Chapter 06 – Efficient Diversification

CHAPTER 06

EFFICIENT DIVERSIFICATION

1. So long as the correlation coefficient is below 1.0, the portfolio will benefit from

3. a and b will have the same impact of increasing the Sharpe ratio from .40 to .45.

4. The expected return of the portfolio will be impacted if the asset allocation is changed.

Since the expected return of the portfolio is the first item in the numerator of the Sharpe

5. Total variance = Systematic variance + Residual variance = β2 Var(rM) + Var(e)

When β = 1.5 and σ(e) = .3, variance = 1.52 × .22 + .32 = .18. In the other scenarios:

sMs(e) b

TOTAL

Variance

Corr Coeff

0.2 0.3 1.65 0.1989 0.7399

a. Both will have the same impact. Total variance will increase from .18 to .1989.

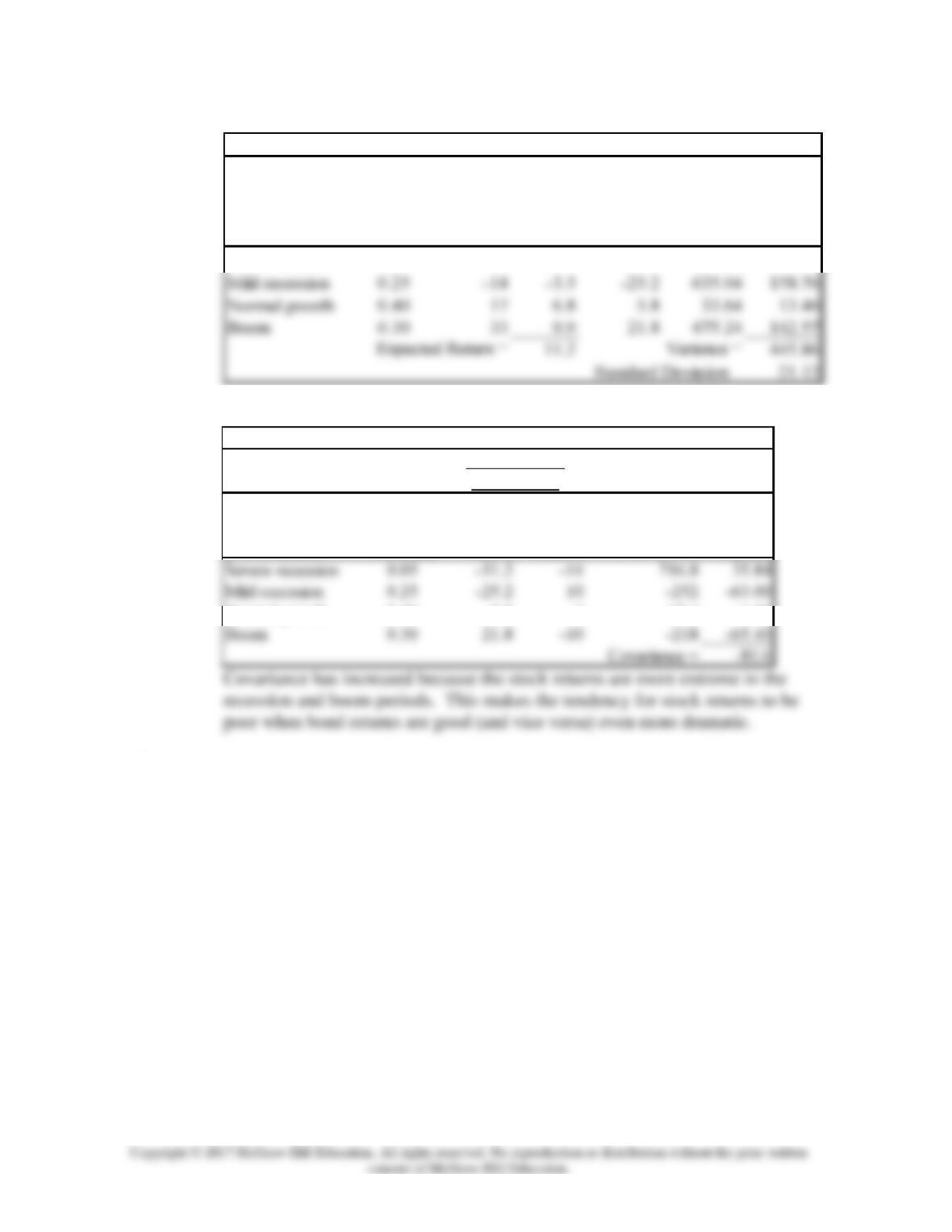

6. a. Without doing any math, the severe recession is worse and the boom is better.

