5-25. To answer the discussion questions, two forecasting models are required: a three-period

moving average and a three-period weighted moving average. Once the actual forecasts have

been made, their accuracy can be compared using the mean absolute differences (MAD).

a., b. Because a three-period average forecasting method is used, forecasts start for period 4.

Period

Month

Demand

Average

Weighted Average

4

Apr.

10

13.67

14.5

5

May

15

13.33

12.67

6

June

17

13.67

13.5

7

July

11

14

15.17

8

14

14.33

13.67

9

17

14

13.50

10

Oct.

12

14

15

11

14

14.33

14

12

Dec.

16

14.33

13.83

13

11

14

14.67

14

Feb.

13.67

13.17

c. MAD for moving average is 2.2. MAD for weighted average is 2.72. Moving average

forecast for February is 13.67. Weighted moving average forecast for February is 13.17.

Thus, based on this analysis, the moving average appears to be more accurate. The forecast

for February is about 14.

5-26. a. = 0.20

Sum of

Absolute

Actual

Forecast

Forecast

Week

Miles

(Ft)

Error

RSFE

Errors

MAD

Track Signal

1

17

17.00

—

—

—

—

—

2

21

17.00

+4.00

+4.00

4.00

4.00

1

3

19

17.80

+1.20

+5.20

5.20

2.60

2

4

23

18.04

+4.96

+10.16

10.16

3.39

3

7

20

18.26

+1.74

+8.04

15.76

2.63

3.05

9

22

18.49

+3.51

+10.94

19.88

2.49

4.21

10

20

19.19

+0.81

+11.75

20.69

2.30

5.11

12

22

18.48

+3.52

+10.92

28.56

2.60

4.20

b. The total MAD is 2.60.

c. RSFE is consistently positive. Tracking signal exceeds 2 MADs at week 10. This could

indicate a problem.

5-27. a., b. See the accompanying table for a comparison of the calculations for the exponential-

ly smoothed forecasts using constants of 0.1 and 0.6.

c. Students should note how stable the smoothed values for the 0.1 smoothing constant are.

Actual

Smoothed

Smoothed

Week,

Value,

Value,

Forecast

Value,

Forecast

t

Yt

Ft(

= 0.1)

Error

Ft(

= 0.6)

Error

1

50

50

—

—

2

35

50.00

-15.00

50.00

-15.00

3

25

48.50

-23.50

41.00

-16.00

4

40

46.15

-6.15

31.40

8.60

5

45

45.54

-0.54

36.56

8.44

6

35

45.48

-10.48

41.62

-6.62

7

20

44.43

-24.43

37.65

-17.65

8

30

41.99

-11.99

27.06

2.94

9

35

40.79

-5.79

28.82

6.18

10

20

40.21

-20.21

32.53

-12.53

11

15

38.19

-23.19

25.01

-10.01

12

40

35.87

4.13

19.00

21.00

13

55

36.28

18.72

31.60

23.40

14

35

38.16

-3.16

45.64

-10.64

15

25

37.84

-12.84

39.26

-14.26

16

55

36.56

18.44

30.70

24.30

17

55

38.40

16.60

45.28

9.72

18

40

40.06

-0.06

51.11

-11.11

19

35

40.05

-5.05

44.45

-9.45

20

60

39.55

20.45

38.78

21.22

21

75

41.59

33.41

51.51

23.49

22

50

44.93

5.07

65.60

-15.60

23

40

45.44

-5.44

56.24

-16.24

24

65

44.90

20.10

46.50

18.50

25

46.91

57.60

5-28. Using data from Problem 5-27, with = 0.9

Actual

Smoothed

Week,

Value,

Value,

Forecast

t

Yt

Ft(

= 0.9)

Error

1

50

50

—

2

35

50.00

-15.00

3

25

36.50

-11.50

4

40

26.15

13.85

5

45

38.62

6.39

6

35

44.36

-9.36

7

20

35.94

-15.94

8

30

21.59

8.41

9

35

29.16

5.84

10

20

34.42

-14.42

11

15

21.44

-6.44

12

40

15.64

24.36

13

55

37.56

17.44

14

35

53.26

-18.26

15

25

36.83

-11.83

16

55

26.18

28.82

17

55

52.12

2.88

18

40

54.71

-14.71

20

60

35.65

24.35

21

75

57.56

17.44

22

50

73.26

-23.26

23

40

52.33

-12.33

24

65

41.23

23.77

25

Note that in this problem, the initial forecast (for the first period) was not used in computing the

MAD = 14.48. Either approach is considered valid.

