CHAPTER 2

PRICING OF BONDS

CHAPTER SUMMARY

This chapter will focus on the time value of money and how to calculate the price of a bond.

When pricing a bond it is necessary to estimate the expected cash flows and determine the

appropriate yield at which to discount the expected cash flows. Among other aspects of a bond,

we will look at the reasons why the price of a bond changes

REVIEW OF TIME VALUE OF MONEY

Money has time value because of the opportunity to invest it at some interest rate.

Future Value

The future value of any sum of money invested today is:

Pn= P0(1+r)n

wheren = number of periods, Pn= future value n periods from now (in dollars), P0= original

principal (in dollars), r = interest rate per period (in decimal form), and the expression

(1+r)nrepresents the future value of $1 invested today for n periods at a compounding rate of r.

Future Value of an Ordinary Annuity

When the same amount of money is invested periodically, it is referred to as an annuity. When

the first investment occurs one period from now, it is referred to as an ordinary annuity.

The equation for the future value of an ordinary annuity is:

whereA is the amount of the annuity (in dollars).

Example of Future Value of an Ordinary Annuity Using Annual Interest:

( )

11

n

r

+−

08.0

Because 15($2,000,000) = $30,000,000 of this future value represents the total dollar amount of

annual interest payments made by the issuer and invested by the portfolio manager, the balance

Example of Future Value of an Ordinary Annuity Using Semiannual Interest:

Consider the same example, but now we assume semiannual interest payments.

If A = $2,000,000 / 2 = $1,000,000, r = 0.08 / 2 = 0.04, n = 2(15) = 30, then

( )

11

n

r

+−

1

)

04. (1

−

1 2434.3

−

The opportunity for more frequent reinvestment of interest payments received makes the interest

Present Value

The present value is the future value process in reverse. We have:

( )

1

1n

PV r

=

+

.

For a given future value at a specified time in the future, the higher the interest rate (or discount

rate), the lower the present value. For a given interest rate (discount rate), the further into the

future that the future value will be received, then the lower its present value.

Present Value of a Series of Future Values

To determine the present value of a series of future values, the present value of each future value

must first be computed. Then these present values are added together to obtain the present value

of the entire series of future values.

Present Value of an Ordinary Annuity

When the same dollar amount of money is received each period or paid each year, the series is

referred to as an annuity. When the first payment is received one period from now, the annuity is

called an ordinary annuity. When the first payment is immediate, the annuity is called an annuity

due.

The present value of an ordinary annuity is:

( )

1

11n

r

PV = A r

−

+

whereA is the amount of the annuity (in dollars).

The term in brackets is the present value of an ordinary annuity of $1 for n periods.

Example of Present Value of an Ordinary Annuity Using Annual Interest:

If A = $100, r = 0.09, and n = 8, then:

( )

1

11n

r

PV = A r

−

+

=

( )

8

1

1

1.09

$100 0.09

−

1

1

1.99256

$100 0.09

−

=

=

1 0.501867

$100 0.09

−

= $100[5.534811] = $553.48.

Present Value When Payments Occur More Than Once Per Year

If the future value to be received occurs more than once per year, then the present value formula

is modified so that (i) the annual interest rate is divided by the frequency per year, and (ii) the

number of periods when the future value will be received is adjusted by multiplying the number

of years by the frequency per year.

PRICING A BOND

Determining the price of any financial instrument requires an estimate of (i) the expected cash

flows, and (ii) the appropriate required yield. The required yield reflects the yield for financial

In general, the price of a bond can be computed using the following formula:

( ) ( )

111

nttn

t=

M

C

P= +

r + r

+

.

whereP = price (in dollars), n = number of periods (number of years times 2), C = semiannual

coupon payment (in dollars), r = periodic interest rate (required annual yield divided by 2),

M = maturity value, and t = time period when the payment is to be received.