Thus, there appears to be a higher variance, yet the mean is probably the same

since the spread is equally large on both the high and low side. The mean return,

however, should be higher since there is higher probability given to the higher

returns.

Chapter 06 – Efficient Diversification

b. Calculation of mean return and variance for the stock fund:

(A) (B) (C) (D) (E) (F) (G)

Col. B

Col. B

×

Col. C

Col. F

Severe recession 0.05 –40 –2.0 –51.2 2621.44 131.07

Mild recession 0.25 –14 –3.5 –25.2 635.04 158.76

Scenario

Deviation

from

Expected

Return

Squared

Deviation

Rate of

Return

Probability

c. Calculation of covariance:

(A) (B) (C) (D) (E) (F)

Col. C Col. B

Stock Bond

Fund Fund Col. D Col. E

Normal growth 0.40 5.8 3 17.4 6.96

Deviation from

Mean Return

Scenario

Probability

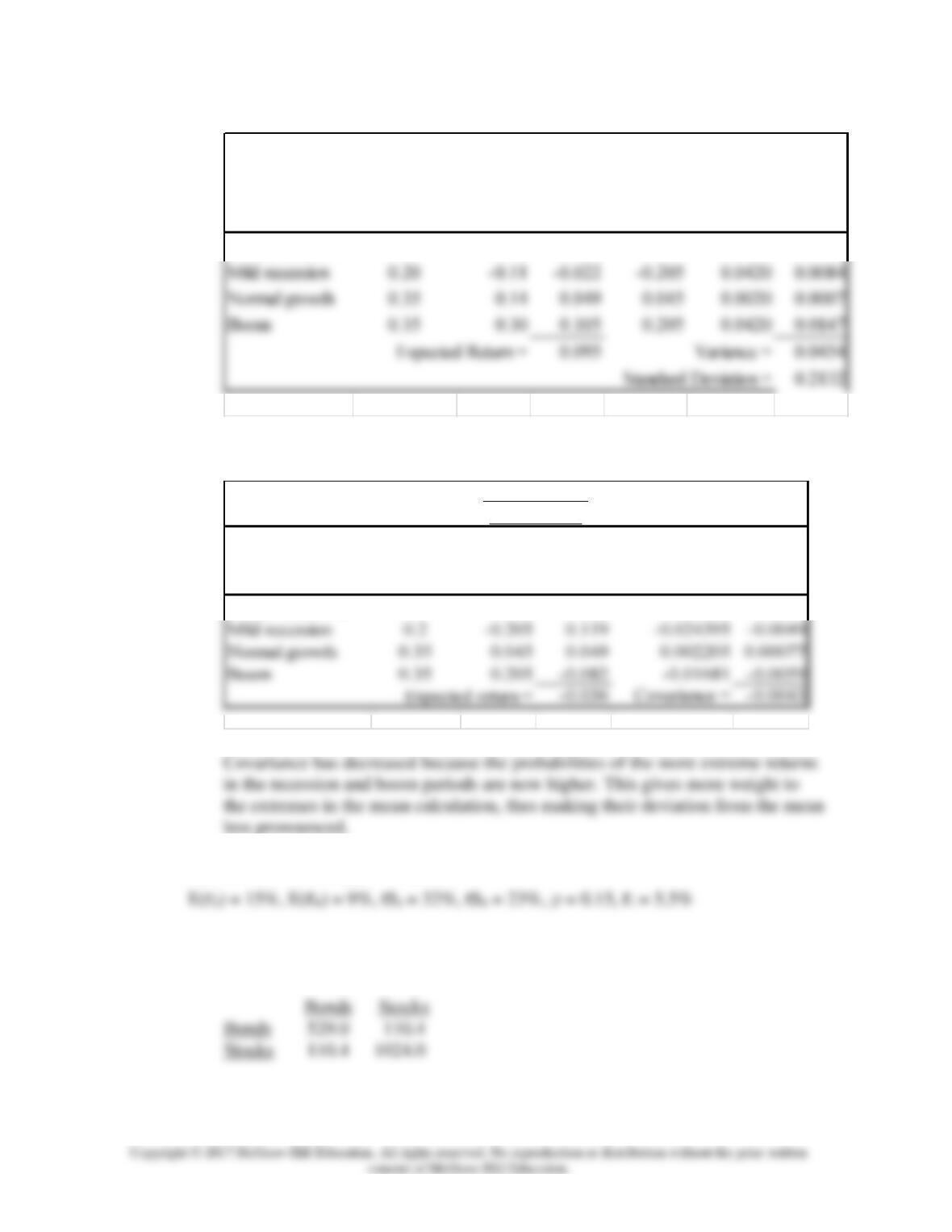

7. a. One would expect variance to increase because the probabilities of the extreme

outcomes are now higher.

