CHAPTER 13

NONAGENCY RESIDENTIAL

MORTGAGE-BACKED SECURITIES

CHAPTER SUMMARY

In this chapter, we discuss the nonagency RMBS market, focusing on the structure of the

securities created, particularly on credit enhancement. We will describe the different forms of

COLLATERALIZED TYPES

Conforming mortgages are typically collateral for agency RMBS while nonconforming

mortgages are for nonagency RMBS. The collateral backing a nonagency RMBS is set forth in

the prospectus as illustrated in an actual deal. Typically a deal will be backed by a combination

of collateral types.

CREDIT ENHANCEMENT

Because there is no government guarantee or guarantee by a GSE, to receive an investment-grade

rating, these securities must be structured with additional credit support. The credit support is

needed to absorb expected losses from the underlying loan pool due to defaults. This additional

rating. The process by which the rating agencies determine the amount of credit enhancement

needed is referred to as sizing the transaction.

Structural Credit Enhancement

Structural credit enhancement refers to the redistribution of credit risks among the bond

classes comprising the structure in such a way as to provide credit enhancements by one bond

class to the other bond classes in the structure. This is achieved by creating bond classes with

The bond class in the capital structure with the highest rating is referred to as the senior bond

class. The subordinated bond classes in the capital structure are those below the senior

Most AAA bond classes have been downgraded since 2007. As of year-end 2010, only a small

amount of outstanding nonagency RMBS have an investment-grade rating.

Shifting Interest Mechanism in a Senior-Subordinated Structure

Because of the major credit concerns in subprime RMBS deals and the need to protect the senior

bond class, almost all senior-subordinated structures backed by subprime loans incorporate

The prospectus will specify how different scheduled principal payments and prepayments will be

allocated between the senior bond class and the subordinated bond class. The scheduled principal

payments are allocated based on the senior percentage. The senior percentage, also called the

and if the collateral or structure fails any of the tests, this will trigger an override of the base

schedule.

Deal Step-Down Provisions

An important feature in analyzing senior-subordinated bond classes or deals backed by

residential mortgages is the deal’s step-down provisions. These provisions allow for the

In addition to triggers based on the performance of the collateral, there is a balance test. This test

involves comparing the change in the senior interest from the closing of the deal to the current

month. If the senior interest has increased, the balance test is failed, triggering a revision of the

base schedule for the allocation of principal pay-ments from the subordinated bond classes to the

senior bond class.

(2) used to pay any losses realized by the collateral for the month, (3) retained by the SPV and

accumulated in a reserve account and used to offset not only current losses experienced by the

collateral but also future losses, or (4) some combination of the others.

In terms of cash collateral, excess spread that we have just described is one of three ways that

an originator/seller of the collateral can provide cash to absorb collateral losses. There are two

Today, few, if any, deals are done with insurance by monoline insurers, bank letters of credit,

and related-party guarantees. Risk-based capital requirements have made letters of credit for

banks unattractive. Third-party related guarantors are rare because the parent of the

originator/seller is typically not triple A rated.

CASH FLOW FOR NONAGENCY MORTGAGE-BACKED SECURITIES

©2013 Pearson Education

294

agency as part of its guarantee. For a nonagency RMBS, one or more bond classes may be

affected by defaults, and therefore, defaults must be taken into account in estimating the cash

flow of a bond class.

Prior to the subprime mortgage crisis, investors assumed that the triple A senior bonds of

nonagency RMBS were exposed to minimal credit risk. The performance of loans backing

nonagency RMBS deals demonstrated the critical importance of assessing the factors that impact

defaults.

What the subprime mortgage crisis clearly showed is that defaults are not just tied to the level of

economic activity but also housing prices. Economic difficulties faced by borrowers that

followed a period of rising prices provided lenders with a strong position in the collateral as long

as the loan-to-value ratio (LTV) was not high.

The opportunity to sell the property to repay the loan is not available if the property declines

below the outstanding mortgage balance (i.e., the current LTV exceeds 1 or, equivalently, the

as the recovered principal. The servicer must report separately traditional prepayments (which

are called voluntary prepayments) and credit-related prepayments (which are called

involuntary prepayments).

