Chapter 13 – Inventory Management

13-1

CHAPTER 13

INVENTORY MANAGEMENT

Teaching Notes

This is a fairly long and important chapter. Important points are:

2. The key issues are when to order and how much to order.

4. EOQ models answer the question of how much to order. Variations of the basic EOQ model

include the quantity discount model and the economic run size model.

6. ROP models are used to answer the question of when to order. Different models are used,

depending on whether demand, lead time, or both are variable.

8. All of the models in this chapter pertain to independent demand.

The Single-Period Model is used to handle ordering of perishables (such as fresh fruits and vegetables,

seafood, and cut flowers) as well as items that have a limited useful life (such as newspapers and

Answers to Discussion and Review Questions

1. Inventories are held (1) to take advantage of price discounts, (2) to take advantage of economic

2. Effective inventory management requires (1) cost information, information on demand and lead

time (amounts and variabilities), an accounting system, and a priority system (e.g., A-B-C).

3. Carrying or holding costs include interest, security, warehousing, obsolescence, and so on.

Procurement costs relate to determining how much is needed, vendor analysis, inspection of

Chapter 13 – Inventory Management

13-2

4. The RFID (Radio Frequency Identification) chip tags are beginning to be used with consumer

products and they contain bits of data, such as product serial number. Scanners will automatically

read the information on an RFID chip into a database, so the companies can keep track of sales

5. It may be inappropriate to compare the inventory turnover ratios of companies in different

industries because the production process, requirements and the length of production run varies

6. a. Only one product is involved.

b. Annual demand requirements are known.

7. The total cost curve is relatively flat in the vicinity of the EOQ, so that there is a “zone” of values

8. As the carrying cost increases, holding inventory becomes more expensive. Therefore, in order to

9. Safety stock is inventory held in excess of expected demand to reduce the risk of stockout

presented by variability in either lead time or demand rates.

10. Safety stock is large when large variations in lead time and/or usage are present. Conversely,

11. Service level can be defined in a number of ways. The text focuses mainly on “the probability

that demand will not exceed the amount on hand.” Other definitions relate to the percentage of

Chapter 13 – Inventory Management

13-3

12. The A-B-C approach refers to the classification of items stocked according to some measure of

13. In effect, this situation is a “quantity discount” case with a time dimension. Hence, buying larger

quantities will result in lower annual purchase costs, lower ordering costs (fewer orders), but

14. Annual carrying costs are determined by average inventory. Hence, a decrease in average

15. The Single-Period Model is used when inventory items have a limited useful life (i.e., items are

not carried over from one period to the next).

17. A company can reduce the need for inventories by:

a. using standardized parts

b. improved forecasting of demand

c. using preventive maintenance on equipment and machines

Taking Stock

1. a. If we buy additional amounts of a particular good to take advantage of quantity discounts,

then we will save money on a per unit purchasing cost of the item. We will also save on

ordering cost because since we bought a larger quantity, we will not have to order this item as

frequently. However, as a result of ordering larger quantity, we will have to carry larger

inventory in stock, which in turn will result in an increase in inventory holding cost.

Chapter 13 – Inventory Management

13-4

2. In making inventory decisions involving holding costs, setting inventory levels and deciding on

quantity discount purchases, the materials manager, plant manager, production planning and

3. The technology has had a tremendous impact on inventory management. The utilization of bar

coding has not only reduced the cost of taking physical inventory but also enabled real time

Critical Thinking Exercise

1. Including a wider range of foods provide fast food companies with a competitive edge in terms of

improving customer satisfaction and service. However, it has also complicated the operational

function of the company. Expansion of menu offerings can create problems for inventory

2. a. How important is the item? For example, does it relate to a holiday or other important event,

such as graduation cards?

3. Among considerations are:

How many stamps does he now have? Does he know how many he has? If so, how many?

What is his usage rate or current need for stamps?

What else does he need the cash for today?

Can he get more money at a bank or ATM?

Chapter 13 – Inventory Management

13-5

Can he purchase “forever stamps” and temporarily avoid a price increase?

4. Student answers will vary.

Memo Writing Exercises

1. Cost of carrying inventory must be weighted against the following costs:

a. cost of shortages (finished goods inventory)

2. The possible advantages of using a single supplier include:

a. obtaining a discount due to additional volume purchased from the supplier

b. building trust and working with the supplier so that the material will be delivered in a timely

fashion to avoid stockouts and excess inventory.