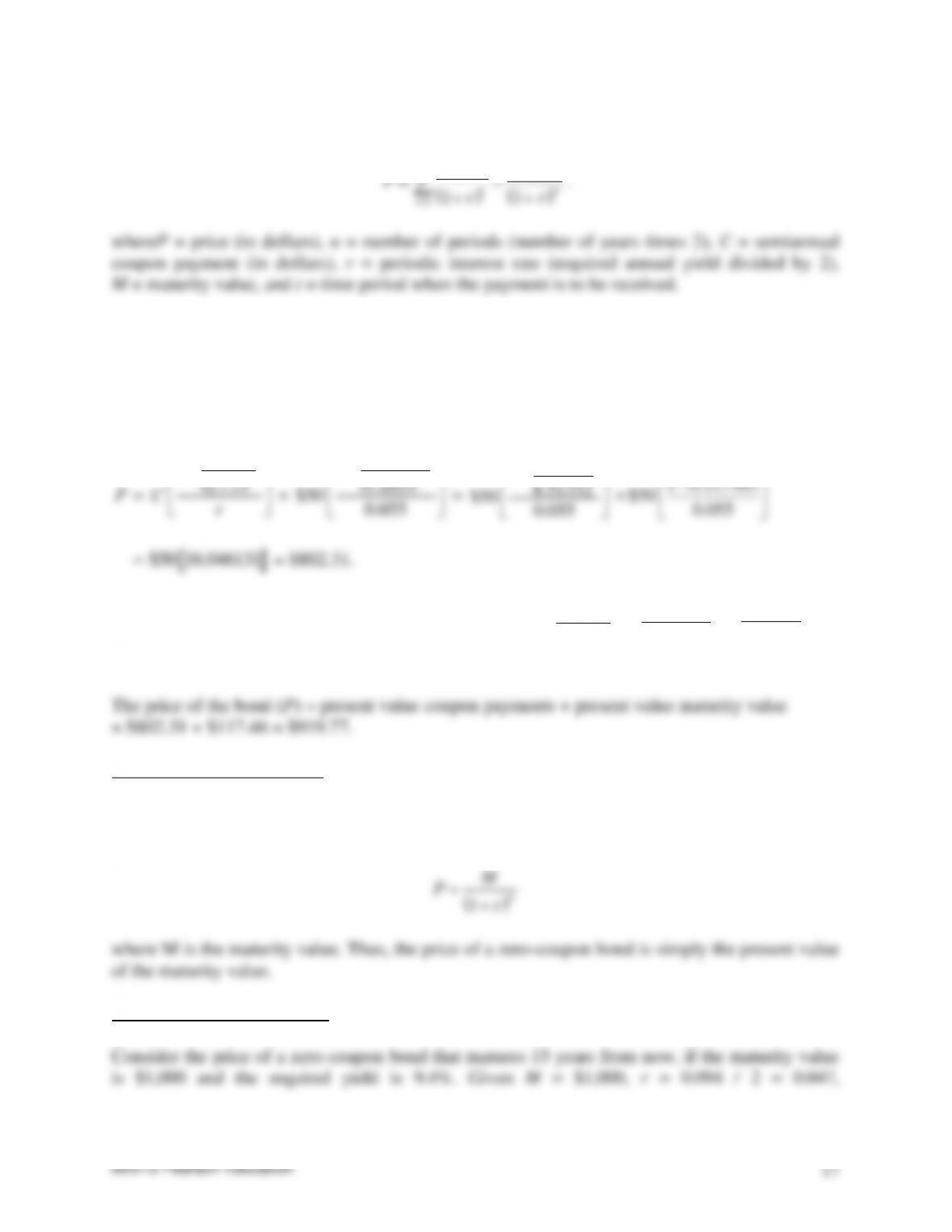

Computing the Value of a Bond: An Example:

Consider a 20-year 10% coupon bond with a par value of $1,000 and a required yield of 11%.

Given C = 0.1($1,000) / 2 = $50, n = 2(20) = 40 and r = 0.11 / 2 = 0.055, the present value of the

coupon payments is:

( )

1

11n

r

P = C r

−

+

=

( )

40

1

1

1.055

$50 0.055

−

=

1

1

8.51332

$50 0.055

−

=

1 0.117463

$50

0.055

−

$50 16.046131 =

= $802.31.