5-29. Exponential smoothing with = 0.1

Month

Income

Forecast

Error

Feb.

70.0

65.0

—

March

68.5

65.0 + 0.1(70 − 65) = 65.5

3.0

May

71.7

65.8 + 0.1(64.8 − 65.8) = 65.7

6.0

July

72.8

66.3 + 0.1(71.3 − 66.3) = 66.8

6.0

MAD = 4.20

Note that in this problem, the initial forecast (for the first period) was not used in computing the

MAD. Either approach is considered valid.

5-30. Exponential smoothing with = 0.3

Month

Income

Forecast

Error

Feb.

70.0

65.0

—

March

68.5

66.5

2.0

April

May

71.7

66.4

5.3

June

71.3

68.0

3.3

July

72.8

69.0

3.8

Based on MAD, = 0.3 produces a better forecast than = 0.1 (of Problem 5-29).

Note that in this problem, the initial forecast (for the first period) was not used in computing the

MAD. Either approach is considered valid.

5-31. Using QM for Windows, we select Forecasting – Time Series and multiplicative decompo-

sition. Then specify Centered Moving Average and we have the following results:

a. Quarter 1 index = 0.8825; Quarter 2 index = 0.9816; Quarter 3 index = 0.9712; Quarter 4

index = 1.1569

5-32. Letting

t = time period (1, 2, 3, . . . , 16)

Q1 = 1 if quarter 1, 0 otherwise

Q2 = 1 if quarter 2, 0 otherwise

5-33 a. Using computer software we get Y = 197.5 – 0.34X where X = time period.

The slope is -0.34 which indicates a small negative trend. Note that the results are not statistical-

ly significant and r2 = 0.001

b) Using QM for Windows for the multiplicative decomposition method with 4 seasons asnd

5-34. For a smoothing constant of 0.2, the forecast for year 11 is 6.489.

Year

Rate

Forecast

|Error|

1

7.2

7.2

0

2

7

7.2

0.2

3

6.2

7.16

0.96

4

5.5

6.968

1.468

5

5.3

6.674

1.374

6

5.5

6.400

0.900

7

6.7

6.220

0.480

8

7.4

6.316

1.084

9

6.8

6.533

0.267

6.1

6.586

0.486

6.489

For a smoothing constant of 0.4, the forecast for year 11 is 6.458.

Year

Rate

Forecast

|Error|

1

7.2

7.2

0

2

7

7.2

0.2

3

6.2

7.12

0.92

4

5.5

6.752

1.252

5

5.3

6.251

0.951

6

5.5

5.871

0.371

7

6.7

5.722

0.978

8

7.4

6.113

1.287

9

6.8

6.628

0.172

10

6.1

6.697

0.597

11

6.458

MAD = 0.673

For a smoothing constant of 0.6, the forecast for year 11 is 6.401.

Year

Rate

Forecast

|Error|

1

7.2

7.2

0

2

7

7.2

0.2

3

6.2

7.08

0.88

4

5.5

6.552

1.052

5

5.3

5.921

0.621

6

5.5

5.548

0.048

7

6.7

5.519

1.181

8

7.4

6.228

1.172

9

6.8

6.931

0.131

10

6.1

6.852

0.752

11

6.401

For a smoothing constant of 0.8, the forecast for year 11 is 6.256.

Year

Rate

Forecast

|Error|

1

7.2

7.2

0

2

7

7.2

0.2

3

6.2

7.04

0.84

4

5.5

6.368

0.868

5

5.3

5.674

0.374

6

5.5

5.375

0.125

7

6.7

5.475

1.225

8

7.4

6.455

0.945

9

6.8

7.211

0.411

6.1

6.882

0.782

6.256

The lowest MAD is 0.577 for a smoothing constant of 0.8.

5-35. To compute a seasonalized or adjusted sales forecast, we just multiply each seasonal index

by the appropriate trend forecast.