The possible advantages of using multiple suppliers include:

a. the adverse effect of tardiness will be felt much less when there are multiple sources for the

materials.

Chapter 13 – Inventory Management

13-6

Solutions

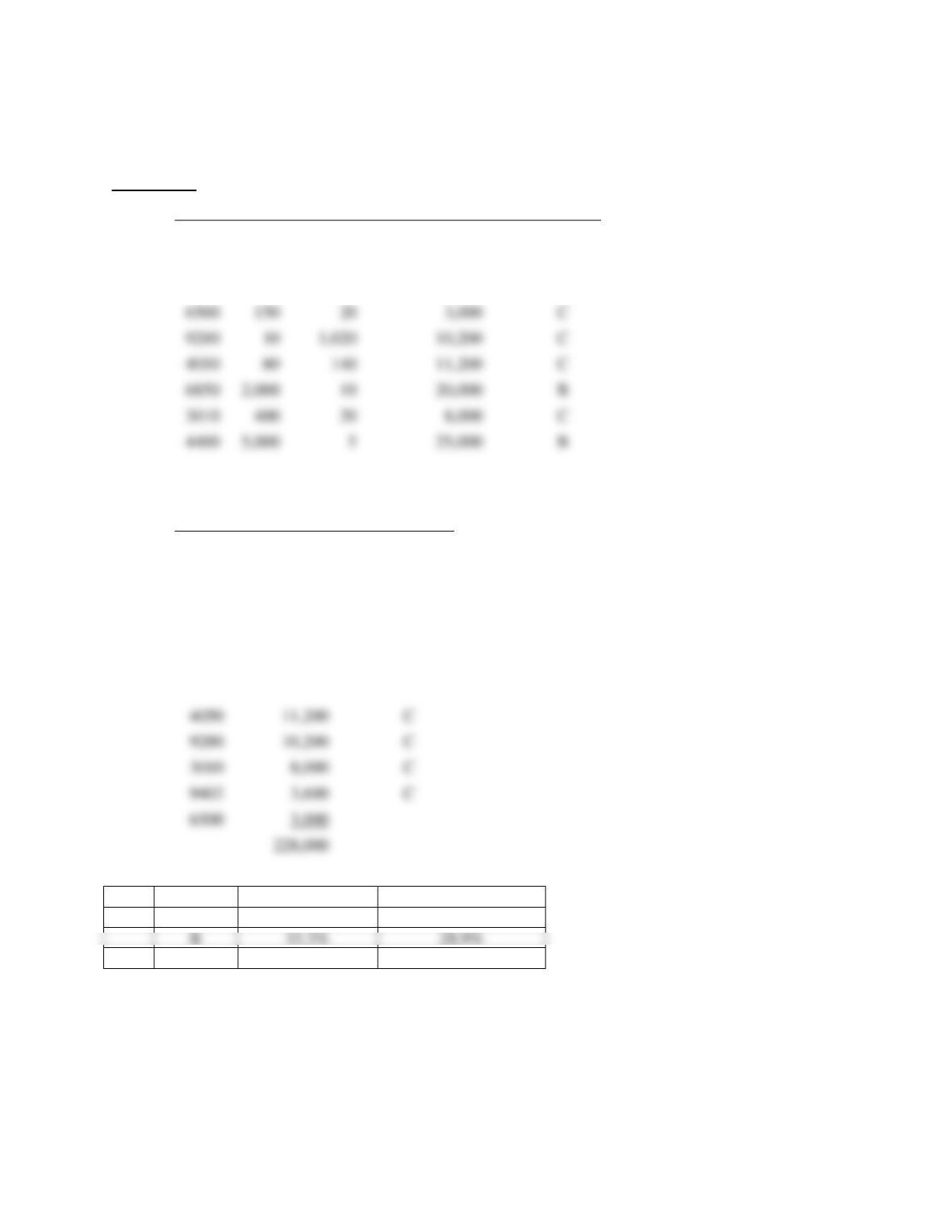

1. a.

