Month 2001

Portfolio

A’s Return

Lehman Aggregate

Bond Index Return

Active

Return

Differences

Squared

January

2.15%

1.65%

0.50%

0.0707(%2)

February

0.89%

–0.10%

0.99%

0.5713(%2)

March

1.15%

0.52%

0.63%

0.1567(%2)

April

–0.47%

–0.60%

0.13%

0.0109(%2)

May

1.71%

0.65%

1.06%

0.6820(%2)

June

0.10%

0.33%

–0.23%

0.2155(%2)

July

1.04%

2.31%

–1.27%

2.2625(%2)

August

2.70%

1.10%

1.60%

1.8655(%2)

September

0.66%

1.23%

–0.57%

0.6467(%2)

October

2.15%

2.02%

0.13%

0.0109(%2)

November

–1.38%

–0.61%

–0.77%

1.0084(%2)

December

–0.59%

–1.20%

0.61%

0.1413(%2)

Sum of Portfolio Returns =

2.81%

Mean Active Return =

0.2342%

Variance (sum of differences squared / 11) =

0.6947(%2)

Standard Deviation = Tracking Error =

0.8335%

Tracking error in basis points =

83.35

Tracking error in basis points annualized =

288.74

To compute the standard deviation of these active returns, we subtract the average (or mean)

active return from each active return, and then square each difference. Each difference squared

value is given in the table above in the “Differences Squared” column. We then divided this sum

(b) Is the tracking error computed in part (a) a backward-looking or forward-looking

tracking error?

The tracking error computed in part (a) is backward-looking because it is calculated based on the

actual active returns observed for a portfolio is prior periods. Calculations computed for a portfolio

(c) Compare the tracking error found in part (a) to the tracking error found for Portfolios

A and B in Exhibits 23-1 and 23-2. What can you say about the investment management

strategy pursued by this portfolio manager?

The tracking error found for our problem is greater especially compared to Portfolio A. A greater

©2013 Pearson Education

518

tracking error means greater deviation from the benchmark. This is seen if we compare active

return values from our table with the greater active return values found in the exhibits. For our

problem, it appears the manager may be employing a high-risk strategy to enhance the indexed

portfolio’s return. This strategy is commonly referred to as enhanced indexing or indexing

plus.

