Multinational Capital Budgeting ❖ 19

euros is 7%, regardless of the maturity of debt. Assume that interest rate parity exists. Cantoon’s cost

of capital is 20%. It plans to use cash to make the acquisition.

a. Determine the NPV under these conditions.

b. Rather than use all cash, Cantoon could partially finance the acquisition. It could obtain a loan of

3 million euros today that would be used to cover a portion of the acquisition. In this case, it

would have to pay back a lump sum total of 7 million euros at the end of 8 years to repay the

loan. There are no interest payments on this debt. This financing deal is structured such that none

of the payment is tax-deductible. Determine the NPV if Cantoon uses the forward rate instead of

the spot rate to forecast the future spot rate of the euro, and elects to partially finance the

acquisition. [You need to derive the 8-year forward rate for this question.]

ANSWER

b. The forward rate premium is:

30. Sensitivity of NPV to Conditions. Burton Co., based in the U.S., considers a project in which it

has an initial outlay of $3 million and expects to receive 10 million Swiss francs (SF) in one year. The

spot rate of the franc is $.80. Burton Co. decides to purchase put options on Swiss francs with an

exercise price of $.78 and a premium of $.02 per unit to hedge its receivables. It has a required rate of

return of 20 percent.

a. Determine the net present value of this project for Burton Co. based on the forecast that the Swiss

franc will be valued at $.70 at the end of one year.

b. Assume the same information in part (a), but with the following adjustment. While Burton

expected to receive 10 million Swiss francs, assume that there were unexpected weak economic

conditions in Switzerland after Burton initiated the project. Consequently, Burton received only 6

million Swiss francs at the end of the year. Also assume that the spot rate of the franc at the end of the

year was $.79. Determine the net present value of this project for Burton Co. if these conditions

occur.

ANSWER

31. Hedge Decision on a Project. Carlotto Co. (a U.S. firm) will definitely receive 1 million British

pounds in one year based on a business contract it has with the British government. Like most firms,

Carlotto Co. is risk averse and only takes risk when the potential benefits outweigh the risk. It has no

other international business, and is considering various methods to hedge its exchange rate risk.

Assume that interest rate parity exists. Carlotto Co. recognizes that exchange rates are very difficult to

forecast with accuracy, but it believes that the one-year forward rate of the pound yields the best

forecast of the pound’s spot rate in one year. Today the pound’s spot rate is $2.00, while the one-year

forward rate of the pound is $1.90. Carlotto Co. has determined that a forward hedge is better than

alternative forms of hedging. Should Carlotto Co. hedge with a forward contract or should it remain

unhedged? Briefly explain.

32. NPV of Partially Hedged Project. Sazer Co. (a U.S. firm) is considering a project in which it

produces special safety equipment. It will incur an initial outlay of $1 million for the research and

development of this equipment. It expects to receive 600,000 euros in one year from selling the

products in Portugal where it already does much business. In addition, it also expects to receive

300,000 euros in one year from sales to Spain, but these cash flows are very uncertain because it has

no existing business in Spain. Today’s spot rate of the euro is $1.50 and the one-year forward rate is

$1.50. It expects that the euro’s spot rate will be $1.60 in one year. It will pursue the project only if it

can satisfy its required rate of return of 24 percent. It decides to hedge all the expected receivables

Multinational Capital Budgeting ❖ 21

due to business in Portugal, and none of the expected receivables due to business in Spain. Estimate

the net present value (NPV) of the project.

ANSWER:

33. Project Financing Strategy. Konk Co., a U.S. firm, considers a project in which it would build a

subsidiary in Belgium that would generate net cash flows of about 10 million euros per year for 5

years and would remit that amount to the parent each year. It has no other international business. It

needs about 20 million euros as the initial outlay to establish the subsidiary. It can finance this initial

outlay in the following ways and the subsidiary would repay the amount of the investment evenly

over the next 5 years: (a) the parent can borrow dollars from a U.S. bank and convert them to euros,

(b) the parent can borrow euros from a Belgian bank, (c) the parent can use its equity (retained

earnings from existing business in the U.S.) and convert the funds into euros, (d) the parent can

borrow dollars from a Belgian bank and convert them to euros, and (e) the parent can diversify its

financing by obtaining one-fourth of the funds from each of the preceding sources. Assume that there

is no cost advantage to any financing method. If Konk Co. wants to use a financing method to

minimize its project’s exposure to exchange rate risk, which method should it use? Briefly explain.

34. NPV and Financing. Louisville Co. is a U.S. firm considering a project in Austria which it has an

initial cash outlay of $7 million. Louisville will accept the project only if it can satisfy its required

rate of return of 18 percent. The project would definitely generate 2 million euros in one year from

sales to a large corporate customer in Austria. In addition, it also expects to receive 4 million euros in

one year from sales to other customers in Austria. Louisville’s best guess is that the euro’s spot rate

will be $1.26 in one year. Today, the spot rate of the euro is $1.40, while the one-year forward rate of

the euro is $1.34. If Louisville accepts the project, it would hedge all the receivables resulting from

sales to the large corporate customer, and none of the expected receivables due to expected sales to

other customers.

a. Estimate the net present value (NPV) of the project.

b. Assume that Louisville considers alternative financing for the project, in which it would use $5

million cash, and the remaining initial outlay would come from borrowing euros. In this case, it

would need 1,600,000 euros to repay the loan (principal plus interest) at the end of one year. Assume

no tax effects due to this alternative financing. Estimate the NPV of the project under these

conditions.

c. Do you think the Louisville’s exposure to exchange rate risk due to the project if it uses the

alternative financing (explained in part b) is higher, lower, or the same as if it has an initial cash

outlay of $7 million (and does not borrow any funds)? Briefly explain.