Chapter 06 – Efficient Diversification

b. Calculation of mean return and variance for the stock fund:

Col. B Col. B

Col. C Col. F

Severe recession 0.10 –0.37 –0.037 –0.465 0.2162 0.0216

Scenario

Probability

Stock

Rate of

Return

Deviation

from

Expected

Return

Squared

Deviation

c. Calculation of covariance

Col. C Col. B

Stock Bond

Fund Fund Col. D Col. E

Severe recession 0.1 –0.465 -0.122 0.05673 0.00567

Mild recession 0.2 –0.205 0.119 –0.024395 –0.0049

Deviation from

Mean Return

Scenario

Probability

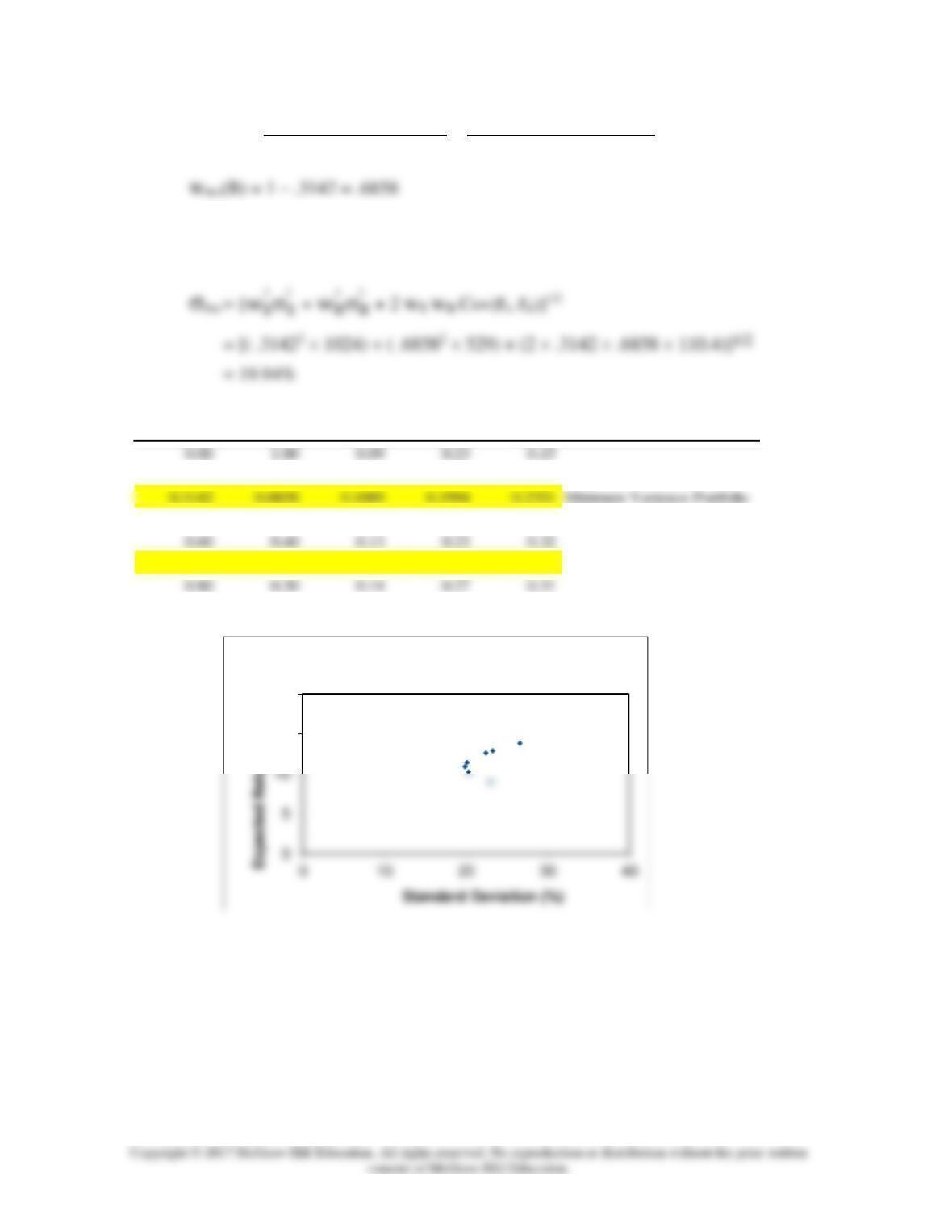

8. The parameters of the opportunity set are:

From the standard deviations and the correlation coefficient we generate the covariance

matrix [note that Cov(rS, rB) = SB]:

The minimum-variance portfolio proportions are:

Chapter 06 – Efficient Diversification

wMin(S) = B2 - Cov(rS, rB)

S2 + B2 - 2Cov(rS, rB) = 529 - 110.4

1,024 + 529 - (2 ×110.4) = .3142

The mean and standard deviation of the minimum variance portfolio are:

E(rMin) = ( .3142 15%) + ( .6858 9%) = 10.89%

% in stocks % in bonds Exp. Return Std dev.