Delinquency Measures

A delinquency is requirement before a loan can be classified as in default. Loans are classified as

©2013 Pearson Education

295

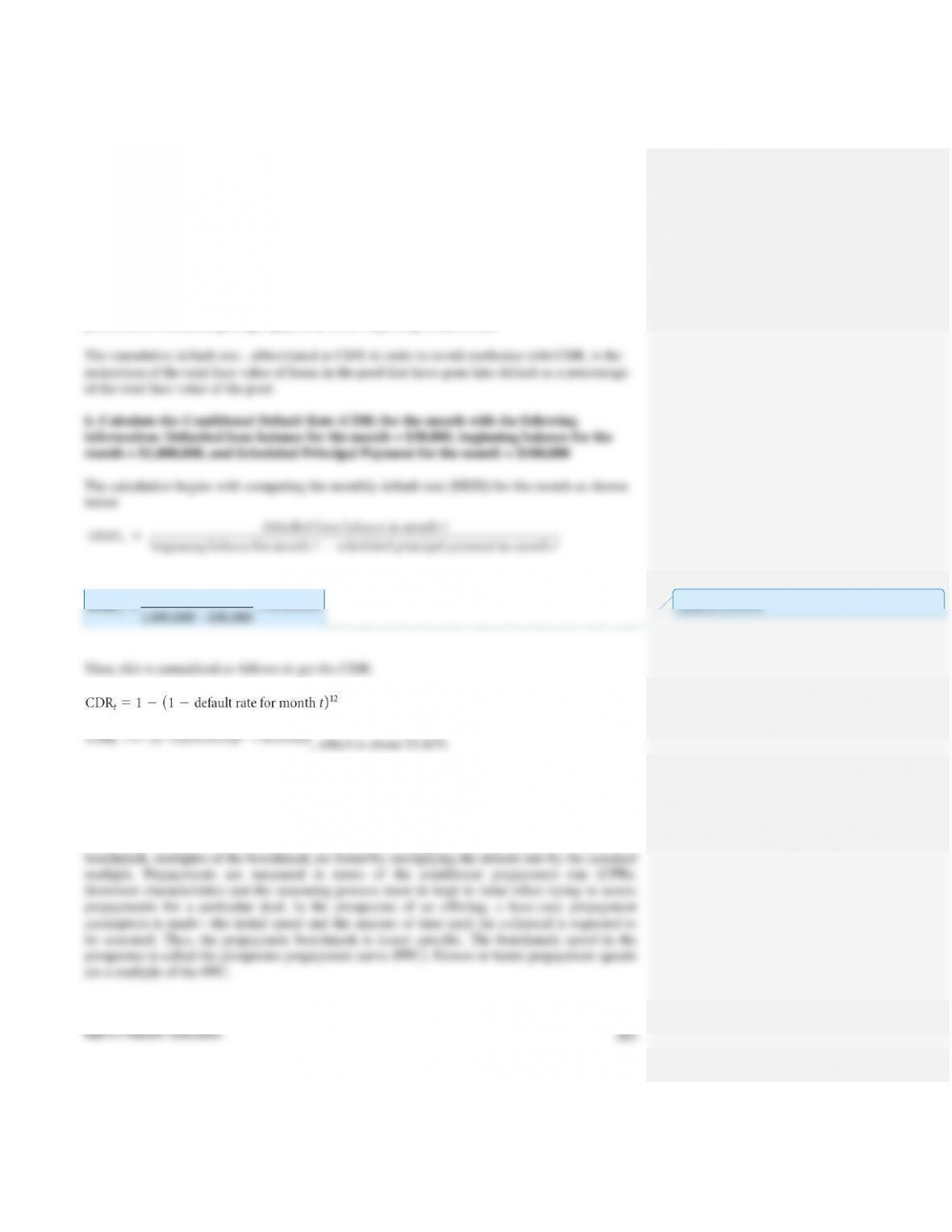

month. The calculation begins with computing the monthly default rate (MDD) for the month

as shown below:

Monthly default rate for month t

MMDt =

defaulted loan balance in month t

beginningbalance for month t scheduled principal payment in month t−

Then, this is annualized as follows to get the CDR:

multiple.

