Chapter 18

Long-Term Debt Financing

Lecture Outline

Financing to Match the Inflow Currency

Using Currency Swaps to Execute the Matching Strategy

Using Parallel Loans to Execute the Matching Strategy

Debt Denomination Decision by Subsidiaries

Debt Decision in Host Countries with High Interest Rates

Debt Denomination to Finance a Foreign Project

Long-Term Debt Financing ❖ 2

Chapter Theme

Should the MNC choose bonds as a medium to attract long-term funds, a currency for denomination

must be chosen. This is a critical decision for the MNC. While there is no clear-cut solution, this chapter

Topics to Stimulate Class Discussion

1. Why would U.S. firms consider issuing bonds denominated in a foreign currency?

2. What are the desirable characteristics related to a currency’s interest rate (high or low) and value

(strong or weak) that would make the currency attractive from a borrower’s perspective?

POINT/COUNTER-POINT:

Will Currency Swaps Result in Low Financing Costs?

POINT: Yes. Currency swaps have created greater participation by firms that need to exchange their

currencies in the future. Thus, firms that finance in a low interest rate currency can more easily establish

an agreement to obtain the currency that has the low interest rate.

COUNTER-POINT: No. Currency swaps will establish an exchange rate that is based on market forces. If

a forward rate exists for a future period, the swap rate should be somewhat similar to the forward rate. If it

was not as attractive as the forward rate, the participants would use the forward market instead. If a

forward market does not exist for the currency, the swap rate should still reflect market forces. The

exchange rate at which a low-interest currency could be purchased will be higher than the prevailing spot

rate, since otherwise MNCs would borrow the low-interest currency and simultaneously purchase the

currency forward so that they could hedge their future interest payments.

WHO IS CORRECT? Use the Internet to learn more about this issue. Which argument do you support?

Offer your own opinion on this issue.

Answers to End of Chapter Questions

1. Floating-Rate Bonds.

a. What factors should be considered by a U.S. firm that plans to issue a floating rate bond

denominated in a foreign currency?

Long-Term Debt Financing ❖ 3

b. Is the risk of issuing a floating rate bond higher or lower than the risk of issuing a fixed rate

Eurobond? Explain.

c. How would an investing firm differ from a borrowing firm in the features (i.e., interest rate and

currency’s future exchange rates) it would prefer a floating rate foreign currency-denominated

bond to exhibit?

ANSWER: An investing firm prefers a bond denominated in a currency that is expected to appreciate

2. Risk From Issuing Foreign Currency-Denominated Bonds. What is the advantage of using

simulation to assess the bond financing position?

3. Exchange Rate Effects.

a. Explain the difference in the cost of financing with foreign currencies during a strong-dollar

period, versus a weak-dollar period for a U.S. firm.

b. Explain how a U.S.-based MNC issuing bonds denominated in euros may be able to offset a

portion of its exchange rate risk.

4. Bond Offering Decision. Columbia Corp. is a U.S. company with no foreign currency cash flows. It

plans to either issue a bond denominated in euros with a fixed interest rate, or a bond denominated in

U.S. dollars with a floating interest rate. It estimates its periodic dollar cash flows for each bond.

Which bond do you think would have greater uncertainty surrounding these future dollar cash flows?

Explain.

5. Borrowing Combined with Forward Hedging. Cedar Falls Co. has a subsidiary in Brazil, where

local interest rates are high. It considers borrowing dollars and hedging the exchange rate risk by

Long-Term Debt Financing ❖ 4

selling the Brazilian real forward in exchange for dollars for the periods in which it would need to

make loan payments in dollars. Assume that forward contracts on the real are available. What is the

limitation of this strategy? ?

6. Financing That Reduces Exchange Rate Risk. Kerr, Inc., a major U.S. exporter of products to

Japan, denominates its exports in dollars and has no other international business. It can borrow

dollars at 9 percent to finance its operations or borrow yen at 3 percent. If it borrows yen, it will be

exposed to exchange rate risk. How can Kerr borrow yen and possibly reduce its economic exposure

to exchange rate risk?

7. Exchange Rate Effects. Katina, Inc., is a U.S. firm that plans to finance with bonds denominated in

euros to obtain a lower interest rate than is available on dollar-denominated bonds. What is the most

critical point in time when the exchange rate will have the greatest impact?

8. Financing Decision. Ivax Corp. (based in Miami) is a U.S. drug company that has attempted to

capitalize on new opportunities to expand in Eastern Europe. The production costs in most Eastern

European countries are very low, often less than one-fourth of the cost in Germany or Switzerland.

Furthermore, there is a strong demand for drugs in Eastern Europe. Ivax penetrated Eastern Europe by

purchasing a 60 percent stake in Galena AS, a Czech firm that produces drugs.

a. Should Ivax finance its investment in the Czech firm by borrowing dollars from a U.S. bank that

would then be converted into koruna (the Czech currency) or by borrowing koruna from a local

Czech bank? What information do you need to know to answer this question?

