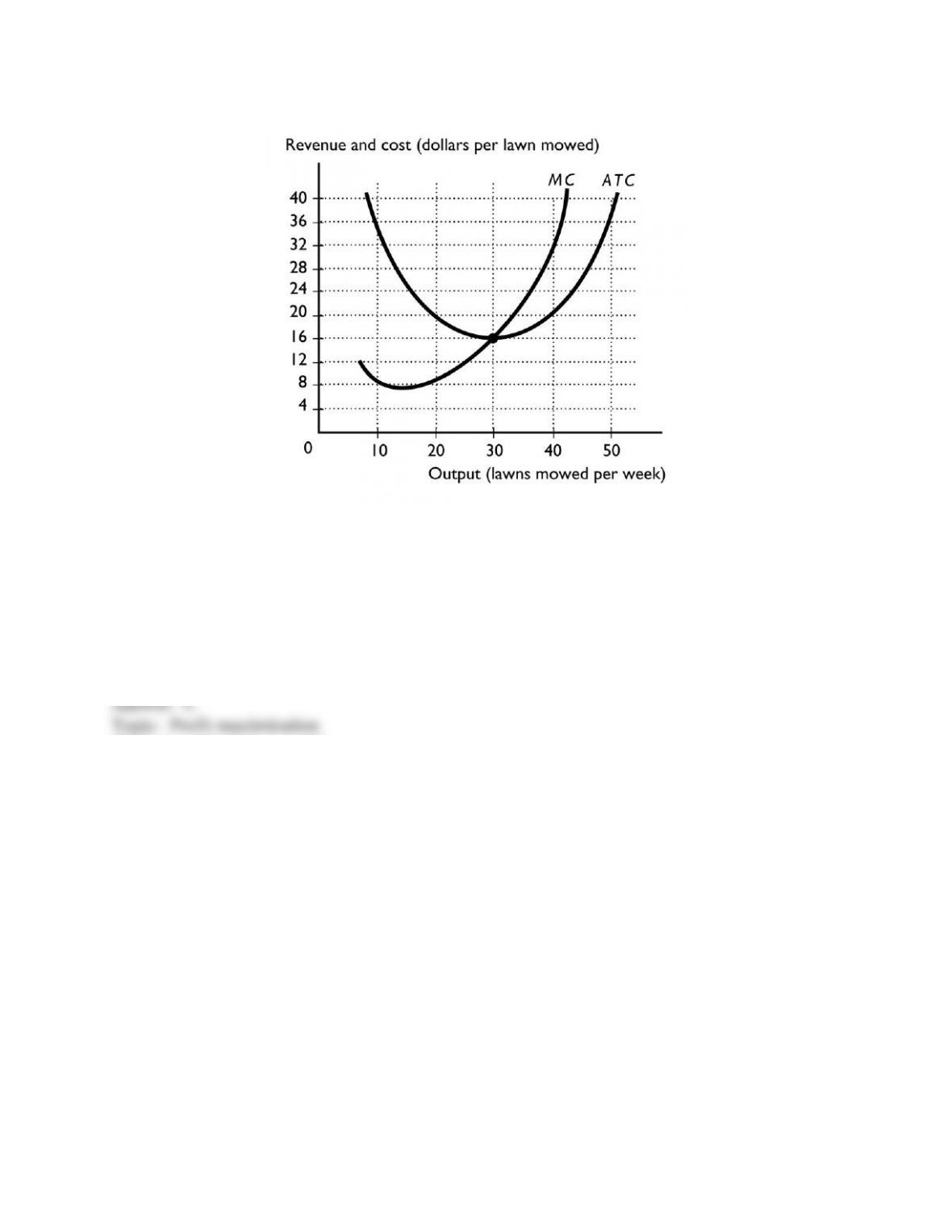

31) Bill owns a lawn-care company in Windermere, Florida, whose cost curves are illustrated in

the above figure. The market equilibrium price in this perfectly competitive market equals $32

per lawn mowed. At this price, how many lawns will Bill mow per week?

A) more than 10 and less than 30

B) 30

C) 40

D) 50

E) 0

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: JC

AACSB: Analytical reasoning

53

Copyright © 2011 Pearson Education, Inc.

32) Bill owns a lawn-care company in Windermere, Florida, whose cost curves are illustrated in

the above figure. The market equilibrium price in this perfectly competitive market equals $32

per lawn mowed. Bill's average total cost curve is ATC, so his total cost of production equals

A) $0 because Bill shuts down.

