Chapter 13: Pricing Concepts

CHAPTER SUMMARY AND LEARNING OBJECTIVES

LO 13.1 Describe the three foundations of pricing strategy.

Marketers consider three factors when establishing the price for a product: costs, potential

demand, and competition.

LO 13.2 Summarize the three pricing objectives.

LO 13.3 Calculate pricing using the markup and margin methods.

LO 13.4 Differentiate between fixed and variable costs.

A product’s total cost is composed of variable costs and fixed costs. Variable cost, such as raw

LO 13.5 Calculate breakeven point.

Breakeven analysis is the method for determining the amount of product that must be sold at a

given price to generate sufficient revenue to cover total costs—both fixed and variable.

LO 13.6 Describe how the cost–volume–profit relationship affects pricing strategy.

LO 13.7 Given cost information and pricing objectives, calculate the breakeven point for

a product.

To accurately assess the effect of pricing decisions on a company, a marketer must be able to

understand different pricing objectives, calculate prices using markup or margin goals,

categorize and calculate fixed and variable expenses, and determine breakeven points.

Chapter 13: Pricing Concepts

ACTIVATOR EXERCISE: Pricing a Disneyland Ticket

Purpose: To prompt discussion about price as an exchange of value.

Format: Small group discussion, then class discussion.

Time: 20–40 minutes, depending on format.

Activity: Divide students into small groups and ask them to discuss the following:

Disneyland charges a flat fee for admissions to the park. That fee gets you unlimited access to

rides, parades, and other attractions. There are a number of factors driving the price Disney

chooses.

Result: Students will have a wide range of opinions about what the “fair price” is, what changes

to the price or product would make it a better value, and how they measure Disney’s price

versus alternatives. These are all issues that drive pricing and relate directly to the three

Chapter 13: Pricing Concepts

LECTURE OUTLINE

13-1 Foundations of Pricing Strategy

In most economies, price refers to the amount of funds required to purchase a product. This

chapter discusses the process for determining a profitable but justifiable price. While there are a

number of factors to consider when building a pricing strategy, the three foundations are costs,

potential demand, and competition. This chapter and the next will build upon these three

concepts.

The Influence of Costs on Pricing Decisions

Marketers must calculate the costs associated with making their products and set a price that, at

a minimum, covers those costs.

While some companies might sell a product below the production costs for short-term

promotional purposes, this is not a sustainable strategy over the long term.

Potential Demand and Pricing Decisions

If costs represent the price floor, the price point at which no more customers are willing to buy

represents the price ceiling.

Competition and Pricing Decisions

Competition also affects a firm’s pricing strategy, perhaps even more than cost.

Chapter 13: Pricing Concepts

Classroom activity: For each of the following examples, ask all students to raise their hands

while you do a reverse auction. You’ll ask them how much they would pay for a particular

product or experience. You’ll start with a low price that presumably all students would be willing

to pay (since it will be below cost). Then go up in increments. Students will put their hands down

when you reach a price they would no longer be willing to pay. Eventually, only a few hands will

still be up.

What would you pay for an iPhone? (Start at $100 and go up in $100 increments.)

What would you pay for a pair of jeans? (Start at $10 and go up in $10 increments.)

First note: Students might ask, “how nice a pair of jeans?” or “how nice a car?” You can reply

that it would represent the ideal version of that product in their eyes—within existing limitations

of realism (i.e., the phone can’t offer tele-transportation, no matter how much you “bid”). They

also should bid based on their current financial capabilities.

Second note: After each reverse auction, have a brief discussion about why students chose the

way they did.

Key Takeaway: Pricing decisions are complex, but they are generally constrained by

three foundations: cost, potential demand, and competition.

Estimated time: 15–20 minutes

13-2 Pricing Objectives

While costs, potential demand, and competition are the foundations of pricing strategy, they

feed into more specific pricing objectives that align with a company’s overall goals.

Chapter 13: Pricing Concepts

Example: Alternatively, a company might seek to be perceived as the highest quality

producer of products in their category. As a result, they might utilize higher levels of

pricing to signal the prestige value of its product.

Discussion questions: What are some real-world examples of companies that fit the

Pricing objectives vary from firm to firm, and can be classified into three major groups: volume

or sales, competition, and prestige.

PRESENTATION VISUAL: MindTap Exhibit 13.2 showing the three major pricing

objectives

Objective

Purpose

Example

Volume or sales

objectives

Sales maximization

Market share

A car manufacturer pricing to ensure they sell

through their production capacity for the year

Vita Coco temporarily cutting prices on

coconut water to gain market share in the

Competition objectives

Competitive parity

Airlines and neighboring gas stations often

Volume or Sales Objectives

Discussion question: What are some drawbacks of using price cuts alone to increase sales

volume and market share?

Follow-up question: What are examples of times you depended on “sale” prices and switched

products when they returned to regular pricing?