ANSWER:

a.

Multinational Capital Budgeting ❖ 22

Cash flows (hedged): 2,000,000 euros × $1.34 = $2,680,000.

Solution to Continuing Case Problem: Blades, Inc.

1. Should the sales and the associated costs of 180,000 pairs of roller blades to be sold in Thailand under

the existing agreement be included in the capital budgeting analysis to decide whether Blades should

establish a subsidiary in Thailand? Should the sales resulting from a renewed agreement be included?

Why or why not?

ANSWER: The sales from the existing agreement should not be included in the capital budgeting

2. Using a spreadsheet, conduct a capital budgeting analysis for the proposed project assuming that

Blades renews the agreement with Entertainment Products. Should Blades establish a subsidiary in

Thailand under these conditions?

3. Using a spreadsheet, conduct a capital budgeting analysis for the proposed project assuming that

Blades does not renew the agreement with Entertainment Products. Should Blades establish a

Multinational Capital Budgeting ❖ 23

subsidiary in Thailand under these conditions? Should Blades renew the agreement with

Entertainment Products?

ANSWER: (See spreadsheet attached.) The spreadsheet shows a positive NPV of $8,746,688 if

4. Since future economic conditions in Thailand are uncertain, Ben Holt would like to know how critical

the salvage value is in the alternative you think is most feasible.

5. The future value of the baht is highly uncertain. Under a worst case scenario, the baht may depreciate

by as much as 5 percent annually. Revise your spreadsheet to illustrate how this would affect Blades’

decision to establish a subsidiary in Thailand (Use the capital budgeting analysis you have identified

as the most favorable from questions 2 and 3 to answer this question.)