Ŷ = seasonal index Ŷtrend forecast

Hence for:

5-36.

(Average demand for season)

( ) ( )

year 1 demand year 2 demand

2

+

=

Overall average demand =

( )

sum of all values

8

Solution Table for Problem 5-36

Average

Year 1

Year 2

(Average Year

1-

Season

Season

Year 3

Season

Demand

Demand

Year 2 Demand)

Demand

Index

Demand

Fall

200

250

225.0

250

0.90

270

Winter

350

300

325.0

250

1.30

390

Spring

150

165

157.5

250

0.63

189

Summer

300

285

292.5

250

1.17

351

5-37. Using Excel with X = 1, 2, 3, …, 20 for years 1991-2010 respectively, the trend equation

is Y = 2898.6 + 499.7X.

For 2009, X = 21; Y = 2898.6 + 499.7 (21) = 13392

5-38. Using QM for Windows, the forecast is 10229 and the MSE = 2676625 (ignoring the first

5-39. a. With a smoothing constant of 0.4, the forecast for 2011 is 10609 with MSE =

3703109.(ignoring the first error)

b. Using QM for Windows, the best smoothing constant is 0.92. This gives the lowest MSE

of 2514990.

5-41. The forecast for January 2010 would be 1.452.

The MSE with the trend equation is 0.00049. The MSE with this exponential smoothing model is

0.00268.

SOLUTIONS TO INTERNET HOMEWORK PROBLEMS

5-44. The trend line found using Excel is: Patients = 29.73 + 3.28(time). Note these coefficients are

rounded. For the next 3 years (time = 11, 12, and 13) the forecasts for the number of patients are:

The coefficient of determination is 0.85, so the model is a fair model.

5-45. The trend line found using Excel is: Crime Rate = 51.98 + 6.09(time). Note these coeffi-

cients are rounded. For the next 3 years (time = 11, 12, and 13) the forecasts for the crime rates are:

Crime Rate = 51.98 + 6.09(11) = 118.97

Crime Rate = 51.98 + 6.09(13) = 131.15

The coefficient of determination is 0.96, so this is a very good model.

5-46. The regression equation (from Excel) is: Patients = 1.23 + 0.54(crime rate). Note these co-

efficients are rounded. If the crime rate is 131.2, the forecast number of patients is:

The coefficient of determination is 0.90, so this is a good model.

5-47. With

= 0.6, forecast for 2003 = 86.2 and MAD = 3.42. With

= 0.2, forecast for 2003 =

63.87 and MAD = 7.23. The model with

= 0.6 is better since it has a lower MAD.