Competition Objectives

Chapter 13: Pricing Concepts

mix and an easy tool for obtaining a differential advantage over competitors. However, when

competitors continually undercut each other to gain that advantage, it can lead to a price war

that damages all companies involved. Many firms attempt to promote stable prices by meeting

competitors’ prices, but not drastically undercutting them.

Discussion questions: As mentioned in MindTap, the airline industry is an example of one

where companies try to maintain the status quo with competitors? What are a few other

examples? (Possible answers: gasoline, movie tickets, autos, etc.)

What are some other examples of companies that try to avoid pricing comparison by offering a

solid value? These aren’t luxury products, but ones that might be sold for a slightly higher price

than competitors because they have higher perceived value due to quality, selection, or another

factor of the marketing mix. (Answer will vary)

Prestige Objectives

Prestige pricing establishes a relatively high price to develop and maintain an image of quality

that price difference can be explained by higher costs for the producer.

Key Takeaway: The three basic pricing objectives drive more specific decisions about

pricing policy, but can also drive branding decisions as well.

Estimated time: 15–25 minutes

13-3 Calculating Markup and Margin

Once managers have established pricing objectives, they can turn their attention to pricing

calculations. Markup and margin are two straightforward methods for calculating sales prices.

Cost-based pricing is using the product cost plus a target markup percentage to calculate the

sales price. Because the markup percentage is related to cost, this is called cost-based pricing.

Chapter 13: Pricing Concepts

The desired markup percentage is often based on industry norms, historical markup

percentages used by the business, or certain profitability objectives. To calculate the sales price

using markup, multiply the cost by one plus the target markup percentage.

Classroom activity: Divide students into groups and have them create their own markup story

problem. They should describe the business and specify what their markup target is (students

can choose this knowing that typical markups range anywhere from 50–200%, depending on

the product category). Finally, they should specify the manufacturing or wholesale cost of the

product they are selling.

who does understand.

Pricing Using Margin

A second pricing method is margin, or gross margin percentage, which is the portion of sales

revenue left over after paying product costs. Margin is also called gross profit.

Utilizing the margin approach enables firms to price their products to realize a desired

Chapter 13: Pricing Concepts

Sales Price = $100 / .65

Sales Price = $153.80

Classroom activity: This is a repeat of the above exercise, but now students are utilizing the

margin formula instead of the markup formula.

Divide students into groups and have them create their own margin story problem. They should

describe the business and specify what their margin target is (students can choose this knowing

that typical margins range anywhere from 20% to 80%, depending on the product category).

Finally, they should specify the manufacturing or wholesale cost of the product they are selling.

Note: You can then repeat the above classroom activity; however, groups can create a story

problem based on either margin or markup. This requires the rest of the class to select the

correct formula before calculating the answer. This ensures they can differentiate between the

two types of calculations.

While some incorrectly use the terms markup and margin interchangeably, it’s clear they are

different and should not be confused. Markup is a percentage added to the cost of the product

and margin is a percentage of the sales price left over after paying for the cost of the product.

The markup percentage is anchored to the cost and the margin percentage is anchored to the

selling price.

Key Takeaway: Markup and margin are two straightforward methods for calculating sales

prices. While some use these terms interchangeably, they are different and should not be

confused.

Chapter 13: Pricing Concepts

13-4 Fixed and Variable Costs

A product’s total cost is composed of total variable costs and total fixed costs.

Variable costs, such as raw materials and labor costs, change with the level of production.

Fixed costs, such as lease payments, administrative staffing, and insurance costs, remain

stable at any production level within a certain range.

Discussion questions: For the following items, raise your hand if you believe this is a variable

cost. Raise your hand if you believe this is a fixed cost. Everyone must vote on one or the other.

Nike running a TV ad (Answer: Fixed cost)

The rubber used in a Nike show (Answer: Variable cost)

The utility bill at Nike headquarters (Answer: Fixed cost)

to understand the difference in order to accurately calculate breakeven point later in the chapter.

Key Takeaway: A product’s total cost is composed of total variable costs and total fixed

costs. Understanding the difference is required in order to calculate profitable pricing

and accurate breakeven points.

Estimated time: 10–15 minutes

13-5 Breakeven Analysis

Note: As breakeven can be a difficult topic for students, the below notes include all the text as it

Chapter 13: Pricing Concepts

Breakeven analysis is the method for determining the amount of product that must be sold at a