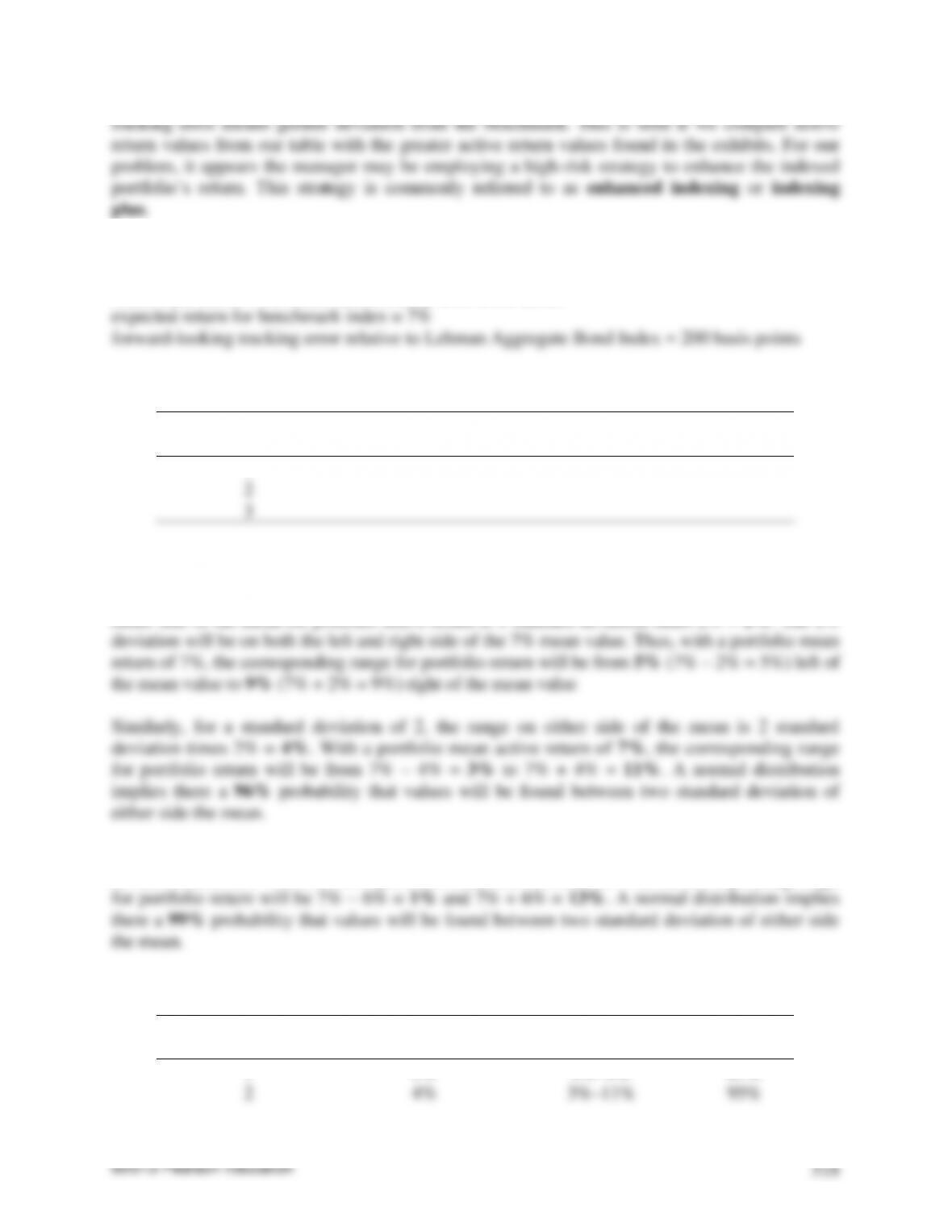

11. Assume the following:

benchmark index = Salomon Smith Barney BIG Bond Index

Assuming that returns are normally distributed, complete the following table:

Number of Standard

Deviations

Range for Portfolio

Active Return

Corresponding Range

for Portfolio Return

Probability

1

2

3

With an expected return of 7% and a standard deviation of 200 basis points or 2%, then a normal

distribution implies there is about a 67% probability that values will be found between one

standard deviation of either side of the mean. Thus, for a standard deviation of 1, the range on

either side of the mean for portfolio active return is 1 standard deviation times 2% = 2%. The 2%

Likewise, for a standard deviation of three, the range on either side of the mean is 3 standard

deviation times 2% = 6%. With a portfolio mean active return of 7%, the corresponding range

The above values can all be found in the below table.

Number of Standard

Deviations

Range for Portfolio

Active Return

Corresponding Range

for Portfolio Return

Probability

1

2%

5%–9%

67%

2

4%

3%–11%

95%

3

6%

1%–13%

99%

12. At a meeting between a portfolio manager and a prospective client, the portfolio manager

stated that her firm’s bond investment strategy is a conservative one. The portfolio manager

told the prospective client that she constructs a portfolio with a forward-looking tracking

error that is typically between 250 and 300 basis points of a client-specified bond index.

Explain why you agree or disagree with the portfolio manager’s statement that the portfolio

strategy is a conservative one.

If the chosen benchmark is the desired norm, then greater deviation from the norm implies more

risk taking, i.e., less conservative than claimed by the portfolio manager. Regardless, it appears

the manager is pursuing an active strategy that involves risk taking. More details are given

below.

Second, the strategy is not passive. When a portfolio is constructed to have a forward-looking

tracking error of zero, the manager has effectively designed the portfolio to replicate the

performance of the benchmark. If the forward-looking tracking error is maintained for the entire

13. What is meant by tracking error due to systematic risk factors?

By tracking error due to systematic risk factors, we mean tracking error caused by factors that

affect the return of securities in the benchmark in varying degrees. More details are given below.

