Chapter 15 – Options Markets

CHAPTER FIFTEEN

OPTIONS MARKETS

CHAPTER OVERVIEW

This chapter describes characteristics of options, terminology used in the options’ markets,

option payoffs and profits to both option owners and sellers (called writers), and positions that

are comprised of combinations of options and stock or multiple option contracts. Option-like

assets, such as callable bonds, warrants, and collateralized loans are also described.

LEARNING OBJECTIVES

After studying this chapter, the student should be able to calculate potential profits resulting from

various option trading strategies and to formulate portfolio management strategies to modify the

risk-return attributes of the portfolio. The student should be able to identify the embedded

options in various assets and to determine how these option characteristics affect the prices of

these assets.

CHAPTER OUTLINE

1. The Option Contract

PPT 15-2 through PPT 15-8

A listed call option is a contract giving the holder the right to buy 100 shares of stock at a preset

price called the exercise or strike price. A listed put option is a contract giving the holder the

right to sell 100 shares of stock at a preset price. Expirations of 1,2,3,6, 9 months and sometimes

1 year are normal contract periods. Contracts expire on the Saturday following the third Friday

American vs. European options

Chapter 15 – Options Markets

With an American style option the option can be exercised at any date after purchase whereas

with a European style option the option can only be exercised immediately before expiration

Options Uses

Options have a long and checkered history. There are records that show that options were used

in ancient Egypt. They were also used during the tulip bulb mania in Holland and when the tulip

bubble burst many option holders lost large sums and option writers defaulted. After this

The OCC

The option exchanges operate the Option Clearing Corporation (OCC). An option buyer or

seller technically buys or sells from or to the OCC. The OCC backs performance of both

counterparties. This allows liquid anonymous trading to occur. To limit the OCC’s risk the

option seller (or writer) must post margin. The margin varies with option price and whether the

option position is covered or exposed. An in the money option requires more margin than an out

2. Values of Options at Expiration

PPT 15-9 through PPT 15-26

Chapter 15 – Options Markets

This section requires the use of some terminology:

Symbols & Valuation

Ct = Price paid for a call option at time t. t = 0 is today,

T = Immediately before the option’s expiration.

Pt = Price paid for a put option at time t.

St = Stock price at time t.

X = Exercise or Strike Price

A call is “in the money” if St > X. A put is “in the money” if St < X.

A call is “out of the money” if St < X. A put is “out of the money” if St > X.

An option is in the money if you could profitably exercise it right now. Basic option pricing

boundaries are developed below:

C and P are greater than zero because the holders have a choice to use them or not. A simple

arbitrage argument (shown above) can be used to demonstrate that the call price must be greater

than or equal to the difference between the stock price and the exercise price. This is the basis

for the price boundary of a call Ct ≥ Max (0, St – X).