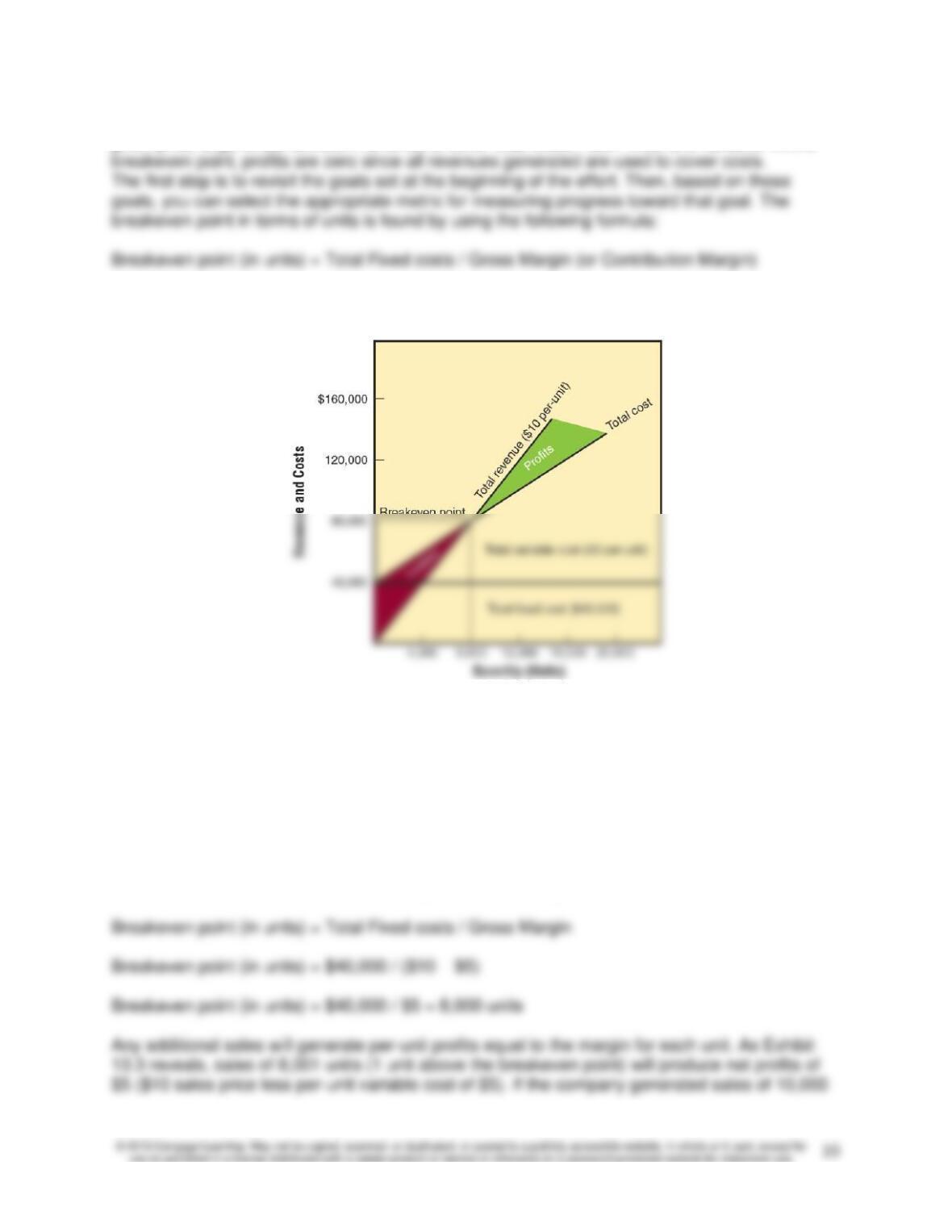

PRESENTATION VISUAL: MindTap Exhibit 13.3 showing a breakeven chart

Explaining the chart: Exhibit 13.3 graphically depicts the breakeven point. In this example, the

selling price is $10 and the variable cost is $5, providing a gross margin per unit of $5. This

gross margin is also called contribution margin, because that is how much a sale of each unit

“contributes” to covering fixed costs. In the chart, fixed costs of $40,000 are represented by the

horizontal line, which doesn’t change as the quantity produced goes up.

The total revenue curve begins at zero when no units are sold and no revenue is realized. As

units are sold, total revenue increases by the sales price of each unit sold.

The breakeven point is the point at which total revenue equals total cost. Returning to our

formula, we can calculate the breakeven point in this example as follows:

Chapter 13: Pricing Concepts

units, that would be 2,000 units beyond the breakeven point and its profit would be $10,000

(2,000 units × $5 contribution margin per unit).

A company can reduce breakeven point by reducing their fixed costs, reducing their variable

costs, or increasing sales price (which increases contribution margin per unit).

Breakeven is a cost-based model and does not directly address the crucial question of whether

consumers will purchase the product at the specified price. While a marketer can utilize a

number of price assumptions when calculating breakeven points, further research is needed to

validate whether those pricing and sales volume assumptions are realistic.

Classroom activity: Divide students into small groups and ask them to create two breakeven

story problems. Have them describe the business and the product it sells, the selling price, the

unit cost, and the company’s overall fixed costs. They should report the fixed costs as a lump

sum for now.

Key Takeaway: To calculate breakeven, divide fixed costs by your gross margin (or

contribution margin or gross profit) per unit.

Estimated time: 20–40 minutes