Probability

Year end

cash flow

T-bill return

Solution

a.

Required risk premium =

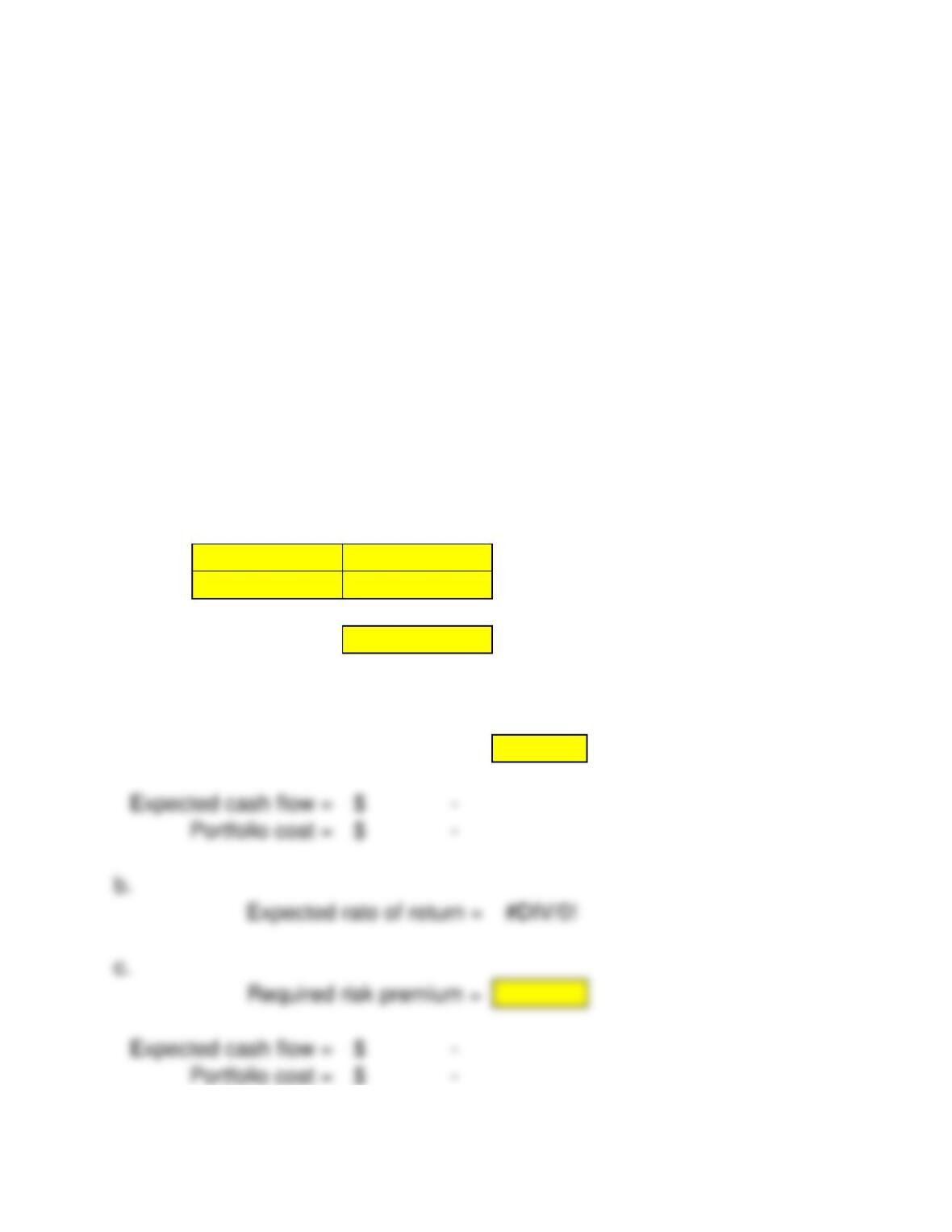

Consider a risky portfolio. The end-of-year cash flow derived from the

portfolio will be either $50,000 or $150,000, with equal probabilities of .5. The

alternative riskless investment in T-bills pays 5%.

a. If you require a risk premium of 10%, how much will you be willing to pay

for the portfolio?

b. Suppose the portfolio can be purchased for the amount you found in (a).

What will the expected rate of return on the portfolio be?

c. Now suppose you require a risk premium of 15%. What is the price you will

be willing to pay now?

d. Comparing your answers to (a) and (c), what do you conclude about the

relationship between the required risk premium on a portfolio and the price at

which the portfolio will sell?

Expected rate of return =

Required risk premium =

T-Bill rate of return

Standard deviation

Fund distribution

Solution

a.