Chapter 15 – Options Markets

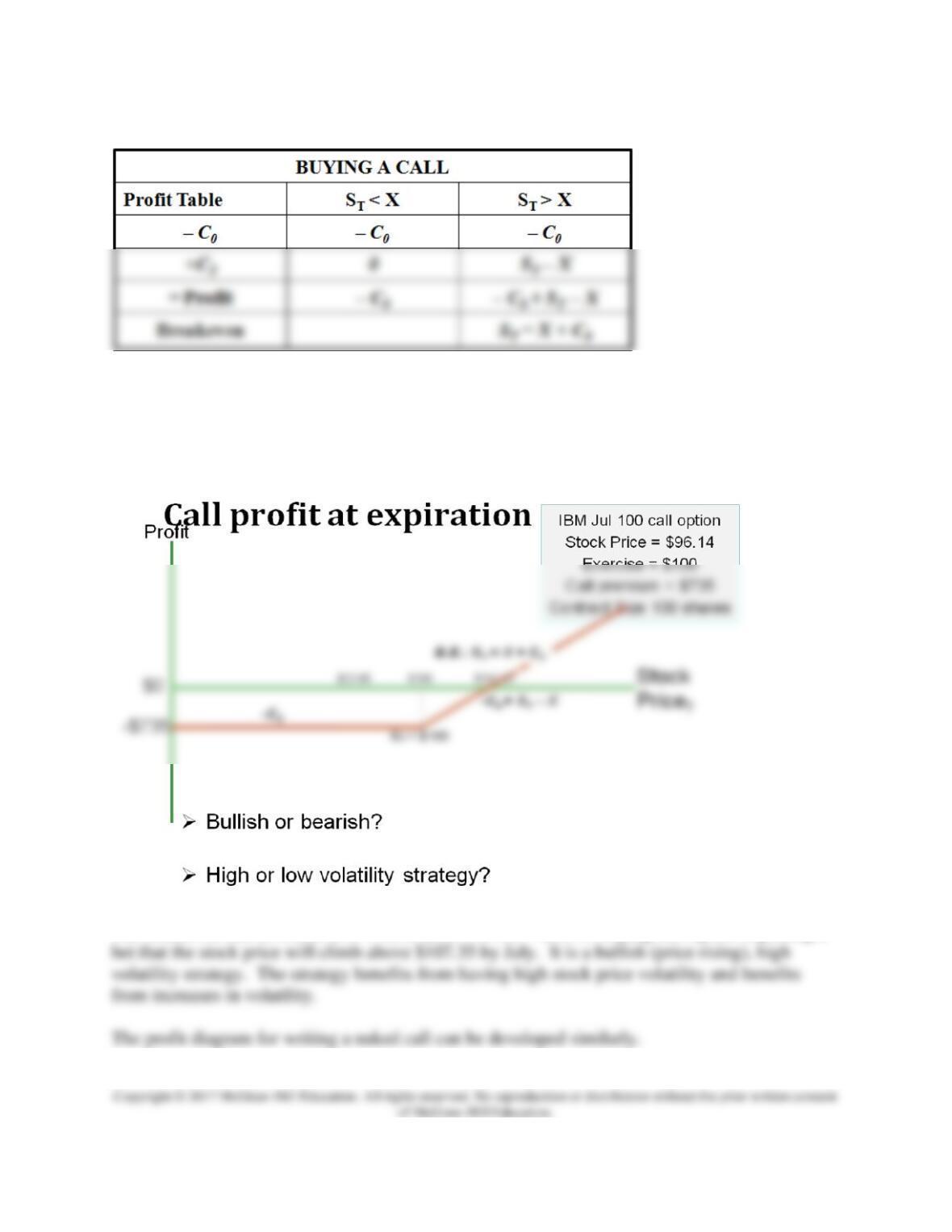

Using data on IMB calls given in Figure 15.1 in the text for the July 100 call we can construct

the profit graph that illustrates the possible payoff at option expiration that can result at various

stock prices.

The breakeven can be found as X + C0 or $100 + $7.35 = $107.3 Buying this option is placing a