Forward-looking tracking error indicates the degree of active portfolio management being

pursued by a manager. Therefore, it is necessary to understand what factors (including

systematic risk factors) affect the performance of a manager’s benchmark index. The degree to

which the manager constructs a portfolio that has exposure to the risk factors that is different

from the risk factors that affect the benchmark determines the forward-looking tracking error.

14. You are reviewing a report by a portfolio manager that indicates that a fund’s predicted

(forward-looking) tracking error is 94.87 basis points. Furthermore, it is reported that the

predicted tracking error due to systematic risk is 90 basis points and the predicted tracking

error due to non-systematic risk is 30 basis points. Why doesn’t the sum of these two

tracking error components total up to 94.87 basis points?

The predicted tracking error is 94.87 basis points. The two major risk categories are systematic

and non-systematic risks. For our portfolio, they are respectively 90 basis points and 30 basis

points. Now this might seem confusing since adding these two risks we do not get to the

predicted tracking error of 94.87 basis points for the portfolio. The reason is that these risk

15. What are the drawbacks of the cell-based approach for bond portfolio construction?

Let us first describe the cell-based approach. Under the cell-based approach, the benchmark is

divided into cells, each cell representing a different characteristic of the benchmark. The most

common cells used to break down a benchmark are (1) duration, (2) coupon, (3) maturity,

(4) market sectors, (5) credit quality, (6) call factors, and (7) sinking fund features.

The number of cells that the indexer uses will depend on the dollar amount of the portfolio. In

a portfolio of less than $100 million, for example, using a large number of cells entails

a problem. The “drawback” faced by the manager is it would require purchasing odd lots of

issues. This increases the cost of buying the issues to represent a cell and thus would increase the

16. Why is it difficult to build a portfolio in pursuing a pure bond indexing strategy?

While it is not simple to build a portfolio for enhanced indexing strategies, it is even more

difficult to implement a pure bond indexing strategy. These grave difficulties apply to both the

cell-based and multi-factor model approaches to portfolio construction. Below we attempt to

describe why.

In a pure bond indexing strategy, the portfolio manager must purchase all of the issues in the

bond index according to their weight in the benchmark index. However, substantial tracking

error will result from the transaction costs (and other fees) associated with purchasing all the

issues and reinvesting cash flow (maturing principal and coupon interest). A broad-based market

forced to follow an enhanced bond indexing strategy with minor mismatches in the primary risk

factors.

A portfolio manager faces several other logistical problems in seeking to construct an indexed

portfolio. First, the prices for each issue used by the organization that publishes the index may

not be execution prices available to the indexer. In fact, they may be materially different from the

prices offered by some dealers. In addition, the prices used by organizations reporting the value

of indexes are based on bid prices. Dealer ask prices, however, are the ones that the manager

17. How can a multi-factor risk model be used to monitor and control portfolio risk?

A multi-factor risk model can be used to monitor and control portfolio risk through

a forward-looking estimate of tracking error. The portfolio manager needs this forward-looking

estimate of tracking error to reflect the portfolio risk going forward. The way this is done in

practice is by using the services of a commercial vendor or dealer firm that has modeled the

factors that affect the tracking error associated with the bond market index (i.e., the portfolio

From the properties of a normal distribution, we know the following:

Number of Standard

Deviations

Range for Portfolio

Active Return

Corresponding Range for

Portfolio Return

Probability

1

–1%

9%–11%

67%

2

–2%

8%–12%

95%

3

–3%

7%–13%

99%

The forward-looking tracking error is useful in risk control and portfolio construction. The

manager can immediately see the likely effect on tracking error of any intended change in the

portfolio. Thus, scenario analysis can be performed by a portfolio manager to assess proposed

portfolio strategies and eliminate those that would result in tracking error beyond a specified

tolerance for risk.

18. How can a multi-factor risk model be used to rebalance a portfolio?

While it is common to illustrate portfolio construction starting with a position of cash and

building a portfolio of securities, in practice the more common task is to rebalance an existing

portfolio. A multi-factor model along with an optimizer can be used to efficiently rebalance the

portfolio. This rebalancing using a multi-factor model involves realigning the portfolio that has

optimizer can identify a package of transactions (i.e., sells and buys) and identify the reduction

(or increase) in risk that would result from the execution of those transactions so that the

portfolio manager can assess the risk adjustment benefit relative to the cost of executing the

transaction.