Prepayment Measures

Prepayments are measured in terms of the conditional prepayment rate (CPR). Borrower

characteristics and the seasoning process must be kept in mind when trying to assess

prepayments for a particular deal. In the prospectus of an offering, a base-case prepayment

In a nonagency RMBS deal the servicer has an important function, not only with respect to

collecting payments due from borrowers in the loan pool and repossessing and then selling the

property when there are defaults, but also in advancing principal and interest on delinquent loans.

There are specific conditions as to when a servicer need not make such advance payments. In

most deals, the servicer is not required to advance any amount that it deems “nonrecoverable”

saw it as the inevitable bursting of the “housing bubble” that had characterized the housing

market in prior years. Others viewed it as the product of unsavory practices by mortgage lenders

who deceived subprime borrowers into purchasing homes that they could not afford. Moreover,

specific mortgage designs such as hybrid loans made it possible for a subprime borrower to

obtain a loan that could have been expected to cause financial difficulties in the future when loan

The securitization of subprime loans works by dividing pools of credit into classes, or bond

classes, separated by the amount of risk each class represents. Naturally, the classes with less risk

offer lower potential returns while the classes with more risk offer higher potential returns.

The more junior, riskier classes are purchased by sophisticated institutional investors who

understand that they may incur losses but hope for high enough returns over a long period of

©2013 Pearson Education

297

Rating agencies were also viewed by some market observers as being a major contributor to the

crisis. Recall that to aid investors in comparing the relative credit risk of securities, issuers

generally ask one or more rating agencies to assign a credit rating to the securitization. The

accuracy of ratings, like any other indicator of credit risk, can only be assessed on a statistical

basis over a long period of time.

What is surprising to market observers is why the crisis occurred in July 2007. There was no new

information in the market at the time. Investors knew well before that time all about the potential

defaults. Moreover, since 2005, the rating agencies took action that was transparent to the

market. Specifically, rating agencies adjusted their criteria and assumptions regarding how they

RMBS and traded in separate markets, following the subprime mortgage crisis in 2007 and

the meltdown of the housing market, these two sectors are no longer viewed differently.

• Although there has been very little issuance since 2008, there is a considerable amount of

nonagency RMBS outstanding backed by prime loans, subprime loans, Alt-A loans, second

lien loans, and option ARM loans.

(2) originator provided (excess spread, cash reserve, overcollateralization), and (3) third-party

provided.

• The cash flow of a nonagency RMBS depends on defaults and prepayments.

• Default rates are measured in terms of the conditional default rate and the cumulative default

©2013 Pearson Education

298

• Voluntary prepayments and involuntary prepayments must be projected in projecting the

collateral’s cash flow.

• The treatment of advances and modified loans by mortgage services has an impact on the

bond classes in a nonagency RMBS deal.

ANSWERS TO QUESTIONS FOR CHAPTER 13

(Questions are in bold print followed by answers.)

1. Answer the below questions.

a. Why is it necessary for a nonagency mortgage-backed security to have credit

enhancement?

and (4) monoline insurance. Common in structures with subprime mortgage loans for senior-

subordinated structures is the shifting interest mechanism. The cash flow of a nonagency MBS

depends on defaults and prepayments. Default rates are measured in terms of the conditional

default rate and the cumulative default rate. A standardized benchmark for default rates was

formulated by PSA.

We can compare what is being done to distribute credit risk in a nonagency MBS with what is

done in an agency CMO. In an agency CMO, there is no credit risk for Ginnie Mae issued

structures and the credit risk of the loan pool for Fannie Mae and Freddie Mac issued structure is

viewed until recent years as small. What is being done in creating the different bond classes in an

agency CMO is the redistribution of prepayment risk. In contrast, in a nonagency MBS, there is

both credit risk and prepayment risk. By creating the senior-subordinated bond classes, credit

risk is being redistributed among the bond classes in the structure. Hence, what is being done is

credit tranching.

b. Who determines the amount of credit enhancement needed?