B) more than $0 and less than $1,200 per week.

C) more than $1,200 and less than $1,400 per week.

D) more than $1,400 per week and less than $1,800 per week.

E) more than $1,800 per week.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: JC

AACSB: Analytical reasoning

33) Bill owns a lawn-care company in Windermere, Florida, Florida, whose cost curves are

illustrated in the above figure. The market equilibrium price in this perfectly competitive market

equals $32 per lawn mowed. If Bill's average total cost curve is ATC, his total economic

________ equals ________.

A) loss; $800 per week

B) profit; $1,280 per week

C) profit; $480 per week

D) loss; $1,280 per week

E) profit; $32 per week

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: JC

AACSB: Analytical reasoning

34) If the market supply curve and market demand curve for a good intersect at 600,000 units

and there are 10,000 identical firms in the market, then each firm is producing

A) 600,000 units.

B) 60,000,000,000 units.

C) 60,000 units.

D) 60 units.

E) 10,000 units.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Analytical reasoning

54

Copyright © 2011 Pearson Education, Inc.

35) In the short run, a perfectly competitive firm

A) must make an economic profit.

B) must incur an economic loss.

C) must make zero economic profit.

D) might make an economic profit, an economic loss, or a normal profit.

E) None of the above answers is correct.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

36) A perfectly competitive firm definitely earns an economic profit in the short run if price is

A) equal to marginal cost.

B) equal to average total cost.

C) greater than average total cost.

D) greater than marginal cost.

E) greater than average variable cost.

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

37) If a perfectly competitive firm is maximizing its profit and is earning an economic profit,

which of the following is correct?

i. price equals marginal revenue

ii. marginal revenue equals marginal cost

iii. price is greater than average total cost

A) i only

B) i and ii only

C) ii and iii only

D) i and iii only

E) i, ii, and iii

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

55

Copyright © 2011 Pearson Education, Inc.

38) The market for watermelons in Alabama is perfectly competitive. A watermelon producer

earning zero economic profit could earn an economic profit if the

A) average total cost of selling watermelons does not change.

B) average total cost of selling watermelons rises.

C) average total cost of selling watermelons falls.

D) marginal cost of selling watermelons does not change.

E) marginal cost of selling watermelons rises.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

