Chapter 20 – Hedge Funds

CHAPTER TWENTY

HEDGE FUNDS

CHAPTER OVERVIEW

While mutual funds are still the dominant type of investment fund, hedge funds enjoyed much

faster growth until the financial crisis of 2008. In 1997 assets under management were about

$200 billion; this number peaked at about $2 trillion before the downturn in 2008 reduced the

number to $1.6 trillion. Hedge funds are organized as private partnerships and are not subject to

SEC disclosure requirements. Hence many people have only a limited understanding of what

LEARNING OBJECTIVES

After studying this chapter students should be able to differentiate between directional and non–

directional strategies and state several of each. Students should understand a pure play strategy

such as alpha capture while hedging out fundamental risk. Readers should have knowledge

CHAPTER OUTLINE

1. Hedge Funds versus Mutual Funds

PPT 20-2

Mutual funds are regulated under the SEC Act 1933 and the Investment Company Act of 1940

and they must invest according to the stated goals in the prospectus. They are adjured to avoid

‘style drift.’

Hedge funds are not open to the general public. The primary investors are institutional investors

Chapter 20 – Hedge Funds

Characteristic

Mutual Funds

Hedge Funds

Transparency

Public info on portfolio

composition

Info provided only to

investors

Investors

Unlimited

< 100, high dollar

minimums

Liquidity

Redeem shares on demand

Multiple year lock up

periods typical

Notes to the table:

Some mutual funds can engage in short selling, but not to the extent that hedge funds can. The

2. Hedge Fund Strategies

PPT 20-3 through PPT 20-6

Chapter 20 – Hedge Funds

Text Table 20.1 provides a comprehensive list of hedge fund strategies. Hedge funds employ

both directional strategies and non-directional strategies. A directional strategy is a position that

benefits if one sector of the market outperforms another, an unhedged bet on a price movement.

convergence arbitrage and was commonly used by the hedge fund Long Term Capital

Management (LTCM). When global risk premiums increased after the Asian currency crisis and

the Russian foreign debt default, spreads increased beyond their historical norms for an extended

time period. Because LTCM was so highly levered, they could not ride out the crisis and

eventually had to be bailed out by their Wall Street clients. The bailout was arranged by the Fed

3. Portable Alpha

PPT 20-7 through PPT 20-12

Chapter 20 – Hedge Funds

Suppose a fund finds a positive alpha stock but the fund expects the overall market to fall. This

is called fundamental risk. The solution is to buy the stock and sell stock index futures to drive

the effective stock beta to zero. By doing so the fund would engage in a ‘market neutral’ pure

play. When this strategy is combined with a passive investment in an index or sector this is

called alpha transfer, hence the term portable alpha. The following pure play example is also in

the text and can be used to illustrate alpha capture; however the example is somewhat technical

and relies on several topics not developed in this chapter. The example employs a stock hedge

ratio and uses spot futures parity that is covered in Chapter 17.

Step 1: Find the ending dollar value of the portfolio based on the given information.

The hedge ratio must do two things: First, it must adjust for the difference in size in the spot and

futures position. Obviously with a fixed contract size, a bigger spot position (the stock portfolio)

will require a greater number of contracts. Second, the ratio must adjust for relative price

fluctuations of the spot and futures. The portfolio beta is just such a relative price adjustment

measure.

Step 2: Find the profit from the short futures position used to hedge out market risk:

Chapter 20 – Hedge Funds

The example assumes the hedge termination date is the futures contract expiration date. That is

why we get convergence. The two terms with rM cancel out and we effectively have a zero beta

position.

Step 3: Verify that the return captures the alpha of 2% (plus the risk free return of 1%).

The expected value of e is zero but it could turn out to be negative and this could wipe out your

gains. Also, the analyst could be wrong about the alpha. The point is this strategy is not riskless.

Figure 20.1 provides a graphical illustration of the concept that can be used in conjunction with

or as a substitute to the numerical example.

4. Style Analysis for Hedge Funds

PPT 20-13

Many fund strategies are directional bets and may be evaluated with style analysis. Style

analysis is covered in Chapter 18 and you may suggest students review that material. Directional

investments will have nonzero betas, called “factor loadings.” Typical factors may include

5. Performance Measurement for Hedge Funds

PPT 20-14 through PPT 20-26

Hasanhodzic and Lo (2007) find that style adjusted alphas and Sharpe ratios are significantly

greater than these measures for the S&P500 for a large sample of hedge funds. Does this mean

that hedge funds are earning abnormal returns? The answer is maybe, but probably not. On the

Chapter 20 – Hedge Funds

Other Problems in Hedge Fund Performance Evaluation

Survivorship bias is a problem in performance measurement of risky hedge funds. Those that

don’t survive don’t report results that are used in estimating average performance. Hedge funds

report returns to publishers only if they choose to. This is another problem in regulation that is

referred to as backfill bias. This problem may be fixed shortly as the industry is coming under

pressure for greater disclosure and transparency.

6. Fee Structure in Hedge Funds

PPT 20-27 through PPT 20-28

Chapter 20 – Hedge Funds

Typical hedge fund fees includes a fixed management fee between 1% and 2% of assets plus an

incentive fee usually equal to 20% or more of investment profits above a benchmark

performance return. Incentive fees are analogous to call options on the portfolio with a strike

price equal to the current portfolio value x (1+ benchmark return). This is illustrated in Figure

20.7, Incentive Fees as a Call Option. This implies that the value of the incentive fee can be

modeled with option pricing as follows:

• Suppose a hedge fund’s returns have an annual =30%

• The annual incentive fee is 20% of the return over the risk free money market rate.

• The fund has a net asset value of $100 per share and the annual risk free rate is 5%.

