Chapter 13 – Equity Valuation

CHAPTER 13

EQUITY VALUATION

1. Theoretically, dividend discount models can be used to value the stock of rapidly

growing companies that do not currently pay dividends; in this scenario, we would be

2. It is most important to use multi-stage dividend discount models when valuing

companies with temporarily high growth rates. These companies tend to be companies

3. The intrinsic value of a share of stock is the individual investor’s assessment of the true

worth of the stock. The market capitalization rate is the market consensus for the

4. Intrinsic value = V0 = D1

1 + k + D2

(1 + k)2 + … + DH + PH

(1 + k)H

5. Intrinsic value = V0 = D0× (1 + g)

k - g :

6. Intrinsic value = V0 = D0× (1 + g)

8. Market value of the firm

= Market value of assets – Market value of debts

9. g = ROE b = 0.10 0.6 = 0.06 or 6%

P/E = 1 - b

k - g = 1 - 0.6

0.08 - 0.06 = 20

11. Given EPS = $6, ROE = 15%, plowback ratio = 0.6, and k = 10%, we first calculate the

price with the constant dividend growth model:

12. FCFF = EBIT(1 – tc) + Depreciation – Capital expenditures – Increase in NWC

13. FCFE1 = FCFF – Interest expenses(1 – tc) + Increases in net debt

Chapter 13 – Equity Valuation

14. Cost of equity = rf + E(Risk premium) = 7% + 4% = 11%

Because the dividends are expected to be constant every year, the price can be

calculated as the no-growth-value per share:

15. k = rf + β [E(rM) – rf ] = 0.05 + 1.5 (0.10 – 0.05) = 0.125 or 12.5%

16.

a. False. Higher beta means that the risk of the firm is higher and the discount rate

applied to value cash flows is higher. For any expected path of earnings and

cash flows, the present value of the cash flows, and therefore, the price of the

firm will be lower when risk is higher. Thus the ratio of price to earnings will be

lower.

a. Using the constant-growth DDM, P0 = D1

k - g :

18. ROE = 20%, b = 0.3, EPS = $2, k = 12%

a. P/E Ratio

We can calculate the P/E ratio by dividing the current price by the projected

earnings:

b. Present Value of Growth Opportunities (PVGO)

g = ROE b = 0.20 0.3 = 0.6

g = ROE b = 0.20 0.2 = 0.04 = 4%

D1 = EPS (1 – b) = $2 (1 – 0.2) = $1.6

19. ROE = 16%, b = 0.5, EPS = $2, k = 12%

a. P0 = D1

k - g =EPS × (1-b)

k - (ROE × b) = $2 × (1 - 0.5)

0.12 - 0.16 × 0.5 = $1

0.12 - 0.08 = $25

20.

a. k = rf + β [E(rM) – rf ] = 0.06 + 1.25 (0.14 – 0.06) = 0.16 or 16%

g = ROE b = 0.09 (2/3) = 0.06 or 6%

Chapter 13 – Equity Valuation

b. Leading P0/E1 = $10.60/$3.18 = 3.33

c. PVGO = P0 – E1

k = $10.60 – $3.18

0.16 = $9.28

d. Now, you revise the plowback ratio in the calculation so that b = 1/3:

g = ROE b = 0.09 1/3 = 0.03 or 3%

e. V0 increases because the firm pays out more earnings instead of reinvesting

21. FI Corporation

22. Nogro Corporation

a. D1 = E1 (1 – b) = $2 0.5 = $1

Therefore:

Chapter 13 – Equity Valuation

b. Since k = ROE, the NPV of future investment opportunities is zero:

c. Since k = ROE, the stock price would be unaffected if Nogro were to cut its

d. Again, if Nogro eliminated the dividend, this would have no impact on Nogro’s

23. Xyrong Corporation

a. k = rf + β [E(rM) – rf ] = 0.08 + 1.2 (0.15 – 0.08) = 0.164 or 16.4%

b. P1 = V1 = V0 (1 + g) = $101.82 (1 + 0.12) = $114.04

24. Before-tax cash flow from operations $2,100,000

Depreciation 210,000

Taxable income 1,890,000

The value of the firm (i.e., debt plus equity) is:

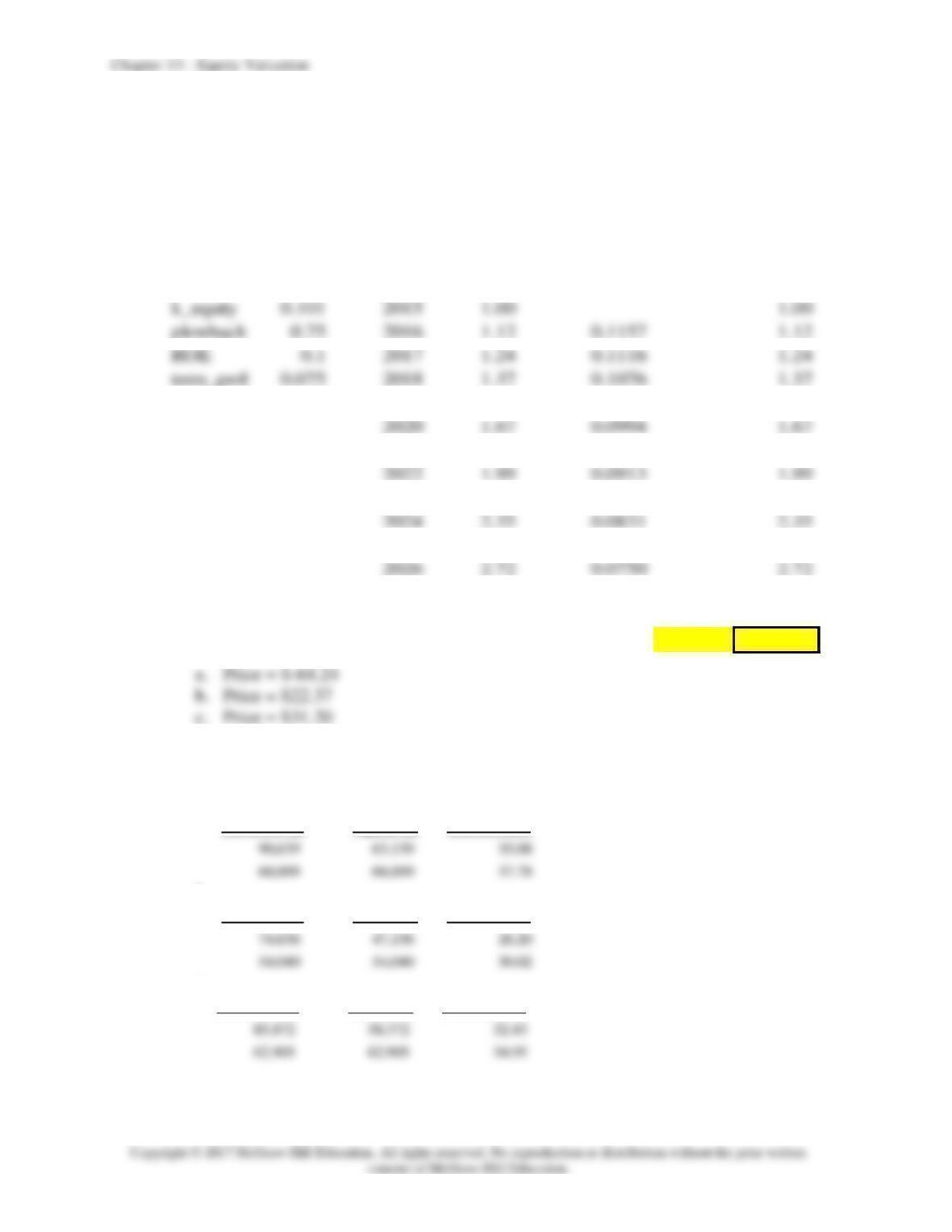

25. Use this spreadsheet for all answers (Chart output taken directly from spreadsheet.

Answers reflect each scenario change).

