Chapter 03 – Securities Markets

CHAPTER THREE

SECURITIES MARKETS

CHAPTER OVERVIEW

This chapter discusses how securities are traded on both the primary and secondary markets,

with coverage of both organized exchanges and over the counter markets. Margin trading and

LEARNING OBJECTIVES

After studying this chapter the student should understand the primary market issue methods and

how investment bankers assist in security issuance. The reader should be able to identify the

various security markets and should understand the differences between exchange and over the

counter trading. The student should understand the mechanics, risk, and calculations involved in

both margin and short trading and should begin to understand some of the implications,

ambiguities, and complexities of insider trading and the regulations concerning these issues.

CHAPTER OUTLINE

1. How Firms Issue Securities

PPT 3-2 through PPT 3-9

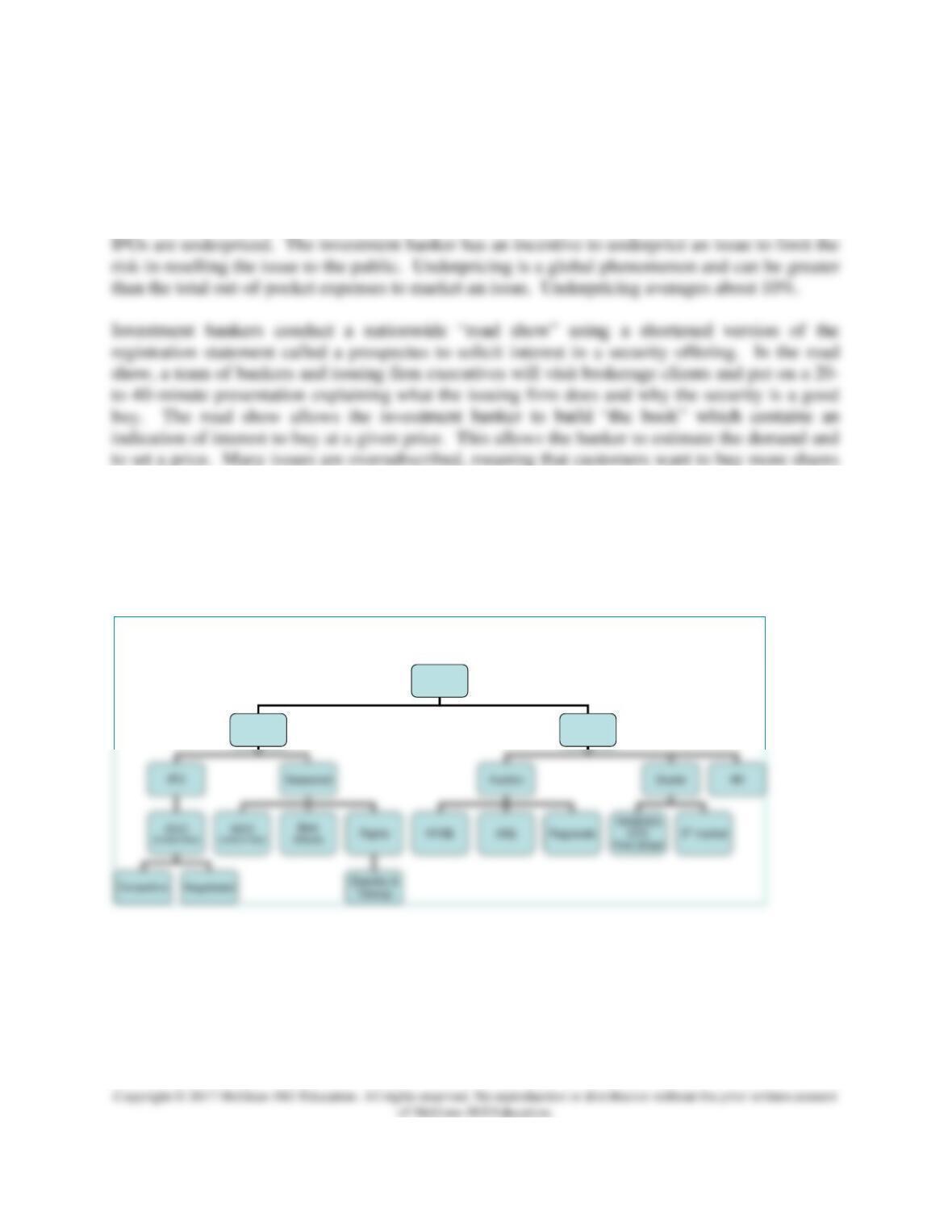

The term primary market refers to the market where new securities are issued and sold. The key

characteristic of this market is that the issuer receives the proceeds from the sale. In the

secondary market, existing securities are traded among investors. The issuing firm doesn’t

receive any proceeds and is not directly involved.

Auction

Chapter 03 – Securities Markets

A General Cash Offer (GCO) can be used for an IPO or a seasoned offering. An IPO is the

initial public offering versus a seasoned offering which is issuing additional equity after the

firm’s IPO. The typical spread for an equity IPO is 7%. IPOs are very expensive. In addition to

out-of-pocket costs which may range from $300,000 to $500,000 depending on issue size, most

than are being offered. This allows the banker to allocate the shares to their better customers and

creates a ‘winner’s curse’ problem for a smaller investor. The IPO smaller investors can actually

get is not going to be a good IPO, otherwise it would be oversubscribed and no shares would be

available. Oversubscription has led to many abuses by Wall Street bankers, who have allocated

shares to firms in exchange for subsequent underwriting business and other perquisites. These

activities are illegal and have led to large fines for many investment bankers.

