Chapter 17 – Understanding Accounting and Financial Information

143. Marissa is taking her first course in accounting this semester. One of the first things she

learns is that “revenue” and “net income” mean the same thing.

Feedback: Although both of these accounts are noted on the income statement, they mean

different things. Revenues are the money coming into the business from the sale of goods and

services. Net income is calculated by subtracting the cost of goods sold, operating expenses,

and taxes from the revenues.

144. Bark Three Times Pet Store’s owner is concerned with how his business decisions affect

the “bottom line”. This is another way of saying that he is concerned with the impact of

his decisions on net income after taxes.

Feedback: The term “bottom line” refers to the bottom line on an income statement, which is

the firm’s net income (or net loss).

145. Potential investors are interested in both a firm’s balance sheet and income statement

when evaluating whether or not to invest in a firm.

Feedback: Financial statements provide insight into a firm’s financial health. Investors and

potential investors seek-out both the balance sheet and the income statement to measure the

fundamentals of a firm.

17–43

149. During a period of rising prices, the FIFO technique of inventory valuation will result in

a lower net income figure than would the LIFO technique.

Feedback: During a period of rising prices, each time a firm purchases inventory, the cost of

goods will increase. The last goods purchased will cost more than the first goods purchased.

In this case, the FIFO technique (first-in, first-out) will result in higher net income, while the

LIFO technique (last-in, first-out) will result in lower net income.

150. In businesses that handle a lot of perishable items (such as supermarkets) the actual

movement of goods through inventory most closely resembles the LIFO inventory

valuation technique.

Feedback: For a business that sells perishable items, the movement of goods will more

closely resemble FIFO (First-in, First-out). When firms are concerned about perishable goods,

they attempt to sell their older stock before selling newer items. Dated, perishable items will

be placed on the sales floor in the order received.

151.

Chapter 17 – Understanding Accounting and Financial Information

If the economy began experiencing a prolonged period of deflation in which the prices

of most goods are falling, many firms would find that the LIFO method of inventory

valuation would result in higher reported profits.

Feedback: The last in, first out (LIFO) inventory valuation technique would base the cost of

goods sold on the items most recently put in inventory. In a period of falling prices, this

would result in a lower cost of goods sold because the most recently purchased items are

lower in price. Since cost of goods sold is subtracted from revenue as part of the process of

computing net income, LIFO would result in a higher reported net income.

152. During periods of rising prices, firms that want to report more attractive profits would

tend to favor the FIFO technique of inventory valuation.

Feedback: In a period of rising prices, the last inventory purchased would cost more than

earlier purchases of the same items. The FIFO (items purchased earlier) approach will yield a

lower cost of goods sold figure. This will cause the net income to be greater than if the LIFO

method had been used.

153. If the goal of a business is to pay lower taxes on its income during an inflationary period,

it is likely to use the FIFO inventory costing method.

Feedback: During a period of inflation, prices are rising. Using a LIFO method of inventory

valuation will produce a lower gross profit, and subsequently, a lower net income before

taxes. Taxes are paid only on the net income produced, after all expenses (including

depreciation) are deducted.

17–47

160. Preferred Pet Care, Inc. successfully took out a loan for $130,000 from Southwest Bank.

It used $80,000 of this loan to pay-off an existing loan that had a higher interest rate, and

purchased X-ray equipment with the remaining funds. These events were noted as

financing and investing activities on its balance sheet.

Feedback: These activities are financing and investing activities recorded on the statement of

cash flows.

161. Financial ratios are used to analyze a firm’s financial condition and financial

performance.

162. Liquidity ratios are of particular importance to stockholders, but have little relevance for

creditors.

163. The purpose of liquidity ratios is to indicate the degree to which a firm relies on

borrowed funds in its operations.

164.

Chapter 17 – Understanding Accounting and Financial Information

Liquidity refers to how fast an asset can be converted to cash.

165. The current ratio is used to evaluate a firm’s ability to pay its short-term debts.

166. The current ratio is found by dividing the firm’s total assets by its total liabilities.

167. The current ratio is a good indicator of the degree to which a firm relies on borrowed

funds in its operations.

168. Both the current ratio and the acid-test ratio are liquidity ratios.

17–51

179. The inventory turnover ratio measures the speed of inventory moving through the firm

and its conversion into sales.

180. An extremely high inventory turnover ratio may represent lost sales due to holding

inadequate stocks of merchandise.