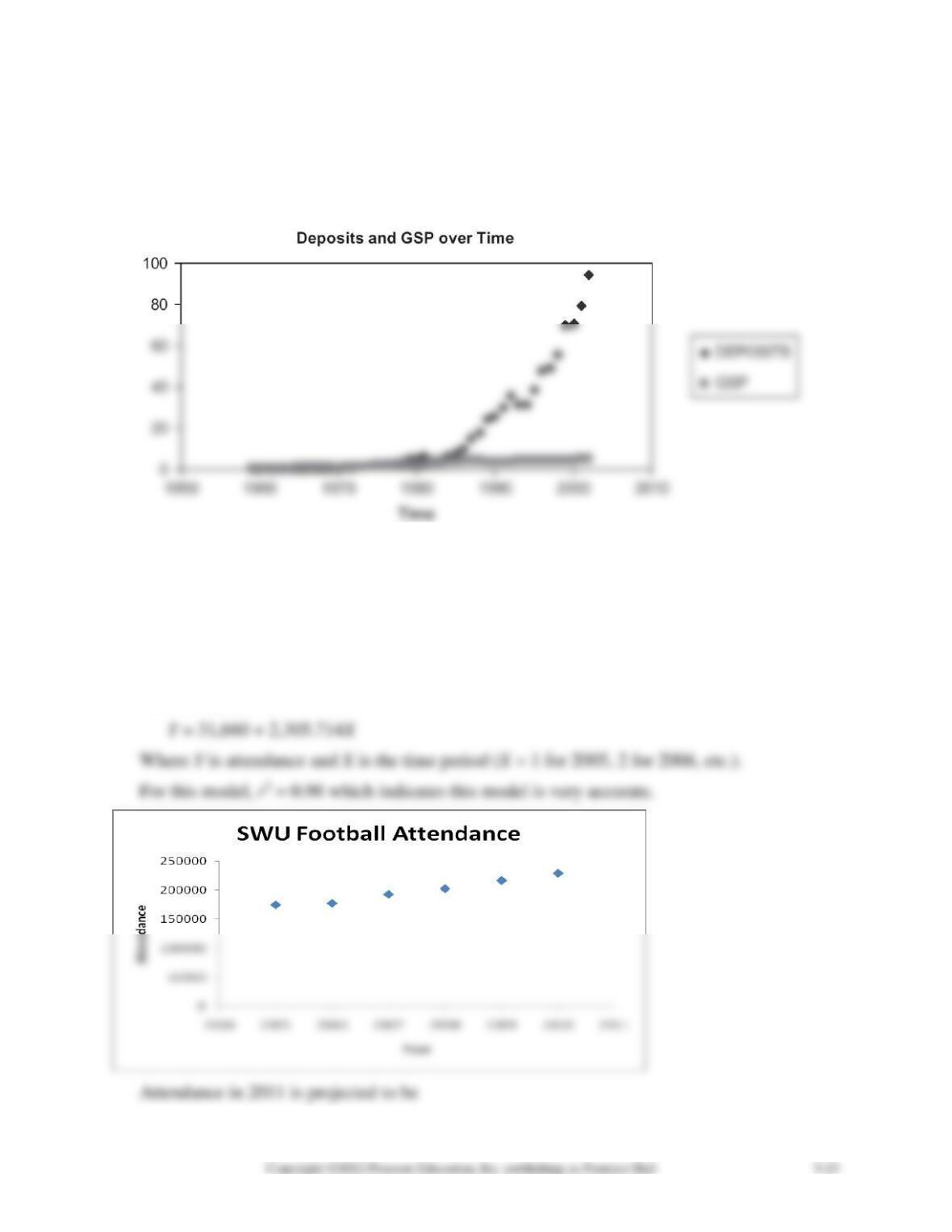

Deposits = –18.968 + 1.638(45) = 54.7

Deposits = –18.968 + 1.638(46) = 56.4

Deposits = –18.968 + 1.638(47) = 58.0

The trend line (coefficients from Excel are rounded) for GSP is:

5-50. The regression equation from Excel is

Deposits = –17.64 + 13.59(GSP)

In the scatterplot of this data that follows, the pattern appears to change around 1985. There are

definitely different relationships before 1985 and after 1985, so perhaps the model should be de-

veloped with 1985 as the first year of data.

CASE STUDIES

FORECASTING ATTENDANCE AT SWU FOOTBALL GAMES

1. Because we are interested in annual attendance and there are six years of data, we find the

average attendance in each year shown in the table below. A graph of this indicates a linear

trend in the data. Using Trend Analysis in the forecasting module of QM for Windows we

find the equation:

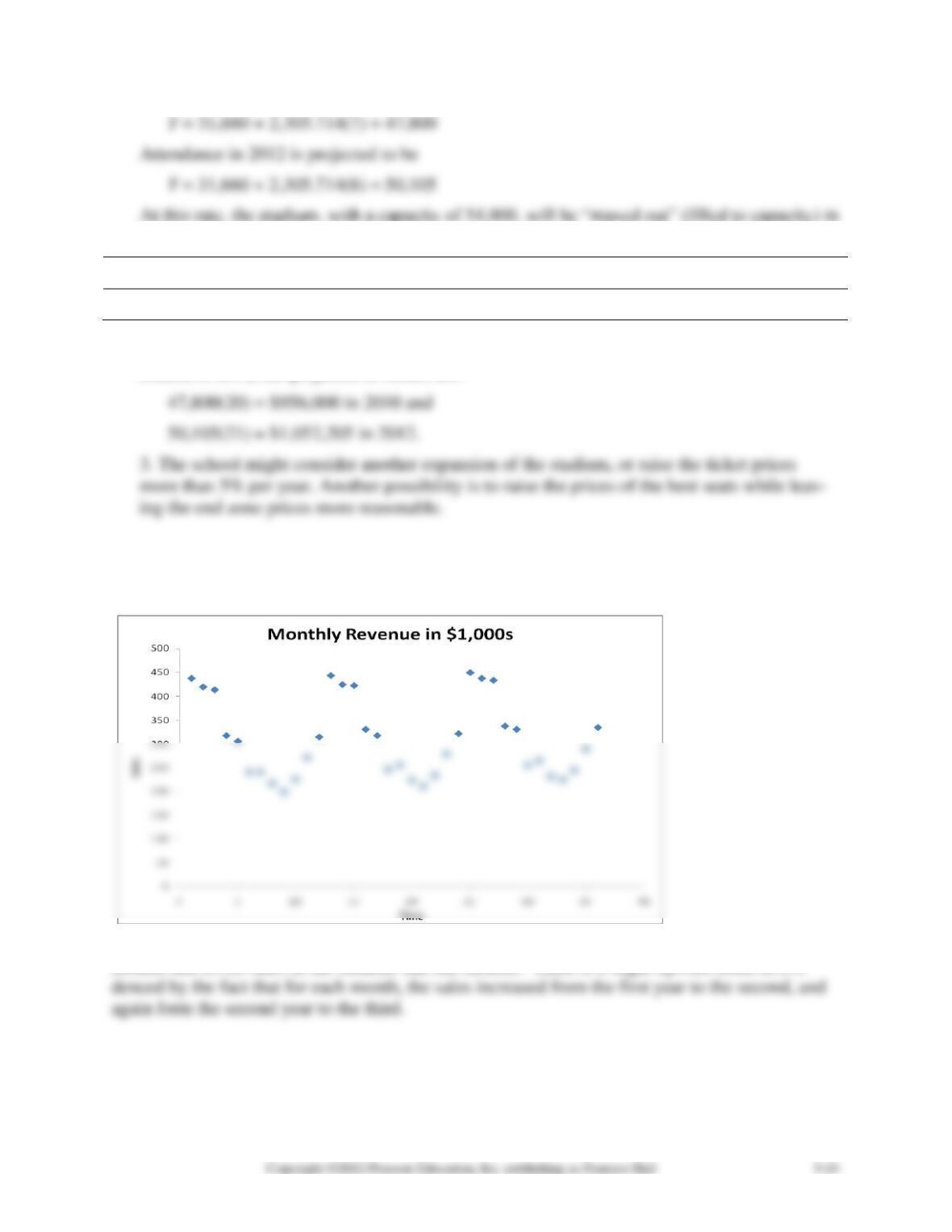

2014.

Year

2005

2006

2007

2008

2009

2010

Attendance

34840

35380

38520

40500

43320

45820

2. Based upon the projected attendance and tickets prices of $20 in 2011 and $21 (a 5% in-

crease) in 2012, the projected revenues are:

FORECASTING MONTHLY SALES

1.

The scatter plot of the data shows a definite seasonal pattern with higher sales in the winter

months and lower sales in the summer and fall months. There is a slight upward trend as evi-

2. A trend line based on the raw data is found to be:

Y = 330.889 – 1.162X

3. There is a definite seasonal pattern and a definite trend in the data. Using the decomposition

method in QM for Windows, the trend equation (based on the deseasonalized data) is

Month

Unadjusted forecast

Seasonal index

Adjusted forecast

January

325.852

1.447

471.5

February

326.711

1.393

455.1

March

327.57

1.379

451.7

April

328.429

1.074

352.7

329.288

1.039

342.1

330.147

0.797

263.1

331.006

0.813

269.1

August

331.865

0.720

238.9

332.724

0.667

221.9

October

333.583

0.747

249.2

334.442

0.891

298.0

335.301

1.033

346.4

SOLUTION TO INTERNET CASES

SOLUTION TO AKRON ZOOLOGICAL PARK CASE

1. The instructor can use this question to have the student calculate a simple linear regression,

using real-world data. The attendance would be the dependent variable and time would be the

independent variable. From the attendance, the expected revenues could be determined. Also, the

r = 0.88

MAD = 9,662

2. The student should respond that the other factors are the variability of the weather, the special

events, the competition, and the role of advertising.