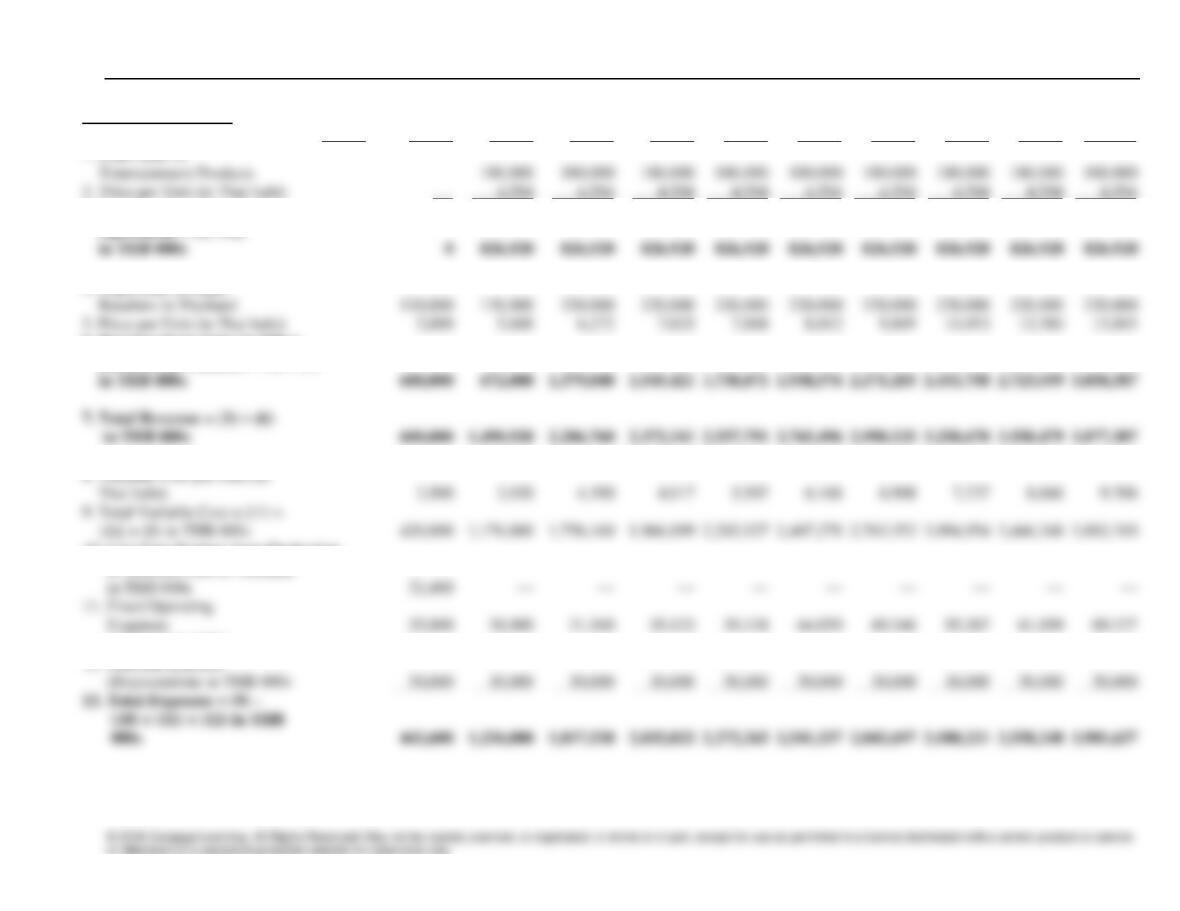

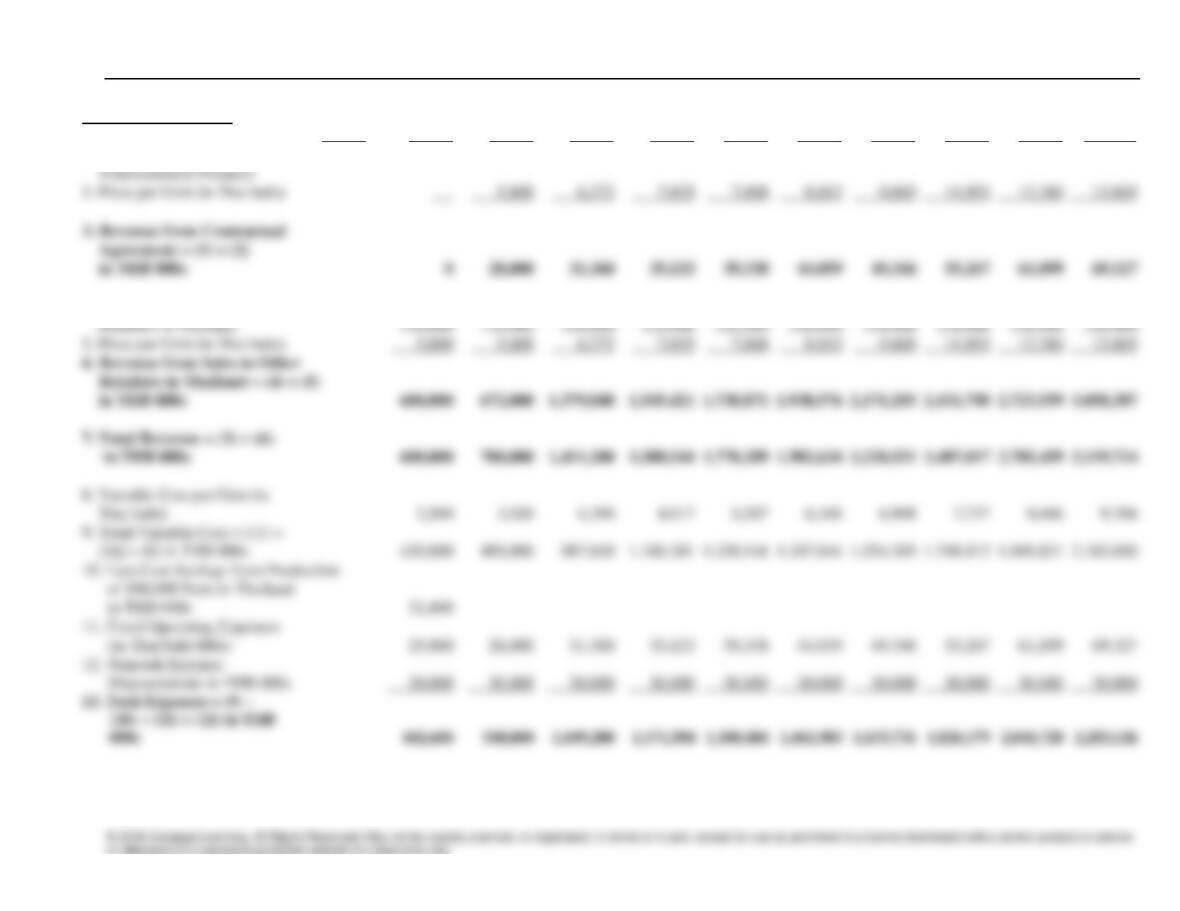

Multinational Capital Budgeting ❖ 24

Answer to Question b:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Entertainment Products

180,000

—

3. Revenue from Contractual

Agreement = (1) ×(2)

5. Price per Unit (in Thai baht)

4. Units Sold to Other

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

Thai baht)

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

10. Less Cost Savings from Production

of 108,000 Pairs in Thailand

(in Thai baht 000s)

13. Total Expenses = (9) –

(10) + (11) + (12) in THB

14. Before-Tax Earnings of

Subsidiary = (7) – (13) in

THB 000s

157,400

264,920

389,240

340,318

285,526

224,159

155,428

78,449

(7,768)

(104,331)

15. Host Government Tax

(25%) in THB 000s

(26,083)

16. After-Tax Earnings of

Subsidiary (100% of CF)