Feedback: A high inventory turnover ratio can reflect the fact that inventory is turning over

rapidly, and the firm may find it difficult to replenish the inventory in a timely way.

181. Prattville Manufacturing has applied for a short-term loan with the First National Bank.

The loan officers of the bank are likely to look carefully at Prattville’s liquidity ratios

before they decide to grant the loan.

Feedback: Prattville’s liquidity ratios will indicate its ability to pay its short-term liabilities.

182.

Chapter 17 – Understanding Accounting and Financial Information

The acid-test ratio emphasizes the ability to convert inventory quickly into cash.

Feedback: Inventory is not included as a highly liquid asset in the acid-test ratio. Thus, the

acid-test ratio is actually a better measure of liquidity than the current ratio for firms that are

likely to have difficulty converting inventory into cash.

183. The inventory turnover ratio for all firms should be greater than 2 times.

Feedback: There is no set gauge for what constitutes a good inventory turnover ratio. Most

businesses try to determine an acceptable industry average, and then evaluating the firm’s

capabilities, the business will utilize internal strategies to meet or exceed that industry norm.

184. The Barkley Company is a fast growing start-up. The accountant calculated earnings per

share = $.13. This information will provide him/her with insight into the firm’s ability to

pay dividends.

Feedback: EPS (earnings per share) is calculated using net income after taxes. Dividends are

always paid from earnings (or net income) after taxes. If there is a “net loss” instead of a “net

income”, funds are not available for investor dividends.

17–54

188. A lower than average inventory turnover ratio indicates excellent inventory

management practices.

Feedback: Low inventory turnover ratio indicates the firm is not selling its inventory in a

timely manner, preventing the business from holding a larger cash position. Cash flow

problems can occur when a firm does not sell its inventory in a timely manner. It prevents

inventories from turning to cash.