Sharpe Ratio

0.20 0.80 0.10 0.20 0.23

0.40 0.60 0.11 0.20 0.29

0.6466 0.3534 0.1288 0.233382 0.3162 Tangency Portfolio

1.00 0.00 0.15 0.32 0.30

9.

15

20

Investment Opportunity Set

Chapter 06 – Efficient Diversification

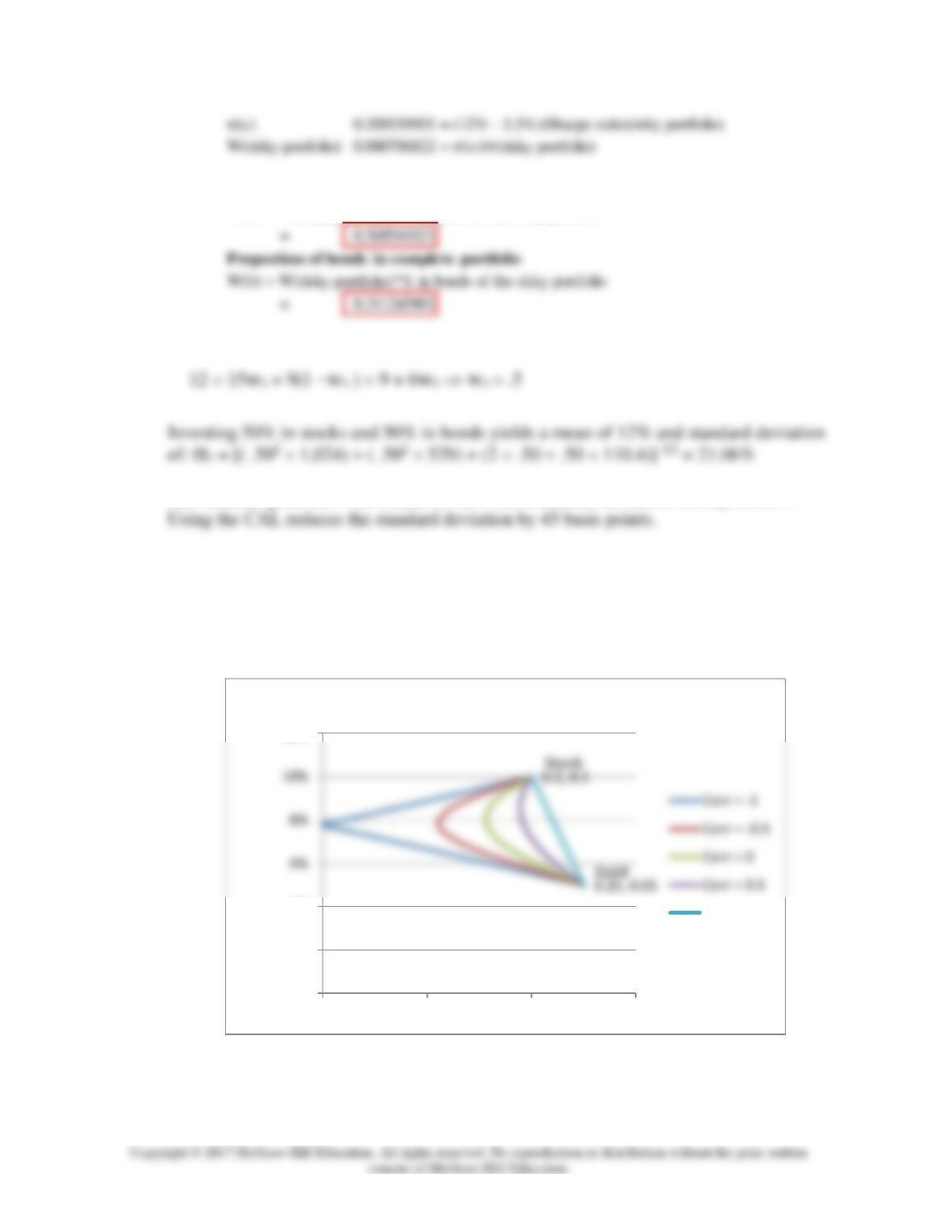

10. The Sharpe ratio of the optimal CAL is:

11.