Exhibit 23-14Trades for Portfolio Rebalancing

Buys

Identifier

Description

Position Amount

Market Value

912828LK

US TREASURY NOTES

3,133,909

3,235,179

912828LS

US TREASURY NOTES

2,814,967

2,924,353

489170AB

KENNAMETAL INC

1,959,720

2,087,886

94986EAA

WELLS FARGO CAPITAL XIII

1,286,097

1,360,888

912810QD

US TREASURY BONDS

1,118,189

1,111,380

465138ZR

ISRAEL STATE OF

920,297

1,097,735

912810QB

US TREASURY BONDS

1,017,169

991,185

GNG03410

GNMA II Single Family 15yr

117,277

119,672

Total

12,928,278

Sells

Identifier

Description

Position Amount

Market Value

912828NV

US TREASURY NOTES

–2,662,260

–2,586,183

16132NAV

CHARTER ONE BANK FSB

–2,203,358

–2,332,312

05946NAD

BANCO BRADESCO SA

–1,564,870

–1,828,328

827065AA

SILICON VALLEY BANK

–1,692,776

–1,770,613

912828NL

US TREASURY NOTES

–1,603,631

–1,612,239

912810QC

US TREASURY BONDS

–1,462,336

–1,468,727

912810QE

US TREASURY BONDS

–1,298,352

–1,329,875

Total

–12,928,278

19. In a factor model, what is meant by isolated tracking error?

An isolated tracking error refers to the method of calculating the partial tracking error due to

a single group of risk factors in isolation; no other forms of risk are considered. Illustrations

giving more details are given below.

Let us first illustrate an isolated tracking error by considering the risk factor “securitized spread”

in Exhibit 23-7. This risk factor is the exposure to changes in the spreads in the agency MBS

market. The value of 2.5 means that if the portfolio only differs from the benchmark with respect

to its exposure to changes in the spread in the agency MBS sector, then this mismatch relative to

the benchmark would result in a monthly isolated tracking error of 2.5 basis points.

Portfolio isolated systematic TE = [(TE1)2 + (TE2)2 + … + (TEK)2]1/2

where TE denotes tracking error and the subscript denotes the risk factor.

Consider the 50-security portfolio in Exhibit 23-13 where the monthly isolated TE for each risk

factor is shown in Exhibit 23-7. Here the portfolio isolated systematic TE is 6.24 basis points per

month as shown below:

©2013 Pearson Education

526

Portfolio TE = [(TEF1)2 + (TEF2)2 + 2 Cov(F1,F2)]1/2

where Cov(F1,F2) is the covariance between risk factor exposures 1 and 2.

20. Following is a portfolio consisting of 50 bonds with a market value of $100 million as of

April 29, 2011:

Identifier

Description

Position

Market Value

003723AA

ABN AMRO BANK NV

1,449,636

1,422,596

00104BAC

AES EASTERN ENERGY

1,682,044

1,206,446

02051PAC

ALON REFINING KROTZ

592,304

630,655

02360XAL

AMERENENERGY GENERATING

707,484

737,343

101137AD

BOSTON SCIENTIFC

1,551,232

1,656,030

12527GAA

CF INDUSTRIES INC

1,328,707

1,499,778

165167BS

CHESAPEAKE ENERGY CORP

797,314

880,013

125896BG

CMS ENERGY

1,286,476

1,337,697

251591AY

DEVELOPERS DIVERS REALTY

646,714

644,344

FGB08000

FHLM Gold Guar Single F. 30yr

2,683,702

3,040,911

FGB07001

FHLM Gold Guar Single F. 30yr

690,235

780,262

FGB06402

FHLM Gold Guar Single F. 30yr

885,600

1,004,579

FGB07002

FHLM Gold Guar Single F. 30yr

3,751,831

4,235,068

FGB05403

FHLM Gold Guar Single F. 30yr

1,411,009

1,531,707

FGB06003

FHLM Gold Guar Single F. 30yr

1,387,727

1,537,027

FGB06004

FHLM Gold Guar Single F. 30yr

633,691

700,545

FGB05011

FHLM Gold Guar Single F. 30yr

651,568

690,585

FNA07098

FNMA Conventional Long T. 30yr

884,357

1,014,899

FNA08000

FNMA Conventional Long T. 30yr

1,643,844

1,883,297

FNA05402

FNMA Conventional Long T. 30yr

1,707,042

1,854,853

FNA06402

FNMA Conventional Long T. 30yr

1,155,221

1,311,433

FNA07002

FNMA Conventional Long T. 30yr

2,241,336

2,563,939

FNA05003

FNMA Conventional Long T. 30yr

641,485

684,085

FNA05403

FNMA Conventional Long T. 30yr

3,194,556

3,469,103

FNA06003

FNMA Conventional Long T. 30yr

1,548,573

1,715,870

FNA05010

FNMA Conventional Long T. 30yr

794,384

843,855

FNA05011

FNMA Conventional Long T. 30yr

1,105,717

1,173,465

GNB04411

GNMA II Single Family 30yr

2,391,899

2,509,580

381427AA

GOLDMAN SACHS CAPITAL II

3,123,435

2,761,546

45905CAA

INTERNATL BANK RECON DEV-GLOBA

1,151,247

1,200,080

45950KBJ

INTL FINANCE CORPORATION

1,227,607

1,198,808

46513E5Y

ISRAEL STATE OF-GLOBAL

1,797,220

1,911,761

500769BR

KREDIT FUER WIEDERAUFBAU-GLOBA

3,461,061

1,012,672

500769CH

KREDIT FUER WIEDERAUFBAU-GLOBA

3,430,115

941,429

582834AM

MEAD CORP

727,352

787,191

