Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 21 - Taxes, Inflation, and Investment Strategy

CHAPTER TWENTY ONE

TAXES, INFLATION, AND INVESTMENT STRATEGY

CHAPTER OVERVIEW

This chapter presents material on developing a framework for retirement planning. The chapter

is built around a set of Excel models that can be used to plan for retirement. The first model

ignores inflation and taxes and subsequent models add the effects of inflation, a flat tax rate and

a progressive tax rate. This method allows students to see the effects on the retirement portfolio

LEARNING OBJECTIVES

After studying this chapter the student should have an understanding of the basic elements

required to build a financial plan and how taxes and inflation will affect retirement income.

Students should be able to describe the basic types of tax sheltered retirement accounts and how

CHAPTER OUTLINE

**Topics 1 through 6 of this chapter are written around a series of spreadsheets so the

Instructor’s Manual follows the same format. I have labeled each spreadsheet and

discussed the inputs and outputs beneath the appropriate spreadsheet.

1. Saving for the Long Run

PPT 21-2 through PPT 21-3

The development of the basic retirement plan involves identification of the time until retirement,

the allocation of the percentage allocation to saving, the life expectancy following retirement and

the expected rate of return. These key factors become the base of the plan. The first step in the

Chapter 21 - Taxes, Inflation, and Investment Strategy

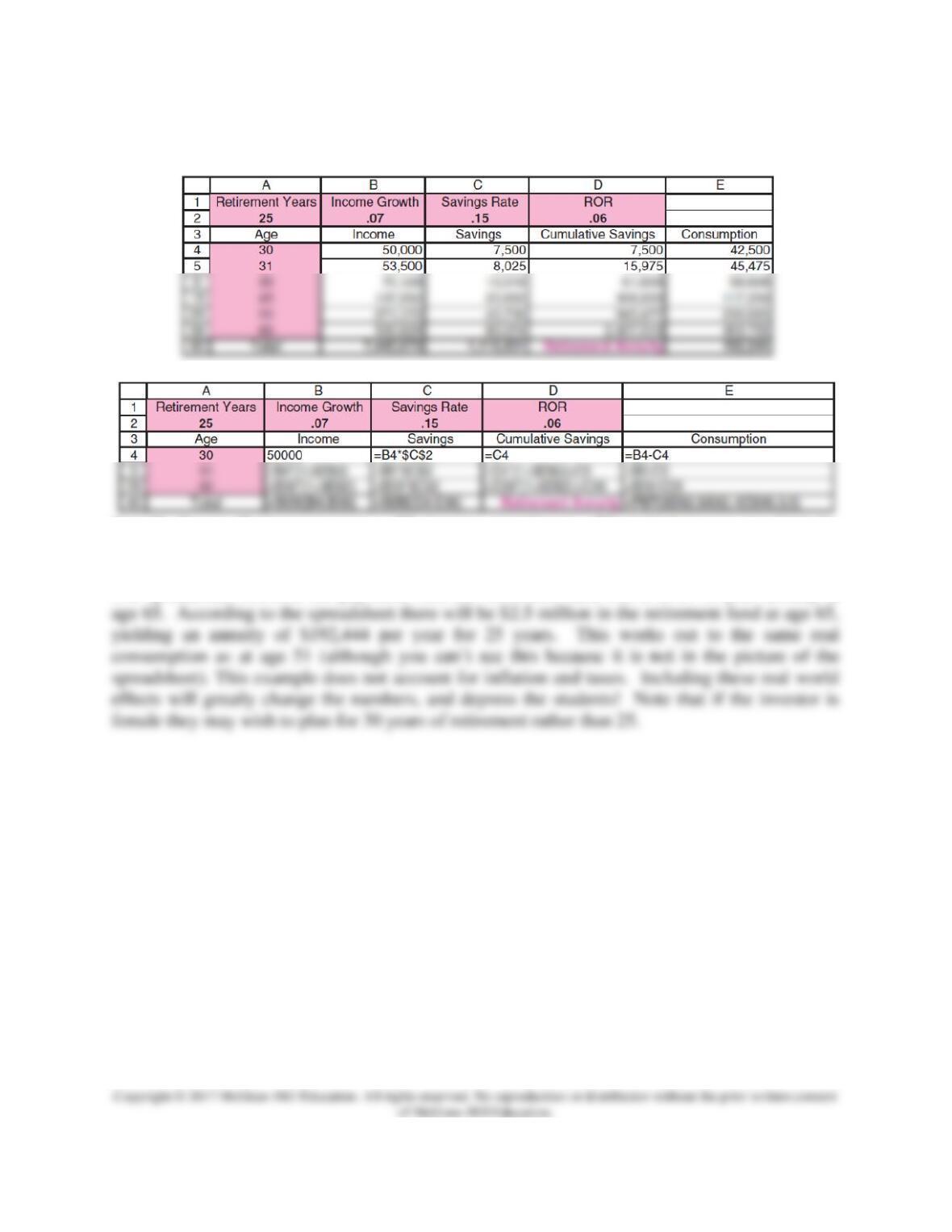

Spreadsheet 21.1: The Savings Plan

Specific Inputs: Retirement years = 25, income growth rate =7% (which is way too high for

many people); income at age 30 = $50,000, the rate of savings (% of income) which is very high

at 15%, and the rate or return on investment (ror) which is low at 6% for a retirement portfolio.

The spreadsheet converts the payments into the retirement fund into a level 25 year annuity at