0.0%

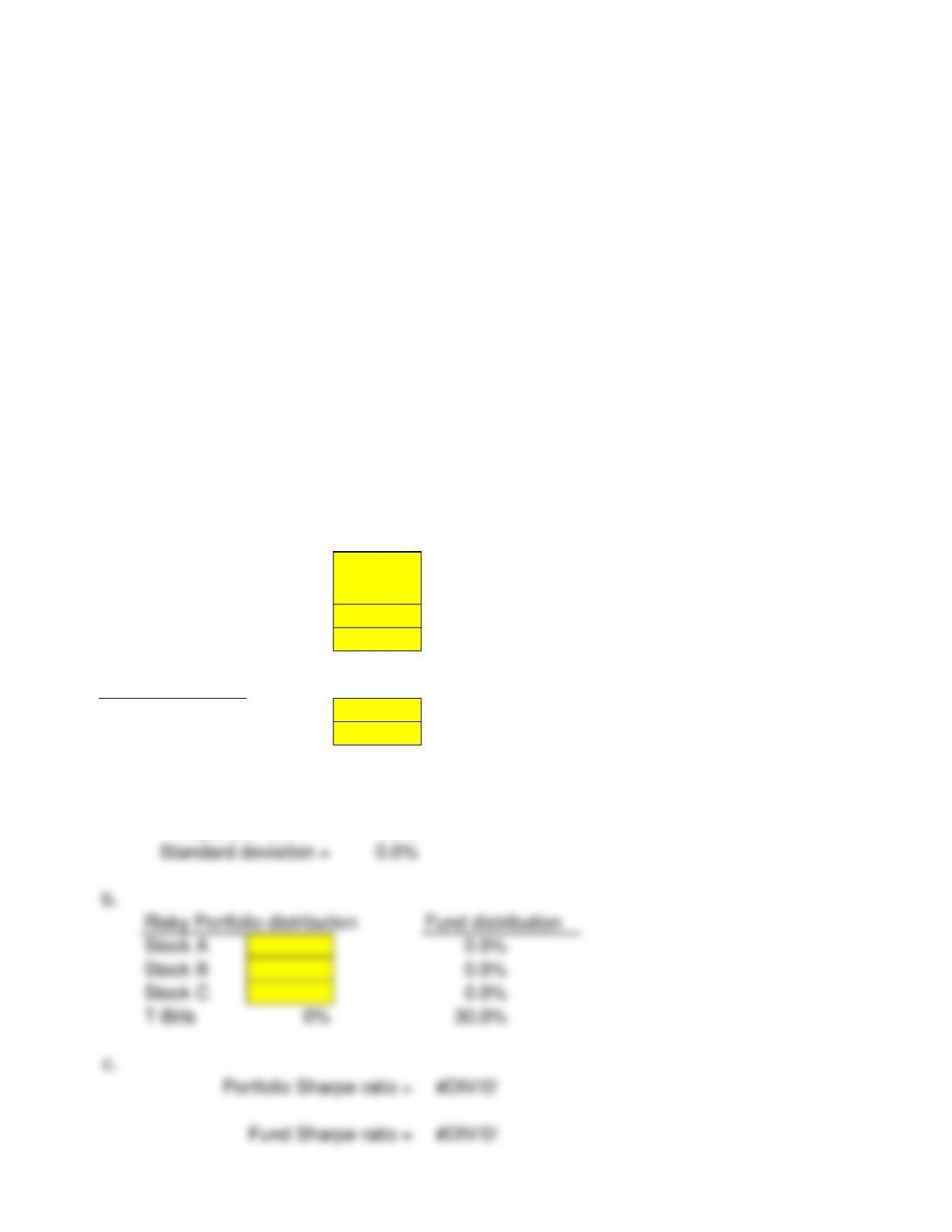

Assume that you manage a risky portfolio with an expected rate of return of 17%

and a standard deviation of 27%. The T-bill rate is 7%. Your client chooses to

invest 70% of a portfolio in your fund and 30% in a T-bill money market fund.

a. What is the expected return and standard deviation of your client’s portfolio?

b. Suppose your risky portfolio includes the following investments in the given

proportions:

Stock A 27%

Stock B 33%

Stock C 40%

What are the investment proportions of your client’s overall portfolio, including

the position in T-bills?

c. What is the reward-to-volatility ratio (S) of your risky portfolio and your

client’s overall portfolio?

d. Draw the CAL of your portfolio on an expected return/standard deviation

diagram. What is the slope of the CAL? Show the position of your client on your

fund’s CAL.

Expected rate of return

on a risky portfolio

Portfolio of risky assets =

T-Bill =

Expected return =

T-Bill rate of return

Standard deviation

S&P 500 fund expected rate of return =

S&P 500 fund standard deviation =

Solution

b.

#DIV/0!