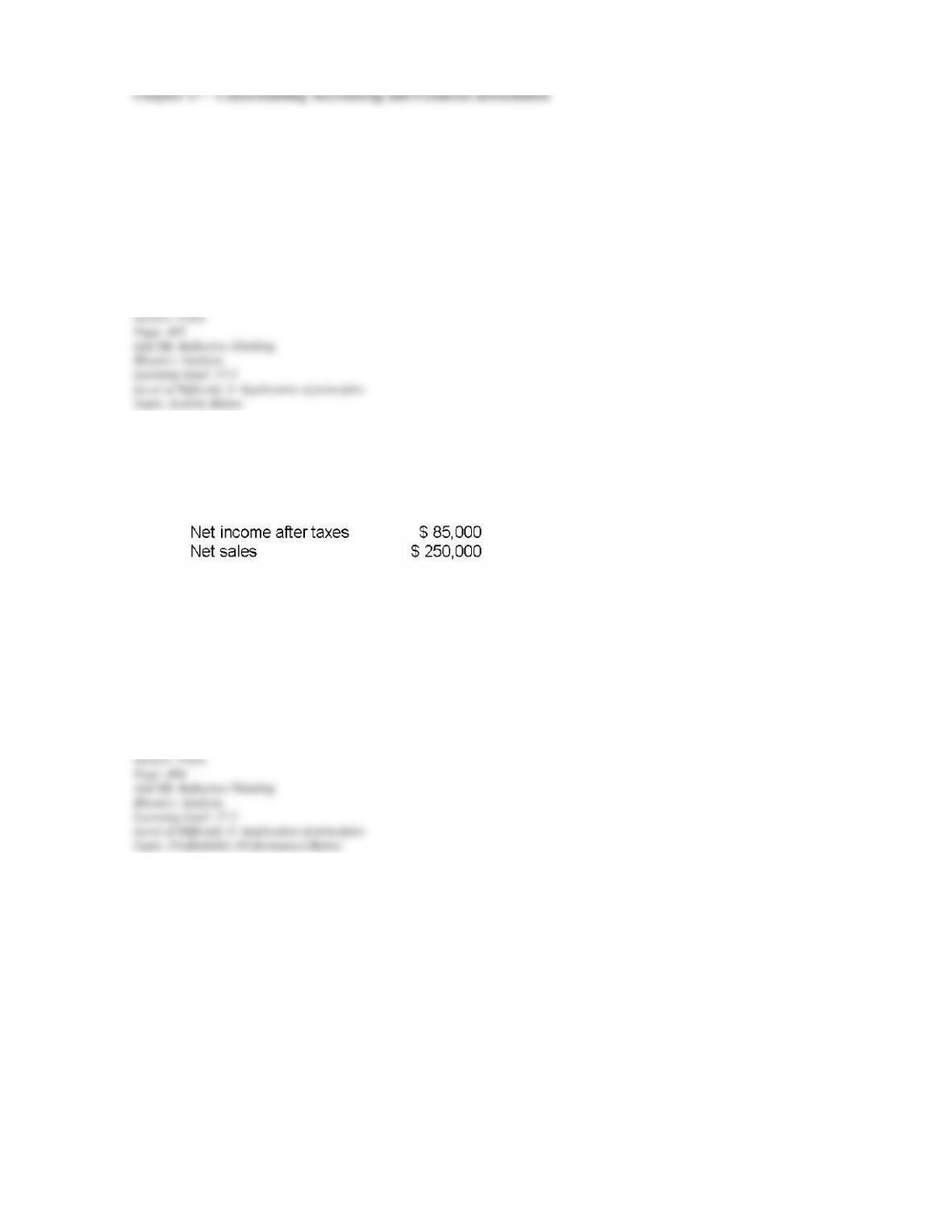

189. Preferred Pet Care, Inc., has recorded the following on its income statement for the

period ending, December 31, 2012:

The return on sales = 34%. This return is outstanding and there is no need to compare

this return to competitors in the veterinary services industry.

Feedback: While the calculation is accurate: Net income after taxes/net sales =

$85,000/$250,000 = .34 or 34%, in order to determine if this is a good return, the firm would

need to compare it with the ratio of competitor firms in the same industry.

190.

Chapter 17 – Understanding Accounting and Financial Information

Bark Three Times Pet Store’s accountant has recorded the following: Total current

assets = $60,000, including Cash = $24,000; Accounts Receivable = $20,000; and,

Inventory = $16,000. Total assets = $230,000; Total current liabilities = $48,000; and,

Total current and long-term liabilities = $98,000. The store’s current ratio = 1.25. The

store’s acid-test ratio = .92

Feedback: The current ratio = Total current assets/total current liabilities = $60,000/$48,000 =

1.25. The acid-test ratio = Cash + Accounts Receivables/total current liabilities = .92.

17–56

191. An important difference between accounting and other business functions, such as

marketing and management, is that:

A. Accounting functions must be performed by an “outsider” (rather than by an

employee of the business) in order to avoid conflicts of interest.

B. Accounting offers us insight into whether the business is financially sound.

C. Accounting involves mainly clerical activities and thus requires very little analysis.

D. Accounting deals exclusively with numbers.

192. To effectively run a business, it is necessary to:

A. Hire a full-time accountant.

B. Use a public accounting firm.

C. Understand and use accounting information.

D. Make certain that you do not spend too much time on your accounting system.

193. Which of the following is an example of a financial transaction?

A. A firm purchases a fire insurance policy.

B. An internal auditor discovers an error in a firm’s inventory valuation.

C. A potential customer accesses a firm’s Web page.

D. A manager reviews the financial statements prepared by an accountant.

17–58

197. The reports and financial statements prepared by accountants:

A. Are more useful for profit-seeking businesses than they are for not-for-profit

organizations.

B. Are mainly used to help the firm complete its tax forms.

C. Provide information that can be used by decision-makers both inside and outside the

organization.

D. Are not as useful now that firms have moved into a more global environment.

198. As an accountant, Joe Billing’s responsibilities include:

A. Developing plans to help his company establish a supply chain.

B. Setting prices for specific goods and services.

C. Summarizing and interpreting financial information needed by his firm’s managers.

D. Developing a fringe benefit program that improves employee morale.

Feedback: Accounting is the recording, classifying, summarizing, and interpreting of

financial events.

199.

Chapter 17 – Understanding Accounting and Financial Information

A person’s pulse rate and blood pressure are indicators of a person’s health. Similarly,

_________ can help assess the health of a business.

A. financial statements

B. production schedules

C. transactions

D. databases

Feedback: Financial statements can be used as diagnostic tools to identify existing and

potential problem areas.

200. Accounting transactions are very important to a firm’s operations. Which of the

following activities would affect the firm’s account balances?

A. Buying and selling goods and services

B. Interviewing prospective employees

C. Understanding economic reports

D. Forecasting consumer demand

Feedback: Accounting transactions will result in a change in two or more account balances.

Forecasting consumer demand implies that this has yet to occur. Understanding economic

reports does not require buying or selling items that would affect financial statements.

Interviewing prospective employees also does not require buying or selling items or

information. These therefore would not change any account balances.