The present value of the par or maturity value of $1,000 is:

( )

1n

M

r+

=

( )

40

$1,000

.055

1

=

51331.8

000,1$

= $117.46.

Pricing Zero-Coupon Bonds

For zero-coupon bonds, the investor realizes interest as the difference between the maturity value

and the purchase price. The equation is:

( )

1n

M

P r

=+

where M is the maturity value. Thus, the price of a zero-coupon bond is simply the present value

of the maturity value.

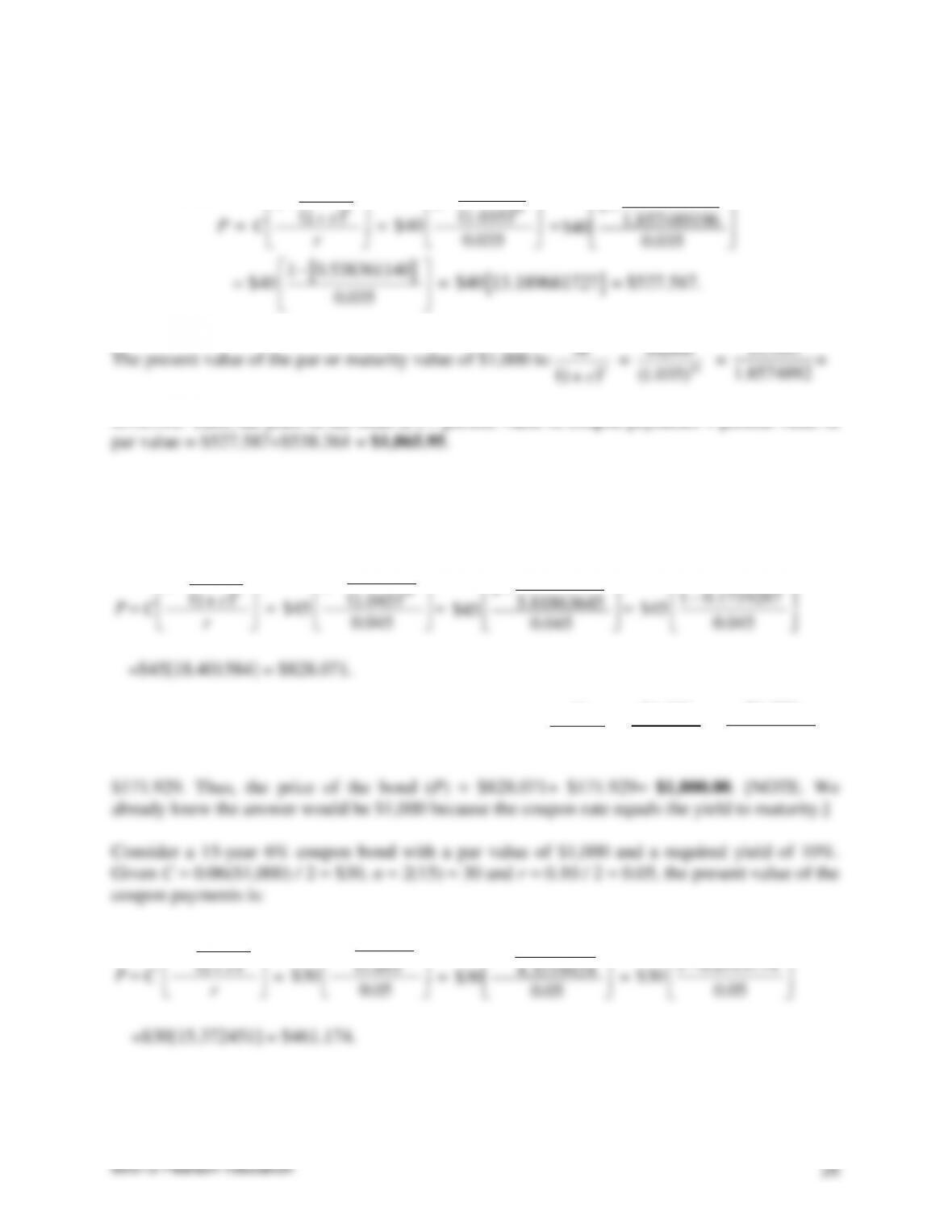

Zero-Coupon Bond Example

©2013 Pearson Education

18

and n = 2(15) = 30, we have:

(1 )n

M

=

P + r

=

( )

30

$1,000

1.047

=

99644.3

000,1$

= $252.12.