Inputs

Year Dividend Div growth

Term

value

Investor

CF

beta 0.9

2012 0.72 0.72

mkt_prem

0.08

2013 0.81 0.81

rf 0.029

2014 0.91 0.91

2015 1.00 1.00

2016 1.12 0.1157 1.12

2017 1.24 0.1116 1.24

2018 1.37 0.1076 1.37

2019 1.52 0.1035 1.52

2020 1.67 0.0994 1.67

2021 1.83 0.0954 1.83

2022 1.99 0.0913 1.99

2023 2.17 0.0872 2.17

2024 2.35 0.0831 2.35

2025 2.53 0.0791 2.53

2026 2.72 0.0750 2.72

2027 2.93 0.0750 120.96 123.89

Price = $36.79

26. The solutions derived from Spreadsheet 13.2 are as follows:

a.

Intrinsic val Equity val Intrin/share

b.

Intrinsic val Equity val Intrin/share

c.

Intrinsic val Equity val Intrin/share

27.

Chapter 13 – Equity Valuation

a. g = ROE b = 0.20 0.5 = 0.10 or 10%

b.

Time

EPS

Dividend

BVPS

Comment

0

$1.0000

$0.5000

$5.5000

Book Value Per Share is $5.5.

1

$1.1000

$0.5500

$6.0500

g = 10%, plowback = 0.50

payout ratio = 0.60

15% (1 – 0.6) = 6% from next year.

(Because the market is unaware of the changed competitive situation, it believes

the stock price should grow at 10% per year.)

P2 = D3

k - g = $0.5881

0.15 - 0.06 = $6.5340 after the market becomes aware of the

d.

Year

Return

55.0$)11$10.12($ ==

+−

e.

Year

Return

CFA 1

Chapter 13 – Equity Valuation

Answer:

a. This director is confused. In the context of the constant growth model, it is true

that price is higher when dividends are higher holding everything else (including

CFA 2

Answer:

a. It is true that NewSoft sells at higher multiples of earnings and book value than

Capital. But this difference may be justified by NewSoft’s higher expected

b. The most important weakness of the constant-growth dividend discount model in

CFA 3

Answer:

a. The industry’s estimated P/E can be computed using the following model:

P0/E1 = payout ratio/(r − g)

Therefore:

Chapter 13 – Equity Valuation

Chapter 13 – Equity Valuation

b.

i. Forecast growth in real GDP would cause P/E ratios to be generally higher

for Country A. Higher expected growth in GDP implies higher earnings

growth and a higher P/E.

CFA 4

Answer:

a. k = rf + β [E(rM) – rf ] = 0.045 + 1.15 (0.145 − 0.045) = 0.16 or 16%

b. Year Dividends

2013 $1.72

Present value of dividends paid in years 2014 to 2016:

Year PV of Dividends

2013 $1.93/1.16 = $1.66

c. The table presented in the problem indicates that QuickBrush is selling below

intrinsic value, while we have just shown that SmileWhite is selling somewhat

above the estimated intrinsic value. Based on this analysis, QuickBrush offers

Chapter 13 – Equity Valuation

d. Strengths of two-stage DDM compared to constant growth DDM:

• The two-stage model allows for separate valuation of two distinct periods in

a company’s future. This approach can accommodate life cycle effects. It

also can avoid the difficulties posed when the initial growth rate is higher

than the discount rate.

CFA 5

Answer:

a. The value of a share of Rio National equity using the Gordon growth model and

the capital asset pricing model is $22.40, as shown below.

Calculate the required rate of return using the capital asset pricing model:

b. The sustainable growth rate of Rio National is 9.97%, calculated as follows:

g = ROE × b = ROE × Retention Rate = ROE × (1 – Payout Ratio)

CFA 6

Answer:

a. To obtain free cash flow to equity (FCFE), the two adjustments that Shaar

should make to cash flow from operations (CFO) are:

Chapter 13 – Equity Valuation

b. Note 1: Rio National had $75 million in capital expenditures during the year.

Adjustment: Negative $75 million

Note 2: A piece of equipment that was originally purchased for $10 million was

sold for $7 million at year-end, when it had a net book value of $3 million.

Equipment sales are unusual for Rio National.

Note 3: The decrease in long-term debt represents an unscheduled principal

repayment; there was no new borrowing during the year.

Note 4: On 1 January 2015, the company received cash from issuing 400,000

shares of common equity at a price of $25.00 per share.