Equity

Primary

Secondary

Chapter 03 – Securities Markets

GCOs may be competitive or negotiated. In a competitive GCO the issuing firm solicits sealed bids from

competing investment banks. In a negotiated deal (by far the most common), the issuing firm works with

the public. Once the shelf registration is approved, the firm may issue the securities at any time within

two years by providing the SEC with 24-hour notice of issuance. This provides the issuer with greater

flexibility in timing when to market the issue. There are certain minimum-firm-size restrictions to qualify

and firms cannot have recently violated certain securities laws and disclosure requirements.

Certain private placements rules are governed by SEC Rule 144A. Private placements allow a firm to sell

2. How Securities Are Traded

PPT 3-10 through PPT 3-15

The overarching purpose of financial markets is to facilitate low cost investment.

a) Markets bring together buyers and sellers at low cost and there are different types of markets:

• Direct search market:

• Buyers and sellers locate one another on their own

Chapter 03 – Securities Markets

b) Well functioning markets provide adequate liquidity by minimizing time and cost to trade

and promoting price continuity.

Types of Orders

a) Order type

Market orders execute immediately at the best price. Limit orders are orders to buy or sell at a

specified price or better. The limit order is placed in a limit-order book kept by an exchange

official or computer. For example, if a stock is trading at $50 an investor might place a buy limit

at $49.50 or a sell limit order at $50.25. The limit order may or may not execute depending on

which way the market price moves. The range around the current price that the limit should be

set depends on the price the investor is willing to pay. Setting the price further from the current

market reduces the probability of execution.

b) Time dimensions on orders: Limits and stop orders also have a time dimension. These

orders may be immediate or cancel (IOC); good for the day only (Day) (typically the

default); or good till cancelled (GTC).

3. The Rise of Electronic Trading

PPT 3-16 through PPT 3-18

Chapter 03 – Securities Markets

New technologies and regulations have driven markets towards electronic trading. The first

ECN, Instinet, was established in 1969. In 1975, fixed commissions on the NYSE were

eliminated, which freed brokers to compete for business by lowering their fees. In that year also,

Congress amended the Securities Exchange Act to create a National Market System to at least

partially centralize trading across exchanges and enhance competition among different market

4. U.S. Markets

PPT 3-19 through PPT 3-20

A dealer market is a market without centralized order flow. The NASDAQ is a dealer market.

NASDAQ is the largest organized stock market for over-the-counter or OTC trading. NASDAQ

is a computer information system for individuals, brokers and dealers. It connects more than

350,000 terminals and processes more than 5,000 transactions per second (Source: NASDAQ).

Securities traded include stocks, most bonds and some derivatives.

Auction markets are markets with centralized order flow. In these markets the dealership

function can be competitive or assigned by the exchange as in the case of NYSE Specialists.

Examples include the NYSE, the American Stock Exchange (ASE), the Chicago Board Options

Exchange (CBOE), the Chicago Mercantile Exchange (CME) and others.

The unique role of the specialist deserves some attention. The specialist is an exchange-

appointed firm in charge of the market for a given stock. A specialist acts as both a broker and a

dealer in the market. The specialist is charged with maintaining a continuous, orderly market.

5. New Trading Strategies

PPT 3-21

Electronic trading has spawned a number of new trading strategies. Algorithmic trading

6. Globalization of Stock Markets

PPT 3-23 through PPT 3-22-23

7. Trading Costs

PPT 3-25

8. Buying on Margin

PPT 3-25 through PPT 3-31

Buying stock on margin is not the same as a margin arrangement in futures. While both futures

and stock trading have similar maintenance margins and margin calls, the costs of borrowed

funds must be factored into analysis of the returns of stock margin trading. The degree of

leverage available in equities is set by the Federal Reserve Board under Regulation T and is less

than is typically available in futures.

9. Short Sales

PPT 3-32 through PPT 3-40

With the background developed in margin trading, the concept of short selling is covered next. A brief

description of the mechanics of a short sale is first introduced. The instructor may wish to use slide 35 or

skip it. Slide 35 compares long positions with short positions.

A short seller has a liability as opposed to an asset. The liability is that the short seller must buy the stock

10. Regulation of Securities Markets

PPT 3-41

A brief history of securities regulation is provided and the new Financial Industry Regulatory

Authority (FINRA) created in 2007 is mentioned. The instructor may wish to cover the Excerpts

from the CFA Institute Standards of Professional Conduct found on PPT slide 68.

Recent scandals have rocked the securities markets and a great deal of press coverage has been

2. ‘Good Government and Animal Spirits: Every Talented Player Understands the

3. ‘How Business Schools Have Failed Business: Why Not More Education on the

Responsibility of Boards?’ by Michael Jacobs, Wall Street Journal Online, April 24,

2009.

Chapter 03 – Securities Markets

5. ‘Can Ethical Restraint Be Part of the Solution to the Financial Crisis?’ by Stephen

Jordan, Fellow, Caux Round Table

Excel Applications

Two Excel models are available for margin trading and short sales. These models allow students

to examine the impact of margining combined with stock price volatility.