Chapter 11 – Managing Bond Portfolios

CHAPTER ELEVEN

MANAGING BOND PORTFOLIOS

CHAPTER OVERVIEW

This chapter discusses active- and passive- bond-portfolio-management strategies. Much of the

chapter is devoted to explaining interest rate risk management. The concept and use of duration

are explained, as are several types of portfolio immunization strategies utilizing duration. In

addition, various active strategies, or bond swaps, are described.

LEARNING OBJECTIVES

After studying this chapter, the student should have an understanding of duration, modified

duration and convexity. He or she should be able to calculate duration and should understand

how to construct an immunized portfolio. The student should also understand active bond

portfolio management, from the concept of interest-rate predictions, and exploit mispriced bonds.

CHAPTER OUTLINE

The basic decision involved in fixed-income management is the decision to purse an active- or a

passive- investment strategy. An active strategy seeks to earn superior returns from the fixed-

income portfolio. Superior returns can be earned if the investor can predict interest-rate

movements that are not currently incorporated into a bond’s price or if the investor can identify

1. Interest Rate Risk

PPT 11-2 through PPT 11-13

As interest rates rise and fall, bondholders experience capital gains and losses and changes in the

1. Inverse relationship between bond price and interest rates (or yields)

2. Long-term bonds are more price sensitive than short–term bonds. There are some exceptions

to this rule because deep discount bonds can have a lower duration at longer maturities. This

is pretty much a math quirk and won’t be true for most traded bonds.

5. Sensitivity of a bond’s price to a change in its yield is inversely related to the yield to

maturity at which the bond currently is selling. At higher yield rates the present values of the

6. An increase in a bond’s yield to maturity results in a smaller price decline than the gain

associated with a decrease in yield. This is an characteristic of convexity. Because the bond-

1. Any security that gives an investor more money back sooner (as a % of investment) will

have lower price volatility when interest rates change.

3. It is not the only factor; in particular the coupon rate and the current ytm are also major

determinants.

Be careful not to equate lower price volatility with lower interest-rate risk. Interest-rate risk is

reduced by minimizing the difference between the duration of the bond portfolio and the

investor’s investment horizon and not necessarily by reducing the duration or the price volatility.

Duration is the first derivative of the bond-price formula with respect to interest rates. The

description of duration used here stresses the concept of average life. Since the measurement of

Duration can be used to predict the price change of a coupon bond when interest rates change

because price changes on fixed-income securities are approximately proportional to duration.

Duration incorporates both the coupon rate and maturity effects on price volatility into a single

measure. The concept of modified duration is used extensively in the industry.

Chapter 11 – Managing Bond Portfolios

D* = D / (1+y)

P/P = – D* x y

The minus sign in this equation reminds us that if interest rates go up, prices go down and vice

versa. Although the text simplifies this you have to be careful using modified duration. It is used

for instruments that have non-annual cash flows as follows:

2. Passive Bond Management

PPT 11-14 through PPT 11-19

Interest-rate risk is the possibility that an investor does not earn the promised ytm because of

interest rate changes. A bond investor faces two types of interest-rate risk:

1. Price risk: The risk that an investor cannot sell the bond for as much as anticipated. An

increase in interest rates reduces the sale price.

The two types of risk are potentially offsetting because if interest rates rise, the sale price will

fall but the reinvestment income will be higher and vice versa. If one could choose just the right

amount of price volatility to offset the change in the future value of the reinvestment income one

could eliminate interest-rate risk. This is the concept of ‘immunization.’

Immunization of interest-rate risk is a tool that can be used for a type of passive management.

Immunization is an investment strategy designed to ensure the investor earns the promised ytm.

Financial institutions use immunization to minimize risk to their rate of return on investments.

Chapter 11 – Managing Bond Portfolios

There are some problems with immunization strategies:

1. May be suboptimal if you have a rate forecast and are willing to take a position on which

way rates will move. If you think rates will fall you want a duration longer than your