ANSWER: Ivax would need to consider the interest rate in the U.S. versus the interest rate when

borrowing koruna (the Czech currency). It would also need to consider the potential change in the

b. How can borrowing koruna locally from a Czech bank reduce the exposure of Ivax to exchange

rate risk?

Long-Term Debt Financing ❖ 5

c. How can borrowing koruna locally from a Czech bank reduce the exposure of Ivax to political

risk caused by government regulations?

Advanced Questions

9. Bond Financing Analysis. Sambuka, Inc. can issue bonds in either U.S. dollars or in Swiss francs.

Dollar-denominated bonds would have a coupon rate of 15 percent; Swiss franc-denominated bonds

would have a coupon rate of 12 percent. Assuming that Sambuka can issue bonds worth $10,000,000

in either currency, that the current exchange rate of the Swiss franc is $.70, and that the forecasted

exchange rate of the franc in each of the next three years is $.75, what is the annual cost of financing

for the franc-denominated bonds? Which type of bond should Sambuka issue?

ANSWER:

If Sambuka issues Swiss franc-denominated bonds, the bonds would have a face value of

10. Bond Financing Analysis. Hawaii Co. just agreed to a long-term deal in which it will export products

to Japan. It needs funds to finance the production of the products that it will export. The products will

be denominated in dollars. The prevailing U.S. long-term interest rate is 9 percent versus 3 percent in

Japan. Assume that interest rate parity exists, and that Hawaii Co. believes that the international

Fisher effect holds.

a. Should Hawaii Co. finance its production with yen and leave itself open to the exchange rate

risk? Explain.

b. Should Hawaii Co. finance its production with yen and simultaneously engage in forward

contracts to hedge its exposure to exchange rate risk?

Long-Term Debt Financing ❖ 6

c. How could Hawaii Co. achieve low-cost financing while eliminating its exposure to exchange

rate risk?

11. Cost of Financing. Assume that Seminole, Inc., considers issuing a Singapore dollar-denominated

bond at its present coupon rate of 7 percent, even though it has no incoming cash flows to cover the

bond payments. It is attracted to the low financing rate, since U. S. dollar-denominated bonds issued

in the United States would have a coupon rate of 12 percent. Assume that either type of bond would

have a four-year maturity and could be issued at par value. Seminole needs to borrow $10 million.

Therefore, it will either issue U. S. dollar denominated bonds with a par value of $10 million or bonds

denominated in Singapore dollars with a par value of S$20 million. The spot rate of the Singapore

dollar is $.50. Seminole has forecasted the Singapore dollar’s value at the end of each of the next

four years, when coupon payments are to be paid:

End of Year Exchange Rate of Singapore Dollar

1 $.52

2 .56

3 .58

4 .53

Determine the expected annual cost of financing with Singapore dollars. Should Seminole, Inc., issue

bonds denominated in U.S. dollars or Singapore dollars? Explain.

ANSWER:

End of Year:

1

2

3

4

12. Interaction Between Financing and Invoicing Policies. Assume that Hurricane, Inc., is a U.S.

company that exports products to the U.K., invoiced in dollars. It also exports products to Denmark,

invoiced in dollars. It currently has no cash outflows in foreign currencies, and it plans to issue bonds

in the near future. Hurricane could likely issue bonds at par value in (1) dollars with a coupon rate of

12 percent, (2) Danish kroner with a coupon rate of 9 percent, or (3) pounds with a coupon rate of 15

percent. It expects the kroner and pound to strengthen over time. How could Hurricane revise its

invoicing policy and make its bond denomination decision to achieve low financing costs without

excessive exposure to exchange rate fluctuations?

Long-Term Debt Financing ❖ 7

ANSWER: Hurricane could invoice goods exported to Denmark in kroner instead of dollars. Thus, it

13. Swap Agreement. Grant, Inc., is a well-known U.S. firm that needs to borrow 10 million British

pounds to support a new business in the United Kingdom. However, it cannot obtain financing from

British banks because it is not yet established within the United Kingdom. It decides to issue dollar-

denominated debt (at par value) in the U.S., for which it will pay an annual coupon rate of 10%. It

then will convert the dollar proceeds from the debt issue into British pounds at the prevailing spot rate

(the prevailing spot rate is one pound = $1.70). Over each of the next three years, it plans to use the

revenue in pounds from the new business in the United Kingdom to make its annual debt payment.

Grant, Inc., engages in a currency swap in which it will convert pounds to dollars at an exchange rate

of $1.70 per pound at the end of each of the next three years. How many dollars must be borrowed

initially to support the new business in the United Kingdom? How many pounds should Grant, Inc.,

specify in the swap agreement that it will swap over each of the next three years in exchange for

dollars so that it can make its annual coupon payments to the U.S. creditors?

14. Interest Rate Swap. Janutis Co. has just issued fixed rate debt at 10 percent. Yet, it prefers to

convert its financing to incur a floating rate on its debt. It engages in an interest rate swap in which it

swaps variable rate payments of LIBOR plus 1% in exchange for payments of 10%. The interest

rates are applied to an amount that represents the principal from its recent debt issue in order to

determine the interest payments due at the end of each year for the next three years. Janutis Co.

expects that the LIBOR will be 9% at the end of the first year, 8.5% at the end of the second year, and

7% at the end of the third year. Determine the financing rate that Janutis Co. expects to pay on its

debt after considering the effect of the interest rate swap.