2. Accounting for Inflation

Chapter 21 - Taxes, Inflation, and Investment Strategy

PPT 21-4 through PPT 21-9

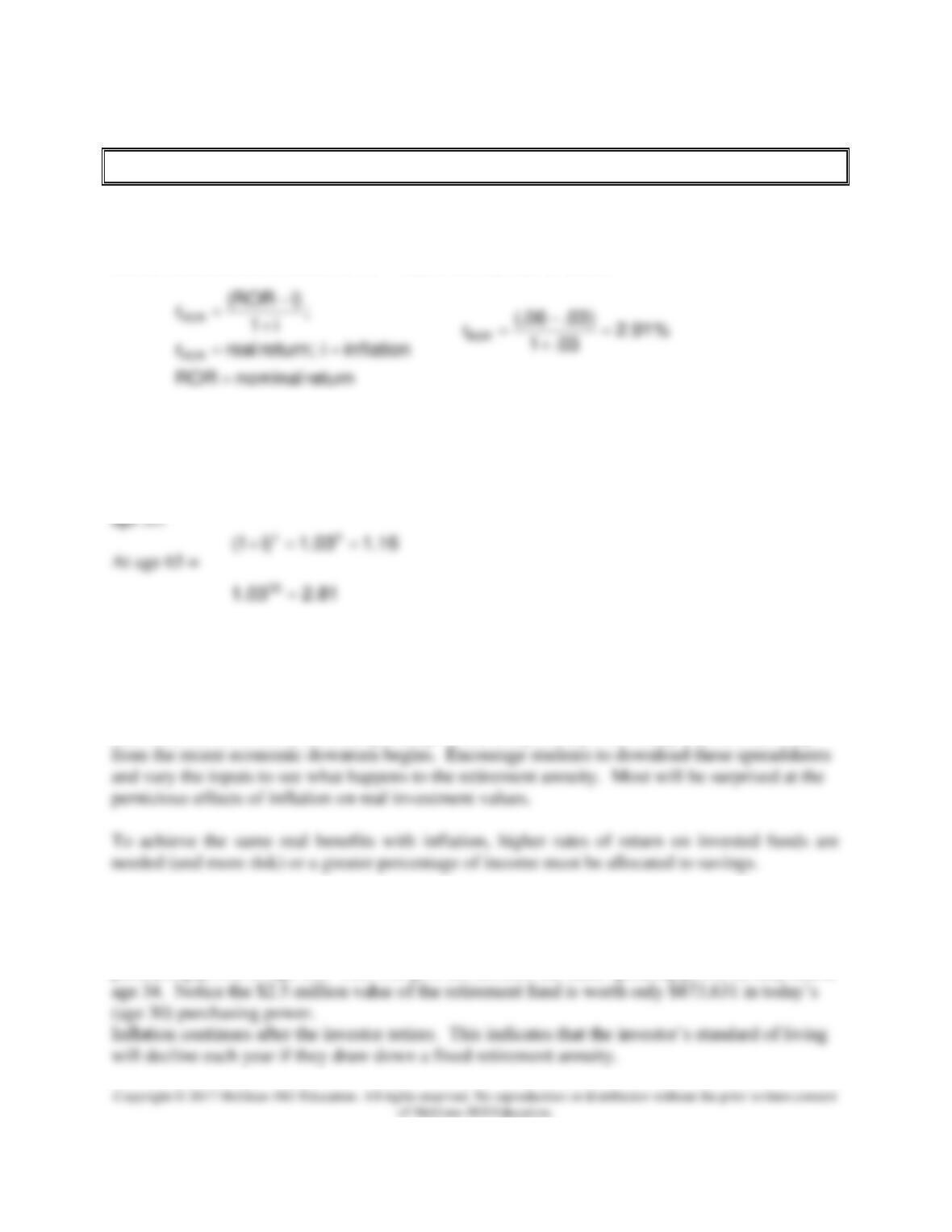

Inflation reduces the purchasing power of the savings accumulation. Real and nominal

consumption can be related as follows: Real consumption = Nominal consumption / Price

Deflator. A simple example can be used to illustrate the point. Suppose inflation = 3% per year

and the nominal rate of return is 6%. What is the real rate of return?

Inflation turns the 6% nominal return into a 2.91% real return. This is before taxes are

considered. Since taxes are paid out of nominal earnings, the combine effect of inflation and

taxes results in even greater reductions than may be expected in real after tax rates of return.

The investor in the example is 30 years old. The size of the price deflator with 3% inflation at

Both of these numbers are in the spreadsheet. These deflators are used to convert the nominal

purchasing power in year t to starting date (age 30) dollars.

Historically inflation has been much higher than in recent time periods. From the 1990s on the

Federal Reserve has managed the money supply to limit inflation. Nevertheless much higher

rates than the 3% used in the example are possible and probably even likely after the recovery

Spreadsheet 21.2 A Real Retirement Plan

The inputs are the same as before with inflation of 3% added. rConsumption is real consumption.

Thus the $192,244 nominal annuity buys only $49,668 in real purchasing power (the same

purchasing power as age 30). This will give the investor the same spending power as they had at

Chapter 21 - Taxes, Inflation, and Investment Strategy

Should an investor take on more risk to offset inflation? What are the effects of increasing the

riskiness of the retirement portfolio? Increasing the risk increases the expected return, but also

the probability of not having enough to live on when the investor retires. As one gets older,

increasing the risk to make up for years in which one did not save is really rolling the dice. Nor

is it is not easy to reduce the risk level as you retire. It is particularly difficult if one has some

Real returns based on historical averages

Investment

Average Real

Return

Because we have had a long period of low inflation people forget how regressive the effects of

inflation really are. It erodes investment returns and drives up the cost of necessities which

reduces the standard of living of low income individuals, the group that can least afford it.

3. Accounting for Taxes

PPT 21-10 through PPT 21-11

Chapter 21 - Taxes, Inflation, and Investment Strategy

Spreadsheet 21.4, Saving With a Simple Tax Code

The effects of inflation and taxes together really have major impacts on the ability to meet

investment goals. In this case the real retirement annuity is $37,882 with very modest inflation

of 3%, saving a lot of their income, 15% and a tax rate of 25%. Note that the tax rate should

(roughly) be the sum of federal, state and local income taxes.