in THB 000s

228,690

321,930

285,239

244,145

198,119

146,571

88,836

24,174

18. Thai Baht Remitted by

19. Withholding Tax on Remitted

Funds (10%) in THB 000s

21. Salvage Value in THB

000s

650,000

25. Initial Investment by

Parent

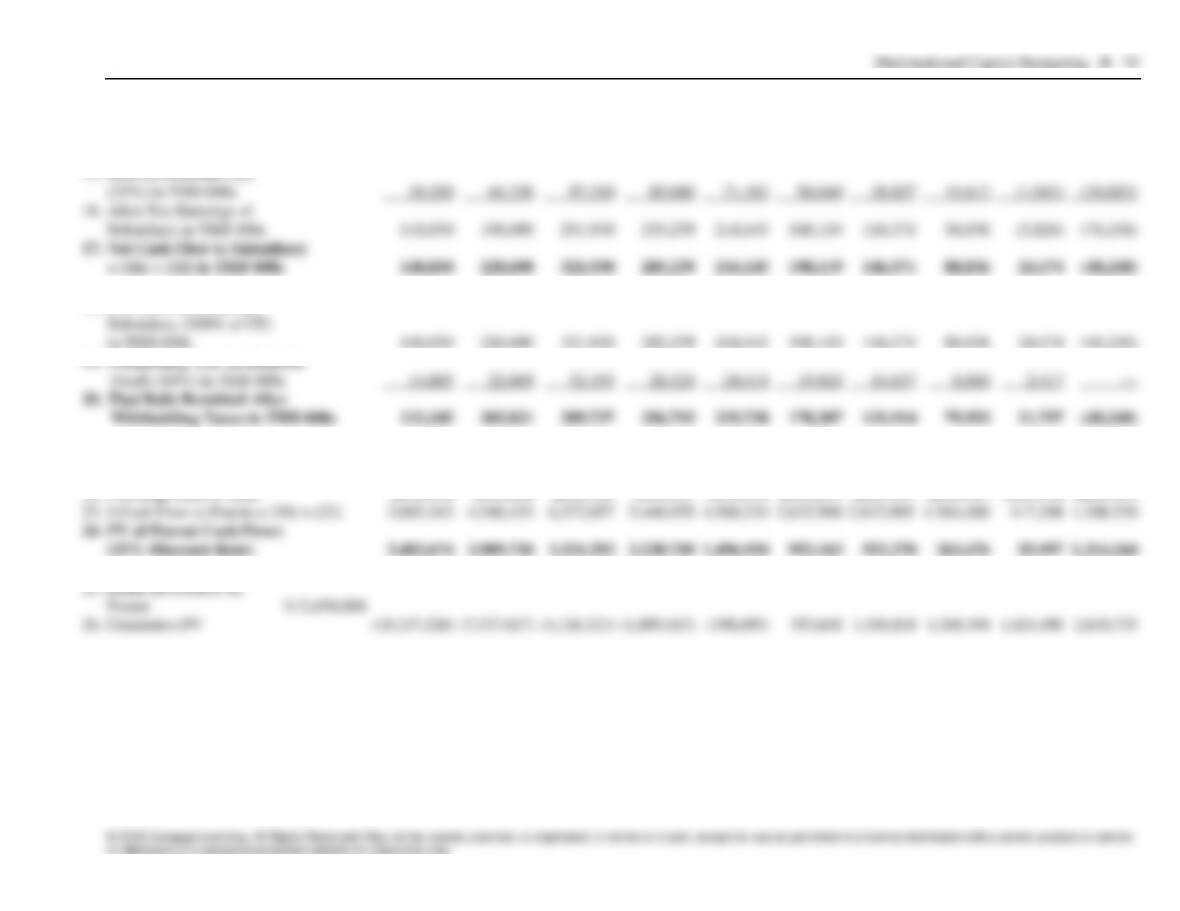

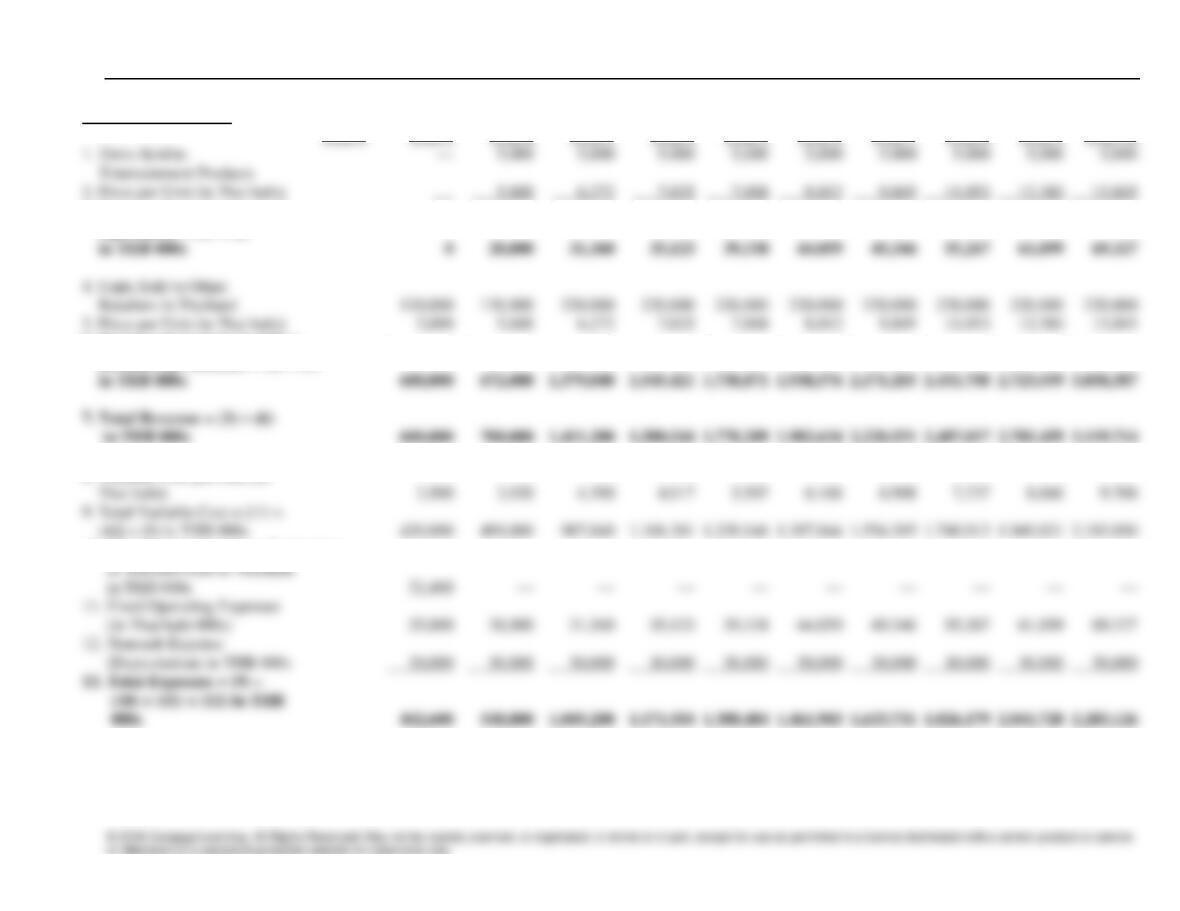

Answer to Question c:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

1. Units Sold to

Entertainment Products

4. Units Sold to Other

Retailers in Thailand

3. Revenue from Contractual

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

Thai baht)

