assets. Due to the relation between the modified duration and Macaulay duration, the modified

duration analysis can be classified in terms of the latter. Manager C should agree with Manager

16. Why is there greater risk in a multiperiod immunization strategy than a cash flow-matching

strategy?

To understand the greater risk in a multiperiod immunization strategy, we need to first

understand the differences between the cash flow matching and multiperiod immunization

strategies. First, unlike the immunization approach, the cash flow matching approach has no

duration requirements. Second, with immunization, rebalancing is required even if interest rates

do not change. In contrast, no rebalancing is necessary for cash flow matching except to delete

17. Answer the below questions.

(a) What is a contingent immunization strategy?

A contingent immunization strategy is a strategy that consists of identifying both the available

immunization target rate and a lower safety net level return with which the investor would be

minimally satisfied. More details are given below.

For a contingent immunization strategy, the portfolio manager pursues an active portfolio

strategy until an adverse investment experience drives the then-available potential return—the

combined active return from actual past experience and immunized return from expected future

plan is abandoned.

(b) What is the safety net cushion in a contingent immunization strategy?

The safety cushion is the difference between the immunized return and the safety net return.

More details including an illustration of the safety cushion is given below.

Suppose that a client investing $50 million is willing to accept a 10% rate of return over

a four-year investment horizon at a time when a possible immunized rate of return is 12%. The

(c) Is it proper to classify a contingent immunization as a combination active/immunization

strategy?

In a contingent strategy, the portfolio manager is permitted to manage the portfolio actively until

the safety net is violated. The manager could theoretically employ an active strategy for the whole

period. While it is doing this, it is also following the guidelines of an immunization strategy. Given

these considerations, one might classify a contingent immunization as a combination

18. What is a combination matching strategy?

A popular variation of multiperiod immunization and cash flow matching to fund liabilities is

one that combines the two strategies. This strategy, referred to as combination matching or

horizon matching, creates a portfolio that is duration matched with the added constraint that it

19. In a stochastic liability funding strategy, why is an interest-rate model needed?

Changes in interest rates impact the cash flows for a stochastic liability funded strategy. Thus, an

interest model is needed to track the cash flows. More details are given below.

Since the mid-1980s, a number of models have been developed to handle real-world situations in

which liability payments and / or asset cash flows are uncertain. Such models are called

stochastic models. Such models require that the portfolio manager incorporate an interest-rate

20. Suppose that a client has granted an asset management firm permission to pursue an

active/immunized combination strategy. Suppose further that the minimum return

expected by the client is 9% and that the asset management firm believes that an

achievable immunized target return is 14% and the worst possible return from the actively

managed portion of the portfolio is 1%. Approximately how much should be allocated to

the active component of the portfolio?

The following formula can be used to determine the portion of the initial portfolio to be managed

actively, with the balance immunized:

immunization target rate expected worst case active return

−

In the formula it is assumed that the immunization target return is greater than either the

minimum return established by the client or the expected worst-case return from the actively

managed portion of the portfolio. Inserting in our values we get:

©2013 Pearson Education

553

active component =

14% 9%

14% 1%

−

−

=

5%

11%

= 0.454545 or about 45.45%.

21. A liability-driven strategy for defined benefit pension funds is to create an immunizing

portfolio and an excess return portfolio. Explain this strategy.

Ross, Bernstein, Ferguson, and Dalio of Bridgewater Associates propose the following

liability-driven strategy for a pension plan, which involves two steps. First, create an immunizing

portfolio. The purpose of this portfoliois to hedge the adverse consequences associated with the

exposure to the liabilities. Second, create what they refer to as an “excess return portfolio.” The

22. The following excerpt is from a January 18, 2008 article (“LDI Strategy that is Liable to

Word?”) by Penny Green, Chief Executive of the SAUL Trustee Company (a U.K. that

advises on pension management) and deals with liability-driven strategies:

“…there is no one asset class that precisely matches a plan’s liabilities. It is the case that

bonds provide a cash flow that can be used to meet the cash flows out of a pension plan.

But so do equities – it is just that the cash flows from equities (dividends) cannot be

Explain why you agree or disagree with this viewpoint.