Credit enhancement is a key part of the securitization transaction in structured finance, and is

important for credit rating agencies when rating a securitization. Credit enhancement is the

process of reducing credit risk by requiring collateral, insurance, or other agreements to provide

the lender with reassurance that it will be compensated if the borrower defaulted. When rating

2. What is the difference between a private label and subprime mortgage-backed security?

Be sure to mention how they differ in terms of credit enhancement.

The residential mortgage-backed securities (RMBS) market is divided into two sectors: agency

MBS and nonagency MBS. RMBS issued in the nonagency MBS market require that credit

enhancement be provided to protect against losses from the loan pool. The nonagency MBS market

3. Answer the below questions.

a. What is an option ARM loan?

A type of adjustable-rate mortgage (ARM) loans popular during the period between 2001 and

2007 (when ARM issuance reached its peak) was hybrid ARM loans, also referred to as option

b. Why is it unlikely that this loan type will be originated in the future?

The 2007 subprime mortgage crisis, it is not likely that this loan type will continue due to the

risks that were brought out with this crisis. This is explained below.

While the flexibility built into option ARM loans come with risks. First, investors can not

increase their equity unless the make the larger amortizing payments. Most investors choose

4. Answer the below questions.

a. At one time, prime and subprime RMBS were traded in separate markets. Why?

The nonagency RMBS market is divided into the private label RMBS market and subprime RMBS

market. Private label RMBS, also referred to as prime or residential deals, are backed by prime

mortgage loans; subprime RMBS are backed by subprime loans and prior to 2007 commonly

b. Why after 2007 are prime and subprime RMBS treated as one asset type?

5. Answer the below questions.

a. What is meant by a senior-subordinated structure?

A senior-subordinated structure refers to a structure that is created with two general categories of

bond classes: a senior bond class and subordinated bond classes.

b. Why is the senior-subordinated structure a form of credit enhancement?

Credit enhancement is the process of reducing credit risk by requiring collateral, insurance, or

other agreements to provide the lender with reassurance that it will be compensated if the

within the structure. For example, the senior bond class is being protected against losses by the

subordinated bond class.

We can compare what is being done to distribute credit risk in a nonagency MBS with what is

done in an agency CMO. In an agency CMO, there is no credit risk for Ginnie Mae issued

structures and the credit risk of the loan pool for Fannie Mae and Freddie Mac issued structure is

6. Calculate the Excess Spread with the following information:

Weighted Average Interest Rate: 10%

7. Answer the below questions.

a. What is the difference between credit tranching and prepayment tranching?

Credit tranching refers to redistributing credit risk among bond classes in the structure, while

prepayment tranching refers to redistributing prepayment risk among bond classes.

b. Why would there be both types of tranching in a nonagency deal but only one type of

tranching in an agency deal?

8. Answer the below questions.

a. What is meant by conditional default rate and cumulative default rate?

The conditional default rate (CDR) is the annualized value of the unpaid principal balance of

newly defaulted loans over the course of a month as a percentage of the unpaid balance of the

pool (before scheduled principal payment) at the beginning of the month.

333333.0

000,100000,000,1

000,30 =

−

=

t

MMD

Then, this is annualized as follows to get the CDR:

33424.0)0333333.01(1 12 =−−=

t

CDR

, which is about 33.42%

9. Why was the PSA Standard Default curve introduced?

A standardized benchmark for default rates was formulated by the Public Securities Association

(PSA). The PSA standard default assumption (SDA) benchmark gives the annual default rate for

a mortgage pool as a function of the seasoning of the mortgages. As with the PSA prepayment

Commented [SC1]: I can’t get in the equation, but the answer

should be 0.03333333

10. Why might an interest rate derivative such as an interest rate swap or interest rate cap

be used in a securitization transaction for residential mortgage loans?

Securitization is the process of taking an illiquid asset, or group of assets, and through financial

engineering, transforming them into a security. There are standard mechanisms for providing credit

enhancement in nonagency MBS. When prime loans are securitized, the credit enhancement

11. Why is a shifting interest mechanism included in a securitization where the collateral is

residential mortgage loans?

Almost all existing senior-subordinated structures backed by residential mortgage loans also

incorporate a shifting interest mechanism. This mechanism redirects prepayments disproportionately

12. Suppose that for a securitization with a shifting interest mechanism, you are given the

following information for some month:

subordinate interest = 30%

shifting interest percentage = 75%

regularly scheduled principal payment = $2,000,000

prepayments = $1,200,000

a. What is the senior prepayment percentage for the month?