58551TAA

MELLON CAPITAL IV

3,326,734

3,102,915

651715AF

NEWPAGE CORP

6,414,006

1,603,501

665772CE

NORTHERN STATES PWR MINN

889,932

907,113

723787AG

PIONEER NATURAL RESOURCES

945,542

1,045,275

749685AQ

RPM INTERNATIONAL INC

591,159

642,823

797440BM

SAN DIEGO GAS & ELECTRIC

957,058

856,840

784635AM

SPX CORPORATION

708,877

766,621

91311QAD

UNITED UTILITES PLC

844,170

848,272

915436AF

UPM-KYMMENE CORP

655,540

648,265

912810PW

US TREASURY BONDS

797,859

804,588

912810QA

US TREASURY BONDS

8,725,929

7,505,533

912810QK

US TREASURY BONDS

4,408,259

4,048,097

912828PA

US TREASURY NOTES

3,507,446

3,378,751

912828PF

US TREASURY NOTES

21,453,185

20,596,365

962166AV

WEYERHAEUSER CO

750,667

871,588

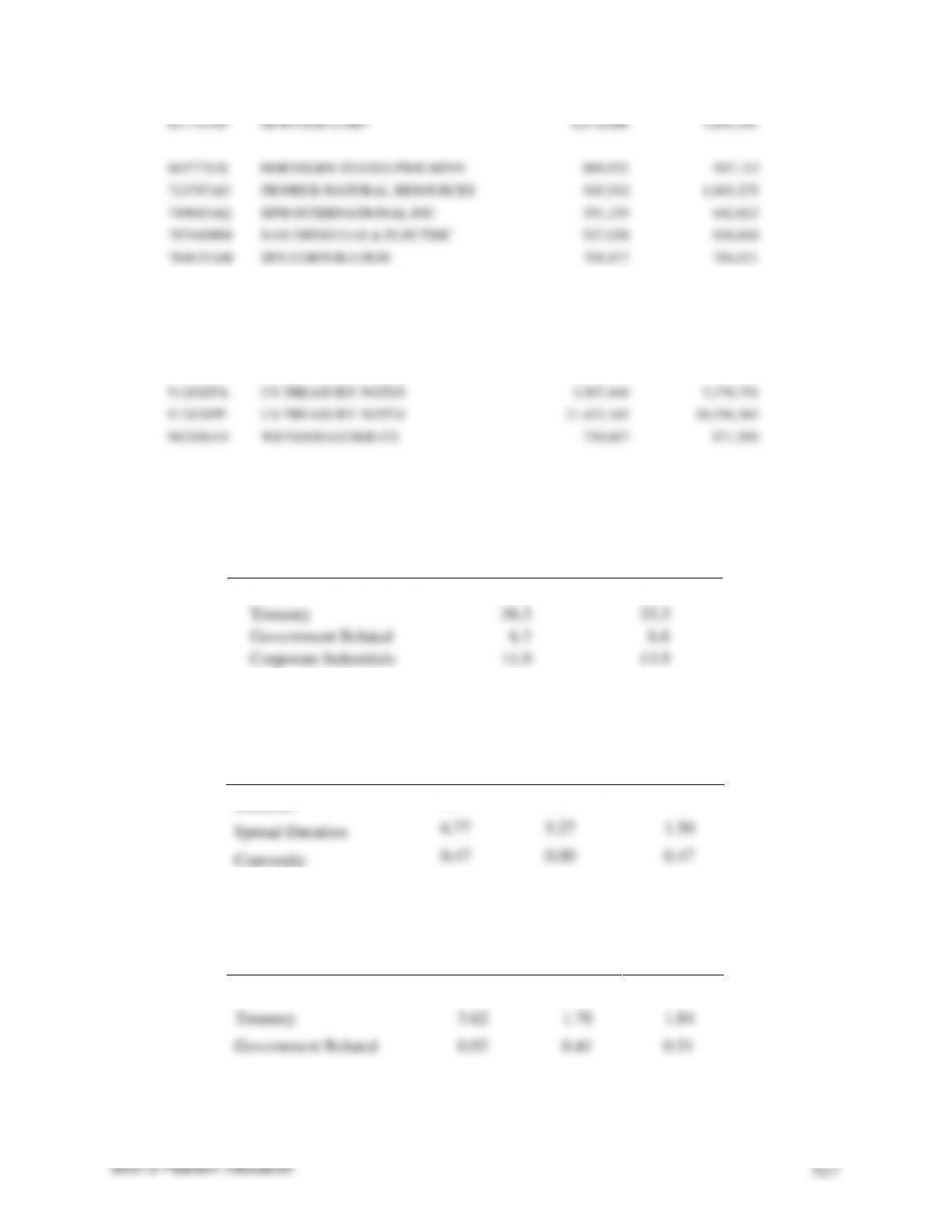

The benchmark for the manager who has constructed this portfolio is a composite index

consisting one-third each of the Barclays Capital U.S. Treasury index, Barclays Capital U.S.

Credit Index, and Barclays Capital U.S. MBS index.

Asset Class

Portfolio

Benchmark

Total

100.0

100.0

Treasury

36.3

33.3

Government Related

6.3

6.8

Corporate Industrials

11.0

13.9

Corporate Utilities

5.9

2.9

Corporate Financials

7.9

9.7

MBS Agency

32.6

33.3

Analytics

Portfolio

Benchmark

Difference

Duration

6.87

5.37

1.50

Spread Duration

6.77

5.27

1.50

Convexity

0.47

0.00

0.47

Vega

0.01

0.03

0.02

Spread

355

55

300.00

Duration Contribution

Portfolio

Benchmark

Difference

Total

6.87

5.37

1.50

Treasury

3.62

1.78

1.84

Government Related

0.92

0.41

0.51

Corporate

1.10

1.74

–0.63

Securitized

1.23

1.45

–0.22

Risk Factor Categories

Risk

Curve

40.8

Swap Spreads

2.5

Volatility

2.8

Spread Government Related

5.3

Spread Corporate

30.6

Spread Securitized

5.8

Volatility

Portfolio

Benchmark

Tracking Error

Systematic

141.9

117.4

37.9

Idiosyncratic

19.3

4.8

18.7

Total

143.2

117.5

42.3

Portfolio Beta

1.18

Risk Factor Group

Isolated TEV

Contribution to

TEV

Liquidation

Effect on TEV

TEV Elasticity

(%)