In general one would agree with the views being presented concerning (i) the problems of any

asset class rendering cash flows that can perfectly match a plan’s liabilities, and (ii) the

shortcomings of any asset class meeting longevity risk. More details are given below.

23. In explaining how a pension fund should transition to a liability-driven investment strategy,

Duane Rocheleau, managing director of Northern Trust’s global investment solutions team,

writes in “Implementing LDI in Pension Plans,” January 2007:

“1. Analyze and characterize the liabilities;

Describe each of the above elements.

In terms of analyzing and characterizing the liabilities, the manager wants to know the amounts

of cash flows and the timing of the cash flows that are owed pension fund recipients. This is

In terms of quantifying the relation between the assets and liabilities, the manager wants to be

able to match the cash flows from the assets with those of the liabilities so that pension fund

recipients will be paid in full and on time. To understand this problem and the need to quantify,

In regards to developing and implementing appropriate investment strategies, there are two

strategies to choose from: multiperiod immunization and cash flow matching.

A multiperiod immunization strategy is one in which a portfolio is created that will be capable of

satisfying more than one predetermined future liability regardless if interest rates change. Even if

there is a parallel shift in the yield curve, it has been demonstrated that matching the duration of

A cash flow matching strategy is used to construct a portfolio that will fund a schedule of

liabilities from a portfolio’s cash flows, with the portfolio’s value diminishing to zero after

payment of the last liability. This strategy can be summarized as follows. A bond is selected with

In regards to further action (monitoring, rebalancing, and tweaking) on the investment strategy as

necessary, we can note that action is required because the market yield will fluctuate over the

investment horizon. As a result, the duration of the portfolio will change (and change by more

than that caused simply by the passage of time).In the face of changing yields, a portfolio can

A question we can pose is: How often should the portfolio be rebalanced to adjust its duration?

24. One of your clients, a newcomer to the life insurance business, questioned you about the

following excerpt from Peter E. Christensen, Frank J. Fabozzi, and Anthony LoFaso,

“Dedicated Bond Portfolios,” Chapter 43 in Frank J. Fabozzi (ed.), The Handbook of Fixed

Income Securities (Homewood, IL: Richard D. Irwin, 1991):

For financial intermediaries such as banks and insurance companies, there is

a well-recognized need for a complete funding perspective. This need is best illustrated

by the significant interest-rate risk assumed by many insurance carriers in the early

years of their Guaranteed Investment Contract (GIC) products. A large volume of

Answer the below questions posed to you by your client.

(a) “It is not clear to me what risk an issuer of a GIC is facing. A carrier can invest the

proceeds in assets offering a higher yield than they are guaranteeing to GIC policyholders,

so what’s the problem? Isn’t it just default risk that can be controlled by setting tight credit

standards?”

An issuer of a GIC is facing reinvestment rate risk. As rates increase, the issuer of a GIC will

face paying a higher rate of return on subsequent securities because GICs mature in three to

seven years. This liability is matched by a longer term asset that pays an increasingly lower

©2013 Pearson Education

557

assets gave a return too low to meet the return guaranteed on the liabilities. This problem has no

immediate relationship to default risk. However, due to the mismatch in assets and liabilities the

company has put itself in a precarious net surplus situation.

(b) “I understand that disintermediation means that when a policy matures, the funds are

withdrawn from the insurance company by the policyholder. But why would a rise in

interest rates cause GIC policyholders to withdraw their funds? The insurance company

can simply guarantee a higher interest rate.”

Under a GIC policy, for a lump-sum payment a life insurance company guarantees that specified

dollars will be paid to the policyholder at a specified future date. Or, equivalently, the financial

institution (i.e., life insurance company) guarantees a specified rate of return on the payment.

(c) “What do the authors mean by ‘pricing GICs on a spread basis and investing the

proceeds on a mismatched basis,’ and what is this ‘rollover risk’ they are referring to?”