Expected rate of return

on a risky portfolio

Slope of CML =

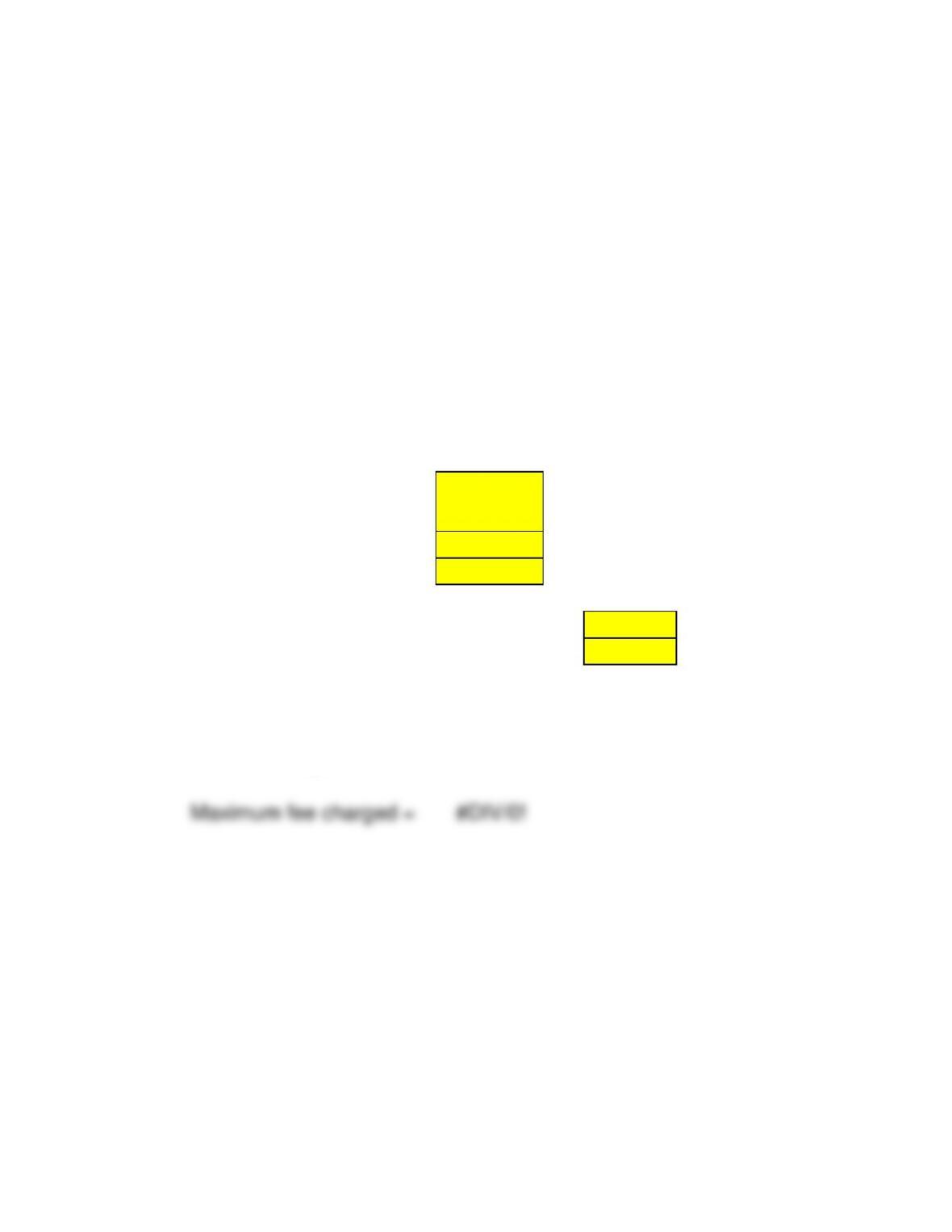

Assume that you manage a risky portfolio with an expected rate of return of 17%

and a standard deviation of 27%. The T-bill rate is 7%. You estimate that a

passive portfolio invested to mimic the S&P 500 stock index yields an expected

rate of return of 13% with a standard deviation of 25%. Your client wonders

whether to switch the 70% that is invested in your fund to the passive portfolio.

a. Explain to your client the disadvantage of the switch.

b. Show your client the maximum fee you could charge (as a percent of the

investment in your fund deducted at the end of the year) that would still leave

him at least as well off investing in your fund as in the passive one. (Hint: The

fee will lower the slope of your client’s CAL by reducing the expected return net

of the fee.)

Treasury bill return =

Investment allocation

Equity fund

Treasury bill

Solution

Expected return on equity fund = 0.00%

Equity fund expected risk premium =

Equity fund expected standard deviation =

You manage an equity fund with an expected risk premium of 10% and a

standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses

to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill

money market fund. What is the expected return and standard deviation of

return on your client’s portfolio?