2. Does not work as well for complex portfolios with option components, nor for large

interest rate changes

3. Convexity

PPT 11-20 through PPT 11-21

Chapter 11 – Managing Bond Portfolios

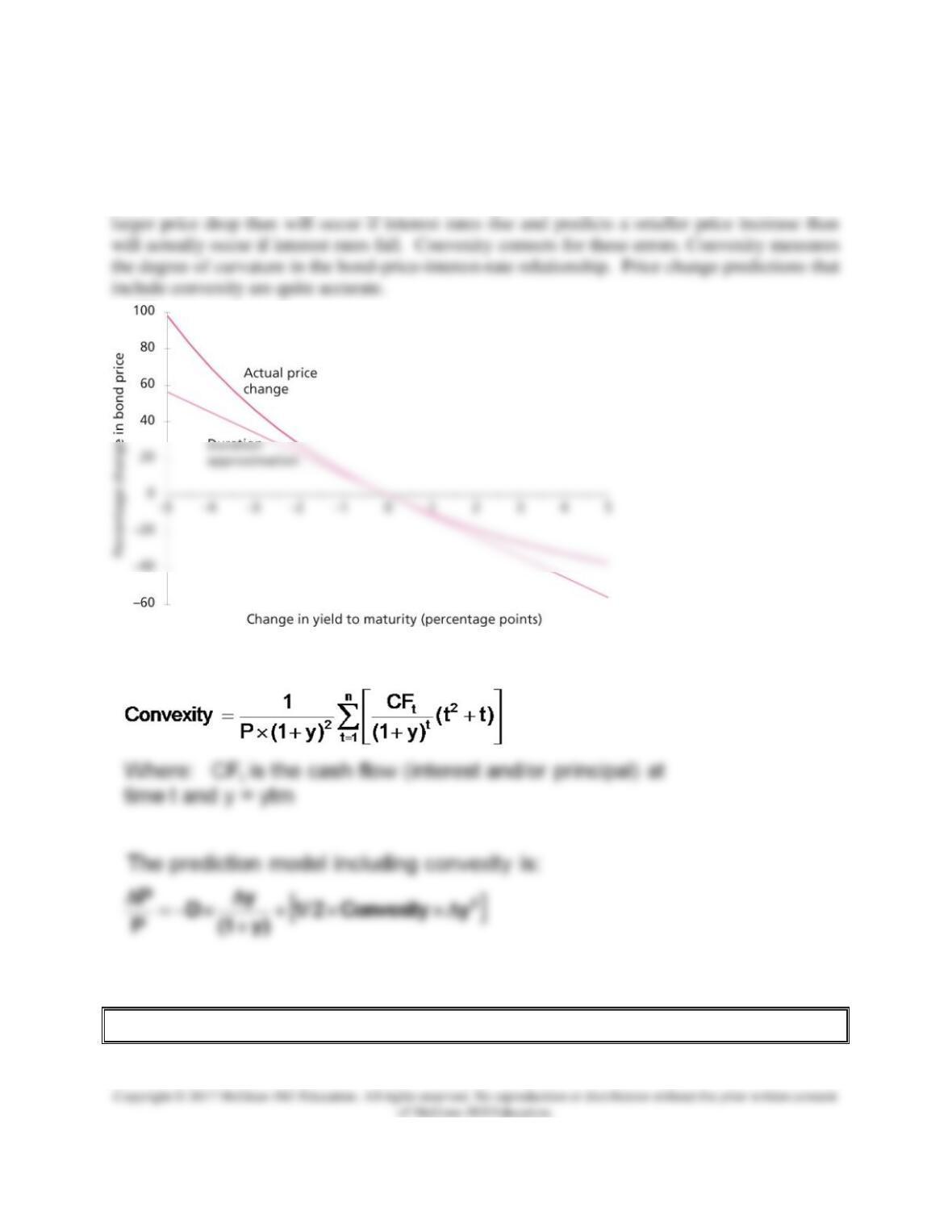

Because duration is the first derivative of the bond-price formula, its price change predictions

strictly hold only for infinitesimally small interest-rate changes. For larger interest-rate changes,

duration predictions will be wrong. The duration prediction is always pessimistic. It predicts a

The convexity formula and the predicted P/P formula with convexity are:

4. Active Bond Management

PPT 11-22 through PPT 11-23

Chapter 11 – Managing Bond Portfolios

Several active bond strategies are presented. Various bond swaps may be instituted when the

fixed-income portfolio is being actively managed. Substitution, intermarket spread and rate

anticipation swaps require some level of market disequilibrium. With a substitution swap, two

bonds that are substitutes offer different rates of return. The strategy involves purchase of the

bond that is offering the higher rate of return and selling the bond that has the lower rate of

return.

Excel Applications

Two excel spreadsheets for this chapter are available on the website. The first spreadsheet

provides a template for students to calculate convexity. The second model is constructed to

apply the concept of time-period immunization. It is built to demonstrate how price and interest-