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

(4)] × (8) in THB 000s

8. Variable Cost per Unit (in

of 108,000 Pairs in Thailand

in THB 000s

32,400

10. Less Cost Savings from Production

11. Fixed Operating Expenses

(in Thai baht 000s)

25,000

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

(Depreciation) in THB 000s

30,000

13. Total Expenses = (9) –

12. Noncash Expense

14. Before-Tax Earnings of

Subsidiary = (7) – (13) in

THB 000s

157,400

152,000

362,000

409,040

461,725

520,732

586,820

660,838

743,738

836,587

16. After-Tax Earnings of

Subsidiary (100% of CF)

in THB 000s

144,000

301,500

336,780

376,294

420,549

470,115

525,628

587,804

657,440

19. Withholding Tax on Remitted

18. Thai Baht Remitted by

21. Salvage Value in THB

Multinational Capital Budgeting ❖ 28

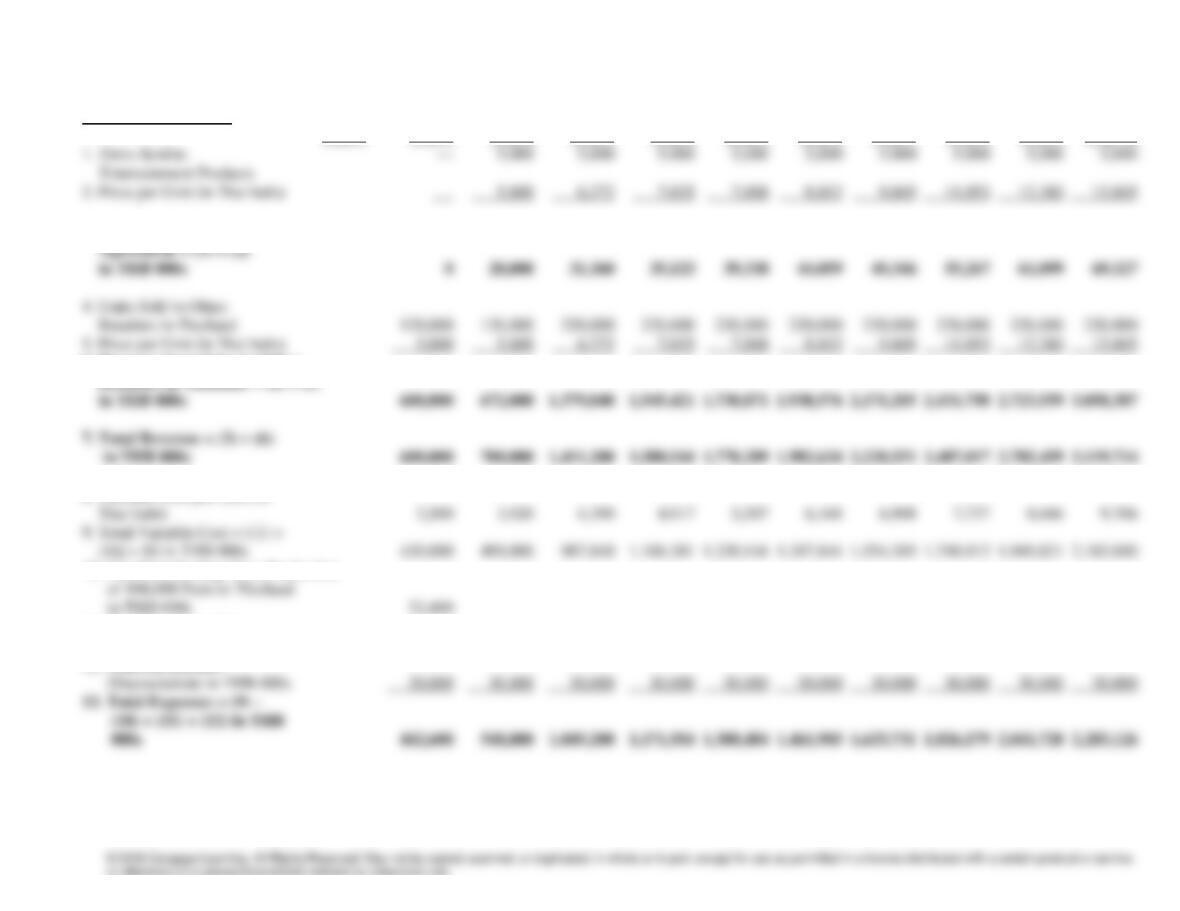

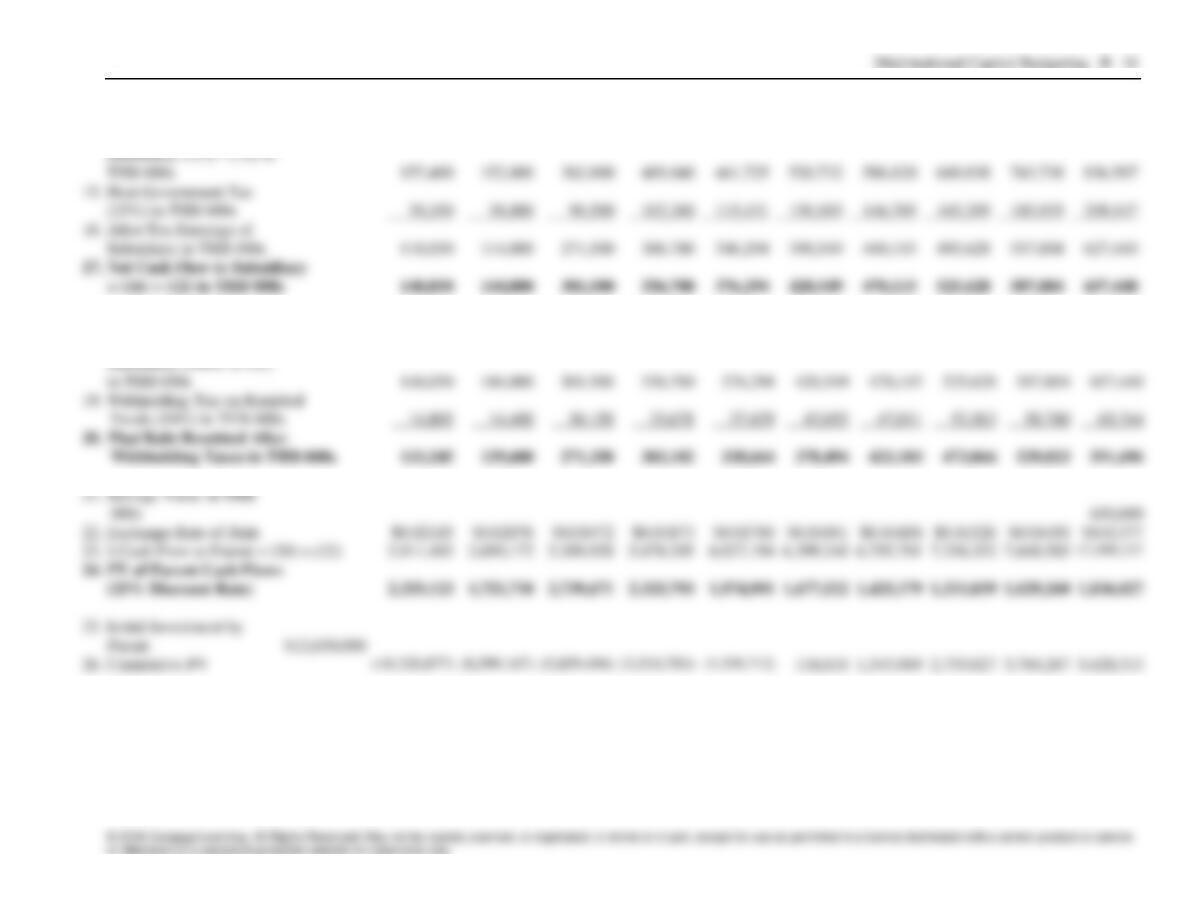

Answer to Question d:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

1. Units Sold to

—

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

8. Variable Cost per Unit (in

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

of 108,000 Pairs in Thailand

11. Fixed Operating Expenses

39,338

44,059

49,346

55,267

61,899

69,327

12. Noncash Expense

30,000

4. Units Sold to Other

Subsidiary = (7) – (13) in

15. Host Government Tax

14. Before-Tax Earnings of

16. After-Tax Earnings of

19. Withholding Tax on Remitted

Funds (10%) in THB 000s

18. Thai Baht Remitted by

Subsidiary (100% of CF)