The GICs were priced such that the bank and insurance companies would realize what they

believed was a healthy spread compared to other possible liabilities. However, the profit was

25. Suppose that a life insurance company sells a five-year guaranteed investment contract

that guarantees an interest rate of 7.5% per year on a bond-equivalent yield basis (or

equivalently, 3.75% every six months for the next 10 six-month periods). Also suppose that

the payment made by the policyholder is $9,642,899.

Consider the following three investments that can be made by the portfolio manager:

Bond X: Buy $9,642,899 par value of an option-free bond selling at par with a 7.5%

yield to maturity that matures in five years.

Answer the below questions.

(a) Holding aside the spread that the insurance company seeks to make on the invested

funds, demonstrate that the target accumulated value to meet the GIC obligation five years

from now is $13,934,413.

To compute the target accumulated value, we need to take the future value of the annuity

resulting from the policyholder’s payment and add it to this payment due at the end of the last

period. We have:

annual coupon rate

(1 + 1

)

−

n

y

(b) Complete Table A assuming that the manager invests in bond X and immediately

following the purchase, yields change and stay the same for the five-year investment horizon.

For the each row, we have six columns. Below we show how all values are gotten for the first

row of 11.00%. The same process can be repeated to get values for the remaining rows.

Column One gives the new yield which is 11% for the first row. This means the semiannual yield

will be 5.5%. This value changes for each row with each new yield provided for each row.

For (i), we have:

annual coupon rate

2

(P)

(1 + 1

)

−

n

y

y

=

0.075

2

($9,642,899)

10

(1.055 1

)

0.055

−

=$361,608.71[12.87535379] = $4,655,840.11.

Column Five is the total accumulated value. This is computed by adding (i) the future value of

semiannual coupon payment annuity for ten periods at the yield of 11% 2 = 5.5%and (ii) the

maturity value given in the fourth column. The value for (i) was given previously as

$4,655,840.11 when computing the interest on interest. This value is also given by adding the

second and third column values. The value for (ii) is $9,642,899 as given in the fourth column.

For the accumulated value, we have:

changes for each row.

We repeat the above process to get all values for each row. These values are given below with

Table A filled in.

Table A

Accumulated Value and Total Return After Five Years:

Five-Year 7.5% Bond Selling to Yield 7.5%

Investment horizon (years): 5

Coupon rate: 7.50%

Maturity (years): 5

Yield to maturity: 7.50%

Price: 100.00000

Par value purchased: $9,642,899

Purchase price: $9,642,899

Target accumulated value: $13,934,413

After Five Years

New Yield

Coupon

Interest on

Interest

Price of

Bond

Accumulated

Value

Total Return

11.00%

$3,616,087

$1,039,753

$9,642,899

$14,298,739

8.04%

10.00%

$3,616,087

$ 932,188

$9,642,899

$14,191,175

7.88%

9.00%

$3,616,087

$ 827,436

$9,642,899

$14,086,423

7.73%

8.00%

$3,616,087

$ 725,426

$9,642,899

$13,984,412

7.57%

7.50%

$3,616,087

$ 675,427

$9,642,899

$13,934,413

7.50%

7.00%

$3,616,087

$ 626,089

$9,642,899

$13,885,073

7.43%

6.00%

$3,616,087

$ 529,352

$9,642,899

$13,788,338

7.28%

5.00%

$3,616,087

$ 435,153

$9,642,899

$13,694,139

7.14%

4.00%

$3,616,087

$ 343,427

$9,642,899

$13,602,414

7.00%

(c) Based on Table A, under what circumstances will the investment in bond X fail to satisfy

the target accumulated value?

Given that the target accumulated value is $13,934,413, we see any new yield below 7.50% will

(d) Complete Table B, assuming that the manager invests in bond Y and immediately

following the purchase, yields change and stay the same for the five-year investment horizon.

For the each row, we have six columns. Below we show how all values are gotten for the first

will be 5.5%. This value changes for each row with each new yield provided for each row.

For (ii), we have: n(semiannual coupon payment) = 10[(0.0375)($9,642,899]) = 10[$361,608.71]

= $3,616,087.13. Note that this value is the value also computed in column two.