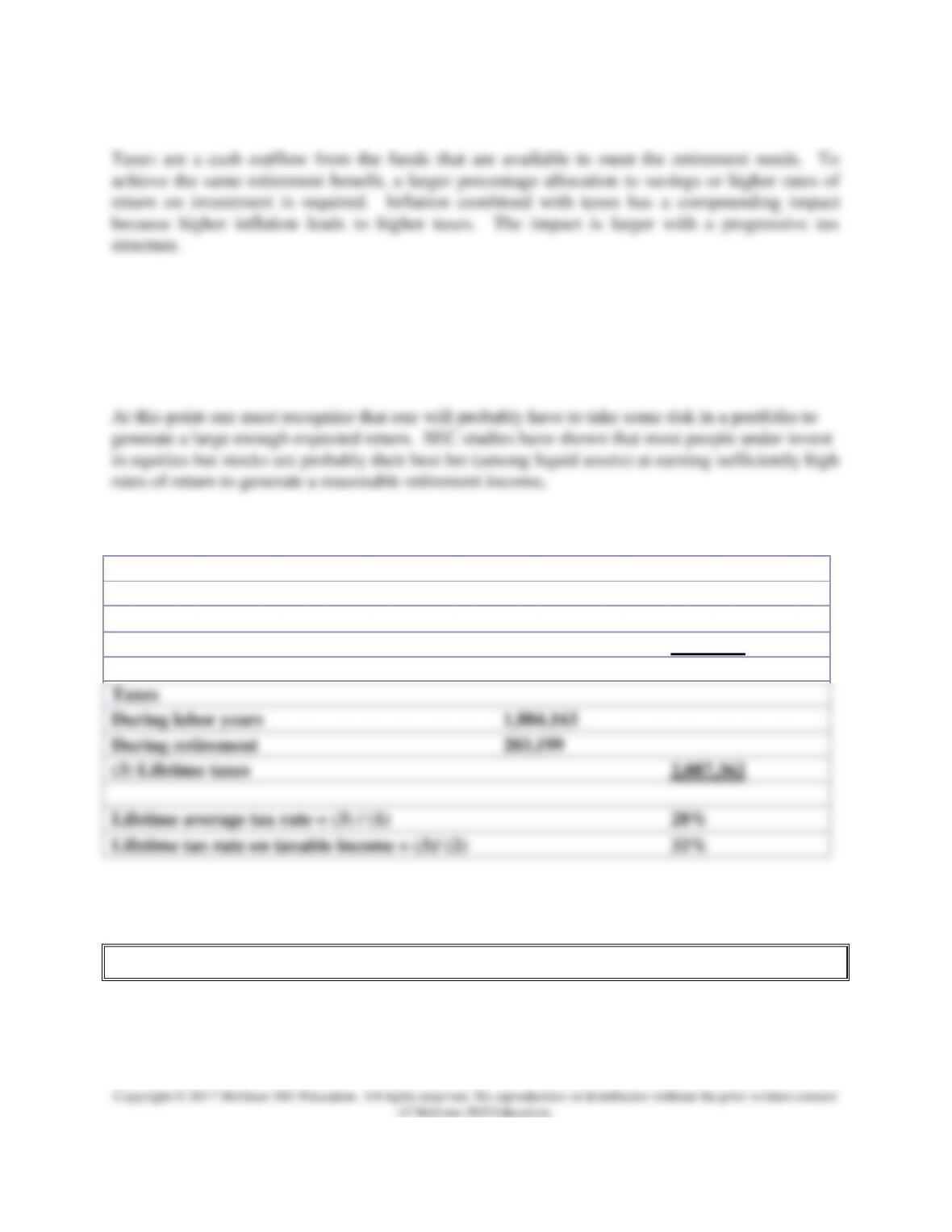

Investors pay income taxes and pay taxes on unsheltered savings. One can use the numbers in

Spreadsheet 21.4 to illustrate the effect on the overall tax rate:

Income

(1) Lifetime labor income

$7,445,673

Total exemptions during working years

$949,139

(2) Lifetime Taxable labor income

6,496,534

As a result the average tax rate is elevated above the marginal tax rate of 25%.