The prospectus will specify how different scheduled principal payments and prepayments will be

allocated between the senior bond class and the subordinate bond class. The scheduled principal

payments are allocated based on the senior percentage. The senior percentage, also called the

b. How much of the $2,000,000 regularly scheduled principal payment is distributed to the

senior class?

0.70($2,000,000) = $1,400,000. Thus, the subordinate bond class will get 0.30($2,000,000) =

$600,000 (or the difference of $2,000,000 – $1,400,000 = $600,000).

c. How much of the $1,200,000 is distributed to the senior class?

then 0.9250($1,200,000) = $1,110,000 is allocated to the senior bond class. The subordinate

bond class will get the remainder of $1,200,000 – $1,110,000 = $90,000.

13. What kind of provisions allow for the reduction in credit support over time in a

securitization?

classes are diverted to the senior bond class if a trigger is reached. The diversion of principal

varies from issuer to issuer. The most conservative approach is to stop all principal payments

from being distributed to the subordinate bond classes. Alternatively, some issuers allow the

subordinate bond classes to receive regularly scheduled principal (amortization) on a pro rata

basis but divert all prepayments to the senior bond class.

14. What is meant by the prospectus prepayment curve?

First, we note that repayments are measured in terms of the conditional prepayment rate (CPR).

Borrower characteristics and the seasoning process must be kept in mind when trying to assess

pre-payments for a particular deal. In the prospectus of an offering, a base-case prepayment

assumption is made—the initial speed and the amount of time until the collateral is expected to

©2013 Pearson Education

307

comparisons among deals can be difficult because PPC may be defined differently in each

security’s prospectus.

15. Answer the below questions.

a. What is meant by an involuntary prepayment?

In regards to the reporting of nonagency RMBS, once a loan moves from the delinquent category

to the default category, the borrower loses possession of the property and the mortgage servicer

takes possession with the purpose of selling the property. The proceeds received by the servicer

b. Why is the distinction between a voluntary and involuntary prepayment important in

nonagency RMBS?

16.When will a mortgage servicer not advance payments for principal and interest?

©2013 Pearson Education

308

Because a property’s projected recovered principal depends on its current LTV, servicers

typically cease advancing on loans where the current LTV is greater than a specified threshold.

17. Why does the treatment of modified loans in a nonagency RMBS deal impact the bond

classes?

A modified loan is one in which the terms have been altered in order to help the borrower satisfy

the monthly mortgage obligation. Prior to the problems in the market, deal transactions gave the

18. There are some mortgage loans that are balloon loans. This means that when the loan

matures, there is a mortgage balance that will require financing. It is the responsibility of

the borrower to obtain the refinancing. What is the added risk associated with a pool of

loans backed by balloon loans?

A balloon loan is a long-term loan, often a mortgage, which has one large payment (the balloon

payment) due upon maturity. A balloon loan will often have the advantage of very low interest

payments, thus requiring very little capital outlay during the life of the loan. Since most of the

19. Suppose that the loans in the collateral pool for a nonagency RMBS deal have a floating

rate. What is the risk associated with issued fixed-rate bond classes?

©2013 Pearson Education

309

loans in the collateral pool for a nonagency RMBS deal have a floating rate and the bond classes

are fixed rate. The risk can be handled by interest rate derivatives such as interest rate swaps and

interest rate caps. While these are often employed in nonagency RMBS structures, they are not

allowed in agency RMBS structures. Since we do not cover interest rate derivatives until later

chapters, we merely point out for now that they are used when there is a mismatch between the

character of the cash flows for the loan pool and the character of the cash payments that must be

made to the bond classes.

20. What is the concern with the inclusion of fixed-rate mortgage loans in the collateral

pool when the liabilities are floating rate?

21. An interest rate cap allows the buyer of the cap to be compensated if interest rates rise

above a reference rate. The buyer has to pay a periodic premium to obtain this protection.

When an RMBS transaction has a pool of floating-rate loans, what type of protections does

an interest rate cap provide?