Column Four provides the maturity value of the bond, which is $8,024,638.89. This value is

computed by taking the present value of the bond value at the end of five years. Because the

maturity has seven remaining years after five years, this means we compute (i) the value at the

0.055

©2013 Pearson Education

562

For (ii), we get:

( )

P

1+n

y

=

( )

14

$9,642,899

1.055

= $9,642,899(0.4725693866) = $4,556,938.66.

Adding (i) and (ii), we get the value of the bond price at the beginning of period 11 (or at the end

of period 10) as $3,467,700.23 + $4,556,938.66 = $8,024,638.89 or about $8,024,639. This value

changes for each row because it is a function of the new yield which changes for each row.

Column Five is the total accumulated value. This is computed by adding (i) the future value of

semiannual coupon payment annuity for ten periods at the yield of 11% 2 = 5.5%and (ii) the

policyholder payment

where accumulated value is the fifth column value of $12,680,479.00, the policyholder payment

is the value of $9,642,899, and n is the number of periods which is 10. Inserting in these values,

we have:

Table B

Accumulated Value and Total Return After Five Years:

Twelve-Year 7.5% Bond Selling to Yield 7.5%

Investment horizon (years): 5

Coupon rate: 7.50%

Maturity (years): 12

Yield to maturity: 7.50%

Price: 100.00000

Par value purchased: $9,642,899

Purchase price: $9,642,899

Target accumulated value: $13,934,413

After Five Years

New Yield

Coupon

Interest on

Interest

Price of

Bond

Accumulated

Value

Total Return

11.00%

$3,616,087

$1,039,753

$8,024,639

$12,680,479

5.55%

10.00%

$3,616,087

$ 932,188

$8,449,753

$12,998,030

6.06%

9.00%

$3,616,087

$ 827,436

$8,903,566

$13,347,090

6.61%

8.00%

$3,616,087

$ 725,426

$9,388,251

$13,729,764

7.19%

7.50%

$3,616,087

$ 675,427

$9,642,899

$13,934,413

7.50%

7.00%

$3,616,087

$ 626,089

$9,906,163

$14,148,337

7.82%

6.00%

$3,616,087

$ 529,352

$10,459,851

$14,605,289

8.48%

5.00%

$3,616,087

$ 435,153

$11,052,078

$15,103,318

9.18%

4.00%

$3,616,087

$ 343,427

$11,685,837

$15,645,352

9.92%

(e) Based on Table B, under what circumstances will the investment in bond Y fail to

satisfy the target accumulated value?

Given that the target accumulated value is $13,934,413, we see any new yield above 7.50% will

give accumulated value which is less than the target.

This is due to fact that the increase in interest rates lowers the value of the coupon and principal

payments which are discounted at a higher yield in the future.

(f) Complete Table C, assuming that the manager invests in bond Z and immediately

following the purchase, yields change and stay the same for the five-year investment

horizon.

For the each row, we have six columns. Below we show how all values are gotten for the first

row of 11.00%. The same process can be repeated to get values for the remaining rows in the

table.

564

Column One gives the new yield which is 11% for the first row. This means the semiannual yield

will be 5.5%. This value changes for each row with each new yield provided for each row.

Column Two provides the coupon which is the total interest paid for each of the ten periods.

Thus, the interest paid is ten times the semiannual coupon payment. The semiannual coupon

payment is the semiannual coupon rate (0.06752 = 0.03375) times the par value purchased of

$10,000,000. We have: 10[(0.03375)($10,000,000]) = 10[$337,500] = $3,375,000. This value is

the same for each row since the coupon rate of 6.75% does not change.

Column Three provides interest on interest. To get interest on interest, we compute (i) the future

value of semiannual coupon payment annuity for ten periods at the yield of 11% 2 = 5.5%, and

(ii) the total interest paid which is the number of periods (10) times the semiannual coupon

payment (0.03375× $10,000,000). For (iii), we take the value in (i) minus the value in (ii).

For (i), we have:

annual coupon rate

2

(P)

−

y

yn1

)

+ (1

=

0.0675

2

($10,000,000)

055.0

1

)

055(1. 10

−

= $337,500[12.87535379] = $4,345,431.90.