Price-Yield Relationship

A fundamental property of a bond is that its price changes in the opposite direction from the

change in the required yield. The reason is that the price of the bond is the present value of the

cash flows.

Relationship Between Coupon Rate, Required Yield, and Price

When yields in the marketplace rise above the coupon rate at a given point in time, the price of

the bond falls so that an investor buying the bond can realizes capital appreciation. The

Relationship Between Bond Price and Time if Interest Rates Are Unchanged

For a bond selling at par value, the coupon rate is equal to the required yield. As the bond moves

closer to maturity, the bond will continue to sell at par value. Its price will remain constant as the

bond moves toward the maturity date.

Reasons for the Change in the Price of a Bond

The price of a bond can change for three reasons: (i) there is a change in the required yield owing

to changes in the credit quality of the issuer; (ii) there is a change in the price of the bond selling

COMPLICATIONS

The framework for pricing a bond assumes the following: (i) the next coupon payment is exactly

six months away; (ii) the cash flows are known; (iii) the appropriate required yield can be

determined; and, (iv) one rate is used to discount all cash flows.

Next Coupon Payment Due in Less than Six Months

When an investor purchases a bond whose next coupon payment is due in less than six months,

the accepted method for computing the price of the bond is as follows:

11

=1

=

(1 + r)

n

vt vn

t

M

C

P +

(1 + r (1 + r (1 + r

)))

−−

wherev = (days between settlement and next coupon) / (days in six-month period).

Cash Flows May Not Be Known

Determining the Appropriate Required Yield

One Discount Rate Applicable to All Cash Flows

PRICING FLOATING-RATE AND INVERSE-FLOATING-RATE SECURITIES

The cash flow is not known for either a floating-rate or an inverse-floating-rate security; it will

depend on the reference rate in the future.

Price of a Floater

The coupon rate of a floating-rate security (or floater) is equal to a reference rate plus some

Price of an Inverse Floater

In general, an inverse floater is created from a fixed-rate security. The security from which the

inverse floater is created is called the collateral. From the collateral two bonds are created: a

floater and an inverse floater.

The price of a floater depends on (i) the spread over the reference rate and (ii) any restrictions

that may be imposed on the resetting of the coupon rate. For example, a floater may have a

maximum coupon rate called a capor a minimum coupon rate called a floor. The price of a

PRICE QUOTES AND ACCRUED INTEREST

Price Quotes

A bond selling at par is quoted as 100, meaning 100% of its par value. A bond selling at a

Accrued Interest

When an investor purchases a bond between coupon payments, the investor must compensate the

seller of the bond for the coupon interest earned from the time of the last coupon payment to the

KEY POINTS

• The price of a bond is the present value of the bond’s expected cash flows, the discount rate

being equal to the yield offered on comparable bonds.For an option-free bond, the cash flows

• For a zero-coupon bond, there are no coupon payments. The price of a zero-coupon bond is

equal to the present value of the maturity value, where the number of periods used to compute

the present value is double the number of years and the discount rate is a semiannual yield.

• A bond will be priced below, at par, or above par depending the bond’s coupon rate and the

required yield required by investors. When the coupon rate is equal to the required yield, the

bond will sell at its par value. When the coupon rate is less (greater) than the required yield,

the bond will sell for less (more) than its par value.

• Over time, the price of a premium or discount bond will change even if the required yield

does not change.Assuming that the credit quality of the issuer is unchanged, the price change

• The price of a floating-rate bond will trade close to par value if the spread required by the

market does not change and there are no restrictions on the coupon rate.