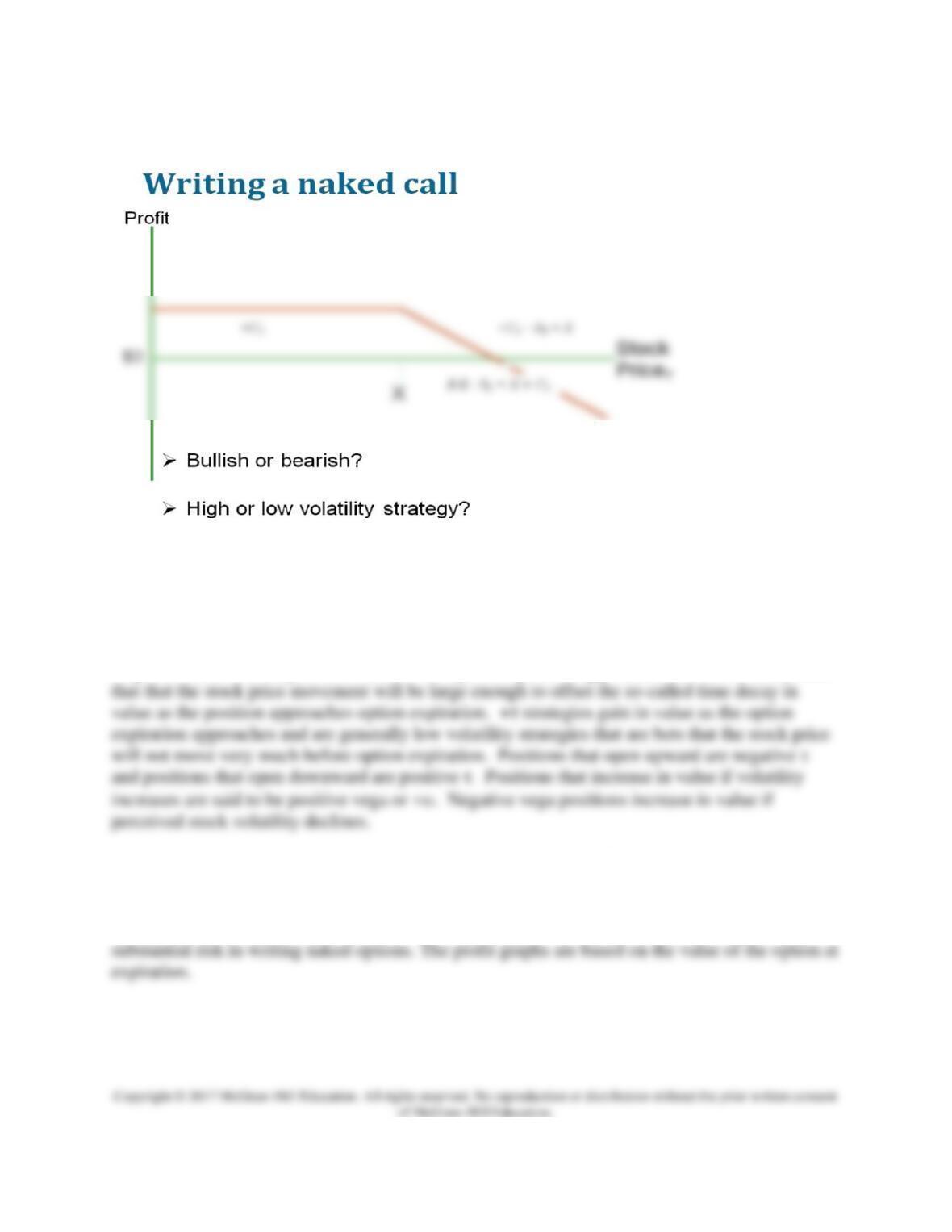

Chapter 15 – Options Markets

This is a bearish and low volatility strategy. Any strategy that opens upward will be a high

volatility strategy and any strategy that opens downward will be a low volatility strategy.

Option traders use Greek symbols to characterize strategies. A +∆ strategy is bullish, a bearish

strategy is said to be negative delta or –∆. A delta neutral strategy is unaffected by a stock price

change or is equally affected by the same amount for a given price increase or decrease.

Negative theta –τ strategies lose value as the option expiration approaches and are basically bets

The put writer has unlimited loss potential if the stock price falls. The profit for a put writer is

limited to a premium of the option. The text has an excellent boxed item entitled, “The Black

Hole: How Some Investors Lost All Their Money in the Market Crash.” The example of the risk

involved in writing naked puts surrounding the October 1987 Market Crash points out the

upside potential and offers some protection to the owner of the stock if the stock price declines.

A straddle is constructed by purchasing a call and a put with the same exercise date and maturity

date. A straddle will result in profits if the stock price increases or decreases enough to

overcome the premiums for the options.

Warnings about Option Strategies

Options may have to move 10-15% or more in a short time period before an investor recovers the

price & commission. Most options expire worthless. Options are by definition short term

instruments; an investor can ride out bad times in spot markets but not in options. The limited

loss feature makes options appear safer than they are. You have to compare equal dollar

investments in stocks and options to truly see the higher risk of the option position. Options are

3. Optionlike Securities

PPT 15-27 through PPT 15-34

Many securities are complex products that include imbedded options. The payoffs and profits

associated with securities that contain imbedded options will present payoffs that are similar to

options or groups of options. Examples that demonstrate the impact of embedded options include

callable bonds, convertible bonds, collateralized loans and levered equity and these are covered

4. Exotic Options

PPT 15-35

Discussion of these options is useful in making students aware of the all the various types of

options that are available to construct different desired payoffs. Asian- Payoffs depend on the

average (rather than the final) price of the underlying asset during a portion of the life of the

option. Barrier Options’ value depends on whether the underlying asset price has passed through

Excel Applications