For (ii), we have: n(semiannual coupon payment) = 10[(0.03375)($ 10,000,000]) = 10[$337,500]

= $3,375,000. Note that this value is the value also computed in column two.

For (iii), we have:$4,345,431.90 – $3,375,000 = $970,431.90.

This third column value changes for each row because it is a function of the new yield which

annual coupon rate

2

(P)

( )

1

1

1 +

−

n

y

y

=

0.0675

2

($10,000,000)

( )

2

1

1

1 .055

0.055

−

= $337,500[1.8463197] = $623,132.90.

( )

P

1+n

y

)055.1(

000,000,10$

2

Adding (i) and (ii), we get the value of the bond price at the beginning of period 11 (or at the end

of period 10) as $623,132.90+ $8,984,524.16 = $9,607,657.06 or about $9,607,657. This value

changes for each row because it is a function of the new yield which changes for each row.

Column Five is the total accumulated value. This is computed by adding (i) the future value of

total return = 2

1/

accumulated value 1

policyholder payment

−

n

$9,642,899

7.53%. This value changes for each row because it is a function of the new yield which changes

for each row.

Table C

Accumulated Value and Total Return After Five Years:

Six-Year 6.75% Bond Selling to Yield 7.5%

Investment horizon (years): 5

Coupon rate: 6.75%

Maturity (years): 6

Yield to maturity: 7.5%

Price: 96.42899

Par value purchased: $10,000,000

Purchase price: $9,642,899

Target accumulated value: $13,934,413

After Five Years

New Yield

Coupon

Interest on

Interest

Price of

Bond

Accumulated

Value

Total Return

11.00%

$3,375,000

$970,432

$ 9,607,657

$13,953,089

7.53%

10.00%

$3,375,000

$870,039

$ 9,789,325

$13,942,885

7.51%

9.00%

$3,375,000

$772,271

$ 9,882,119

$13,936,596

7.50%

8.00%

$3,375,000

$677,061

$ 9,929,017

$13,934,180

7.50%

7.50%

$3,375,000

$630,395

$ 9,976,254

$13,934,413

7.50%

7.00%

$3,375,000

$584,345

$10,071,755

$13,935,599

7.50%

6.00%

$3,375,000

$494,059

$10,168,650

$13,940,814

7.51%

5.00%

$3,375,000

$406,141

$10,266,965

$13,949,791

7.52%

4.00%

$3,375,000

$320,531

$10,266,965

$13,962,495

7.54%

(g) Based on Table C, under what circumstances will the investment in bond Z fail to

satisfy the target accumulated value?

for 8.00% yield where the target value is $13,934,180 which is $133 off.

(h) What is the modified duration of the liability?

Modified duration is a measure of the sensitivity of a bond’s price to interest-rate changes,

assuming that the expected cash flow does not change with interest rates. One modified duration

expression we can use is:

( )

( )

( )

1

2

100 /

1

1

11

+

−

−+

++

nn

n C y

C

yyy

For our bond (expressing numbers in terms of a $100 bond quote), we have: C = $3.75, y =

0.0375, n = 10, and P = $96.43. Inserting these values in our modified duration formula, we can

solve as follows:

( )

( )

( )

1

2

100 /

1

1

11

+

−

−+

++

nn

n C y

C

yyy

P

=

( ) ( )

( )

( )

2 10 11

10 $100 $3.75/ 0.0375

$3.75 1

1

0.375 1 .0375 1 .0375

$96.43

−

−+

=

$2,666.67 (0.3079795) $0

$96.43

+

=

$821.28

$96.43

= 8.52.