21. Salvage Value in THB

000s

0

26. Cumulative PV

25. Initial Investment by

Multinational Capital Budgeting ❖ 30

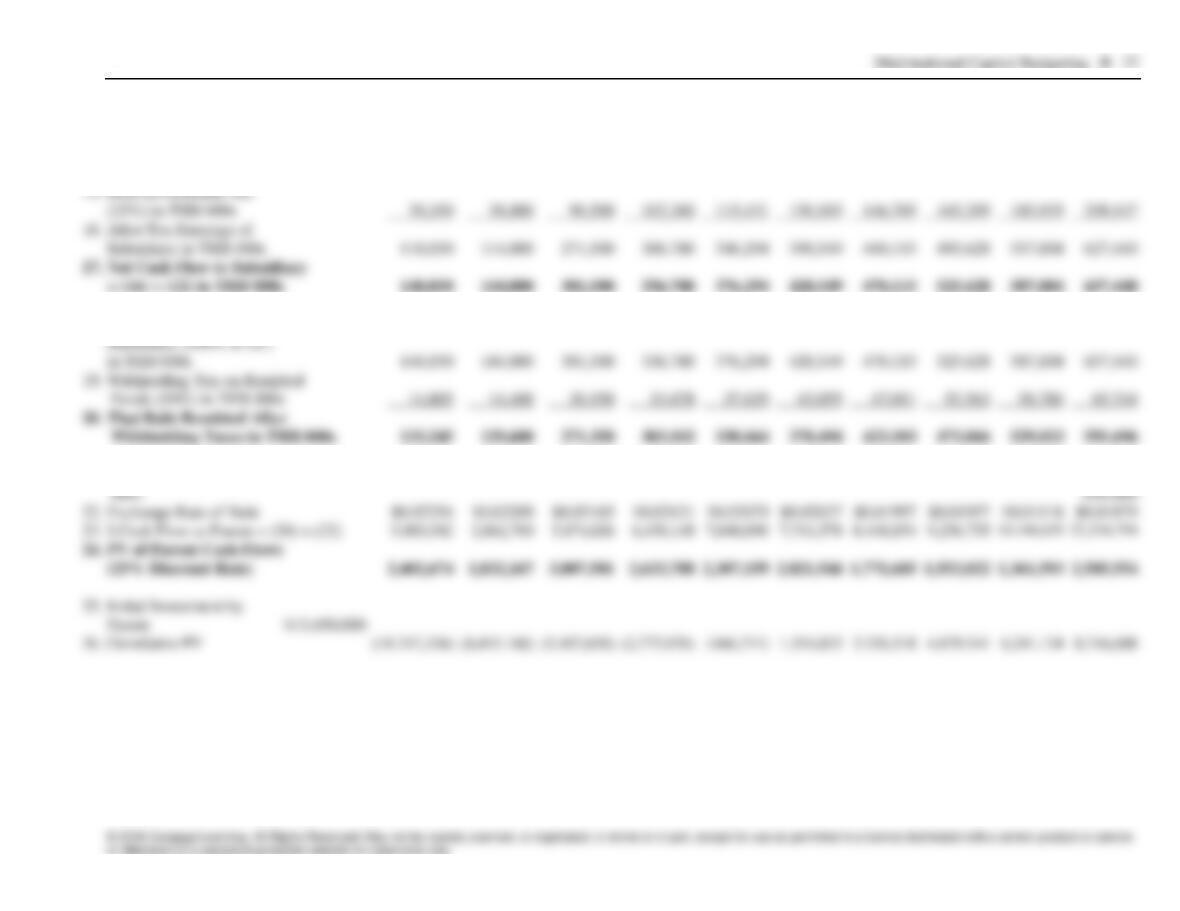

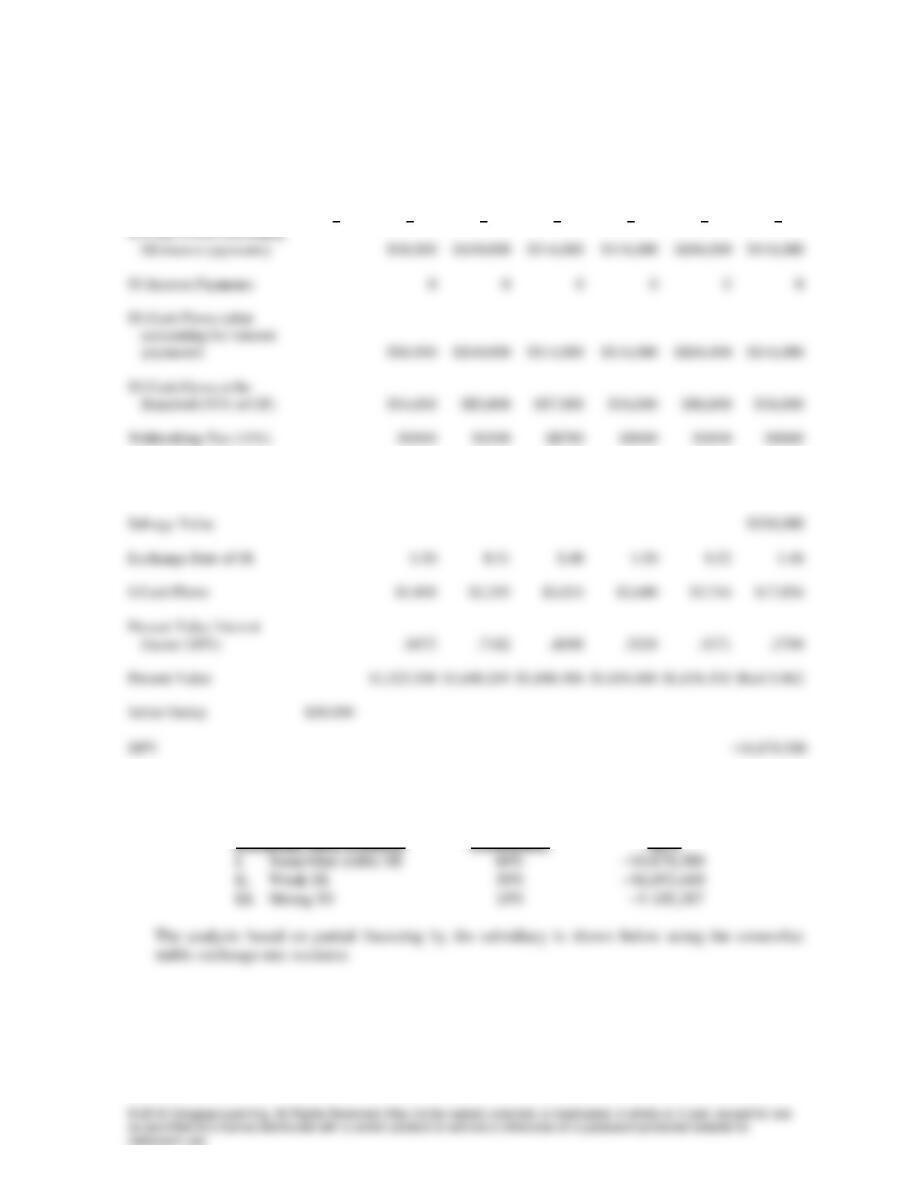

Answer to Question e:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

1. Units Sold to

3. Revenue from Contractual

Agreement = (1) × (2)