• The price of an inverse floater depends on the price of the collateral from which it is created

and the price of the floater.

• Accrued interest is the amount that a bond buyer who purchases a bond between coupon

ANSWERS TO QUESTIONS FOR CHAPTER 2

(Questions are in bold print followed by answers.)

1. A pension fund manager invests $10 million in a debt obligation that promises to pay

7.3% per year for four years. What is the future value of the $10 million?

2. Suppose that a life insurance company has guaranteed a payment of $14 million to a

pension fund 5.5 years from now. If the life insurance company receives a premium of

$10.4 million from the pension fund and can invest the entire premium for 5.5 years at an

annual interest rate of 6.35%, will it have sufficient funds from this investment to meet the

$14 million obligation?

3. Answer the below questions.

(a) The portfolio manager of a tax-exempt fund is considering investing $500,000 in a debt

instrument that pays an annual interest rate of 5.7% for four years. At the end of four

years, the portfolio manager plans to reinvest the proceeds for three more years and

expects that for the three-year period, an annual interest rate of 7.2% can be earned. What

is the future value of this investment?

At the end of year four, the portfolio manager’s amount is given by: Pn= P0 (1 + r)n. Inserting in

(b) Suppose that the portfolio manager in Question 3, part a, has the opportunity to invest

the $500,000 for seven years in a debt obligation that promises to pay an annual interest

rate of 6.1% compounded semiannually. Is this investment alternative more attractive than

the one in Question 3, part a?

©2013 Pearson Education

23

we have P7= $500,000(1 + 0.061/2)2(7) = $500,000(1.0305)14 = $500,000(1.522901960) =

$761,450.98. Thus, this investment alternative is not more attractive. It is less by the amount of

$761,450.98 – $768,872.47 = −$7,421.49.

4. Suppose that a portfolio manager purchases $10 million of par value of an eight-year

bond that has a coupon rate of 6% and pays interest once per year. The first annual

coupon payment will be made one year from now. How much will the portfolio manager

have if she (1) holds the bond until it matures eight years from now, and (2) can reinvest all

the annual interest payments at an annual interest rate of 6.2%?

At the end of year eight, the portfolio manager’s amount is given by the following equation,

which adjusts for annual compounding.

We have:

( )

11

+ Par Value

n

n

+ r

P A

r

−

=

where A = coupon rate times par value. Inserting in our values, we have:

062.0

1)062.01(

)000,000,10($06.0 8

8

−+

=P

+ $10,000,000 = $600,000[9.9688005] + $10,000,000 =

$5,981,280.33 + $10,000,000 = $15,981,280.33.

5. Answer the below questions.

(a) If the discount rate that is used to calculate the present value of a debt obligation’s cash

flow is decreased, what happens to the price of that debt obligation?

A fundamental property of a bond is that its price changes in the opposite direction from the

change in the required yield. The reason is that the price of the bond is the present value of the

(b) Suppose that the discount rate used to calculate the present value of a debt obligation’s

cash flow is x%. Suppose also that the only cash flows for this debt obligation are $2,000

four years from now and $2,000 five years from now. For which of these cash flows will the

present value be greater?

Cash flows that come earlier will have a greater value. As long as x% is positive and the amount

is the same, the present value will be greater for the $2,000 four years from now compared to

( ) ( )

45

1 x 1 x

++

6. The pension fund obligation of a corporation is calculated as the present value of the

actuarially projected benefits that will have to be paid to beneficiaries. Why is the interest

rate used to discount the projected benefits important?

7. (a) A pension fund manager knows that the following liabilities must be satisfied:

Years from Now

Liability (in millions)

1

2.0

2

3.0

3

5.4

4

5.8

Suppose that the pension fund manager wants to invest a sum of money that will satisfy

this liability stream. Assuming that any amount that can be invested today can earn an

annual interest rate of 7.6%, how much must be invested today to satisfy this liability

stream?

To satisfy year one’s liability (n = 1), the pension fund manager must invest an amount today

that is equal to the future value of $2.0 million at 7.6%. We have:

( )

1

nn

PV P

1 + r

=

=

)

076(1.