Mutual funds as a group suffered large losses during the subprime fallout and the related

financial crisis. However according to the Economist Magazine in 2009, hedge fund customers

were largely satisfied with their hedge fund investments and planned on continuing to invest in

these funds IF fees were reduced. It is reasonable to expect lower fees in the future.

High Water Mark

Chapter 20 – Hedge Funds

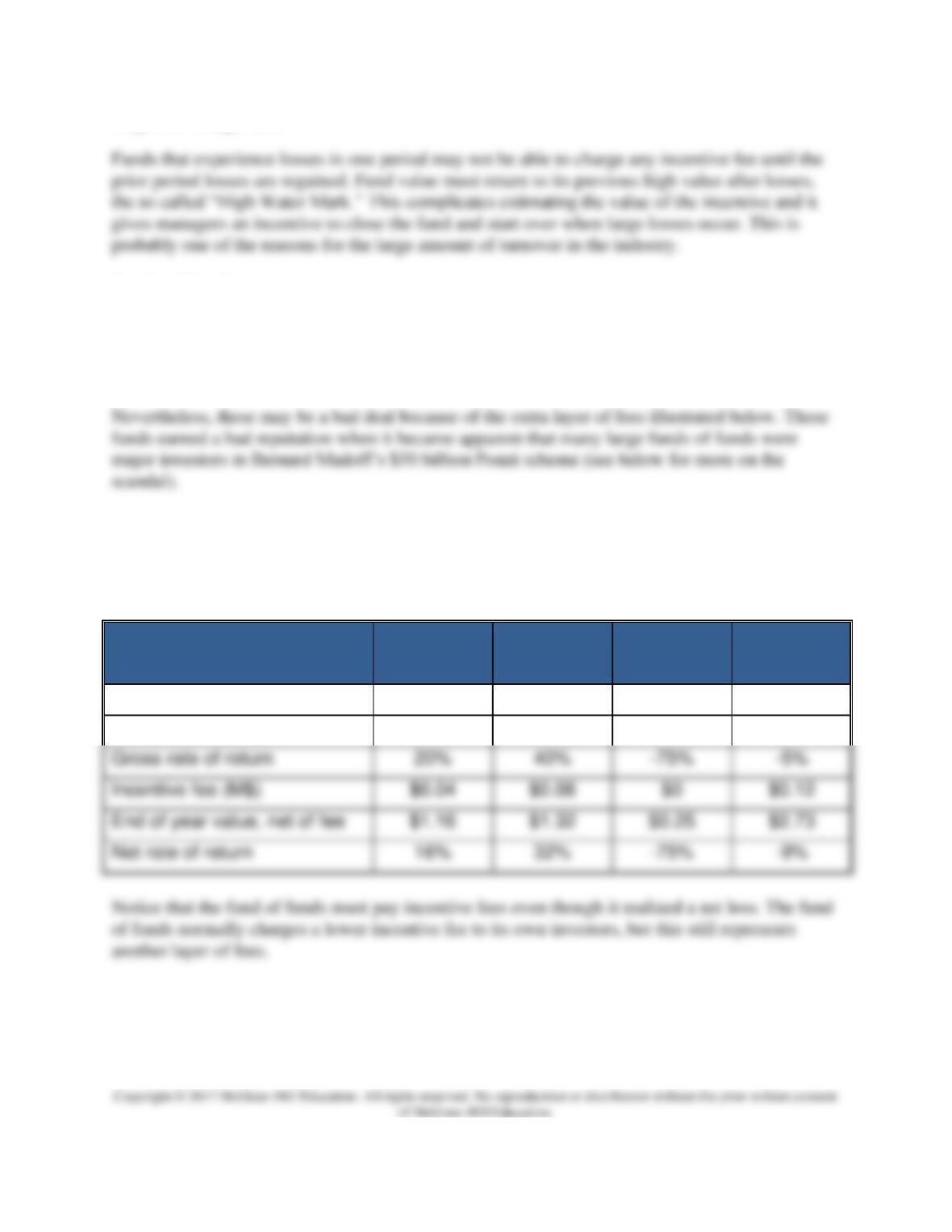

Funds of Funds

Funds of funds invest in one or more other hedge funds and serve as ‘feeder funds’ to the

ultimate hedge fund. This allows investors to easily diversify across hedge funds, as long as the

fund of funds diversifies by investing in funds that employ different strategies. By 2008 about

one half of assets invested in hedge funds were in funds of funds.

Suppose a fund of funds has $1 million invested in each of three hedge funds. For simplicity

assume the hurdle rate to earn incentive fees is a zero rate of return (no losses) and the normal

fixed asset management fee is zero. The following text table illustrates the effect of the fees on

this fund of funds:

FUND 1

FUND 2

FUND 3

FUND OF

FUNDS

Start of year (M$)

$1.00

$1.00

$1.00

$3.00

End of year (M$)

$1.20

$1.40

$0.25

$2.85

Gross rate of return

Incentive fee (M$)

$0.04

$0.08

$0.12

End of year value, net of fee

$1.16

$1.32

$0.25

$2.73

Net rate of return

The $50 Billion Madoff Scandal

Madoff. For instance, Fairfield Greenwich Advisors had exposure of $7.5 billion. Other funds

with exposure over $ 1 billion included Tremont Group Holdings, Banco Santander, Ascot

Partners and Access International Advisors. Their due diligence must have been poorly done.

In 2008 redemptions began as more clients needed money and the scheme unwound. The lack of

reporting requirements in this industry made the fraud possible but there were several warning

signs including:

• Returns were too stable for too long. His firm was Bernard L. Madoff Investment

Securities LLC and the firm reported earnings of between 10% and 12% in both good

markets and bad. Some institutional investors were leery of the Madoff fund because of

the fund’s opacity.