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

8. Variable Cost per Unit (in

13. Total Expenses = (9) –

10. Less Cost Savings from Production

14. Before-Tax Earnings of

18. Thai Baht Remitted by

Solution to Supplemental Case: North Star Company

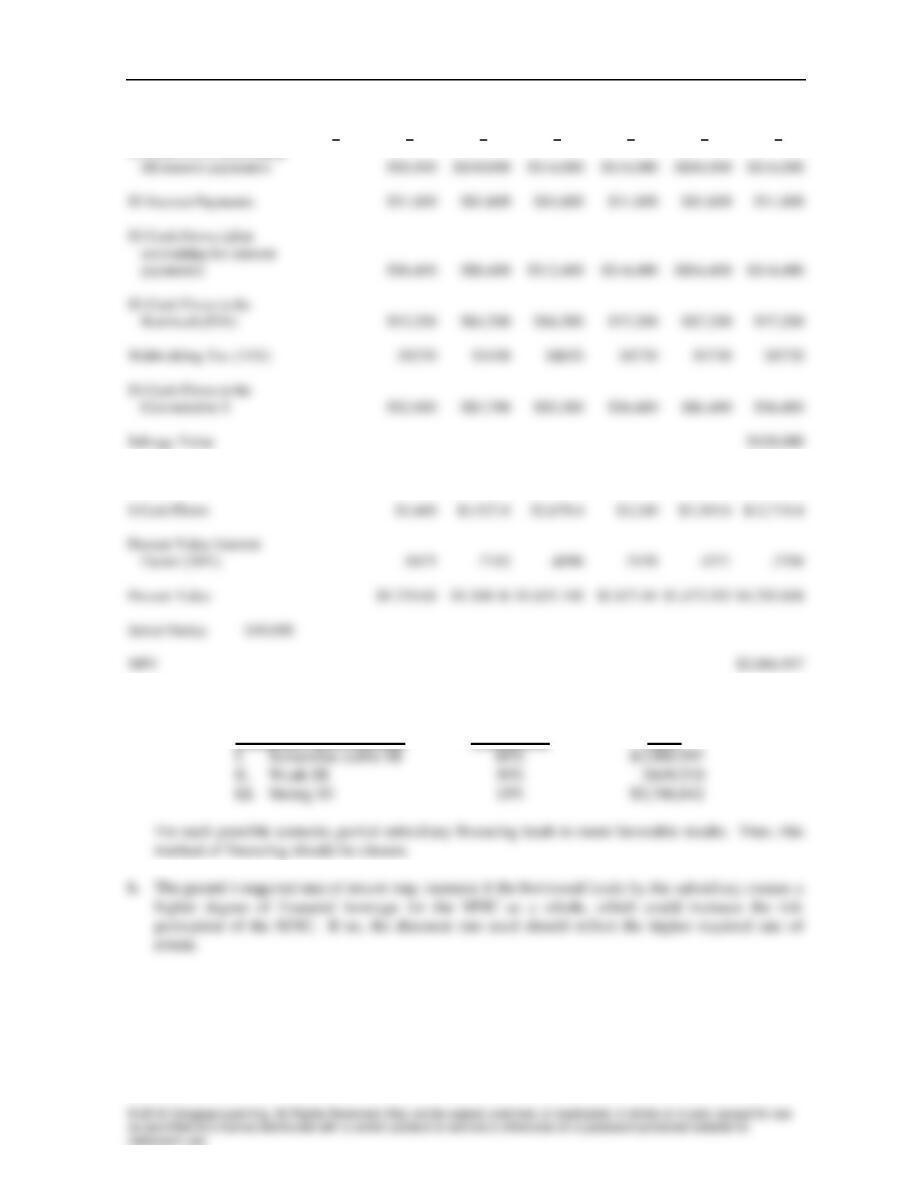

a. The analysis based on total parent financing is shown below using the somewhat stable exchange

rate scenario (in 1,000s):

0 1 2 3 4 5 6

S$ Cash Flows to be

Converted to $ S$3,600 S$4,500 S$6,300 S$7,200 S$7,200 S$7,200

Applying the same procedure from the previous table, the NPV for each exchange rate scenario is:

Exchange Rate Scenario Probability NPV

Multinational Capital Budgeting ❖ 33

(Cash amounts in thousands)

0 1 2 3 4 5 6

S$ Cash Flows (excluding

Exchange Rate of S$ $.50 $.51 $.48 $.50 $.52 $.48

Applying the same procedure from the previous table, the NPV for each exchange rate scenario is:

Exchange Rate Scenario Probability NPV

Multinational Capital Budgeting ❖ 34

c. When using a 20 percent withholding tax instead of a 10 percent withholding tax, the results

change as follows (based on partial financing by the subsidiary):

Exchange Rate Scenario Probability NPV

d. The estimate of net cash flows could be revised, which would result in a lower NPV for each

e. As of the end of Year 2, the present value of forgone cash flows for the following 4 years

Small Business Dilemma

Multinational Capital Budgeting by the Sports Exports Company

1. Describe the capital budgeting steps that would be necessary to determine whether this proposed

project is feasible, as related to this specific situation.

ANSWER: Jim would need to estimate the amount of footballs that would be sold to the

2. Explain why there is uncertainty surrounding the cash flows of this project.