1

000,000,2$ 1

=

929368030.0000,000,2$

= $1,858,736.06.

To satisfy year two’s liability (n = 2), the pension fund manager must invest an amount today

that is equal to the future value of $3.0 million at 7.6%. We have:

( )

1

nn

PV P

=

1 + r

)

076(1.

1

To satisfy year three’s liability (n = 3), the pension fund manager must invest an amount today

that is equal to the future value of $5.4 million at 7.6%. We have:

( )

nn

PV P

1 + r

=

)

076(1.

1

1

To satisfy year four’s liability (n = 4), the pension fund manager must invest an amount today

that is equal to the future value of $5.8 million at 7.6%. We have:

( )

1

nn

PV P

1 + r

=

=

)

076(1.

1

000,800,5$ 4

=

30.74602076000,800,5$

= $4,326,920.42.

If we add the four present values, we get $1,858,736.06 + $2,591,174.80 + $4,334,679.04 +

$4,326,920.42 = $13,111,510.32, which is the amount the pension fund manager needs to invest

today to cover the liability stream for the next four years.

b) How much must be invested today if the interest rate is the same but the liabilities

stream is changed to the following table?

Years from Now

Liability (in millions)

1

2.0

2

3.0

3

3.0

4

3.0

5

5.4

6

5.4

7

5.4

8

5.4

9

5.8

10

5.8

C = 0.08($1,000) / 2 = $40, n = 2(9) = 18 and r = 0.07 / 2 = 0.035, the present value of the

coupon payments is:

( )

1

11n

r

P = C r

−

+

=

( )

18

1

1

1.035

$40

0.035

−

=

1

1

1.857489196

$40 0.035

−

1 0.538361140

$40

0.035

−

=

=

$40 13.189681727

= $527.587.

( )

1n

M

+ r

18

$1,000

(1.035)

$1,000

1.8574892

$538.361. Thus, the price of the bond (P) = present value of coupon payments + present value of

Consider a 20-year 9% coupon bond with a par value of $1,000 and a required yield of 9%.

Given C = 0.09($1,000) / 2 = $45, n = 2(20) = 40 and r = 0.09 / 2 = 0.045, the present value of

the coupon payments is:

( )

1

11n

r

P = C r

−

+

=

( )

40

1

1

1.045

$45 0.045

−

=

1

1

5.81863645

$45 0.045

−

=

1 0.1719287

$45 0.045

−

=$45[18.401584] = $828.071.

The present value of the par or maturity value of $1,000 is:

( )

1n

M

+ r

=

( )

40

$1,000

1.045

=

$1,000

5.81863645

=

( )

1

11n

r

P = C r

−

+

=

( )

30

1

1

1.05

$30 0.05

−

=

1

1

4.3219424

$30 0.05

−

=

1 0.2313774

$30

0.05

−

=$30[15.372451] = $461.174.

©2013 Pearson Education

27

( )

1n

M

+ r

( )

30

$1,000

1.05

3219424.4

000,1$

$231.377. Thus, the price of the bond (P) = $461.174+ $231.377= $692.55.

Consider a 14-year 0% coupon bond with a par value of $1,000 and a required yield of 8%.

Given C = 0($1,000) / 2 = $0, n = 2(14) = 28 and r = 0.08 / 2 = 0.04, the present value of the

coupon payments is:

( )

1

11n

r

P = C r

−

+=

28

1

1

(1.04)

$0 0.04

−

=

1

1

2.998703319

$0 0.055

−

=

055.0

0.33477471 1

0$

−

=$0[16.66306322] = $0.[NOTE. We already knew the answer because the coupon rate is

zero.]

The present value of the par or maturity value of $1,000 is:

( )

1n

M

+ r

=

( )

28

$1,000

1.04

=

$1,000

2.99870332

9. Consider a bond selling at par ($100) with a coupon rate of 6% and 10 years to maturity.

(a) What is the price of this bond if the required yield is 15%?