ANSWER: The fixed rate of 10% to be received from the interest rate swap offsets the 10%

15. Financing and the Currency Swap Decision. Bradenton Co. is considering a project in which it will

export special contact lenses to Mexico. It expects that it will receive 1 million pesos after taxes at the

end of each year for the next 4 years, and after that time its business in Mexico will end as its special

patent will be terminated. The peso’s spot rate is presently $.20. The U.S. annual risk-free interest rate

is 6% while Mexico’s annual risk-free interest rate is 11%. Interest rate parity exists. Bradenton Co.

uses the one-year forward rate as a predictor of the exchange rate in one year. Bradenton Co. also

presumes that the exchange rates in each of the years 2 through 4 will also change by the same

Long-Term Debt Financing ❖ 8

percentage as it predicts for year 1. Bradenton searches for a firm with which it can swap pesos for

dollars over each of the next 4 years. Briggs Co. is an importer of Mexican products. It is willing to

take the 1 million pesos per year from Bradenton Co. and will provide Bradenton Co. with dollars at

an exchange rate of $.17 per peso. Ignore tax effects.

Bradenton Co. has a capital structure of 60% debt and 40% equity. Its corporate tax rate is 30%. It

borrows funds from a bank and pays 10% interest on its debt. It expects that the U.S. annual stock

market return will be 18% per year. Its beta is .9. Bradenton would use its cost of capital as the

required return for this project.

a. Determine whether the NPV of this project if Bradenton engages in the currency swap.

b. Determine the NPV of this project if Bradenton does not hedge the future cash flows.

ANSWER:

a) No hedge

Year 1

Year 2

Year 3

Year 4

After tax profit

in MXP

MXP1,000,000

MXP1,000,000

MXP1,000,000

MXP1,000,000

Long-Term Debt Financing ❖ 9

b) Swap

Year 1

Year 2

Year 3

Year 4

Cash Flow to

PV (discount

After tax profit

16. Financing and Exchange Rate Risk. The parent of Nester Co. (a U.S. firm) has no international

business but plans to invest $20 million in a business in Switzerland. Since the operating costs of this

business are very low, Nester Co. expects this business to generate much cash flows in Swiss francs

that will be remitted to the parent each year.

Nester will finance half of this project with debt. It has these choices for financing the project:

* obtain half of the funds needed from parent equity and the other half by borrowing dollars

* obtain half of the funds needed from parent equity and the other half by borrowing Swiss francs

* obtain half of the funds that are needed from parent equity and obtain the remainder by borrowing

an equal amount of dollars and Swiss francs

The interest rate on dollars is the same as the interest rate on Swiss francs.

a. Which choice will result in the most exchange rate exposure?

b. Which choice will result in the least exchange rate exposure?

c. If the Swiss franc was expected to appreciate over time, which financing choice would result in the

highest expected net present value?

ANSWER:

17. Financing and Exchange Rate Risk. Vix Co. (of the U.S.) presently serves as a distributor of

products by purchasing them from other U.S. firms and selling them in Europe. It wants to purchase a

manufacturer in Thailand that could produce similar products at a low cost (due to low labor costs in

Thailand) and export the products to Europe. The operating expenses would be denominated in Thai

currency (the baht). The products would be invoiced in euros. If Vix Co. can acquire a manufacturer,

it will discontinue its existing distributor business. If Vix Co. purchases a company in Thailand, it

expects that its revenue might not be sufficient to cover its operating expenses during the first 8 years.

It will need to borrow funds for an 8-year term to ensure that it has enough funds to pay all of its

operating expenses in Thailand. It can borrow funds denominated in U.S. dollars, in Thai baht, or in

euros. Assuming that its financing decision will be primarily intended to minimize its exposure to

exchange rate risk, which currency should it borrow? Briefly explain.

Long-Term Debt Financing ❖ 10

18. Financing and Exchange Rate Risk. Compton Co. has a subsidiary in Thailand that produces

computer components. The subsidiary sells the components to manufacturers in the U.S. The

components are invoiced in U.S. dollars. Compton pays employees of the subsidiary in Thai baht and

makes a large monthly lease payment in Thai baht. Compton financed the investment in the Thai

subsidiary by borrowing dollars from a U.S. bank. Compton has no other international business.

a. Given the conditions, is Compton affected favorably or unfavorably, or not affected by depreciation

of the Thai baht? Briefly explain.

b. Assume that interest rates in Thailand declined recently, so Compton subsidiary considers

obtaining a new loan in Thai baht. Compton would use the proceeds to pay off its existing loan from a

U.S. bank. Will this form of financing increase, reduce, or have no impact on its economic exposure

to exchange rate movements? Briefly explain.