4. The Economics of Tax Shelters

PPT 21-12 through PPT 21-15

Chapter 21 - Taxes, Inflation, and Investment Strategy

Tax shelters are means of postponing taxes as long as possible. One can’t get rid of taxes, one

Spreadsheet 21.5 Savings with a Flat Tax and IRA Style Tax Shelter

This spreadsheet redoes sheet 21.4 with the tax shelter. It still uses a flat tax rate. All funds in

Spreadsheet 21.6 Savings with a Progressive Tax Rate

We have seen that taxes on income during the working years reduce the future value of the

investments dramatically. A progressive tax code magnifies this effect because retirement tax

Spreadsheet 21.7, IRA with a Progressive Tax Code

The real annuity is increased considerably in this case; it is now up to $83,380. This is better than

with a flat tax rate for the reasons noted above.

5. A Menu of Tax Shelters

PPT 21-16 through PPT 21-24

Individual Retirement Accounts (IRAs) were created by the Tax Reform Act of 1986. Current

rules allow investors to contribute up to $5,000 per year to a retirement account. Individuals age

50 and older may contribute another $1,000 per year. There is a 10% tax penalty for withdrawal

Chapter 21 - Taxes, Inflation, and Investment Strategy

Spreadsheet 21.8 Roth IRA with Progressive Tax Code

The effectiveness of the Roth IRA as a tax shelter is independent of tax rates during retirement.

Table 21.2 Traditional vs. Roth IRA Tax Shelters under a Progressive Tax Code

This table summarizes the differences between traditional and Roth IRAs. Note that although

the Roth IRA results in less taxes paid over the lifetime and a lower average tax rate, the

traditional IRA offers a substantially higher retirement annuity. The higher tax rates on the

With defined benefit (DB) plans the employer promises to pay a defined or known benefit to

employees when they retire. The benefit is typically a percentage of salary based on years of

service. The employer must fund the pension obligation by setting aside a certain amount of

funds in a pension trust. Many of these funds are managed by life insurance firms (listed under

separate account business). A fully funded pension plan is one where the firm has set aside the

full present value of expected future payments. Many plans are only partially funded. The

Table 21.3 Investing Roth IRA Contributions into Stock and Bonds

Some investors make the mistake of putting stocks in their IRA and buy bonds outside their IRA.

6. Social Security

PPT 21-24 through PPT 21-28

Social Security (SS) is a federal pension plan established to provide minimum retirement

benefits to all workers. Technically it is the Old Age and Survivors Disability Fund. It is

unfunded although it is in surplus on a current year basis, but it is projected to go in the red

around 2016.

U.S. citizens pay 6.2% of their income to SS, plus 1.45% toward Medicare and their employer

matches their contribution.

1

SS is a means of redistributing income. In dollar terms taxes are

regressive, rising with income but low income workers receive a relatively larger share of

preretirement income upon retirement than higher income workers.

There are four steps required to calculate an individual’s benefits:

1. The series of the taxed annual earnings is compiled

3. Average Indexed Monthly Earnings (AIME)

The 35 highest annual indexed contributions are summed and then divided by (35 x 12) =

4. Primary Insurance Amount (PIA): The PIA is the amount the individual receives each

year. No exact formula is provided for this calculation. The income replacement rate is

the percentage of the working income received in retirement. The income replacement

1

Actually you would pay the 7.65% taxes on the first $106,800 of your income in 2009. On your paycheck this will be in the

FICA section. Note that between the employee and the employer 12.4% is being paid in to fund SS.

7. Additional Considerations

PPT 21-30 through PPT 21-32

The text identifies and very briefly describes how specific considerations such as funding a

child’s college education, should be built into the financial plan. Financing a child’s education

involves the same procedure as funding retirement. One gains no equity in renting, and equity is

a safeguard for tough times. Too many people try to buy too much house and this can limit their

ability to save as well as stress their relationships. Houses are illiquid investments whose value

does not always increase.

Excel Applications

The best method to cover the material in this chapter involves the integrated use of the models

that are available on the web. The impact that each of the factors has on performance can be