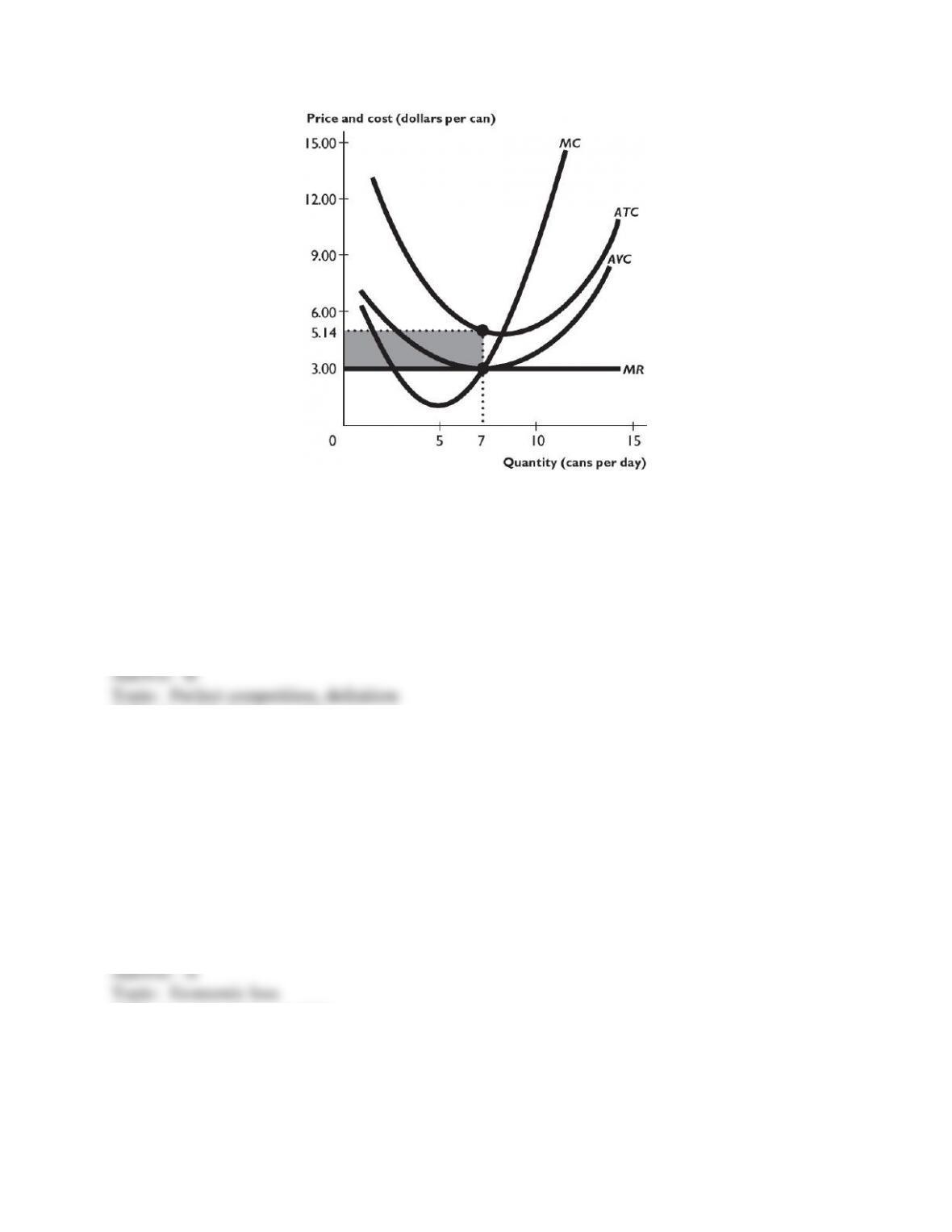

39) Juan's Software Service Company is in a perfectly competitive market. Juan has total fixed

cost of $25,000, average variable cost for 1,000 service calls is $45, and marginal revenue is $75.

Juan's makes 1,000 service calls a month. What is his economic profit?

A) $5,000

B) $25,000

C) $45,000

D) $75,000

E) $50,000

Skill: Level 3: Using models

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Analytical reasoning

40) If a perfectly competitive firm finds that price is less than its ATC, then the firm

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is earning an economic profit.

D) is incurring an economic loss.

E) is earning zero economic profit.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

56

Copyright © 2011 Pearson Education, Inc.

41) A perfectly competitive video-rental firm in Phoenix incurs an economic loss if the average

total cost of each video rental is

A) greater than the marginal revenue of each rental.

B) less than the marginal revenue of each rental.

C) equal to the marginal revenue of each rental.

D) equal to the price of each rental.

E) greater than the average variable cost of each video.

Skill: Level 2: Using definitions

Section: Checkpoint 14.2

Author: STUDY GUIDE

AACSB: Reflective thinking

14.3 Output, Price, and Profit in the Long Run

1) When new firms enter the perfectly competitive Miami bagel market, the market

A) supply curve shifts leftward.

B) supply curve does not change.

C) demand curve shifts rightward.

D) supply curve shifts rightward.

E) demand curve shifts leftward.

Skill: Level 2: Using definitions

Section: Checkpoint 14.3

Author: JC

AACSB: Reflective thinking

2) If new firms enter a perfectly competitive industry, the market supply

A) does not change.

B) becomes more price elastic.

C) becomes more price inelastic.

D) increases.

E) decreases because each firm produces less than before the entry.

Skill: Level 2: Using definitions

Section: Checkpoint 14.3

Author: TS

AACSB: Reflective thinking

57

Copyright © 2011 Pearson Education, Inc.

3) Alice, Bud, and Celia can produce rubber bands in a perfectly competitive market. If they

enter the market, the minimum average total cost for a bundle of rubber bands, for the three of

them is $2, $3, and $4, respectively. If the market price is $2.10 per bundle, then

A) all three of them will enter the market.

B) only Alice will enter the market.

C) Alice and Bud will enter the market.

D) Bud and Celia will enter the market.

E) Alice and Celia will enter the market.

Skill: Level 2: Using definitions

Section: Checkpoint 14.3

Author: SA

AACSB: Reflective thinking

4) Suppose a perfectly competitive market is in long-run equilibrium and then there is a

permanent increase in the demand for that product. The new long-run equilibrium will have

A) fewer firms in the market.

B) more firms in the market.

C) the same number of firms in the market.

D) probably a different number of firms, but it is not possible to determine if there will be more

or fewer firms.