(i) Complete the following table for the three bonds assuming that each bond is trading to

yield 7.5%:

Bond

Modified Duration

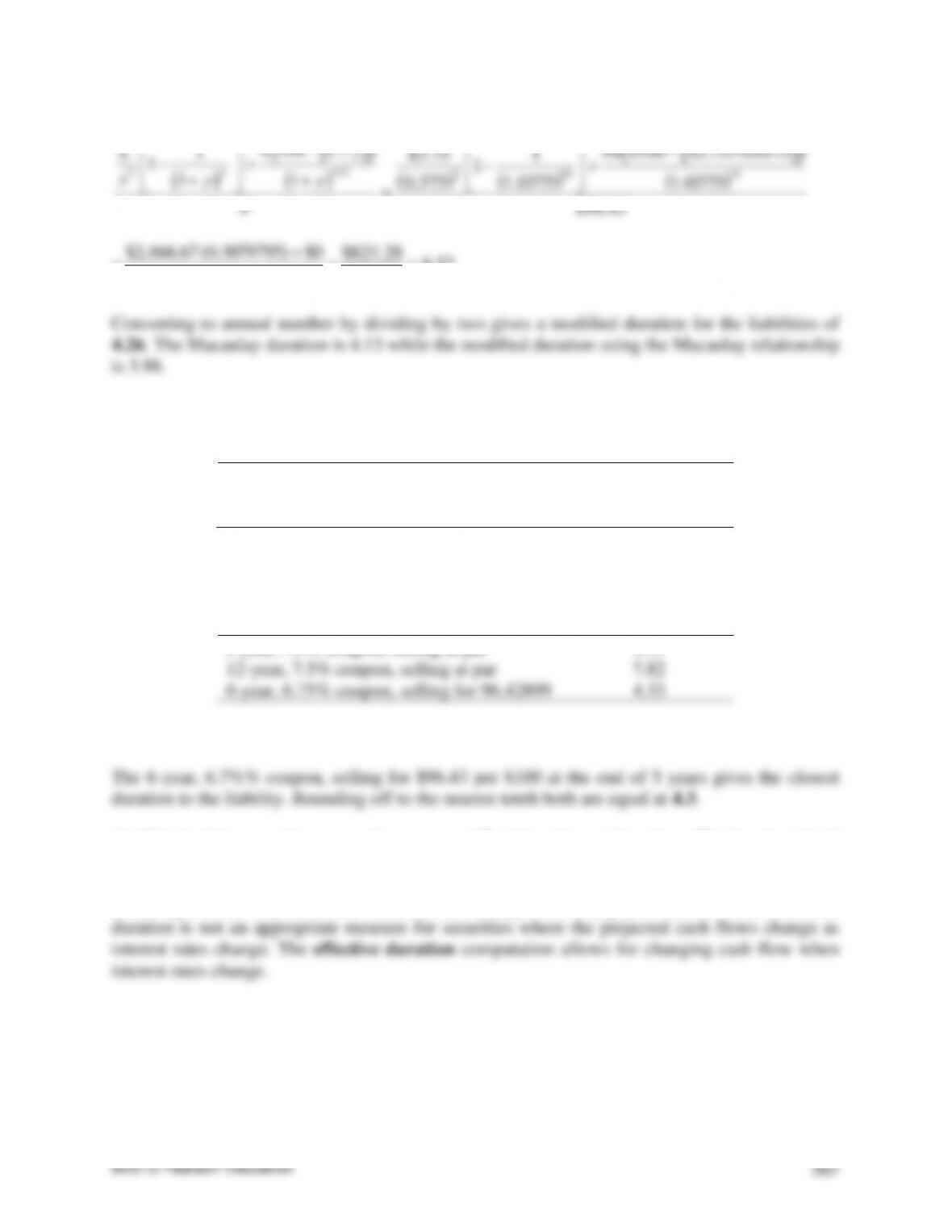

5-year, 7.5% coupon, selling at par

12-year, 7.5% coupon, selling at par

6-year, 6.75% coupon, selling for 96.42899

Using the formula in part (h) for modified duration, we get the below values as given in the

completed table:

Bond

Modified Duration

5-year, 7.5% coupon, selling at par

4.11

12-year, 7.5% coupon, selling at par

7.82

6-year, 6.75% coupon, selling for 96.42899

4.33

(j) For which bond is the modified duration equal to the duration of the liability?

(k) Why in this example can one focus on modified duration rather than effective duration?

Modified duration is a measure of the sensitivity of a bond’s price to interest-rate changes,

assuming that the expected cash flows do not change with changes in interest rates. Modified