Item

Usage

Unit Cost

Usage x Unit Cost

Category

4021

90

$1,400

$126,000

A

9402

300

12

3,600

C

4066

30

700

21,000

B

In descending order:

Item

Usage x Cost

Category

4021

$126,000

A

4400

25,000

B

4066

21,000

B

6850

20,000

B

11,200

C

9280

10,200

C

3010

8,000

C

9402

3,600

C

6500

1. b.

Category

Percent of Items

Percent of Total Cost

A

11.1%

55.3%

C

55.6%

15.8%

9280

10

10,200

C

4050

80

140

11,200

C

6850

2,000

10

20,000

B

4400

5,000

25,000

B

Chapter 13 – Inventory Management

13-7

2. The following table contains figures on the monthly volume and unit costs for a random sample

of 16 items for a list of 2,000 inventory items.

Dollar

Item

Unit Cost

Usage

Usage

Category

K34

10

200

2,000

C

K35

25

600

15,000

A

K36

36

150

5,400

B

F99

20

60

1,200

C

D45

10

550

5,500

B

D48

12

90

1,080

C

D52

15

110

1,650

C

D57

40

120

4,800

B

N08

30

40

1,200

C

P09

10

30

300

C

a. Develop an A-B-C classification for these items. [See table.]

b. How could the manager use this information? To allocate control efforts.