a. The equation for the CAL is:

b. The mean of the complete portfolio as a function of the proportion invested in

the risky portfolio (y) is:

E(rC) = (l − y)rf + yE(rP) = rf + y[E(rP) − rf] = 5.5 + y(12.88 − 5.5)

To prevent rounding error, we use the spreadsheet with the calculation of the

previous parts of the problem to compute the proportion in each asset in the

complete portfolio:

18

20

Investment Opportunity Set

Chapter 06 – Efficient Diversification

Proportion of stocks in complete portfolio

W(s) = W(risky portfolio)*% in stock of the risky portfolio

12. Using only the stock and bond funds to achieve a mean of 12%, we solve:

The efficient portfolio with a mean of 12% has a standard deviation of only 20.61%.

13.

a. Although it appears that gold is dominated by stocks, gold can still be an

attractive diversification asset. If the correlation between gold and stocks is

sufficiently low, gold will be held as a component in the optimal portfolio.

b. If gold had a perfectly positive correlation with stocks, gold would not be a part

of efficient portfolios. The set of risk/return combinations of stocks and gold

0%

2%

4%

12%

0% 10% 20% 30%

Corr = 1

Standard

Deviation

Return

Chapter 06 – Efficient Diversification

14. Since Stock A and Stock B are perfectly negatively correlated, a risk-free portfolio can

be created and the rate of return for this portfolio in equilibrium will always be the risk-

free rate. To find the proportions of this portfolio [with wA invested in Stock A and wB

= (1 –wA ) invested in Stock B], set the standard deviation equal to zero. With perfect

negative correlation, the portfolio standard deviation reduces to:

P = ABS[wAA −wBB]