19. Selecting a Loan Maturity. Omaha Co. has a subsidiary in Chile that wants to borrow from a local

bank at a fixed rate over the next 10 years.

a. Explain why Chile’s term structure of interest rates (as reflected in its yield curve) might cause the

subsidiary to borrow for a different term to maturity.

b. If Omaha is offered a more favorable interest rate for a term of 6 years, explain the potential

disadvantage compared to a 10-year loan.

c. Explain how the subsidiary can determine whether to select the 6-year loan versus the 10-year loan.

ANSWER

20. Project Financing. Dryden Co. is a U.S. firm that plans a foreign project in which it needs

$8,000,000 as an initial investment. The project is expected to generate cash flows of 10 million euros

in one year, after the complete repayment of the loan (including the loan interest and principal). The

project has zero salvage value and is terminated at the end of one year. Dryden considers financing

this project with:

*all U.S. equity,

*all U.S. debt (loans) denominated in dollars provided by U.S. banks,

*all debt (loans) denominated in euros provided by European banks, or

*half of funds obtained from loans denominated in euros, and half obtained from loans denominated

in dollars.

Which form of financing will cause the project’s NPV to be the least sensitive to exchange rate risk?

Solution to Continuing Case Problem: Blades, Inc.

1. Given that Blades expects to use the cash flows generated by the Thai subsidiary to pay the interest

and principal of the notes, would the effective financing cost of the baht-denominated notes be

affected by exchange rate movements? Would the effective financing cost of the yen-denominated

notes be affected by exchange rate movements? How?

2. Construct a spreadsheet to determine the annual effective financing percentage cost of the yen-

denominated notes issued in each of the three scenarios for the future value of the yen. What is the

probability that the financing cost of issuing yen-denominated notes is lower than the cost of issuing

baht-denominated notes?

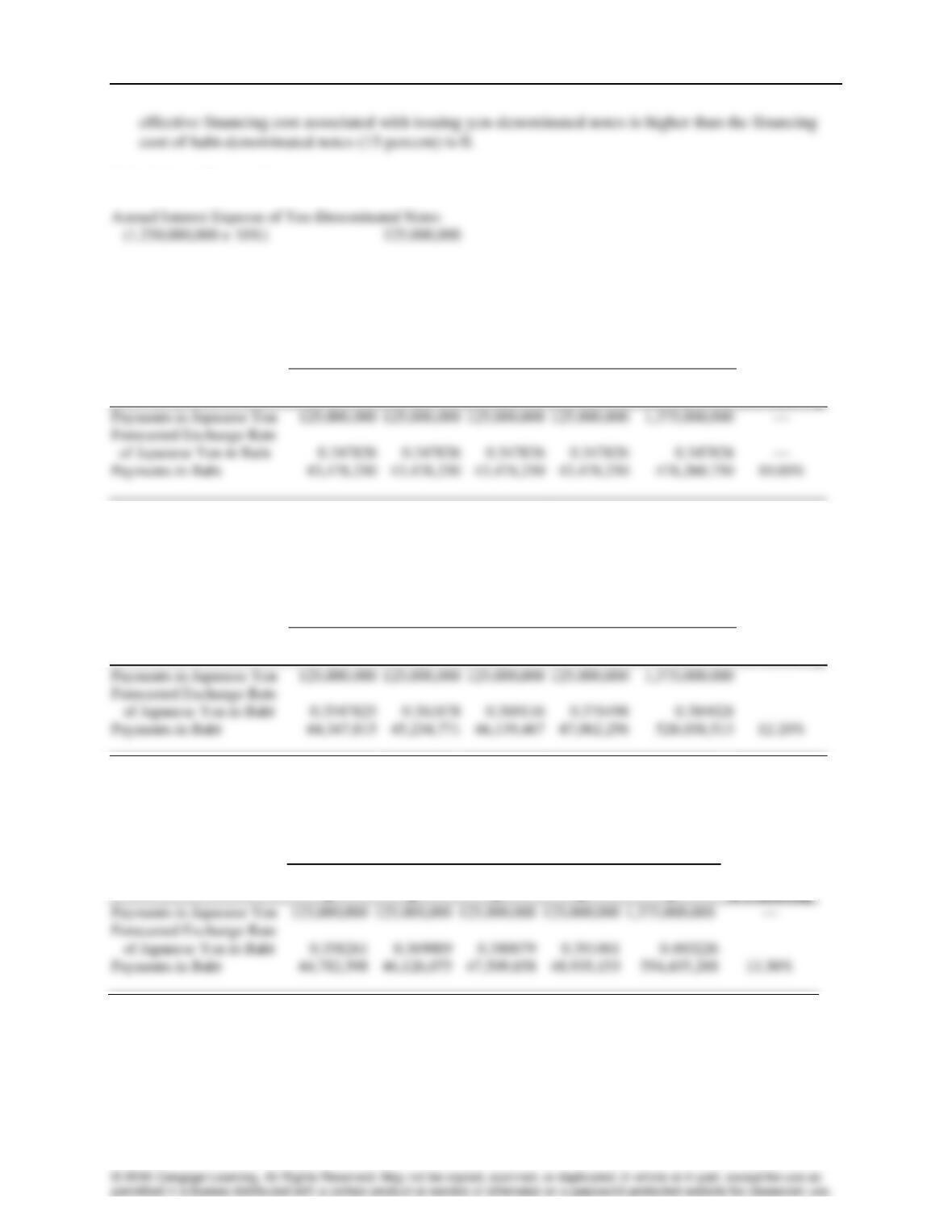

Long-Term Debt Financing ❖ 12

Calculation of Interest Expense:

Annual Interest Expense of Yen-Denominated Notes

(1) Yen Value Changes

by 0 Percent Annually

Relative to the Baht

End of

Year:

Annual Cost

1

2

3

4

5

of Financing

Payments in Japanese Yen

Payments in Baht

(2) Yen Value Changes

by 2 Percent

Annually Relative

to the Baht

End of

Year:

Annual Cost

1

2

3

4

5

of Financing

Payments in Japanese Yen

Payments in Baht

(3) Yen Value Changes

by 3 Percent Annually

Relative to the Baht

End of

Year:

Annual Cost

1

2

3

4

5

of Financing

Payments in Japanese Yen

1,375,000,000

Payments in Baht

3. Using a spreadsheet, determine the expected annual effective financing percentage cost of issuing

yen-denominated notes. How does this expected financing cost compare with the expected financing

cost of the baht-denominated notes?

Long-Term Debt Financing ❖ 13

(1)

(2)

(3) = (1) × (2)

Exchange Rate Scenario

Effective Financing

Percentage Cost

Probability

Product

Scenario 1: No Change in Yen Value

2.00%

4. Based on your answers to the previous questions, do you think Blades should issue yen- or baht-

denominated notes?

5. What is the tradeoff involved?

Solution to Supplemental Case: Devil VCR Corporation

a. It can reduce its exposure to exchange rate risk, because it could convert the proceeds of the bond

into pounds to cover future production expenses and could use a portion of the revenue in

Singapore dollars each year to pay its coupon payments to bondholders.

b. This approach would increase Devil VCR’s exchange rate risk, because it already has expenses in

pounds and no revenue in pounds.

c. This approach would not reduce the exchange rate risk resulting from the exporting program,

because it is not offsetting the revenue received in Singapore dollars.

Small Business Dilemma

Long-Term Financing Decision by the Sports Exports Company

The Sports Exports Company continues to focus on producing footballs in the U.S. and exporting them to

the United Kingdom. The exports are denominated in pounds, which has continually exposed the firm to

exchange rate risk. It is now considering a new form of expansion where it would sell specialty sporting

goods in the U.S. If it pursues this U.S. project, it would need to borrow long-term funds. The dollar-

denominated debt has an interest rate that is slightly lower than the pound-denominated debt.

1. Jim Logan, owner of the Sports Exports Company, needs to determine whether dollar-denominated

debt or pound-denominated debt would be most appropriate for financing this expansion, if he does

expand. He is leaning toward financing the U.S. project with dollar-denominated debt, since his goal

is to avoid exchange rate risk. Is there any reason why he should consider using pound-denominated

debt to reduce exchange rate risk?

2. Assume that Jim decides to finance his proposed U.S. business with dollar-denominated debt if he

does implement the U.S. business idea. How could he use a currency swap along with the debt to

reduce the firm’s exposure to exchange rate risk?

Long-Term Debt Financing ❖ 15

Part 4 — Integrative Problem

Long-Term Asset and Liability Management

Gandor Company is a U.S. firm that is considering a joint venture with a Chinese firm to produce and sell

DVDs. Gandor will invest $12 million in this project, which will help to finance the Chinese firm’s

production. For each of the first three years, 50 percent of the total profits will be distributed to the

Chinese firm, while the remaining 50 percent will be converted to dollars to be sent to the U.S. The

Chinese government intends to impose a 20 percent income tax on the profits distributed to Gandor. The

Chinese government has guaranteed that the after-tax profits (denominated in yuan, the Chinese currency)

can be converted to U.S. dollars at an exchange rate of CHY1 = $.20 per unit and sent to Gandor

Company each year. At the present time, no withholding tax is imposed on profits sent to the U.S. as a

result of joint ventures in China. Assume that even after considering the taxes paid in China, an

additional 10 percent tax imposed by the U.S. government on profits received by Gandor Company.

After the first three years, all profits earned are allocated to the Chinese firm.

The expected total profits resulting from the joint venture per year are as follows:

Year

Total Profits from Joint

Venture (in yuan, CHY)

1

CHY60 million

2

CHY80 million

3

CHY100 million

Gandor’s average cost of debt is 13.8 percent before taxes. Its average cost of equity is 18 percent.

Assume that the corporate income tax rate imposed on Gandor is normally 30 percent. Gandor uses a

capital structure composed of 60 percent debt and 40 percent equity. Gandor automatically adds 4

percentage points to its cost of capital when deriving its required rate of return on international joint

ventures. Though this project has particular forms of country risk that are unique, Gandor plans to

account for these forms of risk within its estimation of cash flows.