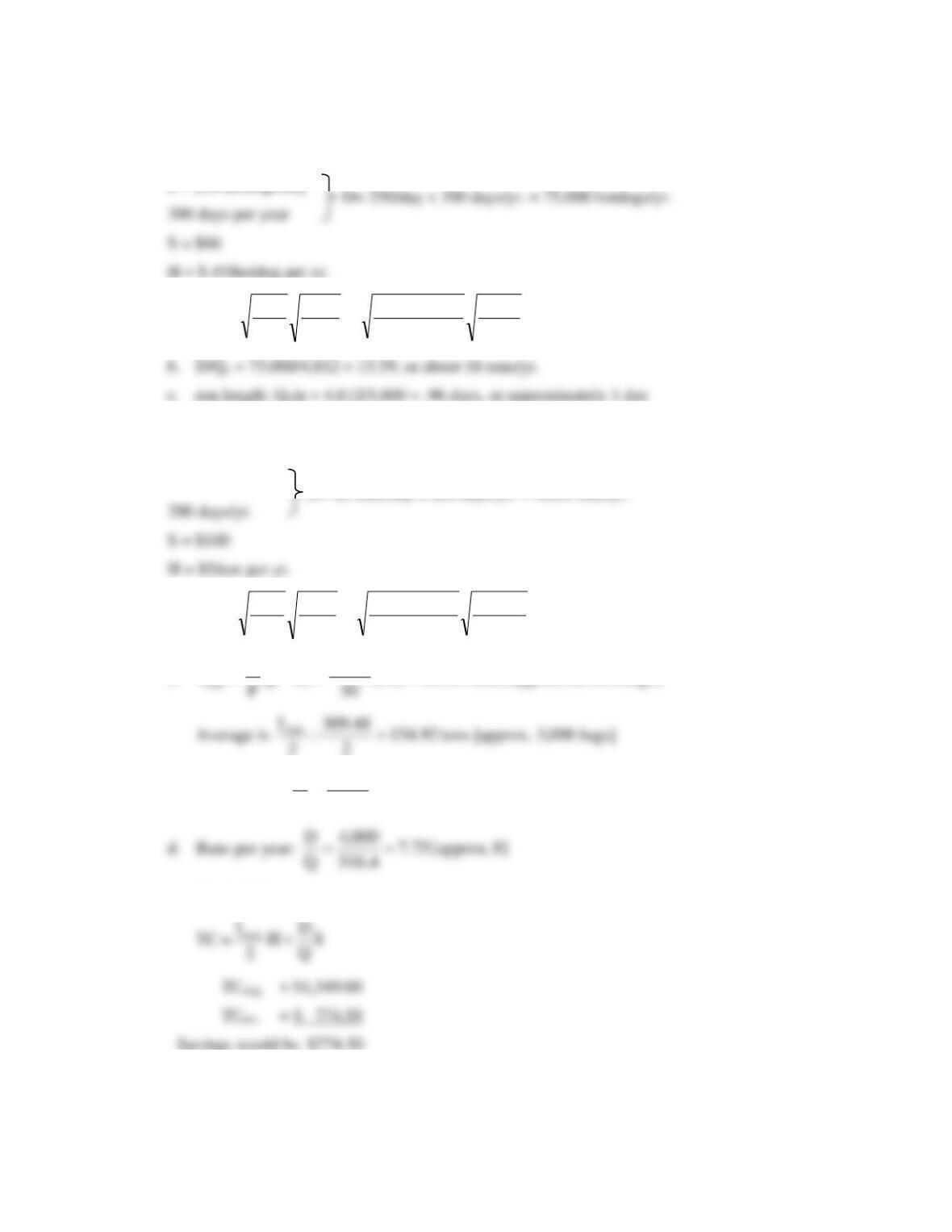

3. D = 1,215 bags/yr.

c.

orders

ordersbags

bags

Q

D 5.67

/ 18

215,1 ==

M10

16

25

400

C

M20

20

80

1,600

C

F14

20

300

6,000

B

F95

30

800

24,000

A

Chapter 13 – Inventory Management

13-8

d.

S

Q

D

H2/QTC +=

350,1$675675)10(

18

215,1

)75(

2

18 =+=+=

4. D = 40/day x 260 days/yr. = 10,400 packages

S = $60 H = $30

a.

oxesb 20496.203

30

60)400,10(2

H

DS2

Q0====

Chapter 13 – Inventory Management

13-9

5. D = 750 pots/mo. x 12 mo./yr. = 9,000 pots/yr.

Price = $2/pot S = $20 H = ($2)(.30) = $.60/unit/year

60.

H

6.774

2

TC = 232.35 + 232.36

= 464.71

If Q = 1500

6. u = 800/month, so D = 12(800) = 9,600 crates/yr.

H = .35P = .35($10) = $3.50/crate per yr.

50.3$

H

TC at EOQ:

.71.371,1$)28(

392

600,9

)50.3(

2

392 =+

Savings approx. $364.28 per year.

Chapter 13 – Inventory Management

13-10

7. H = $2/month

a.

16.74

2

55)100(2

Q:D

H

DS2

Q010 ===

83.90

55)150(2

Q:D 02 ==

1–6 TC74 = $148.32

*140$)45(

100

)2(

50

TC

=+=

7–12 TC91 = $181.66

185$)45(

150

)2(

50

TC

=+=

Chapter 13 – Inventory Management

13-11

8. D = 27,000 jars/month

a.

.243,464.242,4

18.

60)000,27(2

H

DS2

Q===

TC=

S

D

H

Q+

32.1$

TC4000 =

765)60(

000,4

000,27

)18(.

2

000,4 =

+

TC4243 =

68.76360

243,4

000,27

)18(.

2

243,4 =

+

b. Current:

75.6

000,4

000,27

Q

D==

Difference

Chapter 13 – Inventory Management

13-12

9. p = 5,000 hotdogs/day

a.

4,812] to[round 27.812,4

750,4

000,5

45.

66)000,75(2

up

p

H

DS2

Q0==

−

=

10. p = 50/ton/day

u = 20 tons/day

a.

bags] [10,328 tons 40.516

2050

50

5

100)000,4(2

up

p

H

DS2

Q0=

−

=

−

=

b.

]bags 8.196,6 .approx[ tons 84.309)30(

4.516

)up(

Q

Imax ==−=

c. Run length =

days 33.10

50

4.516

P

Q==

e. Q = 258.2

D= 20 tons/day x 200 days/yr. = 4,000 tons/yr.

Chapter 13 – Inventory Management

11. S = $300

D = 20,000 (250 x 80 = 20,000)

a.

=

−

=

−

=80200

200

10

300)000,20(2

up

p

H

DS2

Q0

Q0 = (1,095.451) (1.2910) = 1,414 units

b. Run length =

days 07.7

200

414,1

P

Q==

No, because present demand could not be met.

e. 1) Try to shorten setup time by .40 days.

f. In order to be able to accommodate a job of 10 days, plus one day for setup, there would

need to be an11 day supply at Imax, which would be 880 units on hand. Solving the

following for Q, we find:

units 880)80200(

200

)(

max =−=−= Q

up

P

Q

I

Q = 1,467.