We have a 10-year 6% coupon bond with a par value of $1,000 and a required yield of 15%.

the coupon payments is:

( )

1

11n

r

P = C r

−

+

=

20

1

1

(1.075)

$30 0.075

−

=

1

1

4.2478511

$30 0.075

−

=

1 0.2354131

$30 0.075

−

=$30[10.1944913] = $305.835.

The present value of the par or maturity value of $1,000 is:

( )

1n

M

+ r

=

( )

20

$1,000

1.075

=

$1,000

4.2478511

(b) What is the price of this bond if the required yield increases from 15% to 16%, and by

what percentage did the price of this bond change?

( )

1

11n

r

P = C r

−

+=

20

1

1

(1.08)

$30

0.08

−

=

9.8181474 30$

= $294.544.

The present value of the par or maturity value of $1,000 is:

( )

1n

M

+ r

=

( )

20

$1,000

1.08

= $214.548.

$509.09 $541.25

−

(d) What is the price of this bond if the required yield increases from 5% to 6%, and by

what percentage did the price of this bond change?

If the required yield increases from 5% to 6%, then we have:

( )

1

11n

r

P = C r

−

+=

20

1

1

(1.03)

$30 0.03

−

=

$30 14.87747486 =

$446.324.

( )

1n

M

+ r =

20

$1,000

(1.03) =

answer would be $1,000 because the coupon rate equals the yield to maturity.]

(e) From your answers to Question 9, parts b and d, what can you say about the relative

price volatility of a bond in a high-interest-rate environment compared to a low-interest-

rate environment?

10. Suppose that you purchased a debt obligation three years ago at its par value of

$100,000 and nine years remaining to maturity. The market price of this debt obligation

today is $90,000. What are some reasons why the price of this debt obligation could have

declined from time you purchased it three years ago?

The price of a bond will change for one or more of the following three reasons:

(i) There is a change in the required yield owing to changes in the credit quality of the issuer.

The first and third reasons are the likely reasons for the situation where the bond has plummeted

from $100,000 to $90,000. The bond has plummeted in value because the credit quality of the

11. Suppose that you are reviewing a price sheet for bonds and see the following prices (per

$100 par value) reported. You observe what seem to be several errors. Without calculating

the price of each bond, indicate which bonds seem to be reported incorrectly, and explain

why.

Bond

Price

Coupon Rate (%)

Required Yield (%)

U

90

6

9

V

96

9

8

W

110

8

6

X

105

0

5

Y

107

7

9

Z

100

6

6

If the required yield is the same as the coupon rate then the price of the bond should sell at its par

value. This is the case of bond Z since par values are typical at or near a $100 quote. If the

required yield decreases below the coupon rate then the price of a bond should increase. This is

12. What is the maximum price of a bond?

Consider an extreme case of a 100-year 20% coupon bond with a par value of $1,000 that after

and r = 0.01 / 2 = 0.005, the present value of the coupon payments is:

( )

1

11n

r

P = C r

−

+=

198

1

1

(1.005)

$100

0.005

−

=

1

1

2.684604

$100

0.005

−

1 0.3724944

$100 0.005

−

==

$1,000[1,125.51012] = $12,550.112.

( )

1n

M

+ r

198

$1,000

(1.005)

$1,000

2.684604

Thus, the price of the bond (P) = $12,550.112 + $372.494 = $12,922.61.

If the required yield falls to 0.001%, then the bond price would increase to $20,778.33, which

13. What is the “dirty” price of a bond?

14. Explain why you agree or disagree with the following statement: “The price of a floater

will always trade at its par value.”

(2) any restrictions that may be imposed on the resetting of the coupon rate. For example, a

floater may have a maximum coupon rate called a cap or a minimum coupon rate called a floor.

15. Explain why you agree or disagree with the following statement: “The price of an

inverse floater will increase when the reference rate decreases.”

As explained below, one would disagree with the statement: “The price of an inverse floater will

increase when the reference rate decreases.”

The factors that affect the price of an inverse floater are affected by the reference rate only to the