Gandor is concerned about two forms of country risk. First, there is the risk that the Chinese government

will increase the corporate income tax rate from 20 percent to 40 percent (20 percent probability). If this

occurs, additional tax credits will be allowed, resulting in no U.S. taxes on the profits from this joint

venture. Second, there is the risk that the Chinese government will impose a withholding tax of 10

percent on the profits that are sent to the U.S. (20 percent probability). In this case, additional tax credits

will not be allowed, and Gandor will still be subject to a 10 percent U.S. tax on profits received from

China. Assume that the two types of country risk are mutually exclusive. This is, the Chinese

government will adjust only one of its taxes (the income tax or the withholding tax), if any.

1. Determine Gandor’s cost of capital. Also, determine Gandor’s required rate of return for the joint

venture in China.

Long-Term Debt Financing ❖ 16

ANSWER: Gandor’s weighted average cost of capital is:

( )

kc

D

D E kd1 t E

D E ke

=+

− + +

2. Determine the probability distribution of Gandor’s net present values for the joint venture.

Capital budgeting analyses should be conducted for these scenarios:

• Scenario 1 Based on original assumptions.

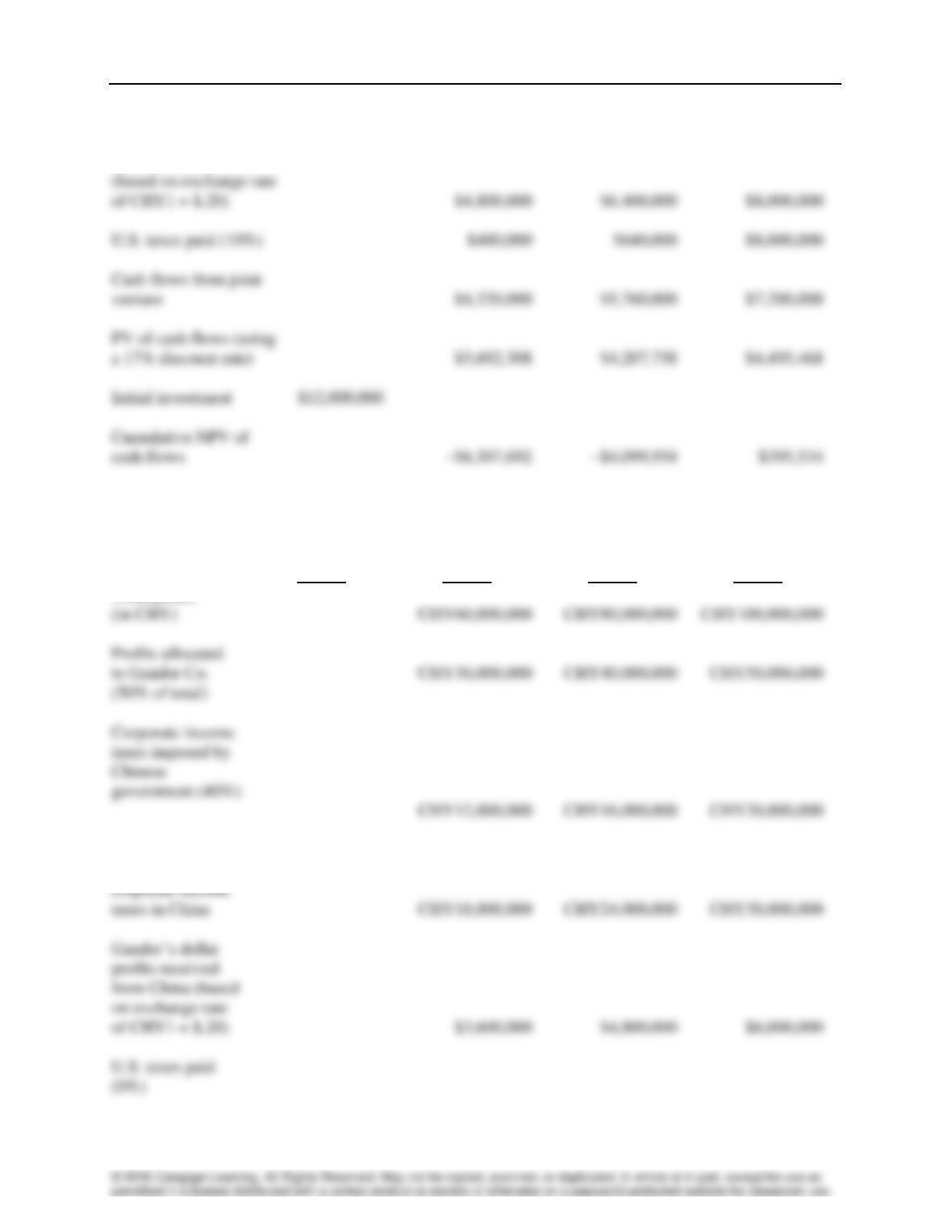

SCENARIO 1: BASED ON ORIGINAL ASSUMPTIONS

(Probability = 60%)

Year 0

Year 1

Year 2

Year 3

Total profits

(in CHY)

CHY60,000,000

CHY80,000,000

CHY100,000,000

Gandor Co.

imposed by Chinese

government (20%)

CHY10,000,000

paying corporate

Long-Term Debt Financing ❖ 17

(based on exchange rate

Cash flows from joint

PV of cash flows (using

Gandor’s dollar profits

received from China

SCENARIO 2: BASED ON INCREASE IN CORPORATE INCOME TAX BY CHINESE GOVERNMENT

(Probability = 20%)

Year 0

Year 1

Year 2

Year 3

Profits allocated

to Gandor Co.