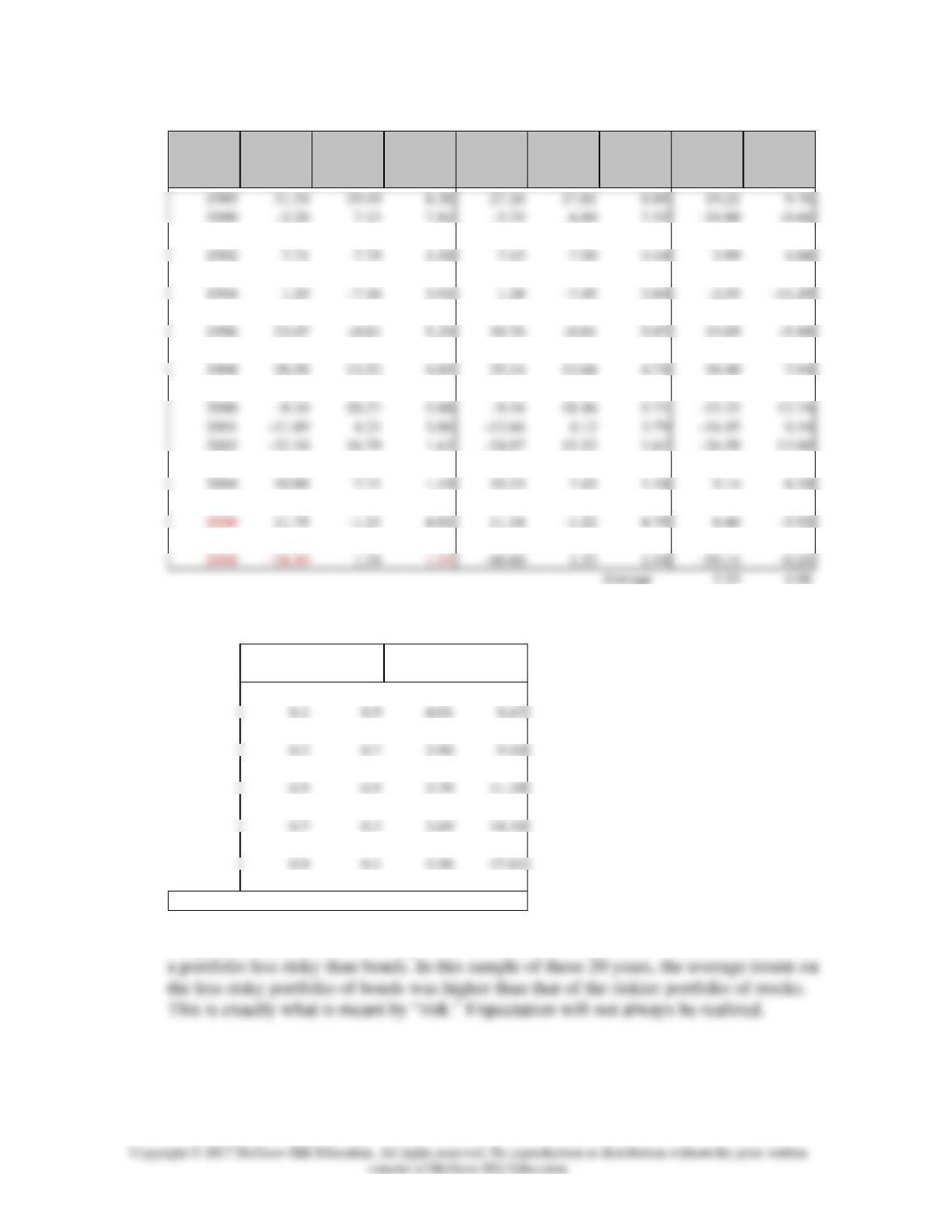

15. Since these are annual rates and the risk-free rate was quite variable during the sample

period of the recent 20 years, the analysis has to be conducted with continuously

compounded rates in excess of T-bill rates. Notice that to obtain cc rates we must

Chapter 06 – Efficient Diversification

Annual returns from Table 2 Continuously compounded rates Excess returns

Year

Large

Stock

Long-

Term T–

Bonds

T-Bills

Large

Stock

Long-

Term T–

Bonds

T-Bills

Large

Stock

Long-

Term T–

Bonds

1991 30.66 18.39 5.60 26.74 16.88 5.45 21.29 11.43

1993 9.87 15.48 2.90 9.41 14.39 2.86 6.55 11.53

1995 37.71 31.67 5.60 32.00 27.51 5.45 26.55 22.06

1997 33.17 15.08 5.25 28.65 14.05 5.12 23.53 8.93

1999 21.04 –8.74 4.69 19.10 –9.15 4.58 14.51 –13.73

2003 28.69 2.38 1.02 25.22 2.35 1.01 24.21 1.34

2005 4.91 6.50 2.98 4.79 6.30 2.94 1.86 3.36

2007 3.53 10.25 4.67 3.47 9.76 4.56 –1.10 5.20

SD 19.64 8.88

Corr(stocks,bonds) 0.13

Stocks Bonds Mean SD

0.0 14.06 8.88

0.2 0.8 3.95 8.55

0.4 0.6 3.85 10.05

0.6 0.4 3.74 12.74

0.8 0.2 3.63 16.04

1.0 03.53 19.64

Min–Var 0.1338 0.8662 3.99 8.44

Weights in

Portfolio

The bond portfolio is less risky as represented by its lower standard deviation. Yet, as

the portfolio table shows, mixing .87% of bonds with 13% stocks would have produced

16. If the lending and borrowing rates are equal and there are no other constraints on

portfolio choice, then the optimal risky portfolios of all investors will be identical.

17. No, it is not possible to get such a diagram. Even if the correlation between A and B

18. In the special case that all assets are perfectly positively correlated, the portfolio

standard deviation is equal to the weighted average of the component-asset standard

19. The probability distribution is:

Probability

Rate of Return

.7

100%

.3

-50%

20. The expected rate of return on the stock will change by beta times the unanticipated

change in the market return: 1.2 ( .08 – .10) = –2.4%

21.

a. The risk of the diversified portfolio consists primarily of systematic risk. Beta

measures systematic risk, which is the slope of the security characteristic line (SCL).

b. The undiversified investor is exposed primarily to firm-specific risk. Stock A

has higher firm-specific risk because the deviations of the observations from the