No adjustment

Note 5: A new appraisal during the year increased the estimated market

value of land held for investment by $2 million, which was not recognized

Chapter 13 – Equity Valuation

c. Free cash flow to equity (FCFE) is calculated as follows:

FCFE = NI + NCC – FCINV – WCINV + Net borrowing

where NCC = non-cash charges

FCINV = investment in fixed capital

WCINV = investment in working capital

Million $

Explanation

NI =

$30.16

From Table 13.6

NCC =

+$67.17

FCINV =

$75.00 (capital expenditures from Note 1)

Net Borrowing =

FCFE =

$71.17 (depreciation and amortization from Table 13.6)

CFA 7

Answer:

Rio National’s equity is relatively undervalued compared to the industry on a P/E-to–

growth (PEG) basis. Rio National’s PEG ratio of 1.33 is below the industry PEG ratio

of 1.66. The lower PEG ratio is attractive because it implies that the growth rate at Rio

National is available at a relatively lower price than is the case for the industry. The

PEG ratios for Rio National and the industry are calculated below:

Rio National

Chapter 13 – Equity Valuation

CFA 8

Answer:

Using a two-stage dividend discount model, the current value of a share of Sundanci is

calculated as follows:

where:

E0 = $0.952

D0 = $0.286

E1 = E0 (1.32)1 = $0.952 1.32 = $1.2566

CFA 9

Answer:

a. Free cash flow to equity (FCFE) is defined as the cash flow remaining after

meeting all financial obligations (including debt payment) and after covering

capital expenditure and working capital needs. The FCFE is a measure of how

much the firm can afford to pay out as dividends, but in a given year may be

more or less than the amount actually paid out.

Chapter 13 – Equity Valuation

b. The FCFE model requires forecasts of FCFE for the high growth years (2017

and 2018) plus a forecast for the first year of stable growth (2019) in order to

allow for an estimate of the terminal value in 2015 based on perpetual growth.

The following table shows the process for estimating Sundanci’s current value

on a per share basis:

Free Cash Flow to Equity

Base Assumptions

Shares outstanding: 84 millions

Required return on equity (r): 14%

Actual

2016

Projected

2017

Projected

2018

Projected

2019

Growth rate (g)

27%

27%

13%

Total

Per share

Earnings after tax

$80

$0.952

$1.2090

$1.5355

$1.7351

Terminal value

Discounted value

$40.7859****

* Projected 2015 Terminal value = (Projected 2016 FCFE)/(r − g)

** Projected 2015 Total cash flows to equity

c. i. The following limitations of the dividend discount model (DDM) are

addressed by the FCFE model. The DDM uses a strict definition of cash flows

to equity, i.e. the expected dividends on the common stock. In fact, taken to its

Chapter 13 – Equity Valuation

needs have been met. Thus the FCFE model explicitly recognizes the firm’s

investment and financing policies as well as its dividend policy. In instances of

a change of corporate control, and therefore the possibility of changing dividend

policy, the FCFE model provides a better estimate of value. The DDM is biased

ii. The following limitations of the DDM are not addressed by the FCFE model.

Both two-stage valuation models allow for two distinct phases of growth, an

initial finite period where the growth rate is abnormal, followed by a stable

growth period that is expected to last indefinitely. These two-stage models share

the same limitations with respect to the growth assumptions. First, there is the

difficulty of defining the duration of the extraordinary growth period. For

example, a longer period of high growth will lead to a higher valuation, and

there is the temptation to assume an unrealistically long period of extraordinary

CFA 10

Answer:

a. The formula for calculating a price earnings ratio (P/E) for a stable growth firm

is the dividend payout ratio divided by the difference between the required rate

of return and the growth rate of dividends. If the P/E is calculated based on

trailing earnings (year 0), the payout ratio is increased by the growth rate. If the

P/E is calculated based on next year’s earnings (year 1), the numerator is the

payout ratio.

P/E on trailing earnings:

Chapter 13 – Equity Valuation

b. The P/E ratio is a decreasing function of riskiness; as risk increases the P/E ratio

decreases. Increases in the riskiness of Sundanci stock would be expected to

lower the P/E ratio.