Corporate income

government (40%)

Total profits

from China (based

on exchange rate

Profits to Gandor

after paying

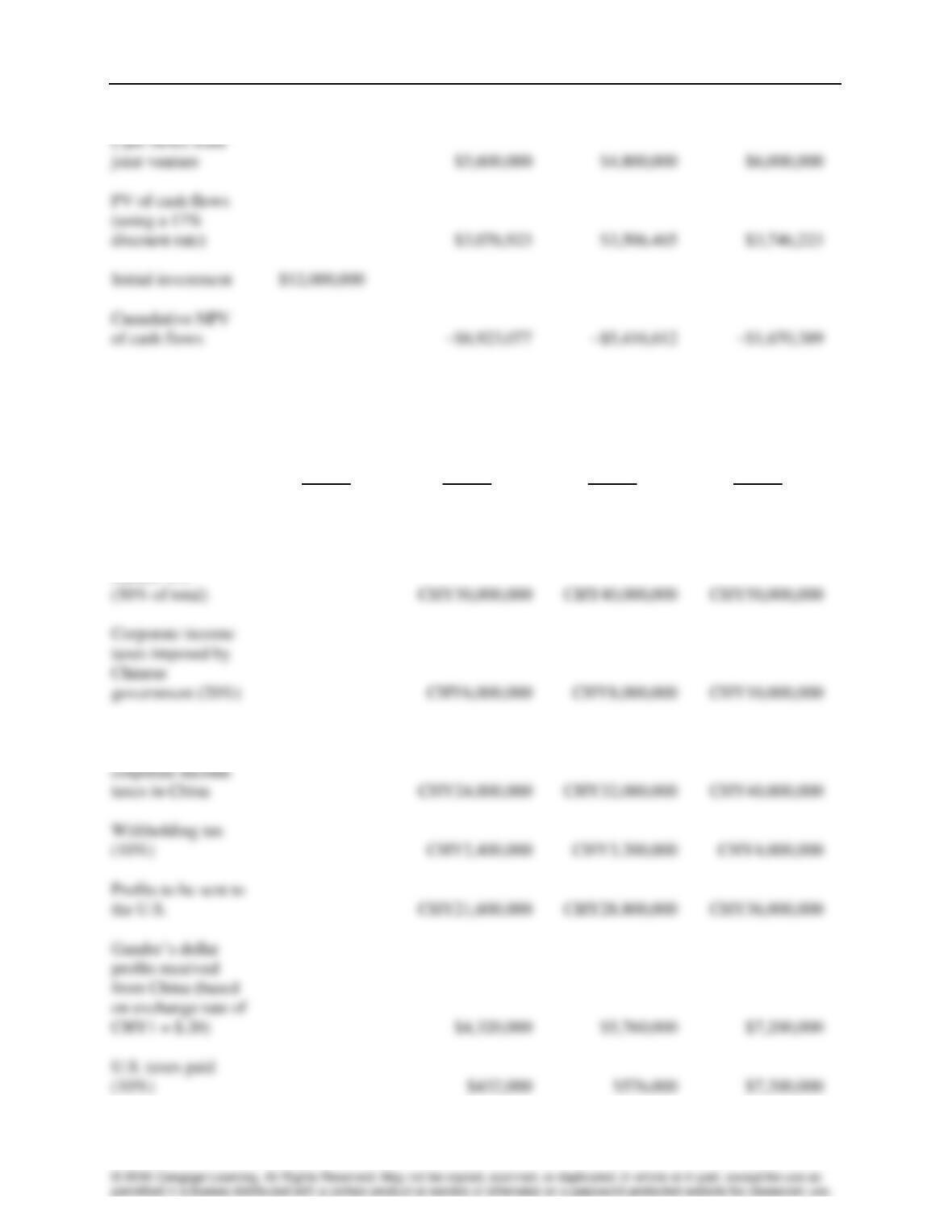

Long-Term Debt Financing ❖ 18

Cash flows from

PV of cash flows

(using a 17%

discount rate)