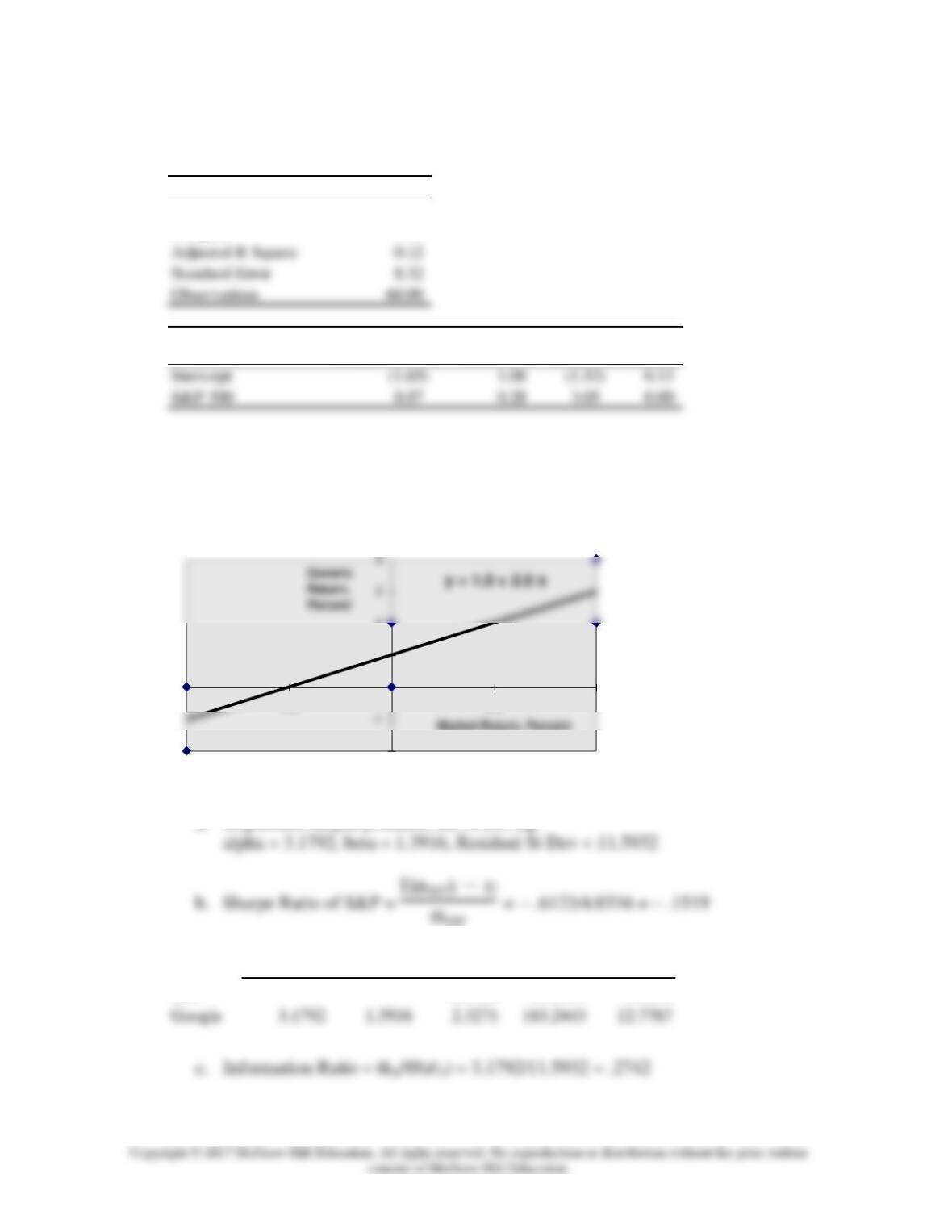

22. Using “Regression” command from Excel’s Data Analysis menu, we can run a

regression of Ford’s excess returns against those of S&P 500, and obtain the following

data. The Beta of Ford is .87.

Chapter 06 – Efficient Diversification

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.37

R Square 0.14

Coefficients

Standard

Error t Stat P-value

23. A scatter plot results in the following diagram. The slope of the regression line is 2.0

and intercept is 1.0.

-2

0

1

2

-1 -0.5 0 0.5 1

24. a. Regression output produces the following:

Alpha Beta E(r) – rf VAR SD

S&P -0.6123 16.2541 4.0316

Chapter 06 – Efficient Diversification

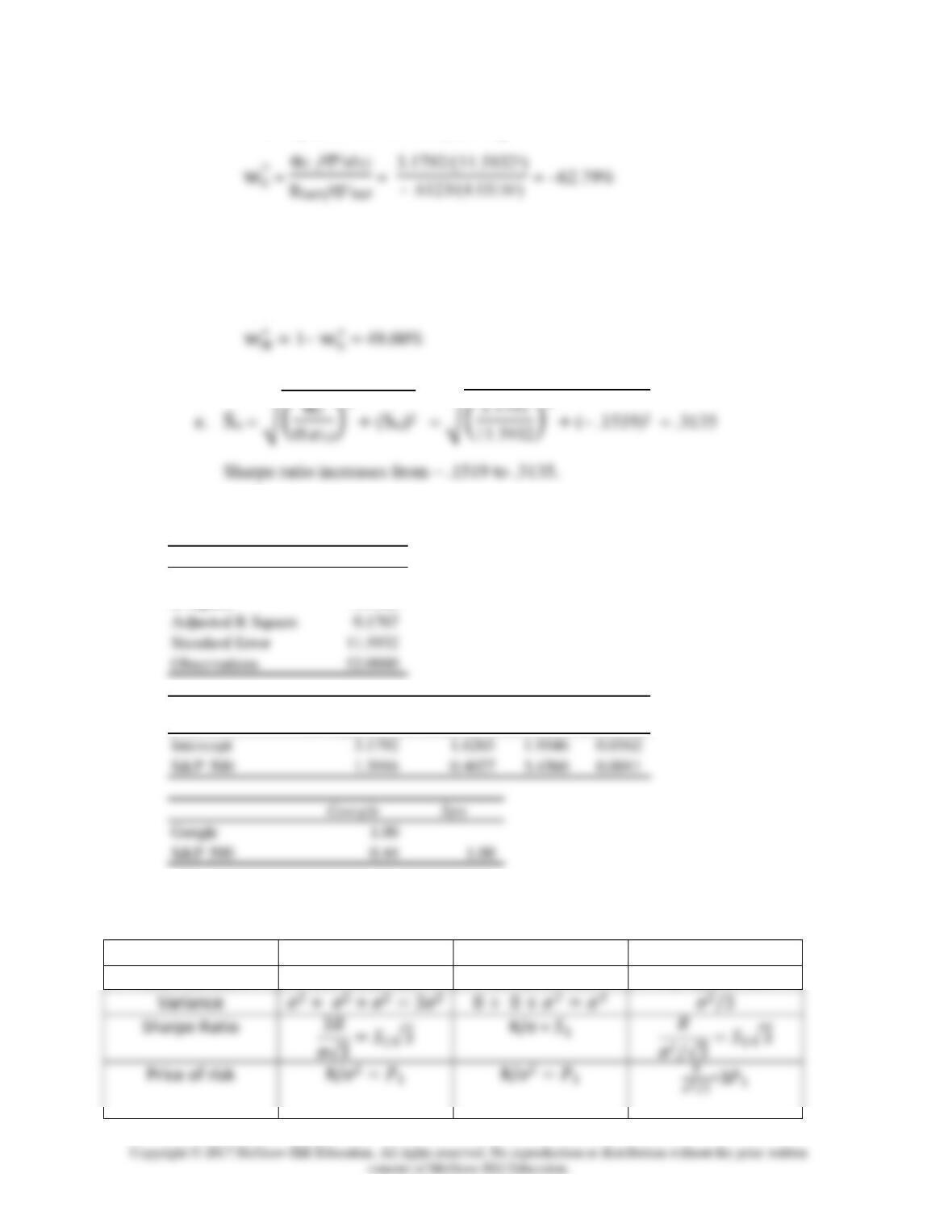

d. We use Equation 6.16 to compute wG

O

Then, plug wG

O into Equation 6.17 to compute the optimal position of Google in

the optimal risky portfolio and the weight in the market index:

wG

∗ = – .6279 / [1 + (– .6279 (1 – 1.3916)] = –50.40%

SUMMARY OUTPUT: Regression of Google on S&P 500 (excess returns)

Regression Statistics

Multiple R 0.4391

R Square 0.1928

Coefficients

Standard

Error

t Stat P-value

25.

a.

Strategy:

Three-In

One-In

Third-In-Three

Risk Premium

R + R + R = 3R

0 + 0 + R = R

3* 1/3 R = R

Chapter 06 – Efficient Diversification

b. The One-In strategy has the lowest Sharpe ratio

c. The Third-In-Three provides the highest price of risk.

f. The Third-In-Three investment’s price of risk is exactly three times higher than that

of the Three-In.

CFA 1 Answer:

CFA 2 Answer:

Fund D represents the single best addition to complement Stephenson’s current

portfolio, given his selection criteria. First, Fund D’s expected return (14.0 percent) has

the potential to increase the portfolio’s return somewhat. Second, Fund D’s relatively

CFA 3

Answer:

Chapter 06 – Efficient Diversification

i. E(rNP) = wOP E(rOP ) + wABC E(rABC ) = ( .9 .67) + ( .1 1.25) = .7280%

b. Subscript OP refers to the original portfolio, GS to government securities, and

NP to the new portfolio.

c. Adding the risk-free government securities would result in a lower beta for the

new portfolio. The new portfolio beta will be a weighted average of the individual

expected returns for the two securities under consideration are identical, the

correlation coefficients between each security and the original portfolio are

e. Grace clearly expressed the sentiment that the risk of loss was more important to

her than the opportunity for return. Using variance (or standard deviation) as a

CFA 4 Answer:

Chapter 06 – Efficient Diversification

CFA 5

Answer:

Risk reduction benefits from diversification are not a linear function of the number of

CFA 6

Answer:

The point is well taken because the committee should be concerned with the volatility

CFA 7

Answer:

a. Systematic risk refers to fluctuations in asset prices caused by macroeconomic

factors that are common to all risky assets; hence systematic risk is often

b. Trudy should explain to the client that picking only the five best ideas would

most likely result in the client holding a much more risky portfolio. The total

Chapter 06 – Efficient Diversification