Total

42.3

42.3

–42.3

1.0

Systematic Risk

37.9

33.2

–22.4

0.8

Curve

40.8

23.4

–4.3

0.5

Swap Spreads

2.5

0.2

–0.1

0.0

Volatility

2.8

0.5

–0.4

0.0

Spread Government Related

5.3

0.0

0.3

0.0

Spread Corporate

30.6

10.0

0.8

0.2

Spread Securitized

5.8

–0.8

1.1

0.0

Idiosyncratic Risk

18.7

9.1

–4.2

0.2

Describe in detail the risk characteristics of this portfolio. Be sure to discuss where it seems

like the manager is taking views on the market?

The benchmark for the manager who has constructed this portfolio is a composite index

consisting of one-third each of the Barclays Capital U.S. Treasury index, Barclays Capital U.S.

Credit Index, and Barclays Capital U.S. MBS index. First, in regards to the Barclays Capital

U.S. Treasury index, this index measures the performance of U.S. Treasury securities. Second, in

regards to the Barclays Capital U.S. MBS index, this index measures the performance of

investment grade fixed-rate mortgage-backed pass-through securities of GNMA, FNMA, and

FHLMC.

The analysis of the portfolio begins with a comparison of the portfolio to that of the benchmark.

Identification of the mismatches indicates where the manager has taken a view (unintentional or

not). The “asset class” table compares the portfolio and the benchmark in terms of the allocation

Although the information contained in the “asset” table (about the allocation based on percentage

market value of sector relative to the benchmark) provides a good starting point for our analysis,

the information has limited value because it is not known how the exposures to the sectors are

related to the exposures to the risk factors that drive the portfolio’s return. Here are three

examples. First, consider the Treasury sector. It is possible that the specific Treasury securities

contained in the portfolio have a lesser contribution to portfolio duration than the contribution to

It is for this reason that the portfolio manager must look beyond a naïve assessment of portfolio

risk relative to the benchmark based on percentage allocation to sectors. The “analytics” table

provides information about the relative exposure to interest rate risk as measured by duration,

spread risk as measured by spread duration, and call/prepayment risk as measured by vega, as

well as the convexity. From these analytics we observe the following:

The analysis thus far is missing a vital element. To understand why, suppose that a portfolio has

more exposure to a risk factor than the benchmark. This would mean if that risk factor moves,

the portfolio will have a greater movement than the benchmark. But the question is: To what

extent does that risk factor move? Another way of asking this is: How volatile is the risk factor?

For example, from the analysis of the analytics, we know that the portfolio has greater exposure

than the benchmark to changes in the level of interest rates (i.e., a higher duration) but less

exposure to changes in spreads (i.e., a higher spread duration). But which exposure (i.e., risk

factor) has greater volatility?

143.2 and 117.5, respectively.

Notice that for the benchmark, the percentage of the total risk (117.5) that is explained by the

18.7 basis points per month, respectively. The portfolio tracking error is

Portfolio tracking error = [(Systematic TE)2 + (Idiosyncratic TE)2]0.5

Therefore, the portfolio tracking error is 42.3 basis points per month. Consequently, although

©2013 Pearson Education

531

to a benchmark, there is tracking error risk of 42.3 basis points per month. (The systematic risk is

responsible for 18.7/42.3 or 44.21% of the total risk.)

This is an extremely important point: It is the tracking error not the idiosyncratic risk (as

measured by the standard deviation of the idiosyncratic returns) that the manager must consider

in portfolio construction and monitoring. In our illustration, the portfolio tracking error is small,

only 42.3 basis points.

As with equities where a portfolio beta is computed that shows the movement of an equity

portfolio in response to a movement in some equity market index (such as the S&P 500), a beta

can be computed for a bond portfolio. As shown in “volatility” table, the portfolio beta is 1.18.

(1) categories of risk factors and (2) asset classes (i.e., sectors of the benchmark).

This “risk factor group” table provides information about the portfolio risk across the different

categories of risk factors. Shown are the systematic risk and the idiosyncratic risk and six

components of systematic risk. The “contribution to TEV” column shows the isolated tracking