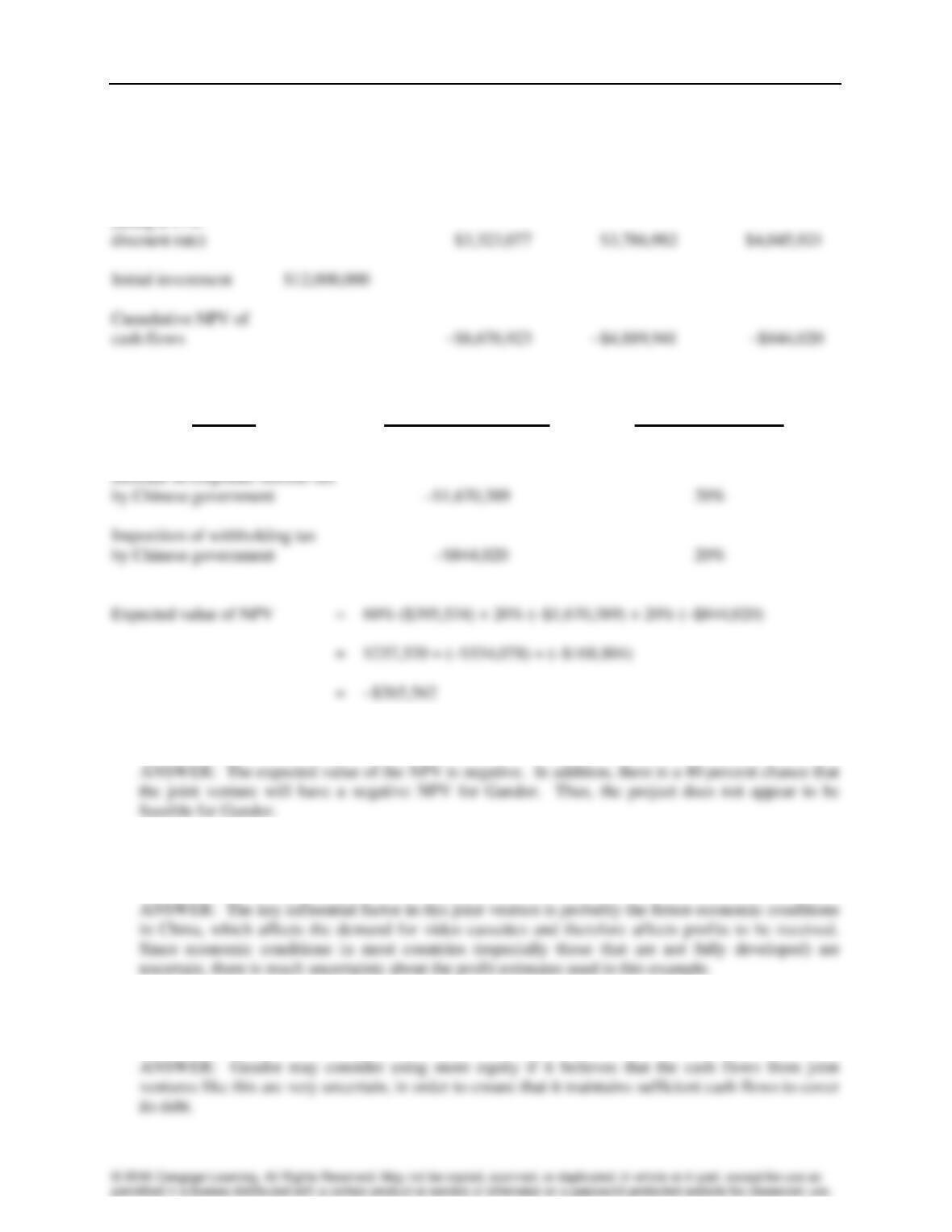

Initial investment

Cumulative NPV

of cash flows

SCENARIO 3: IMPOSITION OF A WITHHOLDING TAX BY CHINESE GOVERNMENT

(Probability = 20%)

Year 0

Year 1

Year 2

Year 3

Total profits

(in CHY)

CHY60,000,000

CHY80,000,000

CHY100,000,000

taxes imposed by

Chinese

Profits allocated to

Gandor Co.

corporate income

the U.S.

CHY21,600,000

CHY28,800,000

CHY36,000,000

profits received

from China (based

on exchange rate of

Profits to Gandor

after paying

Long-Term Debt Financing ❖ 19

Cash flows from

joint venture

$3,888,000

$5,184,000

$6,480,000

(using a 17%

Cumulative NPV of

PV of cash flows

SUMMARY OF SCENARIOS

Scenario

NPV for This Scenario

Probability that This

Scenario Will Occur

Original scenario

$395,534

60%

Increase in corporate income tax

by Chinese government

20%

by Chinese government

20%

3. Would you recommend that Gandor participate in the joint venture? Explain.

4. What do you think would be the key underlying factor that would have the most influence on the

profits earned in China as a result of the joint venture?

5. Is there any reason for Gandor to revise the composition of its capital (debt and equity) obtained from

the U.S. when financing joint ventures like this?

6. When Gandor was assessing this proposed joint venture, some of its managers of recommended that

Gandor borrow the Chinese currency rather than dollars to obtain some of the necessary capital for its

initial investment. They suggested that such a strategy could reduce Gandor’s exchange rate risk. Do

you agree? Explain.