Chapter 13 – Inventory Management

13-14

12. p = 800 units per day

d = 300 units per day

Q0 = 2000 units per day

a. Number of batches of heating elements per year =

5.37

000,2

000,75 =

batches per year

c. Maximum inventory or Imax can be found using the following equation:

units 625

2

2501

2

inventory Average

units 250125)(2,000)(.6

800

300800

0002

0

===

==

−

=

−

=

,

I

,,

p

dp

QI

max

max

Chapter 13 – Inventory Management

13-15

13. D = 18,000 boxes/yr.

S = $96

60.

H

Since this quantity is feasible in the range 2000 to 4,999, its total cost and the total cost of all

lower price breaks (i.e., 5,000 and 10,000) must be compared to see which is lowest.

TC2,400 =

040,23$)000,18(20.1$)96($

400,2

000,18

)60(.

2

400,2 =++

Hence, the best order quantity would be 5,000 boxes.

•

TC

•

•

Lowest TC

Chapter 13 – Inventory Management

13-16

14.

a.

S = $48

D = 25 stones/day x 200 days/yr. = 5,000 stones/yr.

Quantity

Unit Price

a.

H = $2

1 – 399

$10

400 – 599

9

90.489

2

48)000,5(2

H

DS2

Q===

600 +

8

b.

H = .30P

(Feasible)

Q

D

Q

422

600

$8/stone)at feasibleNot (

NF 447

)8(30.

48)000,5(2

EOQ

8$

==

Since an order quantity of 600 would have a lower cost than 422, 600 stones is

the optimum order size.

c.

ROP = 25 stones/day (6 days) = 150 stones.

TC

Chapter 13 – Inventory Management

13-17

15.

Range

P

H

Q

D = 4,900 seats/yr.

0–999

$5.00

$2.00

495

H = .4P

1,000–3,999

4.95

1.98

497 NF

S = $50

4,000–5,999

4.90

1.96

500 NF

6,000+

4.85

1.94

503 NF

Compare TC495 with TC for all lower price breaks:

TC4,000 =

4,000

($1.96) +

4,900

($50) + $4.90(4,900) = $27,991

2

4,000

TC6,000 =

6,000

($1.94) +

4,900

($50) + $4.85(4,900) = $29,626

2

6,000

Hence, one would be indifferent between 495 or 1,000 units

TC495 =

($2) +

4,900

($50) + $5.00(4,900) = $25,490

2

TC1,000 =

1,000

($1.98) +

4,900

($50) + $4.95(4,900) = $25,490

2

1,000

Chapter 13 – Inventory Management

13-18

16. D = (800) x (12) = 9600 units

S = $40

H = (25%) x P

For Supplier A:

)]600,9)(6.13[()40(

500

600,9

)6.13)(25(.

2

500

TC

75.107,134$TC

500

81.471

81.471

++

=

=

For Supplier B:

85.141,133$TC

520,13192.81093.810TC

53.473

2

)7.13)(25(.

81.471

81.471

=

++=

Chapter 13 – Inventory Management

13-19

17. D = 3600 boxes per year

Q = 800 boxes (recommended)

S = $80 /order

H = $10 /order

Even though the inventory total cost curve is fairly flat around its minimum, when there are

quantity discounts, there are multiple U shaped total inventory cost curves for each unit price

depending on the unit price. Therefore when the quantity changes from 800 to 801, we shift to a

different total cost curve.

The order quantity of 801 is preferred to order quantity of 800 because TCQ=801 < TCQ=800 or

7964.55 < 8320.

)D*P(S

Q

D

H

2

Q

TC

boxes 240

10

)80)(600,3(2

H

DS2

EOQ

EOQ

+

+

=

===

Chapter 13 – Inventory Management

13-20

18. Daily usage = 800 ft./day Lead time = 6 days

Service level desired: 95 percent. Hence, risk should be 1.00 – .95 = .05

19. Expected demand during LT = 300 units

dLT = 30 units

20. LT demand = 600 lb.

d LT = 52 lb.

21. −

d = 21 gal./wk.

d = 3.5 gal./wk.

LT = 2 days

SL = 90 percent requires z = +1.28

a.

gallons 398(3.5)(2/7)281(2/7)21)(LTz(LT)dROP d.. =+=+=

871.1

L

6 8.39 gallons

0 1.28 z-scale

90%